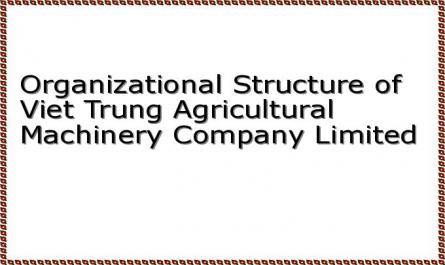

Diagram 2.1: Organizational structure of Viet Trung Agricultural Machinery Company Limited

Manager

Deputy Director

economic responsibility

Deputy Director

production responsibility

Room

accountant

Business room

business

Organization and administration department

main

Next room

plan

Technical room

technique

( Source: Organization and Administration Department)

Functions and tasks of each department

Director : Overall responsibility for the company's production and business activities, decides on policies, sets goals, directions and annual production and business plans of the company. Leads meetings and reviews the company's operations and business results.

Deputy Director in charge of economics : Directly manages three departments: accounting department, administrative department, and business department. Make business plans, organize monthly, quarterly, and annual inspections of operations in the area under his/her charge, calculate and balance input and output business situations.

Deputy Director in charge of production : Directly direct two departments: planning department, technical department. Manage planning as well as quality management, control all planning, technical and production activities of the whole company. Directly manage and control the implementation of production of workshops according to schedule. Research and apply technical advances to production, organize and improve labor skills.

Administrative Department: In charge of human resources and administrative issues, keeping documents related to company establishment, and solving problems for employees.

27

Accounting Department : Calculate the value of imported and exported products, declare taxes to the state. Ensure the import of raw materials, components, and supplies. Conduct tax deductions at the customs department, monitor the application of new tax policies of the government.

Sales Department: Manage sales, confirm sales and orders from customers. Place orders and manage customer quantities.

Planning Department: Make plans for product consumption investment, in charge of planning import and export of raw materials, components, tools and equipment.

Technical Department: Controls the quality of production equipment, maintains records of product quality. At the same time, the technical department is also the department that researches new applications of new technology in production so that new products of good quality can be produced.

2.2. Production and business situation at Viet Trung Agricultural Machinery Company Limited in the period of 2011-2013

2.2.1. The company's production and business performance in the period 2011-2013

From Table 2.1, we can see that in the period 2011-2012, the company's revenue from selling goods decreased by 157,543,038,381 VND compared to 2011, corresponding to 36.06 , while the cost of goods sold in 2012 was 211,162,178,655 VND, a decrease of 166,338,185,421 VND, corresponding to 44.06 . The decrease in revenue is also similar to the decrease in cost of goods sold, proving that in 2012, the company sold fewer goods, so fewer goods were produced. The lower production also reduced costs, such as financial costs and business management costs. In particular, the interest expense in 2012 decreased by nearly 2 billion compared to the previous year, showing that business encountered more difficulties, forcing the company to pay off loans to reduce costs for the company. However, in 2012, the company's other income increased by 339,405,860 VND, equivalent to an increase of 72.13%, due to the company liquidating old assets to replace them with other assets with higher technology to launch newer products. Moreover, the company's revenue deductions increased by 31,580,589,630 VND, equivalent to 309.52%. The reason is that in 2012, the financial market was more difficult, and there were more competitors, forcing the company to offer trade discounts and reduce sales prices to attract customers so that there would be no inventory in the company and production would not be interrupted. This caused the company's profit to drop sharply to negative VND 3,703,139,021 and from there the corporate income tax also dropped to VND 0.

28

Table 2.1. Business performance results of Viet Trung Agricultural Machinery Company Limited in the period 2011-2013

Unit: Dong

STT

Target | Year | Difference in 2012 compared to 2011 | Difference in 2013 compared to 2012 | |||||

2011 | 2012 | 2013 | Value | | Value | | ||

1 | Sales revenue | 436,888,723,600 | 279.345.685.219 | 244.364.837.374 | (157,543,038,381) | (36.06) | (34,980,847,845) | |

2 | Revenue deduction | 10,209,545,458 | 41,790,135,088 | 41,111,983,951 | 31,580,589,630 | 309.32 | (678,151,137) | |

3 | Net revenue | 426.679.178.142 | 237.555.550.131 | 203.252.853.423 | (189.123.628.011) | (44.32) | (34,302,696,708) | |

4 | Cost of goods sold | 377,500,364,076 | 211.162.178.655 | 184.460.018.665 | (166,338,185,421) | (44.06) | (26,702,159,990) | |

| Gross profit | 49,178,814,066 | 26,393,371,476 | 18,792,834,758 | (22,785,442,590) | (46.33) | (7,600,536,718) | |

| Revenue from the contract | 263,772,477 | 171,269,436 | 23,787,868 | (92,503,041) | (35.07) | (147,481,568) | |

7 | Financial costs | 34,904,856,050 | 21,139,121,759 | 12,571,936,187 | (13,765,734,291) | (39.44) | (8,567,185,572) | |

8 | In which: Interest expense | 24,834,801,897 | 19,665,450,834 | 11,477,924,116 | (5,169,351,063) | (20.81) | (8,187,526,718) | |

9 | Business management costs | 11,382,410,869 | 9,014,980,240 | 8,210,400,530 | (2,367,430,629) | (20.80) | (804.579.710) | |

10 | Net operating profit production and business | 3,155,319,624 | (3,589,461,087) | (1,965,714,091) | (6,744,780,711) | (213.76) | 1,623,746,996 | |

11 | Other income | 470,546,366 | 809.952.226 | 149,079,611 | 339,405,860 | 72.13 | (660,872,615) | |

12 | Other costs | 1,852,040,197 | 923.630.160 | 1,073,840,622 | (928,410,037) | (50.13) | 150,210,462 | |

13 | Other profits | (1,381,493,831) | (113,677,934) | (924.761.011) | 1,267,815,897 | (91.77) | (811,083,077) | |

14 | Profit before tax | 1,773,825,793 | (3,703,139,021) | (2,890,475,102) | (5,476,964,814) | (308.77) | 812,663,919 | |

1 | Corporate income tax business payable | 443,456,448 | 0 | 0 | (443,456,448) | (100) | 0 | 0 |

1 | Profit after tax | 1,330,369,345 | (3,703,139,021) | (2,890,475,102) | (5,033,508,366) | (378.35) | 812,663,919 | |

Maybe you are interested!

-

Organizational Chart of Lien Viet Post and Commercial Joint Stock Bank

Organizational Chart of Lien Viet Post and Commercial Joint Stock Bank -

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch -

Organizational Structure of Son Ha Garment Joint Stock Company

Organizational Structure of Son Ha Garment Joint Stock Company -

Organizational Structure of Social Relief Activities in Vietnam.

Organizational Structure of Social Relief Activities in Vietnam. -

Organizational Structure of Management Apparatus: The Organizational Model and Operation of the Nghe An Provincial People's Credit Fund is Shown in Diagram 3.1. Below.

Organizational Structure of Management Apparatus: The Organizational Model and Operation of the Nghe An Provincial People's Credit Fund is Shown in Diagram 3.1. Below.

Source: Business performance report 2011-2013

29

Chart 2.1. Revenue growth, cost of goods sold and profit of Viet Trung Agricultural Machinery Company Limited in the period 2011-2013

Unit: Million VND

2011

2012

2013

450,000,000,000

400,000,000,000

350,000,000,000

300,000,000,000

250,000,000,000

200,000,000,000

revenue cost

net profit

150,000,000,000

100,000,000,000

50,000,000,000

0

-50,000,000,000

Source: Business results report 2011-2013 Period 2012-2013, in 2013 the company's revenue from supplying goods was 244,364,837,374 VND, down 34,980,847,845 VND, equivalent to 12.52 compared to 2012. Along with that, in 2013 the cost of goods sold decreased by 26,702,159,990 VND, equivalent to 12.65 . We can see that the rate of decrease in revenue and the rate of decrease in cost of goods sold are at the same level, proving that the business of the enterprise is showing signs of decline. Less goods sold has made the enterprise more cautious and produce less to avoid having a lot of goods in stock. Along with the decrease in sales revenue, the revenue from financial activities and business management costs of the enterprise decreased significantly due to fewer sales, so the income from payment discounts also decreased as well as the reduction in sales costs and other costs.

30

Other expenses for business services such as electricity and water. However, in 2013, the company significantly reduced the interest expense in the company to 8,187,526,718 VND, equivalent to 41.63%. It can be said that while the company is having difficulties in doing business, paying off loans will help the company save a large amount of interest and increase the company's profit to 812,663,919 VND, equivalent to 21.95%. However, this increase still makes the profit of Viet Trung Agricultural Machinery Company Limited negative and does not increase the company's income tax expense. But on the other hand, it also shows the company's saving policy in difficult economic times.

2.2.2. Asset and capital situation at Viet Trung Agricultural Machinery Company Limited in the period of 2011-2013

2.2.2.1. Asset situation at Viet Trung Agricultural Machinery Company Limited in the period of 2011-2013

From Table 2.2, we can see that after three years from 2011 to 2013, the asset size of Viet Trung Agricultural Machinery Company Limited has decreased significantly. From 2011 to 2012, the total assets of the enterprise decreased by 81,488,242,687 VND, equivalent to 29.17%. The reason for this sharp decrease is that the inventory and receivables of the enterprise in 2012 decreased sharply compared to 2011. The decrease in revenue and difficult business have caused the enterprise to produce moderately, so the inventory has also decreased significantly to avoid the enterprise having to bear the costs of storing goods as well as the quality of goods being reduced due to being left in the warehouse for a long time. Moreover, customers buy less goods, so the amount of money owed to customers is also reduced. From 2012 to 2013, the total assets of the enterprise decreased by 10,613,693,188 VND, equivalent to 5.36%. It can be said that 2013 was still a year of loss for the enterprise, but it showed some signs of recovery, so the enterprise also calculated to increase its inventory to take advantage of opportunities. However, the increase in inventory as well as some items in the enterprise's asset structure was not equal to the decrease in receivables and long-term assets, so the total assets of the enterprise still decreased.

31

Table 2.2. Asset situation at Viet Trung Agricultural Machinery Company Limited in the period 2011-2013

Unit: Dong

Target

2011 | 2012 | 2013 | Difference in 2012 compared to 2011 | Difference in 2013 compared to 2012 | |||

Value | | Value | | ||||

Asset | |||||||

A. Current assets | 258.121.529.157 | 180.314.976.010 | 171,077,744,695 | (77,806,553,147) | (30.14) | (9,237,231,315) | (5.12) |

1. Cash and cash equivalents | 4,526,335,114 | 9,056,779,218 | 10,592,192,477 | 4,530,444,104 | 100.09 | 1,535,413,259 | 16.95 |

Cash | 1,458,205,212 | 1,515,623,168 | 1,489,233,179 | 57,417,956 | 3.94 | (26,389,989) | (1.74) |

Bank deposit | 3,068,129,902 | 7,541,156,050 | 9,102,959,298 | 4,473,026,148 | 145.79 | 1,561,803,248 | 20.71 |

2. Short-term receivables | 46,173,922,881 | 23,932,904,318 | 9,940,071,048 | (22,241,018,563) | (48.17) | (13,992,833,270) | (58.47) |

Accounts receivable | 45,172,585,307 | 23.248.134.013 | 8,781,023,400 | (21,924,451,294) | (48.53) | (14,467,110,613) | (62.23) |

Prepayment to seller | 636,957,755 | 655,498,865 | 1,100,015,258 | 18,541,110 | 2.91 | 444,516,393 | 67.81 |

Other receivables | 364,379,819 | 29,271,440 | 59,032,390 | (335,108,379) | (91.97) | 29,760,950 | 101.67 |

3.Inventory | 199.847.804.615 | 146,704,721,667 | 149,847,071,655 | (53,143,082,948) | (26.59) | 3,142,349,988 | 2.14 |

4. Other short-term assets | 7,573,466,547 | 620,570,807 | 698.409.515 | (6,952,895,740) | (91.81) | 77,838,708 | 12.54 |

VAT deductible | 7,495,448,120 | 527,280,532 | 349,427,610 | (6,968,167,588) | (92.97) | (177,852,922) | (33.73) |

Other current assets | 59,424,427 | 93,290,275 | 348,981,905 | 33,865,848 | 56.99 | 255,691,630 | 274.08 |

B. Long-term assets | 21,229,982,206 | 17,548,292,666 | 16,171,830,793 | (3,681,689,540) | (17.34) | (1,376,461,873) | (7.84) |

1. Fixed assets | 21,017,147,919 | 17,431,773,332 | 16,072,688,374 | (3,585,374,587) | (17.06) | (1,359,084,958) | (7.80) |

Original price | 48,051,124,385 | 48,862,864,385 | 51,279,665,701 | 811,740,000 | 1.69 | 2,416,801,316 | 4.95 |

Accumulated depreciation | (27,502,754,002) | (31,431,091,053) | (35,206,977,327) | (3,928,337,051) | 14.28 | (3,775,886,274) | 12.01 |

2. Other long-term assets | 212,834,287 | 116,519,334 | 99,142,419 | (96,314,953) | (45.25) | (17,376,915) | (14.91) |

Total assets | 279,351,511,363 | 197.863.268.676 | 187.249.575.488 | (81,488,242,687) | (29.17) | (10,613,693,188) | (5.36) |

Source: Balance sheet 2011-2013

32

Chart 2.2. Asset ratio of Viet Trung Agricultural Machinery Company Limited

2011-2013 period

2011

92.40%

7.60%

2012

91.13%

8.87%

2013

91.36%

8.64%

Current Asset Ratio

long term asset ratio

Source: Balance sheet 2011-2013

From the chart, we can see that in all 3 years, the proportion of the company's short-term assets accounted for a large proportion of total assets. In 2011, the proportion of short-term assets was 92.40%, in 2012 it was 91.13% and in 2013 it was 91.36%. In general, the proportion of short-term assets did not change much, but there were still certain changes. With additional investment in machinery to improve product quality, fixed assets in 2013 and 2012 both increased. Along with that, the company's short-term assets also decreased significantly due to a decrease in receivables, especially receivables from customers. This is because in recent years the company has sold fewer products, leading to a decrease in receivables. However, in 2013, inventories and other short-term assets increased but not much and still caused the ratio of short-term assets to decrease. As a manufacturing enterprise, the ratio of short-term assets accounts for a large part of total assets because the company's manufacturing company does not use many high-value machines but mainly workers who work based on their experience in welding and assembling to complete the product. Along with that, the company's factory system is not too large, the warehouse is mainly rented from outside, so the company's long-term assets are not much.

2.2.2.2. Capital situation at Viet Trung Agricultural Machinery Company Limited in the period of 2011-2013

33

Table 2.3. Capital situation at Viet Trung Agricultural Machinery Company Limited in the period of 2011-2013

Unit: Dong

Target

2011 | 2012 | 2013 | Difference in 2012 compared to 2011 | Difference in 2013 compared to 2012 | |||

Value | % | Value | % | ||||

A. Liabilities | 222.060.047.789 | 145,625,991,050 | 138,685,812,350 | (76,434,056,739) | (34.42) | (6,940,178,700) | (4.77) |

1. Short-term debt | 222.002.053.849 | 145,625,991,050 | 138,685,812,350 | (76,376,062,799) | (34.40) | (6,940,178,700) | (4.77) |

Short term loan | 150,474,235,560 | 105,536,004,977 | 102.830.460.974 | (44,938,230,583) | (29.86) | (2,705,544,003) | (2.56) |

Payable to seller | 55,839,059,000 | 2,094,376,149 | 29,303,541,929 | (53,744,682,851) | (96.25) | 27,209,165,780 | 1,299.15 |

Buyer pays in advance | 7,741,902,139 | 36,163,494,015 | 4,913,567,525 | 28,421,591,876 | 367.11 | (31,249,926,490) | (86.41) |

Taxes and other payments to the state | 5,581,758,722 | 637.121.555 | 1,377,100 | (4,944,637,167) | (88.59) | (635,744,455) | (99.78) |

Payable to labor | 1,098,913,102 | 928,938,890 | 978,272,437 | (169,974,212) | (15.47) | 49,333,547 | 5.31 |

Cost to Pay | 1,233,747,326 | 233,617,464 | 626.154.385 | (1,000,129,862) | (81.06) | 392,536,921 | 168.03 |

Other short-term payables | 32,438,000 | 32,438,000 | 32,438,000 | 0 | 0 | 0 | 0 |

2. Long-term debt | 57,993,940 | 0 | 0 | (57,993,940) | (100) | 0 | 0 |

B. Equity | 57,291,463,574 | 52,237,277,626 | 48,563,763,138 | (5,054,185,948) | (8.82) | (3,673,514,488) | (7.03) |

1.Equity | 56,075,882,226 | 51,450,499,678 | 48,222,558,190 | (4,625,382,548) | (8.25) | (3,227,941,488) | (6.27) |

Owner's equity | 29,850,000,000 | 29,850,000,000 | 29,850,000,000 | 0 | 0 | 0 | 0 |

Undistributed profit after tax | 22,116,178,503 | 17,470,625,931 | 14,242,684,443 | (4,645,552,572) | (21.01) | (3,227,941,488) | (18.48) |

Equity funds | 4,129,873,747 | 4,129,873,747 | 4,129,873,747 | 0 | 0 | 0 | 0 |

2.Welfare reward fund | 1,215,581,348 | 786,777,948 | 341,204,948 | (428,803,400) | (35.28) | (445,573,000) | (56.63) |

Total capital | 279,351,511,363 | 197.863.268.676 | 187.249.575.488 | (81,488,242,687) | (29.17) | (10,613,693,188) | (5.36) |

Source: Balance sheet 2011-2013

34

Through the table above, we can see that the company's capital has decreased over the years. From 2011 to 2012, the company's total capital decreased by 81,488,242,687 VND, of which short-term debt decreased by 76,376,062,799 VND, accounting for almost all of the decrease in total capital. The business loss in 2012 forced the company to cut short-term debt to reduce the company's interest expenses. The decrease in profits also led to a reduction in bonus funds, making the owner's equity decrease. In 2013, the total capital decreased by 10,613,693,188 VND, equivalent to 5.36% compared to 2012. In 2013, the company continued to cut short-term loans to reduce interest expenses. However, the business is able to take more from the seller, which shows that the business has more trust from the suppliers. The number of customers paying in advance has decreased because of the difficult economy, so customers are more careful with their money and pay less in advance.

Chart 2.3. Short-term debt ratio at Viet Trung Agricultural Machinery Company Limited in the period 2011-2013

2011 2012

20.51%

79.49%

26.40%

73.60%

2013

25.94%

75.06%

Debt ratio

equity ratio

Source: Balance sheet 2011-2013

From the chart, we can see that the proportion of liabilities accounts for the majority of total capital and is mainly short-term debt. That is, the company does not mobilize long-term debt to serve its business activities (except in 2011, the company mobilized long-term debt but not much). Because in recent years, the economy has fallen into crisis. Banks have limited long-term lending due to the high possibility of capital loss. Therefore, the company cannot find long-term funding sources or if it does find

35

If it is possible, the cost of using it is very high, so the company decided to use all short-term financing sources. Using all short-term debt has reduced the interest expense for the company, thereby contributing to increasing the company's profits. In 2011, the proportion of short-term debt was 79.47%, in 2012 it was 73.60%, in 2013 it was 75.06%, showing that the company is cutting down on debt to reduce interest expenses for the company, helping the company gain more profits. The high proportion of short-term debt shows that the company is managing debt in a radical way. Debt management in a radical way has many advantages such as: reduced cash turnover time, lower costs than long-term sources, because of the high-risk strategy, the required income is high. However, this policy also has the disadvantage that the company may fall into a state of insolvency in the short term.

2.2.3. Some general financial indicators

Table 2.4. General financial indicators

Unit: %

Target

Calculation formula | 2011 | 2012 | 2013 | |

ROS | Profit after tax Net revenue | 0.31 | (1.56) | (1.42) |

ROA | Profit after tax Total assets | 0.48 | (1.87) | (1.54) |

ROE | Profit after tax Equity | 2.32 | (7.09) | (5.95) |

Performance total assets | net revenue Total assets | 153 | 120 | 109 |

Source: Business performance report - balance sheet 2011-2013 Return on sales (ROS): Indicates how much profit is generated for every 100 dong of net revenue. In 2011, every 100 dong of net revenue generated 0.31 dong of profit. In 2012, every 100 dong of net revenue, the company lost 1.56 dong, down 1.87 dong. In 2012, the rate of decrease in net revenue was 44.32% while the rate of decrease in after-tax profit was 378.35%. After-tax profit decreased more sharply than net revenue, causing ROS in 2012 to decrease significantly. In 2013, every 100 dong, the company lost 1.42 dong, up 0.14 dong. The ROS coefficient increased because net revenue decreased less than last year while expenses decreased.

The decrease in profit after tax has reduced the rate of decrease.

Return on assets (ROA): Shows how much profit after tax is generated for every 100 dong of total assets. In 2011, 100 dong of total assets generated 0.48 dong of profit after tax. In 2012, 100 dong of total assets resulted in a loss of 1.87 dong.

36

2.35 dong. In 2012, the rate of decrease of total assets was 29.17%, the rate of decrease of profit after tax was 378.35%, a sharper decrease than the rate of decrease of total assets, causing ROA in 2012 to decrease sharply. In 2013, for every 100 dong of total assets, there was a loss of 1.54 dong, profit after tax increased by 0.33 dong. Because in 2013, total assets decreased by 5.36% and the rate of decrease of profit after tax was %, both of which were smaller decreases than in 2012, ROA increased. This proves that the company's use of assets is more effective.

Return on equity (ROE): shows how much profit after tax is generated for every 100 dong of equity. In 2011, 100 dong of equity generated 2.32 dong of profit after tax. In 2012, 100 dong of equity lost 7.09 dong, a decrease of 9.41 dong compared to 2011. Because in 2011, profit after tax decreased by 378.35%, equity decreased by 8.82%, causing ROE to decrease sharply. In 2013, 100 dong of equity lost 5.95 dong, an increase of 1.14 dong compared to 2012. Because in 2012, profit after tax increased more than the growth rate of equity.

Total asset utilization efficiency: Indicates how much revenue 100 dong of assets generated. In 2011, 100 dong of assets generated 153 dong of revenue. In 2012, 100 dong of assets generated 120 dong of revenue, a decrease of 33 dong compared to 2011. Due to the decrease in revenue in 2012 combined with the increase in revenue deductions, the company's asset utilization efficiency decreased. In 2013, 100 dong of assets generated 109 dong of revenue. This shows that the use of assets to generate revenue is getting worse, so policies are needed to boost revenue.

2.3. Current status of short-term asset management at Viet Trung Agricultural Machinery Company Limited in the period 2011-2013

2.3.1. Analysis of the scale and structure of short-term assets

Chart 2.4. Size of short-term assets

Unit: Dong

258.121.529.157

180.314.976.010

171,077,744,695

300,000,000,000

250,000,000,000

200,000,000,000

150,000,000,000 Current assets

100,000,000,000

50,000,000,000

0

2011 2012 2013

Source: Balance sheet 2011-2013

37

From the chart of short-term assets, we can see that the company's short-term assets are shrinking. In 2011, total short-term assets were 258,121,529,157 VND. By 2012, short-term assets were 180,314,976,010 VND, down 77,806,553,147, equivalent to a decrease of 30.14%. It can be seen that this is a sharp decrease. This is because in 2012, the business suffered a loss, the profit was negative, so the company's assets were significantly reduced, leading to a decrease in short-term assets. In 2013, this indicator was 171,077,744,695 VND, down 9,237,231,315, equivalent to a decrease of 5.12% compared to the previous year. This reflects that the company has shown that its business situation has improved. Current assets decreased, but less than last year. However, this decrease shows that the company's business is not effective and needs more positive changes.

Chart 2.5. Short-term asset structure

2.93%

1.76%

17.89%

77.42%

2011 2012

13.27%

81.36%

0.35%

5.02%

0.40%

2013

6.19%

5.81%

cash and cash equivalents

receivables

inventory

89.60%

Other current assets

Source: Balance sheet 2011-2013

38