According to the industry classification criteria of LienVietPostBank, Joint Stock Company A is scored on financial indicators according to the group of medium-sized enterprises, belonging to the group of light industry.

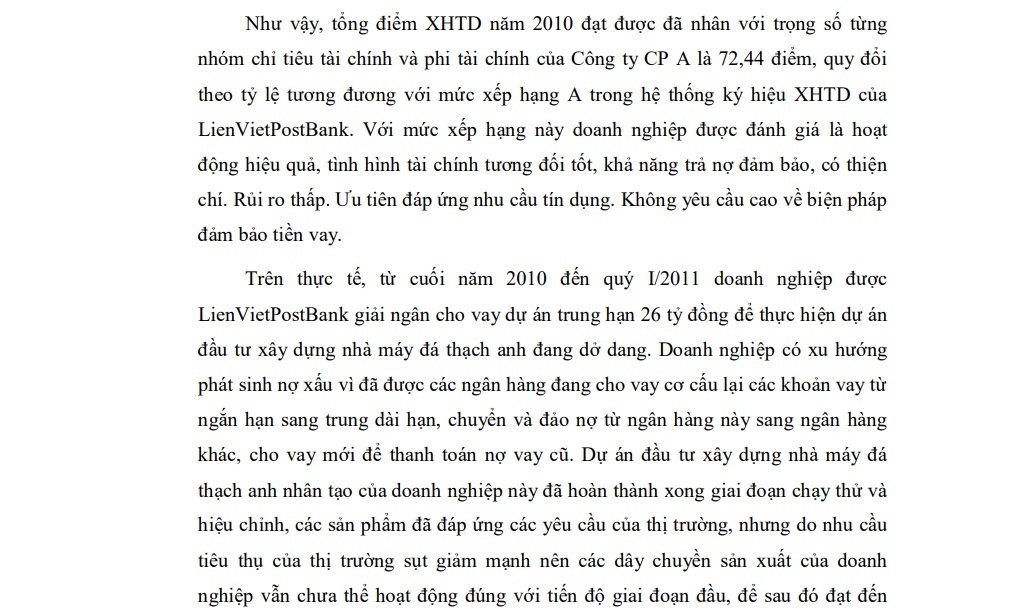

The individual analysis of each financial indicator of Joint Stock Company A shows that compared to industry statistics, the financial capacity of the enterprise is assessed as average. Enterprises diversify products, invest in building a new artificial quartz stone production line, so capital investment in capital construction increases quite quickly, temporarily not serving main business activities. of the enterprise. Based on the scoring criteria and evaluation method in LienVietPostBank’s credit scoring model, Joint Stock Company A is scored on the financial criteria as presented in Table 2.8. The total score of financial indicators after converting the weights of Joint Stock Company A is 56.6 points.

Table 2.8: Scoring of financial indicators of JSC A

| STT | Only title | Single taste | Price value | So with industry average | Score |

| first | Short solvency term | Time | 1.48 | > | 9 |

| 2 | Solvency fast | % | 1.37 | > | twelfth |

| 3 | Growth revenue | % | 1.20 | ~ | 1.2 |

| 4 | Profit growth rate profit | % | 40.48 | > | 6 |

| 5 | Net profit margin | % | 1.16 | < | 1.4 |

| 6 | ROA | % | 0.16 | < | 0.8 |

| 7 | ROE | % | 0.26 | < | 0.8 |

| 8 | Self-funding coefficient | % | 61.55 | > | 15 |

| 9 | Accounts Receivables Turnover collect | Round | 0.20 | < | 1.6 |

| ten | Inventory turnover | Round | 5.53 | > | 6.4 |

| 11 | Working capital turnover | Round | 0.19 | < | 1.6 |

| twelfth | Efficient use of assets | Time | 0.14 | < | 0.8 |

| Total financial score | 56.6 |

(Source: Extracted from LienVietPostBank’s outreach data)

Non-financial indicators include four groups of indicators: Management qualification and internal environment, External factors, Relationship with the Bank and Performance characteristics of the business are scored as presented in Table 2.9. with a total score of 83 points.

Table 2.9: Weighted scores of non-financial indicators of JSC A

| The non-financial factors | Billion important | Points weight | |

| first | Management qualifications and internal environment | 20% | 16.2 |

| 2 | External factors | ten% | 6.6 |

| 3 | Relationship with the Bank | 35% | 32 |

| 4 | Operational characteristics of DN | 35% | 28.2 |

| Total score multiplied number | 83 |

(Source: Lien Viet Post Commercial Joint Stock Bank)

Thus, the total credit score achieved in 2010 has been multiplied by the weight of each group of financial and non-financial indicators of JSC A is 72.44 points, converted at a rate equivalent to the A rating in the system. Credit social symbol system of LienVietPostBank. With this rating, the enterprise is assessed as having efficient operation, relatively good financial position, secured debt repayment capacity, and goodwill. Low risk. Prioritize meeting credit needs. No high requirements on loan security measures.

Maybe you are interested!

-

Similarities Between Edward I. Altman’S Credit Score Model And Standard & Poor’S Credit Rating

Similarities Between Edward I. Altman’S Credit Score Model And Standard & Poor’S Credit Rating -

Lessons From Experience In Credit Relationship For Lienvietpostbank

Lessons From Experience In Credit Relationship For Lienvietpostbank -

Scoring Model Of Corporate Credit Society At Lienvietpostbank’S Branch

Scoring Model Of Corporate Credit Society At Lienvietpostbank’S Branch -

Objectives Of Improving The Credit Rating System Of Lienvietpostbank’S Corporate Customers

Objectives Of Improving The Credit Rating System Of Lienvietpostbank’S Corporate Customers -

Completing the credit rating system of corporate customers at Lien Viet Post Commercial Joint Stock Bank - 9

Completing the credit rating system of corporate customers at Lien Viet Post Commercial Joint Stock Bank - 9 -

Completing the credit rating system of corporate customers at Lien Viet Post Commercial Joint Stock Bank - 10

Completing the credit rating system of corporate customers at Lien Viet Post Commercial Joint Stock Bank - 10

In fact, from the end of 2010 to the first quarter of 2011, the enterprise was disbursed by LienVietPostBank for a medium-term project loan of 26 billion dong to implement an unfinished investment project to build a quartz stone factory. Enterprises tend to incur bad debts because they have been lent by banks to restructure short-term loans to medium-term long-term loans, transfer and reverse debts from one bank to another, provide new loans for payment. old loans. The investment project to build an artificial quartz stone factory of this enterprise has completed the testing and calibration phase, the products have met the requirements of the market, but due to the demand of the market. Due to the sharp decline in the market, the production lines of the enterprise still cannot operate according to the schedule in the first stage, and then reach 100% of capacity. JSC A has shown signs of late payment of principals according to the quarterly repayment schedule and monthly interest payments. Total outstanding loans of this enterprise at banks by the third quarter of 2011 was 41 billion dong.

2.5.2 Second case study: The enterprise is classified as BBB and has incurred overdue debt

The enterprise mentioned in this case study belongs to the type of joint stock company, medium-sized, doing business in the field of construction and installation of industrial and civil works, construction of road traffic works. According to the classification criteria of LienVietPostBank, this enterprise (hereinafter referred to as Joint Stock Company B) belongs to the group of capital construction investment industry. The basic figures on the financial position at the time of ranking in 2010 are presented in Table 2.10. The business results of Joint Stock Company B in 2010 reached a total revenue of 298,630 million VND, profit before tax of 5,359 million VND and profit after tax of 4,796 million VND. Total interest expense paid to the bank in 2010 was VND 2,478 million. The enterprise has an economic relationship with the major shareholder of LienVietPostBank, so the enterprise is given preferential treatment by the bank considering its own special preference for collateral.

Table 2.10: Summary of 2010 balance sheet of B . JSC

| STT | Only title | Single calculus | Numbers money |

| A | Tai> short-term assets | 258.042 | |

| first | Cash and cash equivalents cash equivalents | Million dong | 31.166 |

| 2 | Financial investments short-term main | Million dong | |

| 3 | Receivables | Million dong | 178,818 |

| Of which, payable client | Million dong | 48.079 | |

| 4 | Inventory | Million dong | 42.890 |

| 5 | Other current assets | Million dong | 5.167 |

| B | Tai> fixed assets and long-term investments | 23,688 | |

| first | Long receivables term | Million dong | |

| 2 | Fixed assets | Million dong | 7.246 |

| 3 | Investment real estate | Million dong | |

| 4 | Financial investments long-term main | Million dong | 3,600 |

| 5 | Other long-term assets | Million dong | 12.842 |

| C | Debt payable | 245.053 | |

| first | Short-term debt | Million dong | 244.460 |

| In which, must pay people sell | Million dong | 10,758 | |

| 2 | Long-term liabilities | Million dong | 593 |

| D | Capital owner | 36,677 | |

| Total assets | 281.730 |

(Source: Extracted from LienVietPostBank’s outreach data)

The credit score scoring results of Joint Stock Company B are presented in Tables II.1, II.2, II.3. II.4 and II.5 Appendix II. The total score of weighted financial indicators is 48.4 points and the total score of weighted non-financial indicators is 80.2 points as shown in Table 2.11.

Table 2.11: Weighted scores of non-financial indicators of B . JSC

| The non-financial factors | Billion important | Points weight | |

| first | Management qualifications and internal environment | 20% | 17.8 |

| 2 | External factors | ten% | 6.4 |

| 3 | Relationship with the Bank | 35% | 28.6 |

| 4 | Operational characteristics of the business | 35% | 27.4 |

| Total weighted points | 80.2 |

(Source: Lien Viet Post Commercial Joint Stock Bank)

The total credit score of Joint Stock Company B is 67.48 points, equivalent to the BBB rating as shown in Table 2.12. Enterprises are assessed to operate effectively, have development prospects, have some financial and management limitations, medium risk, can extend credit. Limit the application of preferential conditions. Thorough assessment of the economic cycle and the effectiveness of long-term lending

Table 2.12: Weighted scores of financial and non-financial indicators for credit rating of B . Joint Stock Company

| TT | Only title | Points unweighted | Points weight multiplied | Billion important |

| first | Financial indicators | 48.4 | 19.36 | 40% |

| 2 | Non-financial indicators | 80.2 | 48.12 | 60% |

| 100% | ||||

| Total score | 67.48 | 100% |

(Source: Lien Viet Post Commercial Joint Stock Bank)

Total bank loans of Joint Stock Company B by the end of the third quarter of 2011 was 93,545 million dong, an increase of 34,133 million dong compared to the time of credit association according to 2010 data for loan appraisal. By September 2011, JSC B had incurred overdue debt at LienVietPostBank due to late payment of loan interest. Currently, this business has paid off all loan interest to the bank and is in a challenging period to be able to move back to the qualified debt group. The situation of inflation, high interest rates, prolonged freezing of the real estate market, adverse fluctuations of the world economy; These factors have a spillover effect on the consumption of products of JSC B in 2011 and the following period. In addition, the situation of late payment of debts to major partners of the company will directly affect the business operations and the ability to repay loans of the enterprise, putting banks in a situation where they must consider restructure loans when they are due.

2.6 Evaluation of business credit rating system of LienVietPostBank

LienVietPostBank’s credit system has greatly contributed to the screening and classification of corporate customers, thereby helping the bank to reduce the credit risk ratio within the allowable level. The results of corporate credit are used by the Bank’s Executive Board and Business Council to determine the maximum credit limit for each customer, the application of loan interest rates, and regulations on collateral assets. and some other preferential policies for customers.

Since the application of the credit system at the end of 2008 and the first amendment of the credit system in 2010, credit extension activities at LienVietPostBank have recorded many positive results. Thanks to the reasonable assessment of the customer’s credit rating, LienVietPostBank’s business units have proactively adopted preferential policies for borrowers, screened and marketed corporate customers with high credit ratings, thereby increasing their competitiveness. Compared with other commercial banks according to the business customer market segment, both in terms of lending interest rates, incentives for collateral, service fees, appraisal time, …. Therefore, LienVietPostBank’s outstanding loan has grown quite well over the years. from year to year, from the market loan balance in 1 in 2009 was 5,423 billion dong, in 2010 it was 14,047 billion dong and in 2011 it was 17,399 billion dong.

Besides the above positive aspects, in some cases, LienVietPostBank’s current situation of credit society of corporate customers has not yet accurately assessed the current level of credit society, credit risk as well as forecasted development prospects of the business. This leads to the data on the overdue debt ratio at the bank not accurately reflecting international practices, the level of provision for credit risks has not yet ensured the current role of protecting against credit risks. and in the future for the bank.

In general, the current enterprise credit system of LienVietPostBank is relatively suitable and overcomes the subjective in scoring quantitative indicators by including non-financial indicators. However, from the above research, it also shows that the corporate credit system has limitations that need to be further improved to meet the needs of credit risk management and in accordance with international standards.

2.6.1 Achievements

The internal credit rating model in general and corporate credit rating in particular is an optimal risk management tool in the process of credit appraisal and scoring. Through the advice of domestic banking and finance experts, LienVietPostBank has built and is gradually perfecting the corporate credit model applied in business units, this model is relatively consistent with the standards. are used by credit organizations in the world and the guidance of the State Bank. LienVietPostBank’s corporate credit model follows quite strict and strict procedures and criteria, including: a system of evaluation criteria and weighted scores; how to determine the value of each evaluation criterion; how to convert the value to points of the evaluation criteria; way of credit socialization of corporate customers and the point of view of credit granting, the accompanying incentives for each rating level.

LienVietPostBank’s credit system is built according to its own credit activities and development strategy. With the credit system, the measurement and format of credit risks at LienVietPostBank are uniformly implemented. In general, the scoring model for corporate customers in the credit system of LienVietPostBank still follows the guideline framework of the State Bank but has been adjusted based on the ranking experience of domestic commercial banks and credit institutions in the world. . The scoring model of non-financial indicators for corporate customers at branches has been included in the group of indicators for forecasting the impact of changes in State policies and forecasting the impact of competition on the business sector. This is an improvement point to enhance the ability to predict the risk of future financial difficulties of rated customers.