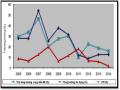

It can be seen that Vietcombank's ratio of bad debt provision to total outstanding loans is the highest compared to some other banks, and has always been the leader in the period 2010-2014, showing caution in assessing loans. and make reasonable provisions.

Besides, we also need to look at the growth in provision for bad debts (on the income statement) along with the growth in customer loans in the same period to better understand the nature of the bad debt provision growth, because these two items affect each other. Accordingly, Vietcombank's credit growth was the lowest compared to the banks selected in the table below, and the growth in provision for bad debts was correspondingly lower, demonstrating Vietcombank's caution in lending in the period of 2008. 2013 compared to other banks. The other banks' lending growth was hotter, and provisioning was also much higher.

Table 3.10: Customer loan growth

Unit: %

| 2008 | 2009 | 2010 | 2011 | 2012 | two thousand and thirteen | 2014 |

| CTG 18.16% | 35.13% | 43.53% | 25.29% | 13.61% | 12.88% | 16.90% |

| VCB 15.65% | 25.56% | 24.85% | 18.44% | 15.16% | 13.74% | 17.87% |

| BIDV 21.97% | 28.21% | 23.15% | 15.64% | 15.65% | 15.04% | 13.98% |

| STB -1.04% | 70.41% | 38.27% | -2.36% | 19.61% | 14.77% | 15.78% |

| MBB 44.44% | 80.49% | 67.31% | 28.33% | 26.81% | 18.44% | 14.09% |

| EIB 15.07% | 80.77% | 62.44% | 19.76% | 0.44% | 11.15% | 4.55% |

Maybe you are interested!

-

Improved Competitiveness And Provision Of Banking Services To Better Meet The Needs Of The Economy

Improved Competitiveness And Provision Of Banking Services To Better Meet The Needs Of The Economy -

Impact Of Loan Portfolio On The Risk Of Joint Stock Commercial Bank

Impact Of Loan Portfolio On The Risk Of Joint Stock Commercial Bank -

Research on the impact of loan portfolios on profitability of joint stock commercial banks - 7

Research on the impact of loan portfolios on profitability of joint stock commercial banks - 7 -

Traditional Concentrations Of The Hirshmann-Herfindahl Index (Hhi):

Traditional Concentrations Of The Hirshmann-Herfindahl Index (Hhi): -

Check The Suitability Of The Selected Regression Model

Check The Suitability Of The Selected Regression Model -

Orientation To Improve Loan Portfolio Management Activities At Vietnamese Joint Stock Commercial Banks

Orientation To Improve Loan Portfolio Management Activities At Vietnamese Joint Stock Commercial Banks

| SCB 19.51% | 34.51% | 5.96% | 0.00% | 0.00% | 0.96% | 50.58% |

| ACB 9.50% | 79.02% | 38.95% | 17.60% | 0.90% | 4.26% | 7.39% |

| SHB 49.46% | 105.17% | 90.01% | 19.63% | 95.78% | 33.76% | 36.13% |

| TECHCOMBANK 0.00% | 0.00% | 25.74% | 19.88% | 7.58% | 2.95% | 14.28% |

| MSB -100.0% | 0.00% | 0.00% | 18.61% | -23.33% | -5.30% | -100.0% |

| HDBANK 0.00% | 33.28% | 42.49% | 18.07% | 52.70% | 108.25% | -4.64% |

| DONGA 43.59% | 34.35% | 11.54% | 14.83% | 15.11% | 4.74% | -100.0% |

| ABB -100.0% | 0.00% | 0.00% | 0.00% | 0.00% | 26.08% | 9.82% |

| OCEAN 26.00% | 71.57% | 73.04% | 8.83% | 36.76% | 8.54% | 0.00% |

| PNB 62.40% | 107.40% | 58.03% | 13.02% | 23.47% | -0.22% | 0.00% |

| MDB 0.00% | 77.95% | 13.10% | 18.22% | 16.66% | 5.45% | 0.00% |

| OCB 13.76% | 18.84% | 35.52% | 27.76% | -100.0% | 0.00% | 0.00% |

| VIETNAM 0.00% | 81.55% | -100.0% | 0.00% | 0.00% | 28.94% | 0.00% |

| MHB 15.69% | 24.98% | 12.38% | 1.44% | 7.39% | 9.09% | 0.00% |

| KIENLONGBANK 0.00% | 122.03% | 43.78% | 19.91% | 15.23% | 25.25% | 0.00% |

| PGBANK 0.00% | 0.00% | -100.0% | 0.00% | 13.83% | 0.58% | 0.00% |

| NAMAs 0.00% | 0.00% | 0.00% | 17.97% | 9.48% | 69.24% | 0.00% |

| VIETCAPITAL 23.37% | -100.0% | 0.00% | 19.59% | -100.0% | 0.00% | 0.00% |

| SGBANK 0.00% | 20.98% | -100.0% | 0.00% | 0.00% | -1.53% | 5.26% |

| BAOVIETBANK 0.00% | 0.00% | 186.03% | 7.25% | 103.12% | -100.0% | 0.00% |

Table 3.11: Growth in provision for bad debts

Unit: %

| 2009 | 2010 | 2011 | 2012 | two thousand and thirteen | |

| CTG | -54.90% | 415.80% | 62.10% | -11.10% | -5.40% |

| EIB | -57.20% | 93.70% | 2.20% | -11.70% | 25.50% |

| MBB | 64.30% | 49.90% | 17.40% | 216.20% | -6.40% |

| ACB | 226.70% | -20.90% | 30.30% | 75.90% | -8.20% |

| STB | 281.20% | 12.50% | 24.30% | 237.10% | -67.40 % |

| SHB | 485.10% | 44.60% | -32.90% | -656.20% | -77.30% |

| VCB | -60.30% | 75.50% | 150.90% | -4.20% | 6.50% |

Source: Author's own calculation 3.5 Assessment of the current situation of the loan portfolio 3.5.1 Achievements - Joint-stock commercial banks basically share the same target market, almost none of them specialize. . Banks have diversified their loan portfolios, allocating their loan capital sources in many fields of industry, customers, loan term... - The loan structure of banks is basically is consistent with the target market of joint stock commercial banks and the development trend of the multi-sector economy in Vietnam.

- From the current situation, the loan portfolio is considered to reflect the management of the loan portfolio at banks. Through the current situation of the loan portfolio presented, it shows that banks have begun to focus on loan portfolio management. A number of joint stock commercial banks have planned targets and developed policies related to loan portfolio management, initially orienting the formation and development of a proactive loan portfolio for banks. Joint Stock Commercial Banks have developed policies to implement the loan portfolio. The year 2005 is considered an important starting year in the implementation of regulations on risk management in accordance with international practices in Vietnam. In that spirit, the State Bank of Vietnam has issued two important documents with orientation for risk management in Vietnam,that is Decision No. 493/QD-NHNN dated 22/4/2005 and Decision 457/QD-NHNN dated 19/4/2005. Based on these documents, banks have developed policies including: lending limit policy, debt classification and provisioning policy, lending restriction policy for certain subjects. Specifically… These are policies to limit the risk of concentration on the portfolio, so they are important in guiding the implementation of loan portfolio management at each joint stock commercial bank. In addition, a small number of joint stock commercial banks have operated an internal credit rating system, creating a premise for the risk assessment process in general and loan portfolio risk in particular.policy of debt classification and provisioning, policy of restricting lending to a number of specific subjects... These are policies to limit the risk of concentration on the portfolio, so they are important in the orientation of implementation of loan portfolio management at each joint stock commercial bank. In addition, a small number of joint stock commercial banks have operated an internal credit rating system, creating a premise for the risk assessment process in general and loan portfolio risk in particular.policy of debt classification and provisioning, policy of restricting lending to a number of specific subjects... These are policies to limit the risk of concentration on the portfolio, so they are important in the orientation of implementation of loan portfolio management at each joint stock commercial bank. In addition, a small number of joint stock commercial banks have operated an internal credit rating system, creating a premise for the risk assessment process in general and loan portfolio risk in particular.creating a premise for the risk assessment process in general and loan portfolio risk in particular.creating a premise for the risk assessment process in general and loan portfolio risk in particular.

3.5.2 Existence - The level of diversification on the portfolio is not high, most banks mainly lend to about 3-4 similar industries.

- The level of concentrated risk is quite clear, showing that the ratio of outstanding loans of an industry to the total outstanding loans of the entire portfolio can be at most 30% to 40%, especially over 50% of total outstanding loans. In addition, the debt balance of some industries on the portfolio is many times larger (2 times even up to 4 times) compared to the equity level at the same time. In the opinion of the Basel Committee, when any single risk/risk group has the potential to create a loss large enough relative to a bank's capital, assets or total loss, it is considered a risk. concentrate.

- Most of the joint stock commercial banks have not implemented loan portfolio management, a few are passively managed, so the level of stability is low, and they are easily affected by market demand in portfolio formation. Through fact-finding, most of the Vietnamese joint stock commercial banks are only interested in the management of each loan transaction, not applying the loan portfolio management. Only a few large-scale commercial joint stock banks apply the passive portfolio management method. Expressed in the annual plans of these banks, there are general orientations/priority orientations in the implementation of loans. Most of the joint stock commercial banks have not established a loan portfolio with the expected structure, nor have the necessary limits established for each industry/business area/type of credit extension. used in accordance with the characteristics of the bank. Therefore,The structure of the bank's loan portfolio is unavoidable, spontaneous, the proportion of different types of loans is randomly formed and is led by the market.

- The organizational structure at joint stock commercial banks is not really suitable with the requirements of portfolio risk management in particular and loan portfolio management in general. Some banks have not established an independent risk management department, but only a risk management department, which is more inclined to deal with symptoms that have already occurred, not focusing on identification and measurement issues. and control portfolio risk before lending decision. For example, Kien Long bank, Dai A bank, Nam Viet bank, Pioneer bank... all have a risk management department but no risk management department.

- Banks have not built an internal risk measurement model, so it is difficult to accurately quantify portfolio risk to apply appropriate management measures. An important content in active loan portfolio management is the application of the portfolio risk measurement model, so the application of the risk measurement model is becoming a popular development trend in commercial banks. many countries in the world. However, in Vietnam, these models are still quite strange. In practice, Vietnamese banks measure risk according to the provisions of Decision 493 of the State Bank, on that basis, make provisions for both estimated and unestimated risks.

3.6 Causes of existence

- A few banks tend to follow profitsIn the short term, unsustainable, affecting the effectiveness of loan portfolio management As pointed out in the current situation of loan portfolios, the lack of diversification and concentration of risks on the portfolios of some banks. Commercial joint stock goods show quite clearly. In addition to the reason of not being fully aware of the need for loan portfolio management, there has not been an appropriate portfolio management method, here it is not excluded that the cause comes from the tendency to pursue immediate profits. of some members of the Board of Directors and the Board of Directors of the bank, even with negative morals, deliberately lending beyond the allowable limit. Although the Law on Credit Institutions stipulates legal safety limits (for lending up to one customer/group of customers),However, in practice there is still a violation of these regulations (as pointed out in the limitations of loan portfolio management). These phenomena are considered serious violations of loan portfolio management, which may stem from the moral hazard of the Board of Directors, from manipulation and excessive interference in lending activities. of some members of the Board of Directors. The root cause of this situation can be traced back to the "cross-ownership" relationship between banks and enterprises and economic groups, which has been quite popular in the Vietnamese economy in recent years.interfere too deeply in the lending activities of some members of the Board of Directors. The root cause of this situation can be traced back to the "cross-ownership" relationship between banks and enterprises and economic groups, which has been quite popular in the Vietnamese economy in recent years.interfere too deeply in the lending activities of some members of the Board of Directors. The root cause of this situation can be traced back to the "cross-ownership" relationship between banks and enterprises and economic groups, which has been quite popular in the Vietnamese economy in recent years.

- Bank leaders are not fully aware of loan portfolio management in the modern economy.

This can also be explained by the fact that Vietnamese banks have long been used to managing each loan transaction and are not aware of loan portfolio management. On the other hand, in the context that the economy is developing strongly, the concentration of risks on the loan portfolio will be masked by the growth of the local/regional economy.

Banks' profits can be greatly enhanced by lending (as was the case with Vietnamese commercial banks in 2006 and 2007) and short-term success (or at least not yet failure). burden) leads banks to believe that such governance is effective. However, entering 2008 when the economy showed signs of recession, the bad consequences of risk concentration became clear. The lack of initiative in loan portfolio management, relying on waiting for signals from the State Bank is not a way to bring good results. In fact, the intervention of the State Bank is often delayed, not keeping up with the happenings. In that context, if any bank is proactive in its strategy, it will avoid troublesome consequences.For example, in 2007 when the State Bank issued Directive 03/2007/CTNHNN and then Decision 03/2008/QD-NHNN on the limit of outstanding loans for securities business, many banks had very difficult to comply with. Because before that, they focused on lending a lot in this field, so when the State Bank suddenly tightened the outstanding loans, many banks became passive, embarrassed to support and could not rule out the possibility of having to pay loans. Executing hastily expanding sales to increase outstanding loans or converting loans to reverse purposes to avoid being considered a violation.Therefore, when the State Bank suddenly tightened the outstanding loans, many banks became passive, embarrassed to support and could not rule out the possibility of having to perform the act of hastily expanding sales to increase outstanding loans or is a loan to convert debt for the purpose of avoiding being considered a violation.Therefore, when the State Bank suddenly tightened the outstanding loans, many banks became passive, embarrassed to support and could not rule out the possibility of having to perform the act of hastily expanding sales to increase outstanding loans or is a loan to convert debt for the purpose of avoiding being considered a violation.

In fact, the lack of awareness among bank administrators about the need for loan portfolio management is also reflected in the allocation of targets to increase outstanding loans for employees, transaction offices, and customers. each bank branch, that is, only focusing on increasing the credit size, not paying attention to the loan portfolio structure.

This leads to uncontrollable level of risk on the forming portfolio and once these potential risks become real losses, the consequences are completely borne by the bank.

- The basic factors for applying the active portfolio management method at joint stock commercial banks are not adequate.

The first thing that can be mentioned is that the information analysis and forecasting work at banks is still weak, leading to difficulties in proactively designing the planned loan portfolio. Weak information analysis leading to inaccurate forecasts are almost inherent limitations of the Vietnamese economy in the transition from a subsidized economy to an integrated open economy. Currently, at commercial banks, the collection of information for credit analysis still has certain limitations. First of all, it is difficult to collect information on economic sectors/sectors to analyze industry risks, serving the internal credit rating process. Currently, there is a CIC (Credit Information Center) under the State Bank that provides information to support the credit department of commercial banks in the credit analysis process.However, the information provided by this organization is often not updated timely, sketchy and in the form of "raw" information that has not been processed, so its benefits to the bank are not high. On the other hand, mainly detailed information about customers, synthesis and forecasts is not available, so it cannot serve the management of the portfolio. These realities have hindered the design of an effective loan portfolio right from the time of planning the lending strategy. Also, due to the poor forecasting, it is easy to have a "get there or go" mentality in the implementation of the loan portfolio. Because it may appear that the information is not accurate, the reliability is not high, if building a loan portfolio with too specific weights, it will lead to continuous adjustment later. So banks usually specify the general direction.It is thought that in order to create conditions for banks to apply the active portfolio management method, it is necessary to improve information forecasting in the economy in general and in the banking system in particular.

Next is the fact that joint stock commercial banks have not yet built and operated well the internal credit rating system as required by the State Bank in Decision 493/QD-NHNN dated 22/4/2005. This is also one of the major technical obstacles for the implementation of loan management in general. Because the internal credit rating system not only provides good support for the management of each loan transaction, but also provides very basic elements to be able to build a quantitative model of portfolio risk, which would otherwise With this model, it would be difficult to implement loan portfolio management. For transaction management, the absence of an internal credit rating system will cause banks to lack a basis to make an accurate decision to approve or deny loans. On the other hand,The bank also has not determined the risk price of each loan to include in the lending interest rate, with the aim of fully covering the expected/expected loss. For loan portfolio management, without an internal credit rating system, the bank would not have the basis to set safe limits on the portfolio, nor build a measurement model. portfolio loss, because of the lack of key inputs such as the probability of default (PD) for each borrower and the loss in default (LGD) rate of each loan, determining the price/fee Loan exchange on the market also has no basis for calculation. Another factor that also hinders the implementation of modern portfolio management methods is that commercial banks, especially small-scale banks, currently lack a fully and scientifically stored database system. ,lack of modern software support for data processing. These factors need to be based on the potential of capital, people and time, so they cannot be easily achieved in a short period of time.

CONCLUSION CHAPTER 3

Through analyzing the current status of the loan portfolio at Vietnamese joint stock commercial banks, chapter 3 has solved the following problem: Analysis of the loan portfolio of Vietnamese joint stock commercial banks in the period from 2004 to 2014 according to different criteria (emphasis on the criterion of portfolio structure by economic sector), thereby indicating signs of diversification, concentration of risk and non-compliance with safety limits. allowed on the loan portfolio of commercial joint stock banks. On the basis of those analyzes, make more in-depth comments and assessments on the loan portfolio management during this time.

CHAPTER 4: RESEARCH METHODS - RESEARCH RESULTS

4.1 Model of the thesis

The thesis inherits the research of Benjamin M. Tabak, DimasM.Fazio and Daniel O.Cajueiro using the profit regression method according to the variables: size of the bank (Bank's size), the ratio of equity to total assets (Equity ratio, EQ), a measure of HHI concentration.

4.1.1 Variables and variable descriptions

The variables used in the research model include: return on total assets (ROA), size of the bank (Bank's size), equity ratio on total assets (Equity ratio, EQ). ), the index measures the concentration of HHI.

4.1.1.1 Return on assets (ROA)

This ratio is calculated by dividing the bank's net profit (or profit after tax) during the reporting period by the average of the bank's total assets for the same period. The figure for net profit or profit before tax is taken from the income statement. The asset value is taken from the balance sheet.

The value of net profit is taken from the market value and the asset value is taken from the book value, so it is necessary to calculate the average value of the bank's assets.

4.1.1.2 Equity to Total Assets (EQ)

Equity/total assets ratio is an independent variable to measure and represent a bank's capital ratio. This ratio reflects the capital structure of each bank.

The bank's equity is a buffer against bankruptcy risk, protects the interests of depositors and contributes to the brand and trust of customers. A high equity/total assets ratio means a low debt/total asset ratio, and the bank will significantly reduce the cost of capital (such as interest expenses, costs related to raising capital, etc.). ,…), reduced costs directly increase profits. Under the assumption of perfect capital markets, an increase in this capital ratio will increase bank profits.

Fotios and Kyriaki (2007) conducted a study on internal bank factors and economic environment affecting domestic and foreign bank profitability of 15 European countries in the period 1995 to 2001. Total number of banks used in this study are 584 banks. The results show that the ratio of equity to total assets has a positive effect on ROA for domestic and foreign banks. Anna and Hoi (2007) also show that banks with a large capital-to-asset ratio have a positive impact on profitability (measured by ROA).