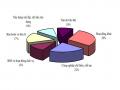

The fields of lending with a high percentage are construction, repair, buying houses for living in combination with leasing, which customers repay with non-salary income (VND 57,113 billion), urban construction (VND 49,258 billion). ; building office buildings for rent (VND35,495 billion), buying houses for sale, leasing, industrial parks, export processing, land use rights… Notably, the bad debt ratio in the field of real estate investment and business as of June 30, 2013 was determined to be 6.4%, equivalent to more than 15.5 trillion VND.

Regarding the disbursement of a loan package of VND 30,000 billion to support housing, up to now, 5 designated commercial banks have committed to lend to 130 individual customers , of which 119 customers have been disbursed with a loan balance of VND 28.46 billion; confirmed to lend to 2 businesses with the amount of 658 billion dong.

The above figure is equivalent to 10 billion USD is really worrying and affects the operation of banks as well as the economy. The fact that a large amount of money up to over 200 trillion VND cannot be put into circulation and is buried in secured assets will cause great waste to society, especially in the current difficult economic context. With a “blood clot in a blood vessel” this large, no matter how much it is pumped, the “credit blood” still can’t flow. Bad debt is the reason why banks have not dared to continue lending in the past time, even though there is no shortage of capital. Banks must be more cautious with loans to avoid further bad debts, resulting in banks having money but unable to lend, and the economy continues to be thirsty for capital.

Vietnam’s bad debt currently mainly falls in the fields of industrial production and construction, which have been affected by the prolonged freezing of the real estate market in recent years. According to the State Bank of Vietnam, by the end of May 2012, outstanding loans for real estate investment and business were about VND 197,000 billion. It only accounts for a not-so-large proportion of the total outstanding loans of VND2.6 million billion. Bad debt for real estate investment and business is about VND 12,000 billion, accounting for about 6.5% of outstanding loans, accounting for about 10.3% of total bank bad debts as reported by credit institutions. For securities trading investment loans, due to the market slump and prolonged difficulties, the lending trend tends to decrease. By the end of May 2012, it was only about 12,000 billion dong, its bad debt was also relatively low with about 485 billion dong.

However, the State Bank of Vietnam still has an optimistic view. Provisions for risks and collateral will help prevent bad debts from having a great impact on the operations of credit institutions. Also according to the State Bank, Vietnam’s bad debt ratio of 8.6% is high and tends to increase, but compared to some countries in the region at the time when the government also had to stand up to handle bad debts, it was still Much lower. For example, Thailand at the time of the financial crisis in 1999, bad debt amounted to 47.7%; Indonesia over 50%; Korea in 1998 was 17% and Malaysia over 11.4%…

The above problems show that this is just the tip of the iceberg, which data is the most accurate can only be determined by the banks themselves. However, one thing is for sure, bad debt to total outstanding loans in the real estate sector is at an alarming level, it is necessary to have measures to control and limit bad debts in this field.

2.3 Trends of Vietnam’s real estate market

The current bad debt crisis of the real estate market comes from two reasons.

The first is a big deviation in the supply-demand relationship for housing. The supply of mid-end and high-end housing products, with high value accounting for a large proportion and completely deviating from the structure of demand, is dominated by the demand for affordable housing of the majority of people. The second reason is the deviation in expectations of real estate businesses. Therefore, even though the market has been “frozen” for a long time, many real estate businesses still think that the difficulties of the real estate market are only temporary and the price has bottomed, so it will quick recovery. Moreover, many real estate businesses still deliberately keep their goods, “hungry prices” to expect the rescue from the State. This expectation is also completely wrong, because with the current scale of bad debt in the real estate market, the State cannot afford to rescue it, even if it wants to.

Maybe you are interested!

-

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 3

Solutions to limit bad debt in real estate lending at Joint Stock Commercial Bank for Investment and Development - 3 -

The Need For Solutions To Limit Bad Debts In Real Estate Lending

The Need For Solutions To Limit Bad Debts In Real Estate Lending -

Organizational Structure, Management Apparatus Of Bidv Quang Trung Branch

Organizational Structure, Management Apparatus Of Bidv Quang Trung Branch -

Current Status Of Bad Debt In Real Estate Lending At Joint Stock Commercial Bank For Investment And Development Of Vietnam And At Bidv Quang Trung Branch

Current Status Of Bad Debt In Real Estate Lending At Joint Stock Commercial Bank For Investment And Development Of Vietnam And At Bidv Quang Trung Branch -

Causes Of Bad Debt Risk In Real Estate Lending At Bidv Quang Trung

Causes Of Bad Debt Risk In Real Estate Lending At Bidv Quang Trung -

Impact Of Bad Debt In Real Estate Lending For Joint Stock Commercial Bank Bidv Vietnam – Quang Trung Branch

Impact Of Bad Debt In Real Estate Lending For Joint Stock Commercial Bank Bidv Vietnam – Quang Trung Branch

According to the latest data on the bad debt structure announced by the State Bank, the manufacturing and processing industries accounted for the highest proportion in the fields (with 22.5%); followed by real estate and service activities (19.25%). large proportion of the total outstanding loans. Moreover, real estate bad debt led to the stagnation of two important industries related to employment and social security: construction (created jobs for about 3.3 million workers – equivalent to 6.4% of the total). economy) and construction material production (about more than 500,000 employees, equivalent to more than 1% of the total labor of the economy). According to statistics, the number of finished apartments is not much in stock (the whole country has 26,444 apartment buildings and 15,786 low-rise houses in stock).But the number of apartments still lying on paper, new projects only compensation for site clearance, may have detailed planning, project design … are many. The number of apartments and low-rise houses in the projects is dozens of times larger than the number of finished built apartments and this is the real concern of the real estate market. The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.new projects only compensation for site clearance, may already have detailed planning, project design… are many. The number of apartments and low-rise houses in the projects is dozens of times larger than the number of finished built apartments and this is the real concern of the real estate market. The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.new projects only compensation for site clearance, may already have detailed planning, project design… are many. The number of apartments and low-rise houses in the projects is dozens of times larger than the number of finished built apartments and this is the real concern of the real estate market. The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.project design… a lot. The number of apartments and low-rise houses in the projects is dozens of times larger than the number of finished built apartments and this is the real concern of the real estate market. The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.project design… a lot. The number of apartments and low-rise houses in the projects is dozens of times larger than the number of finished built apartments and this is the real concern of the real estate market. The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.The scale of bad debt of the real estate sector is significant, but even larger, when analyzing the fluctuations of this debt block. With an economy in the process of adjusting towards debt divestment after a period of hot growth based on high credit growth, the hottest sectors, using the most debt, especially the Real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.In particular, real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.In particular, real estate will have to make the strongest adjustments to bring the economy back to a balanced and sustainable trajectory. The possibility of bad debt in the real estate sector will continue to increase in the medium term.

After a long period of hot development, the scale of “toxic” assets (assets that are not illiquid, at least in the short term) in the real estate sector has been quite large, so solutions need to be taken. If done quickly, we hope to be able to brake the process of “debt expands, assets shrink”. However, there are many challenges related to the implementation of bad debt settlement solutions in the real estate sector. According to many researchers, a “positive destruction” is the best way to get rid of inefficient businesses and shift resources to efficient ones, thereby resolving bad debts in a sustainable way.

The condition to solve “bad debt” according to Resolution 02/NQ-CP of the Government is to eliminate most of the mid-range and high-end apartment projects that investors have aimed for in recent years. Projects that have misdirected the customer segment are forced to pay a price that no one can “save”. Investors are forced to reduce prices to cut losses, or have to drop below 15 million VND/m2 to receive support, even selling below cost to end a wrong investment cycle is also normal. .

There are three types of opinions about the state and trends of the real estate market: The first type of opinion says that the real estate market is still on a downward slope, ie, has not reached the bottom. High-class apartments, villas, and land plots are far from the center, although the price has dropped quite a lot, the inventory is still large, almost cannot be sold, because the price is still high, not suitable for the budget and ability affordability of the majority of customers with real housing needs. For plots and apartments closer to the center, the price is high, or the area is too large, while secondary investors, as well as people with real needs, have the mentality of waiting for the price to drop again before buying. Some projects and apartments have lower prices, but buyers are still afraid of legal issues, about value-added tax, money difference, construction quality… The second type of opinion is that the market is Real estate is at the bottom (meaning there is no longer a downward trend,but not yet reached the bottom exit and go uphill). The basis of this opinion is that real estate prices have fallen deeply, some have decreased by 30-40% (if the interest rate on bank loans for investment in 2 years is about 35-40%, it will decrease even more. ). Most investors at the time the price was high, had already lost. Accordingly, except for a few types of products such as villas, high-class apartments, and land plots located far from the center, it can be further reduced, while other segments will hardly be able to reduce further. According to this type of opinion, the time to stay at the bottom will not be long, maybe by the end of this year, or by the middle of next year, the real estate market will exit the bottom and go uphill, when the domestic and world economy recovers, when the world economy recovers. A real estate credit package of VND 30,000 billion has been disbursed… Accordingly, this type of opinion recommends that it’s time to invest in real estate to catch opportunities, especially for real estate, which takes several years to complete.

The third type of opinion is that the real estate market has begun to bounce off the bottom and go up, because there have been some signals. The number of transactions in some segments has increased again, although not as vibrant as before, but not as sparse as a few years ago. Bullish trading is the premise that the market will warm up again. For investors, in order to build projects that take several years to complete, they can anticipate a new “peak”. Investors already have raw products, which need to be completed quickly, to take advantage of selling at a high price and also lower the selling price, to recover capital quickly, in order to have new investment capital to catch up. If a few years ago, secondary investors sold at the original price plus a large difference; then the market fell, not only was there no margin, but sold below the original price. Recently,The difference has reappeared (for works starting to start construction), although it is not as large as before. Prices in some other segments, in some areas, may still decrease, but the rate of decline has slowed down. The price of construction materials, after a long period of decline, has now begun to increase slightly, while the production output in the first 8 months of this year has increased better than the same period last year… Buyers on the market today have There are shifts in the trend that the proportion of people with real needs – buy to use increases.while the production output in the first 8 months of this year has increased better compared to the same period last year… Buyers in the market today have changed according to the trend of the proportion of people with real needs – buying to use. increase.while the production output in the first 8 months of this year has increased better compared to the same period last year… Buyers in the market today have changed according to the trend of the proportion of people with real needs – buying to use. increase.

In addition, macro conditions are also supporting the market, such as the revised Law on Corporate Income Tax, the revised Law on Value Added Tax, many preferential mechanisms such as corporate income tax reduction, value added tax. increase for social housing… will be put into practice. Along with that, credit support package for low-income people, civil servants, public employees, armed forces, loans to rent, hire-purchase, buy social housing and commercial houses with small area, low selling price. according to Resolution 02/NQ-CP of the Government. Many businesses have actively adjusted their business strategies such as subdividing apartments, using domestically produced finishing materials, etc., to reduce costs; lower the selling price to cut losses; support for homebuyers by supporting bank loans, promotions, paying many times…

Along with supportive policies from the State, confidence in the market also initially showed signs of recovery and consolidation. With that belief, a part of people with real needs began to “spend money” to buy.

Entering 2013, the real estate market continued to face difficulties in terms of capital due to the priority fiscal and monetary policies to curb inflation that were applied by the Government in the previous 2 years. Although credit sources have gradually opened up to the market, it is still not enough to warm up this market due to relatively strict borrowing conditions.

Credit sources still only meet short-term loans of less than 12 months, there are no medium and long-term credit sources for real estate. Moreover, many businesses need capital but still find it difficult to access short-term credit. Lack of capital will inevitably lead to slow implementation of the project on schedule, buyers with insufficient financial resources, and poor transactions. This is the reason why consumers lack confidence when investing in this market, leading to inventory of real estate goods being created. The downtrend in real estate prices began to appear in the market, especially in Ho Chi Minh City. Ho Chi Minh City since 2010 and then Hanoi since 2011.

The initial real estate price reductions were only around 20% of the price level established in 2010, then there were projects down to 50%. Many businesses said that the reduction was already at its maximum, the price had reached the floor of the producer price and could not be reduced any further. Project investors began to feel the difficulty of stopping transactions for high-priced properties that were formed. People who want to buy business houses as well as buy houses to live in are always in a state of waiting for prices to continue to fall, not wanting to buy right away. This is also the common psychology of consumers and becomes a big difficulty for investors in housing projects. Remaining real estate was formed during the price fever period, mainly high-priced real estate to meet the speculative needs that did not meet the housing needs of workers. Up to now, the demand due to speculation is no more, the real demand for housing is not able to pay. Surplus supply,Demand dropped sharply, supply and demand curves did not meet, creating a “tragedy” for the real estate market in 2012.

According to research by Dragon Capital, the total backlog of real estate in Hanoi and Ho Chi Minh City. Ho Chi Minh City has reached 70,000 apartments, which means each place has more than 35,000 apartments ready for sale without transaction. If the average price is VND 1.5 billion per unit, the total amount of capital outstanding in real estate is estimated to be up to VND 100,000 billion. Many experts believe that it takes up to 7 years to settle this amount of real estate inventory.

According to statistics of more than 60 real estate companies listed on the stock exchange, inventory accounts for nearly 50% of the total assets of these enterprises. In particular, some enterprises have a percentage of real estate inventory accounting for 70 to 90% of the total asset value.

Most businesses no longer have cash to operate, to pay debts. This forces real estate businesses to find ways to speed up the settlement of inventories.

Invented real estate that cannot be sold is a bad debt of the bank if the investment capital is credit capital borrowed from banks. Therefore, the problem of solving real estate backlog is also the problem of solving bad debts of commercial banks. Previously, we have not considered this as a serious problem, but simply considered a bottleneck of the real estate market. In recent months, the problem of solving the backlog of real estate is considered a serious issue, which has “heated” the parliament at the last session of the National Assembly. This is not just a matter of the real estate market but a negative impact of the real estate market on the monetary and financial markets. The problem is what solution to solve this backlog of real estate. This issue is considered the central task of the Government in the last month of 2012.

In order to solve the backlog of real estate warehouses, ministerial-level state agencies have proposed many solutions to rescue the real estate market. In recent times, the Ministry of Finance and the Ministry of Construction have discussed many measures to remove inventory of real estate. There are solutions that are strongly supported and there are solutions that are highly controversial.

The main proposed solutions include:

- Credit incentives for the demand side to increase solvency.

- Central and local budgets have been included in the spending plan that can be used to buy backlog real estate for official residence, social housing or resettlement housing.

- Subdivide large apartments to reduce the total value of apartments to match the solvency of the demand.

- Converting the functions of some high-class housing projects into commercial and service functions.

- Review ongoing projects to adjust supply.

- Reducing or deferring taxes for real estate businesses that are falling into difficulties…

Outside public opinion on the mechanism to deal with the backlog of real estate also has many notable points. Many people think that it is necessary to give priority to saving real estate investors in the form of direct help, otherwise the real estate market crash will lead to a financial crisis. In essence, saving the economy is not just a matter of saving real estate project investors.

Another stronger opinion is that it is not fair to take the budget capital contributed by the people to real estate investors, otherwise it is unfair. The mechanism that needs to be established is lending only, possibly at a high incentive rate, and the supported investor must return it to the State after the real estate market warms up again. Both of these opinions are reasonable, the problem is that there must be a large-scale bad debt trading company that can handle the amount of debt in this market and it is also important to operate a bad debt trading company like this. How to create common benefits for the whole economy, the real estate market and all people. This is the main and most important thing that policy designers must think and prove with data.

If anyone says that the current real estate market is “frozen” because there are no transactions, it is not true. In fact, affordable housing still has quite a strong transaction power. In Hanoi, Xa La project with the price of about 14 million VND/m2 and Dai Thanh project (Ha Dong) priced at only 10 million VND/m2 both sold out in a very short time. According to the information of the real estate floor system in Ho Chi Minh City. In Ho Chi Minh City, the number of successful transactions for mid- and low-priced real estate products increased quite high, reflecting the trend of the market warming up in this segment. Dai Thanh project bid 10 million VND/m2, causing mixed opinions. One side asserts that this is the right way to do it, a business strategy in the right direction, and can even bring the price to a lower level. The other side asserted that this was a market devaluation.This debate has attracted the participation of the mass media very strongly. By now, the debate over commercial housing discounts is over. A lot of investors have turned their business like Dai Thanh project did and have the ability to bring prices down. This is a good sign of the real estate market. Of course, bringing cheap real estate prices to a lower level is considered an inevitable rule of the market, but it causes significant difficulties for social housing prices approved by state agencies. The price of social housing of the State, formed with many incentives, currently some projects are priced higher than the price of low-cost commercial housing. In fact, to solve this situation is not difficult because housing prices always depend on construction technology, construction materials, management costs,capital mobilization costs… Social housing prices will also decrease if there are better changes in construction, management and capital mobilization.