Foreign banks will face lower risk due to their concentrated lending portfolio, which means they should pay attention to increasing the proportion of loans in some areas. On the other hand, allocating loans to only a few economic sectors seems to reduce the risk exposure for public banks. For the last two forms of ownership the impact of a concentration on profit is inconclusive. In other words, the profitability of these banks is less affected by the level of lending concentration.

1.2.2 Domestic research

All the research topics that the author studied in the context of Vietnam did not find much mention of the loan portfolio and the impact of the loan portfolio on the bank’s profitability. So far, Vietnam has had a number of research projects such as:

Doctoral thesis of author Bui Dieu Anh (2010) “Lending portfolio management at joint stock commercial banks in Vietnam”. The content of this topic studies the theoretical basis of the loan portfolio and the methods of loan portfolio management.

The doctoral thesis of author Ha Van Duong “State management on diversification of credit activities of joint stock commercial banks in Ho Chi Minh City until 2020”. The thesis supplements and completes the theoretical basis and scientific arguments on the diversification of credit activities and the state management of the diversification of credit activities. In particular, apply Ansoff matrix to choose the direction and choose the type of diversification of credit activities. Select criteria to evaluate the results of state management and identify factors affecting the results of state management of diversification of credit activities.

1.3 Purpose, objectives and research tasks of the topic

The purpose of the thesis is to examine in which direction the loan portfolio affects profitability, increasing or decreasing profits at Vietnamese joint stock commercial banks. Based on the identified purpose, the research tasks of the thesis include the following contents:

– First: Study the impact of loan portfolio on profitability of commercial banks.

– Second: Analyze the loan portfolio and the impact of the loan portfolio on the profits of joint stock commercial banks in Vietnam.

– Third: Assess the impact of the loan portfolio on the Bank’s profit.

– Fourth: Proposing solutions and recommendations to improve the loan portfolio to achieve the highest efficiency in the conditions of Vietnam’s joint stock commercial banks.

In order to achieve the above general purpose and research tasks, the aim of the thesis is expressed through solving the following questions:

– First: Theoretically clarify the concept of loan portfolio, classify the types of loan portfolio. What types of loans are included in the loan portfolio? What measures does a portfolio’s concentration measure include? How does portfolio impact return and risk?

– Second: What is the status of the loan portfolio of joint stock commercial banks in Vietnam in the period 2004-2014? How does the loan portfolio affect profit and risk during this period?

– Third: Which model is used to study the impact of loan portfolio on profitability?

– Fourth: In terms of solutions to improve the effective loan portfolio. When building a solution, it is necessary to clarify the orientation to include content, what are the goals of the solutions? In addition to the proposed solutions for joint-stock commercial banks, there are recommendations to create a legal corridor for the improvement of loan portfolio management activities of joint-stock commercial banks, the content and basis of the recommendations. what?

1.4 Subjects and scope of research

– The object of the study is the loan portfolio and its impact on the profitability of commercial banks.

– Research scope: 28 joint-stock commercial banks in Vietnam with data for the period 2004 – 2014. The author uses loan data of banks in the following 11 industries: commerce, agriculture and forestry, manufacturing and outsourcing, construction, personal and community services, warehousing, transportation and communications, education and training, real estate consulting and trading, restaurants and hotels, services finance and other industries.

1.5 Research Methods:

– Synthetic method: using theoretical research on the loan portfolio being applied in developed countries, from which to form the theoretical basis for the topic.

– Research using quantitative method based on regression model of unbalanced panel data. The research methods used pooled regression models (Pooled OLS), fixed effects model (FEM), random effects model (Random Effect Result-REM).

Data were collected from commercial banks in Vietnam during the period from 2004 to 2014. Data on the research variables were collected from the Statistics Department, the State bank, the annual financial statements of the bank. calculated before entering the model. After data is collected, screened and processed by Eviews software to draw conclusions about the relationship as well as the statistical significance of the variables.

1.6 Scientific and practical significance

In terms of science, the topic contributes to the construction of a model to study the impact of loan portfolios on profitability of commercial banks. Currently, there has not been any joint stock commercial bank in Vietnam to conduct this study to properly assess the role of the loan portfolio. In particular, the study will help banks assess the impact of their loan portfolio on profitability, thereby implementing the most effective management of the bank’s loan portfolio.

In practical terms, the research results are a scientific reference to help bank administrators assess the current status of the loan portfolio in Vietnam, which tends to be diversified or concentrated, and the impact of the portfolio on banks. that loan to the bank’s profits increase or decrease. In order to propose solutions and policies to build and manage the most effective loan portfolio, that is, a high-return loan portfolio with a level of risk that the bank can accept. receive.

1.7 Structure of the thesis:

The thesis is divided into 5 chapters

Chapter 1: Introduction

Chapter 2: Theoretical foundations of loan portfolios affecting profitability at commercial banks.

Chapter 3: Current status of loan portfolio and its impact on profitability at Vietnamese joint stock commercial banks.

Chapter 4: Research model and research results.

Chapter 5: Conclusion – Recommendations.

CONCLUSION CHAPTER 1

In summary, chapter 1 of the thesis has outlined an overview of problems to be solved and solutions for those problems. Throughout the following sections of the thesis, the author will step by step look for evidence to answer the original questions. Finally, the structure of this study is given, clearly delineating each next step to achieve the ultimate goal.

CHAPTER 2: THEORETICAL BASIS ON THE IMPACT OF LOANS ON THE PROFIT OF COMMERCIAL BANKS

2.1 Overview of the commercial bank’s loan portfolio

2.1.1 Concepts

The concept of a portfolio has been around since Harry Markowitz’s work on “efficient portfolio theory” was born. Harry Markowitz is a mathematician and an economist who studied the investment process in economics and proposed the Markowitz problem of portfolio optimization. Harry Markowitz has modeled the portfolio selection process under the problem that investors will have more directions to choose their portfolio. According to Harry Markowitz, a portfolio is “a collection of at least two or more risky asset classes”.

According to research by Andreas Kamp (University of Munster), Andreas Pfingsten (Unversity of Munster), Danek Prath (Deutsche Bundesbank) in 2005, a loan portfolio is an investment in risky assets that these observed variables not necessarily directly applicable because banks are financial intermediaries.

According to financial-dictionary ” Loan portfolios are loans that have been made and are waiting to be repaid. Loan portfolios are the principal assets of banks, credit unions, and other lending institutions. The value of a loan portfolio depends not only on the interest rates on the loans, but also on the value and ability to repay those loans.”

According to Wikipedia encyclopedia, a portfolio is “a collection of investments held by an individual or organization including stocks, bonds, gold certificates, real estate, futures contracts, options” to minimize investment risk.

Joint Stock Commercial Bank is a business organization, providing many financial and monetary products, so the asset portfolio of banks is very rich, but with the particularity of being credit intermediaries, bank loans always accounts for a large proportion of the loan portfolio. In commercial banks in countries with underdeveloped financial markets, the profit brought in from lending activities accounts for a very large proportion of total profits, but conversely, in countries with large financial markets, the rate of return from lending activities is very large. Profit from lending is lower, the rest is profit from fee collection. Although the proportion of profit brought in from lending activities at modern commercial banks is not dominant, this is a potentially risky activity because banks have very high financial leverage, only a small percentage of If the loan is not repaid, it can push the bank to the brink of bankruptcy. Therefore, the loan portfolio plays an important role in commercial banks.

Through the concepts of previous studies, the concept of loan portfolio can be introduced as follows: “Lending portfolio is the aggregate of all loans of a bank built at a point in time. Loan portfolio is the largest proportion of banks’ assets, the value of a loan portfolio depends not only on the profitability of the loans but also on the quality of the loans. loan or is the borrower’s ability to repay principal and interest.”

Loan portfolios can be randomly generated or planned. Random loan portfolio is a portfolio formed spontaneously according to customer needs or in other words is led by the market, the bank is in a passive position.

A planned loan portfolio means a portfolio that has been oriented with a proportion of loans designed from the outset. Banks are more proactive in approving loans.

2.1.2 Loan portfolio classification

According to empirical studies, there are two types of loan portfolios in banks around the world, namely, concentrated loan portfolio and diversified loan portfolio.

– Concentrated loan portfolio: is a collection of bank loans concentrated for one or a few economic sectors. Currently, in some countries banks have decided to specialize their lending activities to the areas that they consider to be the most profitable. For example, the study by Benjamin M. Tabak, Dimas M. Fazio and Daniel O, Cajueiro on the impact of loan portfolios on profitability and risk of banks in Brazil 2010. Loan portfolios of banks goods in Brazil are assessed as concentrated. The study assesses that foreign banks have more concentrated loan portfolios than state-owned or private banks. It is explained that foreign banks are familiar with Brazil’s low economic and financial conditions, and therefore they limit their lending activities to a few sectors, in order to benefit more. from reduced monitoring costs.

– Diversified loan portfolio: is a collection of bank loans that are diversified in many different economic sectors. Some countries have regulations that limit the proportion of banks’ lending to a single lender, aiming to diversify the loan portfolio [BIS, 1991, Morris, 2001]. There are several studies that show that the loan portfolios of banks in some countries are highly diversified. Research by Pfingsten and Rudoiph (2002), or Andreas Kamp, Danek Prath and Pfingster (2005) on loan portfolios of banks in Germany from 1970 to 2001, based on 16 industries. Research results show that banks in Germany tend to diversify their loan portfolios, starting from savings banks and cooperative banks, then spreading to small-scale banks (except for small-sized banks). except regional/local banks, branches/agents of foreign banks). In addition, Acharya (2004) studied the loan portfolio of 105 banks in Italy from 1993 to 1999 based on 23 industries, or Elyasiani and Deng (2004) in service companies. Financial services in the United States also concluded that loan portfolios tend to be highly diversified.

The bank’s loan structure is the proportion of outstanding loans to each part of the total outstanding loans, these parts are considered according to many different criteria (geography, term, purpose, type of business). industry, industry, scale, risk level, ..) these components form the structure of the bank’s loan portfolio.

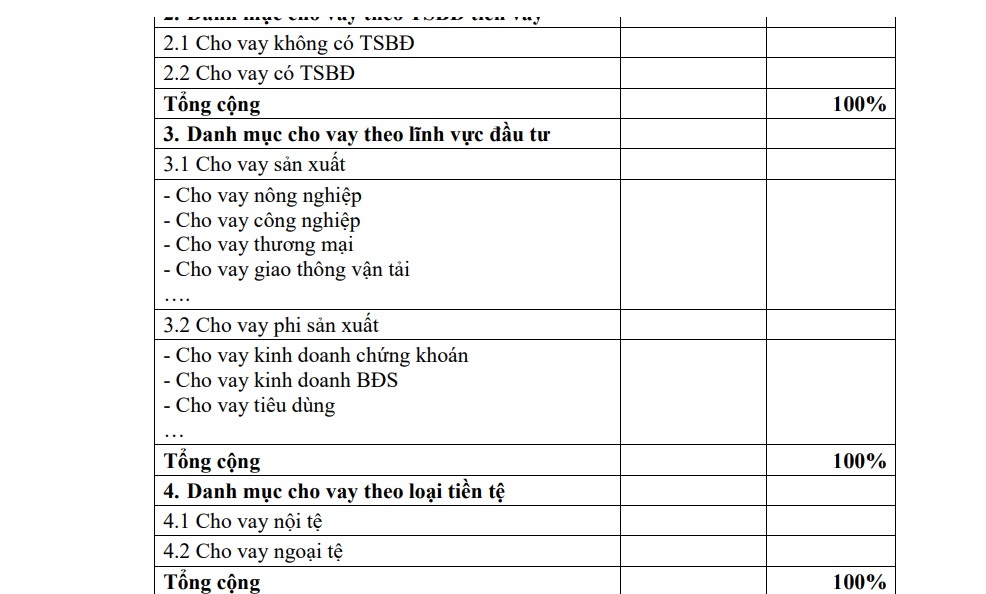

Table 2.1: Structure of commercial banks’ loan portfolio

| Item item | Number money | Billion important |

| 1. Directory term loan | . | . |

| 1.1 Short loans term | . | . |

| 1.2 Medium-term loans | . | . |

| 1.3 Long-term loans | . | . |

| total add | . | 100% |

| 2. Directory loan under collateral money get a loan | . | . |

| 2.1 Loans without collateral | . | . |

| 2.2 Loans with collateral | . | . |

| total add | . | 100% |

| 3. Directory lending by investment sector | . | . |

| 3.1 Product lending export | . | . |

| – Agricultural loans – Industrial loans – Commercial loans – Transport loan download …. | . | . |

| 3.2 Non-product lending export | . | . |

| – Loans for securities business stock – Loans for real estate business – Consumer loans … | . | . |

| Team plus | . | 100% |

| 4. Directory lending by currency | . | . |

| 4.1 Domestic lending bad | . | . |

| 4.2 Foreign loans bad | . | . |

| total add | . | 100% |

| 5. Directory Loans by customer type | . | . |

| 5.1 Enterprises state ownership | . | . |

| 5.2 Company Limited & Neck part | . | . |

| 5.3 Company with 100% capital foreign | . | . |

| 5.4 Joint Venture | . | . |

| 5.5 Combinations cooperative | . | . |

| 5.6 Personal | . | . |

| total add | . | 100% |

| 6. Directory lending by geographical area | . | . |

| 6.1 Area North | . | . |

| 6.2 Area central region | . | . |

| 6.3 Area southern | . | . |

| total add | . | 100% |

| 7. Directory lending by economic sector | . | . |

| 7.1 Agricultural and forestry loans | . | . |

| 7.2 Commercial loans | . | . |

| 7.3 Transport loans load | . | . |

| 7.4 Construction Loans | . | . |

| 7.5 Consumer loans | . | . |

| …. | . | . |

| total add | . | 100% |

Maybe you are interested!

-

Research on the impact of loan portfolios on profitability of joint stock commercial banks - 1

Research on the impact of loan portfolios on profitability of joint stock commercial banks - 1 -

Classification According To Loan Collateral

Classification According To Loan Collateral -

Regression Model Of Benjamin M. Tabak, Dimas M.fazio And Daniel O.cajueiro (2010)

Regression Model Of Benjamin M. Tabak, Dimas M.fazio And Daniel O.cajueiro (2010) -

Improved Competitiveness And Provision Of Banking Services To Better Meet The Needs Of The Economy

Improved Competitiveness And Provision Of Banking Services To Better Meet The Needs Of The Economy

2.1.2.1 Classification by loan term

The object of the bank’s loan is very diverse, stemming from the diverse loan purposes of customers. The object of the loan can be the need for working capital shortage in the production process, the capital need for the purchase of machinery and equipment, the construction of a factory¼ Because each loan object has a different cycle, so require different loan terms. In general, loan terms at commercial banks are usually divided into three groups: short-term, medium-term and long-term.

Short-term loans: are loans with a term of up to 12 months. These loans are often used to cover short working capital of businesses or short-term spending needs of individuals.

Medium-term loans: are loans with a term of 13 to 60 months. Usually medium-term loans are used to finance regular working capital needs, purchase machinery and equipment, build factories of the business or purchase large-value personal assets.

Long-term loans: are loans with a term of more than 60 months. The object of financing of long-term loans is the same as that of medium-term loans.