HUE UNIVERSITY

UNIVERSITY OF ECONOMICS

DEPARTMENT MANAGEMENT

—– —–

UNIVERSITY GRADUATION COURSE

Topic:

ASSESSMENT QUALITY Lending Services FOR PERSONAL CUSTOMERS AT NATIONAL COMMERCIAL JOINT STOCK COMPANY HUE BRANCH

Instructor: MSc Tong Viet Bao

Performed by students: Hoang Le Quang Nhat Minh

Maybe you are interested!

-

Evaluation of loan service quality for individual customers at National Commercial Joint Stock Bank - 2

Evaluation of loan service quality for individual customers at National Commercial Joint Stock Bank - 2 -

Overview Of Services, Service Quality And Service Quality Of Banking

Overview Of Services, Service Quality And Service Quality Of Banking -

General Introduction About National Commercial Joint Stock Bank

General Introduction About National Commercial Joint Stock Bank

Grade: K49D- QTKD

Hue, 2018

ACKNOWLEDGMENTS

During the four years of studying and training at Hue University of Economics, under the enthusiastic guidance of teachers, they have provided me with a lot of useful knowledge. Especially, during my graduation internship at National Commercial Joint Stock Bank, Hue branch, I had the opportunity to apply what I have learned in practice. In order to complete this thesis topic, I would like to express my sincere and deep gratitude to the teachers of Hue University of Economics in general and to the teachers of Faculty of Science and Technology.

Business Administration in particular, who have dedicatedly taught and imparted to me valuable knowledge and experiences so that I can become more mature and confident when entering life.

In particular, I would like to express my sincere thanks to Mr. Th.s Tong Viet Bao Hoang – the instructor who cared and helped me a lot in approaching the research and completing this graduation thesis.

I would like to thank the Board of Directors, the Customer Relations Department and the staff in the National Commercial Joint Stock Bank, Hue branch, for always creating conditions for me to learn and provide information. needed for this thesis.

Sincere thanks to my family and friends who have always facilitated, encouraged and encouraged me during the past time.

With limited theoretical level and practical experience, the thesis cannot avoid errors. I look forward to receiving suggestions from teachers and teachers to improve this thesis.

Once again, thank you very much!

Hue, January 2018

Students perform

Le Quang Nhat Minh

TABLE OF CONTENTS

LIST OF ABBREVIATIONS ……………………………………………………………………… ……………………… iv

LIST OF TABLES …………………………………………………………………. …………………………… ……v

LIST OF PICTURES AND DIAGRAMS…………………………………………………………………… ………………………………… Because

PART I. PROBLEM ……………………………………………………………………… …………………………… ….first

1. Urgency of the topic …………………………………………………………….. ………………………………………….first

2. Research objectives…………………………………………………………………………………… …………………………… …2

3. Objects and scope of the study ……………………………………………………………………………………….. ……………………………..2

4. Research Methodology…………………………………….. ……………………………3

PART II. RESEARCH CONTENTS AND RESULTS……………………………………………………………………… …….7

CHAPTER I. OVERVIEW OF LOANS SERVICE QUALITY FOR PERSONAL CUSTOMERS AT COMMERCIAL BANK …………………….. ….7

1.1. Commercial Bank overview …………………………………………………………………………………….. …………7

1.1.1. The concept of a commercial bank ……………………………………………………………………………………….. ..7

1.1.2. Functions of a Commercial Bank …………………………………………………………………….. ………..7

1.2. Overview of commercial banks’ personal lending activities

…………………………… …………………………… ………………9

1.2.1. The concept of individual customers ……………………………………………………………………………………….. …………9

1.2.2. Concept of lending to individual customers …………………………………………………………….. ………..9

1.2.3. Features of lending to individual customers …………………………………………………………….. ……………..9

1.2.4. The role of lending to individual customers for commercial banks …………11

1.3. Overview of services, service quality and banking service quality …..13

1.3.1. Service concept …………………………………………………………………………… ……………………………13

1.3.2. Main features of the service …………………………………………………………………………… …………13

1.3.3. Service role …………………………………………………………………………… ……………………….14

1.3.4. The concept of service quality …………………………………………………………………………… …………14

1.3.5. The concept of banking service quality …………………………………………………………………………. ……15

1.4. Factors affecting the quality of loans for individual customers at commercial banks ………………………………………………………… …………………………… ……….15

1.4.1. Subjective factors …………………………………………………………………………… ………….15

1.4.2. Objective factors …………………………………………………………………………… ………….17

1.5. Service quality assessment model …………………………………………………………………………… …………18

1.5.1. Service quality model and service quality scale ……………………….18

1.5.2. Proposed research model …………………………………………………………………………… …………22

CHAPTER II. THE SITUATION OF THE QUALITY OF Lending Services FOR PERSONAL CUSTOMERS AT NATIONAL COMMERCIAL BANK HUE BRANCH …………………………………………………… …………………………… …………………………25

2.1. Overview of the National Commercial Joint Stock Bank …………………………………25

2.1.1. General introduction of National Commercial Joint Stock Bank …………………………………………25

2.1.1.1. History of establishment and development of National Commercial Joint Stock Bank …………………………… …………25

2.1.1.2. The process of formation and development of Joint Stock Commercial Bank

Quoc Dan Hue branch …………………………………………………………….. ………….26

2.1.2. Organizational structure and functions ………………………………………………………………………. ………..27

2.1.3. Key credit products and services ……………………………………………………………………………………….. …………28

2.1.3.1. Credit products for individual and household customers …………28

2.1.3.2. Credit products for corporate customers …………………..28

2.1.4. Overview of the operation of the National Commercial Joint Stock Bank, Hue branch …………………………………………………………… …………………………… …………30

2.1.4.1. Labor force situation of National Commercial Joint Stock Bank Hue branch in 2015-2017 ………………………………………………………. …………………………… ………30

2.1.4.2. Status of assets and capital sources of National Commercial Joint Stock Bank, Hue branch in the period 2015-2017 …………………………………………………………… ………….32

2.1.4.3. Business results of National Bank Hue branch in the period of 2015-2017 ………………………………………………………… …………………………… ………..34

2.1.5. Current status of lending activities for individual customers at National Commercial Joint Stock Bank, Hue branch. ………….37

2.2. Evaluation of loan service quality for retail customers at National Commercial Joint Stock Bank, Hue branch. …………40

2.2.1. Descriptive statistics of the survey …………………………………………………………….. …………………………40

2.2.2. Evaluation of loan service quality for individual customers at National Commercial Joint Stock Bank, Hue branch. ………………………43

2.2.2.1. Cronbach’s Alpha reliability test with scales …………43

2.2.2.2. EFA exploratory factor analysis …………………………………………………………………………. ……….45

2.2.2.3. Regression analysis …………………………………………………………………………… ………….49

2.2.3. Customer’s assessment of service quality factors for individual customers at National Commercial Joint Stock Bank, Hue branch ………………………………… ……..53

CHAPTER 3. SOLUTIONS TO IMPROVE LIVING SERVICE QUALITY FOR PERSONAL CUSTOMERS AT NATIONAL COMMERCIAL BANK HUE BRANCH ………… …………………………… …………58

3.1. Orientation to improve the quality of lending services for individual customers at National Commercial Joint Stock Bank, Hue branch. …………58

3.1.1. General direction …………………………………………………………………………… ………….58

3.1.2. Orientation to improve the quality of lending services for individual customers at National Commercial Joint Stock Bank, Hue branch ………………………………… ..59

3.2. Solutions to improve the quality of lending services for individual customers at National Commercial Joint Stock Bank, Hue branch. ………….60

3.2.1. Solutions on Service Capability ……………………………………………………………………………………….. …………60

3.2.2. Responsiveness Solution …………………………………………………………………….. ……………………sixty one

3.2.3. Reliability Solution …………………………………………………………………………… …………62

3.2.4. Solutions for Tangibles …………………………………………………………………………………… ……………….sixty four

PART III. CONCLUSIONS AND RECOMMENDATIONS……………………………………… …………65

1. Conclusion ……………………………………………………………………… …………………………… ..65

2. Recommendations ……………………………………………………………………… …………………………… ……….65

2.1. Recommendations to the Government …………………………………………………………….. ………….65

2.2. Recommendations to the State Bank …………………………………………………………….. ………………….66

LIST OF ABBREVIATIONS ONLY

Unit Unit of measure

Customer Customer

Science and Technology Individual Customers

Commercial Bank Commercial Bank

NCB National Citizen Bank

Joint Stock Commercial Joint Stock Company

Credit institutions Credit institutions

GSO Economic organization

LIST OF TABLES

Table 1.1: Original scale and calibrated scale ………………………………………………. ……….23

Table 2.1: Labor situation of National Bank – Hue branch ……………………………………………………….30

Table 2.2: Situation of assets and capital sources of National Commercial Joint Stock Bank in the period of 2015 – 2017……………………………………………………………………… …………………………… ……………………………32

Table 2.3: Business results of National Bank – Hue branch in the period of 2015-2017 ………………………………………………………… …………………………… …………34

Table 2.4: Credit activities at NCB- Hue branch in the period of 2015-2017 ………………………….. …………………………… …………………………… …..37

Table 2.5: Characteristics of the survey sample ………………………………………………………… ……………..40

Table 2.6: Known sources of information, purposes of use and number of times of service use by customers ………………………………………….. …………………………… ………….42

Table 2.7: Results of testing the reliability of Cronbach’s Alapha scales….43

Table 2.8: KMO and Bartlett’s Test …………………………………………………… …………45

Table 2.9: Result of independent variable factor analysis …………………………………………….. ……………….forty six

Table 2.10: KMO and Bartlett’s Test of Dependent Variables …………………………….48

Table 2.11: Results of dependent variable analysis …………………………………………………………………….. ………..48

Table 2.12: Testing the correlation between the independent variable and the dependent variable ………….49

Table 2.13: Summary model using Enter method …………………………………………………………….. …….51

Table 2.14: Test of the fit of the regression model ………………………………………………………… ……51

Table 2.15: Results of multivariate regression analysis …………………………………………………… …………52

Table 2.16: Customer’s assessment of factors affecting the quality of personal loan services …………………………………………………… …………………………… ………..53

LIST OF PICTURES AND DIAGRAMS

Figure 1.1: The five quality gap model …………………………………………………………………….. ……………..18

Figure 1.2: SERVQUAL model (Parasuraman, Zeithaml & Berry (1988))……………..20

Figure 1.3: Proposed research model …………………………………………………………….. …………22

Figure 2.1: Logo of National Commercial Joint Stock Bank …………………………………………………………………. …………26

Figure 2.2: Management apparatus of National Commercial Joint Stock Bank – Hue branch …………27

PART I. ASKING THE PROBLEM

1. Urgency of the topic

In the current context, Vietnam’s economy is increasingly integrating deeply into the global economy, posing many opportunities as well as challenges for businesses. Especially, in the banking sector, which is also under pressure in this regard, the competition between domestic and foreign commercial banks is becoming increasingly fierce. In a competitive environment, “The products are similar, it is the quality of the service that makes the difference” this is a classic in the banking industry that is not easy to achieve in reality. Achieving this to some extent is also a measure of the position and service quality of each bank. On the other hand, if a business wants to survive and develop, it needs customers (customers), showing the importance of customers in business activities. Therefore, the services that the Bank provides must meet the customer’s satisfaction with the quality of that service. Therefore, capturing customer feedback on service quality is essential. The Bank’s good exploitation of information from customer feedback will create an advantage in dominating the market among banks.

Banks that always seek to retain customers need to first innovate and improve the quality of banking services and meet the needs and desires of customers. Among the Bank’s business operations, credit is the main business. Currently, commercial banks are focusing on individual customers (Science and Technology), lending products and services for individuals are very diverse and rich. Therefore, when measuring the quality of banking services, the indispensable job of the Bank is to measure the quality of credit services, especially the quality of loans for science and technology. It is very necessary to grasp the current status of service quality that the Bank provides, because through that, the Bank promptly knows the shortcomings in its services, thereby supplementing and giving measures. Optimal solutions for timely remedial measures to enhance customer satisfaction and enhance the Bank’s competitive advantage.

Over the years, National Commercial Joint Stock Bank Hue branch has continuously promoted various types of services, and at the same time the Bank has focused on service quality in general and lending service quality in particular. However, the credit performance of National Commercial Joint Stock Bank Hue branch is still limited, and the quality of the Bank’s lending services has not yet fully met customers’ wishes. Therefore, after a period of practice and research at National Commercial Joint Stock Bank, Hue branch, I decided to choose the topic “Evaluating the quality of loan services for individual customers at the National Bank of Vietnam”. Quoc Dan Joint Stock Commercial Bank, Hue branch” as the topic of his thesis.

2. Research objective

2.1. Overall objectives

On the basis of assessing the quality of lending services for science and technology at the National Commercial Joint Stock Bank, Hue branch, giving solutions and recommendations to improve the quality of lending services for science and technology at the Bank during this time. next.

2.2. Detail goal

• Systematize the theoretical basis of service quality in general and the Bank in particular.

• Determining the factors affecting the quality of lending services for science and technology at National Commercial Joint Stock Bank, Hue branch.

• Analysis and assessment of the current situation of loan service quality for science and technology at National Commercial Joint Stock Bank, Hue branch.

• Proposing solutions and recommendations to improve the quality of lending services for science and technology at National Commercial Joint Stock Bank, Hue branch. 2.3. Research question

• How are lending activities for science and technology at National Commercial Joint Stock Bank Hue branch today?

• How do customers rate the quality of loan services at National Commercial Joint Stock Bank, Hue branch?

3. Object and scope of research

Research object: quality of lending services for science and technology at National Commercial Joint Stock Bank, Hue branch. Research scope:

• About space: Research carried out in Hue city.

• About time: 2015-2017.

• About the content: The topic focuses on researching the quality of lending services for science and technology at National Commercial Joint Stock Bank – Hue from the perspective of customers.

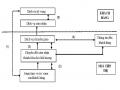

4. Research Methodology

4.1. The method of data collection

a) Secondary data:

Collect and use data related to the business performance of National Bank – Hue (from the following sources: customer relations department, main website of National Bank …)

Refer to data, information on scientific articles, theses, theses and documents on the Internet.

b) Primary data:

Collected through survey questionnaires, distributed questionnaires to collect opinions of science and technology when using lending services at National Bank Information collection methodDan-Hue. and sampling plan.

The overall objective of the study is that customers are using loan services for science and technology at NCB Hue branch. The sample size in the study was based on the requirements of Exploratory Factor Analysis (EFA) based on Hair & et al. al (1998): Minimum sample size is 5 times the total observed variable.

n= m × 5

Where: m is the number of observed variables

The research model includes 24 observed variables. Therefore the minimum number of samples is:

n=24 × 5= 120 (customers)

Thus, the sample size must ensure the following conditions: n ≥ 5 × 24 ≥ 120.

The number of samples required to conduct regression analysis must satisfy the following conditions: n ≥ 8 × p + 50 = 8 × 5 + 50 ≥ 90.

Where: p is the number of independent variables (in the topic: p = 5)

The sample was selected by systematic random sampling method by distributing questionnaires to customers when using lending services for science and technology at the Bank. Thus, to achieve the minimum number of samples for the study and to avoid errors, the number of questionnaires distributed was 130 questionnaires. The interview process will end when 130 questionnaires are reached.

According to information from the Customer Relations Department of NCB Hue branch. In 3 weeks, the number of customers coming to transact at the Bank is 360 customers. It is estimated that 20 customers come to the transaction every day. In 3 weeks, there are 18 working days, each day survey 130/18 = 7.2 8 CZK

Day 1 investigation:

– Calculate the jump k= 20/8 ≈ 3

– Option 3 KH, then investigate the next customer until 8 KHU

Investigate the next day in the same way. 4.2. Data analysis and processing methods

The study used statistical analysis method by SPSS software. The questionnaire uses a 5-point Likert scale: 1. Strongly disagree, 2. Disagree, 3. Neutral, 4. Agree, 5. Strongly agree. After collecting information from customers through questionnaires. Next, check and remove the unsatisfactory questionnaires. Finally, encrypt the data, import the data, and clean the data.

– Descriptive statistics method

Used to analyze the characteristics of the survey object. The results of the analysis are the basis for making initial judgments and creating a foundation for proposing solutions in the future.

Frequency (frequency), Mean (average value).

– Check the reliability of the scale using Cronbach’s Alpha coefficient:

The purpose of calculating this coefficient is to check the closeness and correlation between the observed variables, thereby eliminating the garbage variables.

Variables with a total correlation coefficient (Item-Toatl Correlation) less than 0.3 will be removed and the criteria for choosing a scale when having alpha reliability of 0.6 or higher (Nunnally & Burnstein “Pschy Chometric Theory” , 3rd edition, McGraw Hill, 1994).

Exploratory factor analysis (EFA)

Exploratory factor analysis is a technique used to collect and summarize data. This method is very useful for determining the set of variables needed for the research problem and is used to find the relationship between variables.

According to Hoang Trong, Chu Nguyen Mong Ngoc (2008): Some criteria when analyzing exploratory factors:

KMO coefficient: only used to consider the suitability of EFA, if the KMO coefficient is in the range of 0.5 ≤ KMO ≤ 1, then factor analysis is appropriate.

Significance level of Bartlett test ≤ 0.5, factor loading

0.5, total variance extracted ≥ 50% and Eigenvalue coefficient is greater than 1.

The difference between the factor loading coefficient of an observed variable among the factors is ≥ 0.3 to ensure the discriminant value between the factors.

– Correlation analysis

Correlation analysis is an analysis used to determine the linear relationship between independent and dependent variables in research. Sig coefficient. shows the appropriateness of the correlation coefficient between the variables according to the F-test with the given confidence level of 5%.

Correlation coefficient r: r < 0.2: no correlation; r from 0.2 to 0.4: weak correlation;

r from 0.4 to 0.6: average vibration correlation; r from 0.6 to 0.8: strong correlation; r from 0.8 to

1: very strong correlation.

– Multiple regression analysis

Is an analytical method to determine the influence of factors after being extracted in exploratory factor analysis (EFA) on the dependent variable.

The linear regression model will be built according to the step-by-step regression method

The general regression model is as follows:

HL= 0 + ß1*X1 + ß2*X2 + ß3*X3 + … + ßi*Xi

Inside:

HL: customer satisfaction with the quality of loan services for science and technology

Xi: the importance of factors affecting the quality of lending services for science and technology

ß0: constant

i: regression coefficients

The fit of the regression model is evaluated through the coefficient R

2 adjustments. CHEAP value

2 adjustment is independent of the magnification bias of R2 and is therefore used in a multivariate linear regression fit. The model is more significant as the adjusted R2 gets closer to 1.