business according to assigned tasks. In addition, each room has a function that is both

coordinate and support each other in assigned work.

Vice president

Planning Department

business

Accounting Department

treasury

Manager

According to the regulations on organization and operation of the Vietnam Bank for Agriculture and Rural Development Branch issued under Decision No. 454/QD/HDQT-TCCB dated December 24, 2004, the organization, functions and tasks of each department and office are specified as follows:

Diagram 2.1: Organizational structure of Agribank Minh Hoa district branch. Note:

: Online Relationship

: Functional relationship

Table 2.1: Agribank personnel situation, Minh Hoa district, Bac Quang Binh

Compare | |||||||

Target | 2014 | 2015 | 2016 | 2015/2014 | 2015/2014 | ||

+/- % | +/- % | ||||||

Total | 14 | 15 | 16 | 1 7.14 | 1 6.67 | ||

By degree | |||||||

Master | 0 | 1 | 1 | 1 | 100 | 0 | 0 |

University | 12 | 13 | 14 | 1 | 8.33 | 1 | 7.69 |

College | 0 | 0 | 0 | ||||

Intermediate | 2 | 1 | 1 | -1 | -50 | 0 | 0 |

By gender | |||||||

Male | 9 | 10 | 10 | 1 | 11.11 | 0 | |

Female | 5 | 5 | 6 | 0 | 1 | 20 | |

Maybe you are interested!

-

Customer Evaluation Results on Tangible Facilities of Agribank – Minh Hoa District Branch

Customer Evaluation Results on Tangible Facilities of Agribank – Minh Hoa District Branch -

Organizational Structure and Management of Agribank Ha Nam Province Branch

Organizational Structure and Management of Agribank Ha Nam Province Branch -

General Overview of Agribank Branch in Trieu Son District - Thanh Hoa

General Overview of Agribank Branch in Trieu Son District - Thanh Hoa -

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch -

Organizational Structure of Son Ha Garment Joint Stock Company

Organizational Structure of Son Ha Garment Joint Stock Company

(Source: Agribank Accounting and Treasury Department, Minh Hoa District, Bac Quang Binh)

Through table 2.1 we can see the personnel situation of Agribank Minh Hoa district branch.

North Quang Binh as follows:

In 2015, the number of staff in the unit was 15 people, an increase of 7.14% compared to 2014. In 2016, the number of staff increased by 6.67% compared to 2015. Due to the nature of the management area of the unit, being a monopoly unit, each year an additional staff is added to release and provide services to customers faster and better. In terms of education level, over the years, the number of staff has increased. In addition, in terms of gender from 2014 - 2016, the gender gap in the unit is still dominant. This is consistent with the nature of the work required by the banking industry.

2.1.3. Business performance results at the Bank for Agriculture and Rural Development of Vietnam, Minh Hoa District Branch, Bac Quang Binh (Agribank, Minh Hoa District Branch, Bac Quang Binh)

2.1.3.1. Indicators of total mobilized capital, total outstanding credit, total assets

Minh Hoa is a mountainous district located in the northwest of Quang Binh province. The West borders the Lao People's Democratic Republic with 89 km of border, the North borders Tuyen Hoa district, the South and Southeast borders Minh Hoa district. The whole district has 15 communes and 1 town with a natural area of 1,410 km2. The population is over 49 thousand people, of which the working-age population is over 27 thousand people. Minh Hoa has the majority of Kinh people and ethnic minorities Bru - Van Kieu, Chut with

6,500 people, concentrated in border communes (Dan Hoa, Trong Hoa, Thuong Hoa and Hoa Son). The district has many potentials and strengths. The district has Chalo - Na Phau international border gate, important traffic routes and hubs such as Ho Chi Minh road running the entire length of the district, road 12C is the shortest route connecting the northeastern provinces of Thailand through Laos, to National Highway 1A, to Hon La seaport (Quang Binh), Vung Ang port (Ha Tinh). Besides, Minh Hoa also has many historical relics such as Da Deo pass, Mu Da, Ngam Rinh, Khe Ve, Chalo, Cong Troi..., natural forests, beautiful mountains and rivers that can be built into eco-tourism areas such as Tu Lan cave in Tan Hoa, Thac Mo in Hoa Hop, Nuoc Rung in Dan Hoa, north of Da Deo pass and caves in Thuong Hoa, Hoa Tien, Hoa Thanh. These are favorable conditions for developing production of goods, trade, export services.

import, promote cooperation and economic exchange between the locality and economic regions in the province, domestically and internationally. The district has all economic sectors such as: agriculture, forestry, fishery, salt industry, industry, handicrafts, commerce and services...

The economic situation in the area is developing steadily in both scale and output. On the other hand, the Bank for Agriculture and Development of Vietnam is creating many favorable conditions for the Branch to expand its credit scale and invest in serving economic development in the area. The Party and local government always create favorable conditions for the Branch to operate. Thereby, we can see that Agribank Minh Hoa Bac Quang Binh branch has extremely favorable points in business activities, which are a large market and favorable socio-economic conditions.

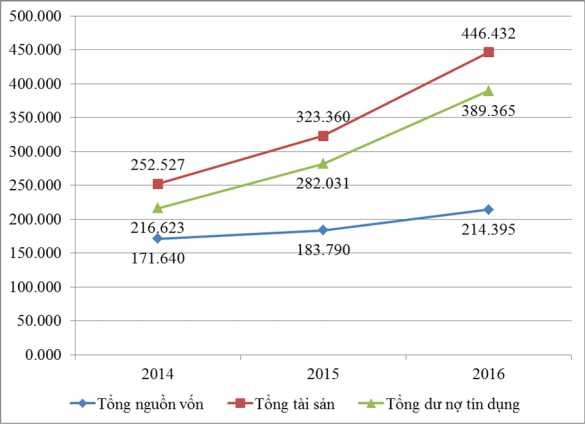

Chart 2.1: Performance indicators at Agribank Minh Hoa district branch

(Source: Business performance report 2014-2016)

Despite the unfavorable economic situation, the Bank has maintained the growth rate of total assets over the years during the period from 2014 to 2016.

to 2016. In 2014, total assets reached VND 252,527 million. In 2015, a difficult and challenging year when bank interest rates increased to control inflation, the Bank's total assets still increased by 70.833% and reached VND 323,360 million. In 2016, a series of bank mergers took place, but the Bank's business results still had a significant improvement. Total assets in the year increased by 123.072%, reaching VND 446,432 billion.

Over the years, Agribank Minh Hoa District branch has also steadily increased its mobilized capital. Specifically, in 2014, the total mobilized capital was 171,640 million VND. In 2015, despite the economy facing many continuous difficulties in recent years, the total mobilized capital of the Bank increased to 183,970 million VND (an increase of 7.08%). By 2016, the total mobilized capital of the Bank reached

214,395 million VND (increase of 16.65%).

Agribank Minh Hoa District Branch has also focused on ensuring the structure and growth of highly stable capital sources from residents and economic organizations; diversifying products and forms of capital mobilization, etc.

The Bank's credit activities have always grown steadily. In 2014, outstanding credit was at VND 216,623 million, and by 2015 it had increased to VND 65,408 million (an increase of 30.19%), and in 2016 it increased by 23.47% to VND 389,365 million. Credit growth has shifted in a positive direction, in line with the Government's policies, especially credit and interest rate solutions to remove difficulties and obstacles for production and business activities, and provide capital for customers with effective production and business plans.

2.1.3.2. ROA, ROE indicators

Return on equity (ROE) indicates how much profit is generated for every 100 dong of bank equity. Looking at Table 1.2, it can be seen that although the bank's ROE index over the years is positive, showing that the bank is still making a profit, the problem is that the bank's equity is increasing, the total assets are increasing but the bank's after-tax profit is decreasing, this is not a good sign for the bank itself.

Table 2.2: ROA, ROE indicators of Agribank Minh Hoa district branch

North Quang Binh

Unit: Million VND

Target

2014 | 2015 | 2016 | |

Equity | 7,759 | 8,718 | 8,821 |

Total assets | 252,527 | 323,360 | 446,432 |

Profit | 6.246 | 7,941 | 9,087 |

ROA | 0.025 | 0.025 | 0.020 |

ROE | 0.81 | 0.91 | 1.03 |

(Source: Business performance report 2014-2016)

In 2014, for every 100 VND of equity, the investment bank earned 0.81 VND of profit after tax, but this number has been increasing over the years, in 2015 it was 0.91 and in 2016 it was 1.03. This ratio has decreased at a rapid rate, showing that the bank's equity capital is used effectively.

The ROA indicator of the bank shows the effectiveness of the process of organizing and managing business activities in the bank. The results from table 2.2 show that in 2014, every 100 VND of assets used in business brought the bank 0.025 VND of profit after tax, but this ratio remained the same and in 2015 it was 0.027 and fluctuated down to 0.020 (Because the total assets in 2016 increased), showing that the bank is investing and effectively managing its capital and assets. Thanks to the correct determination of business strategy and determination of reasonable target market, the business performance of Agribank Minh Hoa Bac Quang Binh branch is always high, the growth rate is steady, the following year is higher than the previous year. Therefore, the profit of Agribank Minh Hoa Bac Quang Binh branch has continuously increased over the years.

This shows that the Bank's business activities in recent years have been very developed and the profit growth rate is high. Along with the development of the network of branches in the province, the expected business results of Agribank Minh Hoa Bac Quang Binh branch in 2017

will achieve high profits. With the results achieved in 2016 and plans for 2017, Agribank Minh Hoa Bac Quang Binh branch continues to affirm sustainable, safe and flexible development, maintaining the motto "Sharing opportunities, successful cooperation".

2.1.3.3. Credit turnover ratio

Credit turnover shows the speed of capital turnover and credit quality of the bank. High credit turnover shows fast capital turnover and good credit quality. On the contrary, low turnover shows slow credit turnover, poor credit quality, and poor debt collection.

Through table 2.3, we can see that the credit turnover has increased over the years: 0.63 times in 2014, 0.78 times in 2015, an increase of 0.15 times compared to 2014. This proves that the use of capital is increasingly effective and the quality of credit capital has been significantly improved. In terms of credit quantity, it can be seen that the loan turnover has increased rapidly over the years, meaning that if the growth rate is higher, the credit turnover will be much higher.

Through the rapid increase in credit turnover ratio of Agribank Minh Hoa Bac Quang Binh over the years, we can see that the quality of service as well as the quality of capital use by customers in business activities is getting higher and higher. This means that the credit quality of Agribank Minh Hoa Bac Quang Binh is quite high.

Table 2.3: Credit turnover at Agribank Minh Hoa district branch

Northern Quang Binh period 2014 -2016

Unit: Million VND

Target 2014 2015 2016

1. Debt collection turnover 136,745 196,325 315,537

2. Total outstanding debt 216,623 282,031 389,365

3. Credit turnover (turns) 0.63 0.70 0.81

(Source: Agribank Credit Department, Minh Hoa District, Bac Quang Binh)

2.1.3.4. Income from lending activities at Agribank Minh Hoa Bac district

Quang Binh period 2014 - 2016

The ultimate goal of commercial banks is to make profits in their business activities. Improving the quality of lending services is only meaningful when it contributes to improving the bank's profitability. Income from lending activities is a necessary indicator to measure the bank's profitability due to credit activities.

Through table 2.5, we can see that, after three years of business operations, Agribank Minh Hoa district, Bac Quang Binh has been profitable, in which the profit from lending activities is decisive to the branch's income. Reaching 88.90% in 2014, 86.97% in 2015 and 87.33% in 2011. This can be understood that the nature of the Agribank system in Minh Hoa district, Bac Quang Binh depends heavily on credit activities, mainly lending.

In addition, the bank also has revenue from service activities through new service products related to money transfer payment activities such as card transaction conversion, E-mobibanking service deployment with all customers has created revenue for the branch. On the other hand, with investment in promotion and attracting a large number of customers from units such as businesses, schools registering to use ATM cards to pay salaries, tuition fees, contributing significantly to the growth of revenue from service activities.

Table 2.4: Income situation at Agribank Minh Hoa Bac district branch

Quang Binh period 2014-2016

Unit: Million VND, %

2014 2015 2016

Target

Amount

Proportion

Amount

Proportion

Amount

Proportion

I. Total Income

28,180 | 100 | 31,829 | 100 | 40,271 | 100 | |

1. Loan interest collection | 25,053 | 88.90 | 27,683 | 86.97 | 35,169 | 87.33 |

2. Revenue from service activities | 920 | 3.27 | 1.110 | 3.49 | 1,422 | 3.53 |

3. Unusual income | 5 | 0.02 | 15 | 0.05 | 51 | 0.13 |

2014 2015 2016

Target

Amount

Proportion

Amount

Proportion

Amount

Proportion

4. Other income

2.202 | 7.81 | 3,022 | 9.49 | 3,629 | 9.01 | |

II. Total Cost | 21,935 | 100 | 23,888 | 100 | 31,184 | 100 |

1. Capital mobilization expenses | 11,262 | 51.34 | 14,018 | 58.68 | 20,006 | 64.15 |

2. Employee expenses | 2,800 | 12.77 | 2,364 | 9.90 | 2,960 | 9.49 |

3. Treasury work expenses | 98 | 0.45 | 108 | 0.45 | 122 | 0.39 |

4. Payment of fees and charges | 22 | 0.10 | 26 | 0.11 | 27 | 0.09 |

5. Management operating costs | 898 | 4.09 | 923 | 3.86 | 937 | 3.00 |

6. Asset expenses | 838 | 3.82 | 696 | 2.91 | 701 | 2.25 |

7. RR and BHTG reserve expenses | 1,341 | 6.11 | 1,770 | 7.41 | 2,820 | 9.04 |

8. Other expenses | 4,676 | 21.32 | 3,983 | 16.67 | 3,612 | 11.58 |

III. Benefits | 6.246 | 7,941 | 9,087 |

(Source: Agribank Credit Department, Minh Hoa District, Bac Quang Binh)

Although the business situation in the market at this time is still difficult due to high capital mobilization interest rates in the market, especially the increased savings interest rates, and the capital mobilized at the branch is mainly from this source. However, thanks to the bank's correct orientation and good cost management, the branch has achieved quite high profits.

2.1.3.5. Overdue debt ratio, bad debt ratio

High or low overdue debt ratio shows whether the lending process is growing healthily or not, because if the loan turnover is higher, the credit balance is larger but the debt cannot be recovered, it is not as effective as lending lower, the balance is lower but the healthy debt ratio is larger, bad debt is at an acceptable level, because any commercial bank must accept bad debt, risk as an inevitable problem in the credit activities of commercial banks. The problem that commercial banks have to solve is not to find a way to completely eliminate overdue debt and bad debt, but to control the bad debt ratio at the lowest possible level.