While 100% foreign-owned banks focus on the potential retail market with low risk, most Vietnamese banks and even BIDV Quang Trung branch focus on the capital lending market. Business enterprises, especially lending for real estate business, are very risky. This is probably the most important cause of bad debt in the whole Vietnamese banking system today.

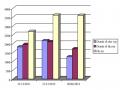

Table 2.2 Statistics of bad debt and bad debt in real estate lending of BIDV Quang Trung and BIDV Vietnam branches

Unit: million VND

| Time | December 31, 2011 | . | December 31, 2012 | . | June 30, 2013 | . |

| Object | BIDV Quang Trung | BIDV Vietnam | BIDV Quang Trung | BIDV Vietnam | BIDV Quang Trung | BIDV Vietnam |

| Bad debt (groups 3, 4, 5) | 1.341 | 8.229.120 | 2.883 | 5.701,904 | 2.513 | 5,968.736 |

| Bad debt/Total outstanding balance | 0.05% | 2.96% | 0.08% | 1.68% | 0.07% | 1.64% |

| Bad debt for real estate business loans | 537 | 3,291,648 | 557 | 4.389.157 | 557 | 4,712.864 |

| Bad debts for real estate business loans / Total outstanding loans | 0.02% | 1.2% | 0.02% | 1.3% | 0.02% | 1.3% |

Maybe you are interested!

-

Organizational Structure, Management Apparatus Of Bidv Quang Trung Branch

Organizational Structure, Management Apparatus Of Bidv Quang Trung Branch -

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 6

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 6 -

Current Status Of Bad Debt In Real Estate Lending At Joint Stock Commercial Bank For Investment And Development Of Vietnam And At Bidv Quang Trung Branch

Current Status Of Bad Debt In Real Estate Lending At Joint Stock Commercial Bank For Investment And Development Of Vietnam And At Bidv Quang Trung Branch -

Impact Of Bad Debt In Real Estate Lending For Joint Stock Commercial Bank Bidv Vietnam – Quang Trung Branch

Impact Of Bad Debt In Real Estate Lending For Joint Stock Commercial Bank Bidv Vietnam – Quang Trung Branch -

Orientation On Limiting Bad Debt In Real Estate Lending At Bidv Vietnam – Quang Trung Branch

Orientation On Limiting Bad Debt In Real Estate Lending At Bidv Vietnam – Quang Trung Branch -

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 11

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 11

(Source: P. Finance and Accounting)

Looking at the data table 2.1, we see that the total outstanding loans increased continuously over the years from 2011 to 2012. Total outstanding loans in 2012 reached VND 3,604,000 billion, up 34% compared to 2011 at VND 2,682,050 billion. However, the bad debt/total outstanding debt ratio also increased with the overdue debt ratio since 2011 being 0.05%. Entering 2012 due to the general influence of the world economy on the financial market and business activities of BIDV Quang Trung’s “debtors”, although total outstanding loans increased by 43% compared to 2012, it was not positive sign. Accordingly, the value of bad debt has not tended to decrease but continued to increase up to 0.08%. This shows that the management of overdue debts and bad debts of the branch has not really improved.

Besides, exchange rate fluctuations are also one of the factors causing bad debt. 2012 was the year when the USD/VND exchange rate fluctuations were very strong along with the gold price continuously reaching new peaks, which made it difficult for material suppliers when they had to import at high prices, meaning this source of debt repayment of these projects is limited. However, BIDV Quang Trung has measures such as restructuring the repayment period, grace period, and extension because these are objective reasons not of the enterprise, so the impact of these loans is not significant. large and partially limit the arising of bad debt. Although bad debts increased (2011-2012), the rate was much slower than overdue debts, especially the bad debt ratio was always below 1%. This is a commendable achievement of credit officers in the post-crisis period.while banks always face the risk of overdue debt, high bad debt in lending for real estate business.

As of December 31, 21011, BIDV Vietnam owns 1.2% of bad debts in real estate lending/Total outstanding loans, ie about 40.5% of total bad debts, BIDV Quang Trung is no less in debt. Bad loans for real estate accounted for 40% of total bad debts. However, by 2012, bad debt in this area only accounted for 25%. There are two reasons for such a decrease, firstly, the value of bad debt increased sharply by 60% from 1,341 million dong in 2011 to 2,883 million dong in 2012 while bad debt in real estate loans increased only slightly from 537 million VND to 557 million VND. By June 30, 2013, this figure decreased slightly to 2,513 million VND. The second reason for the above problem is related to the very slight increase in bad debt for real estate loans. Trends in 2011 -2012,Credit institutions are tightening credit with customers who apply for loans for real estate-related purposes and actively collect overdue debts, debts that need attention, etc., the branch is no exception. The increase of VND 30 million in 2012 is only the interest for a debt of VND 537 million in 2011. By the time of 2013, the value of this debt leveled off to VND 557 million due to the “debtor” almost. insolvency should be facilitated by the Branch to repay the debt by exempting the “debtor” from interest starting from 1/1/2013.By the time of 2013, the value of this debt leveled off to VND 557 million due to the fact that the “debtor” was almost unable to pay, so the Branch facilitated repayment by exempting the “debtor” from interest. “commencing from January 1, 2013.By the time of 2013, the value of this debt leveled off to VND 557 million due to the fact that the “debtor” was almost unable to pay, so the Branch facilitated repayment by exempting the “debtor” from interest. “commencing from January 1, 2013.

In addition, the cause of this is due to the impact of the world and regional economic crisis leading to the freezing of the domestic real estate market, the inventory of goods in very large quantities, and the lack of resources for businesses. collected to repay the bank debt. Entering 2013 with the economy having prospered, the value of bad debt in this field tended to decrease slightly, but in fact, the bad debt of 2012 was transferred to 2013, due to the increase in credit balance, so ratio of bad debt in loans for real estate business / Total outstanding loans decreased.

2.5 Causes of bad debt risk in real estate lending at BIDV Quang Trung

One of the major bottlenecks of the current economy is the problem of bad debt of the banking system, especially bad debt in real estate lending. Many economists call it the “blood clot in the blood vessels” of the economy. Solving this problem can clear the deadlock for the economy, help stabilize the macro-economy and promote the recovery of economic growth.

Bad debt is a constant problem in banks in recent years, because credit activities are always risky. During their operation, credit institutions always incur bad debts. The increase in bad debts of the banking system in general does not mean that it is the banking system that is the author of these bad debts, because the arising of these bad debts is due to the default of the borrowers. to bad debt. Thus, when analyzing the causes of bad debt, we need to mention the causes from the banks and customers as well as the objective causes from the economy.

– Reasons from the bank:

+ BIDV Quang Trung focuses on pursuing fast credit growth strategy.

The reason for bad debt is that BIDV Quang Trung is pursuing a strategy of fast credit growth while the risk management capacity is still limited and slowly improved. Besides, over the past time, a large part of credit capital has been focused on areas with many potential risks, especially the real estate market in the period 2007-2009. At that time, the market was developing. developed very quickly, the land fever continuously appeared, and the house price increased rapidly. In the period 2011 – 2012, the real estate market fell into a frozen state, real estate investment enterprises fell into a crisis, financial capacity decreased, could not pay debts, leading to bad debts in the field of real estate. This increases rapidly.

+ Credit management at BIDV Quang Trung branch is not really effective.

In addition, another reason contributing to the increase in bad debt in real estate lending is that the internal inspection and supervision of the bank for a long time has not been highly effective in detecting and preventing timely prevent and handle violations and risks in credit extension activities, especially violations of regulations on credit restriction and excessive investment in a number of potential high-risk areas.

According to Decision 493/2005/QD-NHNN dated 22/4/2005, debt is divided into 5 groups. For bad debts, commercial banks must classify debts and assess customers’ debt repayment ability on a monthly basis to serve the management of credit risk and quality. Provision ratios for specific debt groups are: Group 3: 20%, Group 4: 50%, Group 5: 100%. Thus, with a figure of more than 500 million, it means that BIDV Quang Trung will have to set aside at least 100 million if it is a group 3 debt and 500 million if it is a group 5 debt. This is not too big a number compared to the bad debt of Group 3. The whole banking system in Vietnam today, but also partly reflects the inefficiency of the branch’s risk management of bad debt and overdue debt.

– The reason comes from the customer

+ Value of collateral “evaporates”

When bad debt occurs, there are many measures to recover bad debt that are being applied throughout the banking system. Currently, the measures taken by banks to recover debts are mainly liquidation of debt security assets or lawsuits in court. However, according to many banking and finance experts, in fact, the implementation of bad debt settlement, especially group 5 debt, through the handling of debt security assets faces many difficulties. processing takes a lot of time and procedures, and the recovery value is low due to many reasons. The current common situation is that many values of assets to secure debt have “evaporated” very strongly compared to the time of borrowing, for example, the value of stocks and real estate values have fallen sharply today. This is the first reason that there are still many problems in handling and recovering bad debts.This makes it very difficult for the branch to handle debt security assets, if handled, only part of the debt can be recovered.

In addition, another difficulty that the branch often encounters is that when the collateral is liquidated, the proceeds will be prioritized to be paid first for the debts according to the order of priority, such as: When liquidating collateral assets, priority must be given to the payment of import tax obligations, because most of these devices are exempt from import tax because they are often considered fixed assets when establishing a company…

Not only that, if the collateral is investment projects, or some other real estate, the division of rights, responsibilities and debt repayment obligations will be very difficult.

For example, BIDV Quang Trung lends a part to the Ecopark new urban area project.

When the investor of the project’s infrastructure could not afford to repay the debt, forcing the bank to squeeze the debt, but customers who are retail investors also put 70% in the assets of each individual, waiting for the delivery date. will pay the remaining 30%. If the bank squeezes the loan on the investor’s loan amount, it is certain that the entire value of the property will be confiscated and blocked, and it is likely that the customers will lose everything. This leads to the implementation of bad debt settlement through debt collateral which is often lengthy and financially costly.

In fact, many collaterals due to lack of cooperation from debtors make banks face many difficulties in handling debt security assets when debtors do not cooperate, deliberately prolonging the repayment period, and If the bank cannot reach an agreement with the customer, the only way is to transfer the lawsuit file to the court, or even ask the court to open bankruptcy proceedings against the business. But with this approach, the processing time that takes 3-4 years is also a difficulty for the bank. The difficulty of banks in dealing with bad debts is not the liquidation of collateral, but the return of those assets, lines and machines to work and production.

This is the root of bad debt settlement because if only selling bad debt from one creditor to another is just a formality. However, to do this depends a lot on the recovery of the economy.

+ Not being able to update all accurate and immediate information about the real estate market in Vietnam and the sense of providing inaccurate information to the bank applying for a loan.

Vietnam’s real estate market has up to 90% of domestic investors. They have the advantage of land, but the disadvantage of capital and lack of professionalism. The majority of real estate businesses have low equity capital, operating mainly on credit financial institutions, capital raised in advance from buyers.

Enterprises participating in the real estate market only focus on short-term calculations, including thinking about investment, on how to create capital to develop the market, while the formal real estate market needs medium and long-term strategies. term. Most businesses do not have or have very little professional marketing activities, do not keep their commitments, do not follow the construction schedule, the products are not of good quality, conduct investment in projects that are rampant. Inability to supervise and manage, no experience in real estate, capital is not used for the right purposes.

When implementing investment projects, most businesses do not have market research to come up with an appropriate business strategy. Many businesses do not understand the market leading to rampant investment, wasteful, even speculative, adversely affecting the market. Bad debt in real estate lending is increasing, causing great harm to the economy and directly affecting businesses. this. The Government’s recent message also shows that dealing with bad debts, mainly in the real estate sector, is a top task in the plan to reform the banking system. Bank bad debt has become a national problem, especially bad debt in real estate lending is causing great hindrance to the development of the national economy, because this is an extremely sensitive commodity in the world. market.Therefore, it is necessary for the State to start to solve it, not let commercial banks manage it themselves. In the past 20 years, from the experience of countries that have had bad debt problems such as South Korea and the US, they have all chosen to deal with debt trading and have been successful.

Besides the general difficulties of the economy, the main reason for the increase in bad debt comes from within the bank itself. Therefore, finding solutions to prevent the increase of bad debt in the field of real estate lending, minimizing the adverse impact of bad debt on the branch in particular and the whole banking system in general. The economy must start from the banks themselves, and at the same time do not underestimate the cause of the general operating policy.

Up to now, bad debt has increased quite quickly, due to different reasons, especially the impact from the business environment. According to the data that the State Bank’s Inspectorate and Supervision Agency has just officially announced recently, Vietnam’s current bad debt figure is 8.6%, equivalent to VND 202 trillion, BIDV Quang Trung itself according to the figure. The most recently announced is more than 500 million. Meanwhile, when the market fluctuates, businesses are under great financial pressure, at risk of bankruptcy, and unable to repay bank loans.

Another risk is that customers provide false information about the business’ financial situation, liquidity, corporate governance, project feasibility, and loan options. Or customers have acts of fraud and corruption, intentionally doing wrong. For example, creating fake documents and fake notarization to mortgage, use a property to mortgage and pledge at many banks, rent another owner’s house for mortgage, borrow other people’s property to pledge, use seals and papers of dissolved enterprises to collude with credit officers to carry out loan procedures.

– Cause comes from the economy

+ Liquidity risk in the real estate market

It is an undeniable fact that Vietnam’s real estate market is in a very difficult period with low purchasing power, low liquidity, large inventories and significant bad debts.

However, in that general situation, there is still a glimmer of businesses selling real estate at a slower rate but still maintaining steady development. Each business has different secrets, but they all meet at one point:

maintain liquidity with its development strategy and product quality.

In 2013, the most important factor is market liquidity, not price. With good liquidity, real estate businesses will have the opportunity to settle inventories, earn profits and repay loans to banks. To solve this problem, the management agencies have also launched many solutions to support the market in the past two years, but the impact on the real estate market has not been much. Annually, the preliminary supply is about 20,000 units, this is a large-scale market. The current problem is that there is a lot of inventory that needs a solution to sell. real estate Most of the inventories are formed during the fever period, mainly high-priced real estate to meet the speculative needs, not to meet the housing needs of the workers. Up to now, the demand due to speculation is no more, the real demand for housing is not able to pay. Oversupply, high demand; But supply and demand do not meet.

This is the tragedy of the current real estate market. The real estate market develops too strongly in the mid- and high-end segments, but the shortage in the below-average segment has led to the situation: real estate is both redundant and insufficient.

Is it possible to reduce the price of real estate only to expect to increase the liquidity of the market? This view is correct, but not sufficient. In fact, there are still projects that, despite wearing a cheap “shirt”, have low liquidity, because people do not believe in the development ability of the project, or have not yet approached the project. They expect that in addition to fulfilling the requirements of the investor, they must also have access to the real project, now housing projects are often not accessible to the investor but must go through an intermediary.

In fact, with the current price when many investors reduce the selling price of houses ranging from 20 million VND/m2 to 22 million VND/m2, there are transactions and with an area of about 70m2, all sold out. Therefore, decisions need to be aimed at buyers to use.

The adjustment to increase and decrease the selling price is an inevitable requirement of the market. Supportive policies of the State will contribute to reducing selling prices and promoting complete real estate products to the market. As for the level of adjustment, it is a difficult problem. Because of the current period, high costs, recent inventories have pushed prices down.

But businesses can’t cut prices so hard to accept losses.

Obviously, each investor needs to find their own direction. Despite difficulties, there will still be opportunities for both investors and investors, especially new investors. In fact, there are still many people willing to buy the project and adjust it to better match the demand.

+ The real estate market lacks professionalism

This lack of professionalism is reflected in the imbalance of goods and market participants. Although the real estate market has grown strongly in recent years, the product structure is not reasonable compared to the market demand. Typically in the housing market segment, for profit reasons, most businesses focus on apartments, luxury villas, townhouses, etc., without taking into account the average income of the vast majority of people. current housing needs. Therefore, leading to an overabundance of high-end products but a shortage of housing for middle and low-income people.