This provision has helped to overcome the instability of the previous budget system. The instability before the 1996 State Budget Law was one of the reasons why budget management was ineffective and local governments had to rely on the central budget for most of their expenditures. The mechanism of revenue allocation and expenditure tasks between the central budget and provincial budgets, and between provincial budgets and other budget levels, has been basically adjusted compared to the period before the 1996 State Budget Law was enacted.

State Budget Law amended in 2002:

The 1996 Budget Law was amended by the National Assembly in May 1998 and took effect from January 1, 1999. The main reason for the amendment was the Law on Value Added Tax (VAT) and the Law on Corporate Income Tax (CIT). Accordingly, the amount of revenue that the central budget enjoys 100% will be reduced, while the revenue sources and expenditure tasks of local budgets will be adjusted. Revenue from agricultural land use tax and resource tax (except crude oil) will be retained 100% for localities. Previously, these revenue sources were divided between the central and local governments. In addition, the Law stipulates more clearly the division of revenue sources and expenditure tasks assigned to local governments, especially district and urban budgets (including both divided and undivided revenue sources). This amendment has supported and encouraged localities to exploit locally available resources. In addition, local budgets are also divided from special consumption taxes on domestic goods, services such as massage, alcohol, karaoke, golf business, casino and Jackpot games. These sources of revenue previously belonged entirely to the central budget.

The 2002 State Budget Law has significantly improved fiscal decentralization and has made an important contribution to the country's economic growth. That is, the management of the State Budget has been standardized and made more effective. The responsibilities and powers of different government agencies in the management and implementation of the State Budget system have been clearly defined to some extent, while the overall position of local budgets and central budgets has also been fully determined. Revenues from taxes, fees and charges have exceeded regular expenditures and met debt repayment obligations, while the budget deficit has been maintained at an acceptable level. A number of detailed regulations on spending standards and norms have been issued by the Government along with a monitoring and control mechanism of the state treasury system. A mechanism for publicity and transparency of the State Budget has also been issued. That has contributed to maintaining the effectiveness and efficiency of the implementation of the State Budget Law. According to Bach Thi Minh Huyen & Kyohito Hanai (2006), the 2002 revised and supplemented Budget Law has overcome limitations such as:

(1) Slow growth and high levels of tax evasion and avoidance;

(2) Overlapping rights and responsibilities between the National Assembly, the Government, the Provincial People's Council and the People's Committee in managing the State budget;

(3) Limitations of local authorities in budget preparation and implementation;

(4) The mismatch between the rights and responsibilities of the government

locality for revenue and expenditure tasks.

(5) The function of the “reward mechanism”,…

With this amendment, local authorities, central agencies and budget-using units have been decentralized and given increased authority in budget management.

2.3. Decentralization of spending tasks and autonomy of local governments

2.3.1. Hierarchical content

Articles 21 and 24 of the 2002 State Budget Law have specific provisions on decentralization of State budget expenditure tasks, including:

Central budget expenditure tasks include :

(1) Development investment expenditure : includes expenditures for investment in developing socio-economic infrastructure; investment and support for enterprises, economic organizations, capital contribution, joint ventures in enterprises in necessary fields with State participation according to law provisions; expenditures for financial support, additional capital, support and export rewards for enterprises and economic organizations according to law provisions; development investment expenditures in national target programs, state projects implemented by central agencies; expenditures for supplementing state reserves managed by the central government.

(2) Regular expenditure : this expenditure relates to human resources and management expenditure for cultural, social, sports, and economic activities managed by the central government.

(3) Other legalized expenses (interest payments, aid, reserve fund supplements, resource transfers, etc.)

The tasks of local budgets include:

(1) Development investment expenditure: includes investment expenditure on construction of economic and social infrastructure works that are not capable of recovering capital; investment and support for enterprises, economic organizations, and State financial organizations managed by localities.

(2) Regular expenditure: Regular expenditure is related to human resources and management expenditure for cultural, social, sports, and economic activities managed by the locality.

(3) Other legalized expenses (interest payments, aid, reserve fund supplements, resource transfers, etc.)

From the above mentioned contents, we can see that the level of decentralization of spending tasks between the central and local levels according to the State Budget Law of 1996 supplemented in 2002 has the following characteristics:

(1) In principle, local authorities mainly perform tasks related to the provision of public services within their locality. However, the decentralization of tasks mentioned above in the Law on Organization and Operation of People's Councils and People's Committees at all levels does not clearly reflect this. That is, there is a lack of coherence between the laws in establishing decentralization. The current decentralization is characterized by the same tasks but they are regulated at both the central and local levels. According to this law, localities must perform most of the same spending tasks as the central government, but the only difference is that they are "managed by localities" (Le Chi Mai, 2006). That blurred boundary leads to duplication and creates gaps for which no one is responsible. At the same time, the tasks of each level must be similar to the budget spending tasks of that level, but this is not clearly stated in the State Budget Law. This decentralization implies that different levels of government share responsibility for providing public services, rather than relying on the optimal basis of providing public goods.

Table 2.1 : Summary of the content of the division of expenditure tasks

Expenses

Central government | Local government | |

Medical | Centrally managed services | Locally managed services |

Education | Centrally managed services (above universities and most universities), national programs. | Locally managed services |

Economic activities | Economic services provided by the center management | Services managed by the provincial level |

Sports culture | Intermediate level activities nursery National programs | Local activities, individual support. |

Society | National Social Security Programs | Locally managed activities |

Defense and security | Defense and security | Military service Other defense and security activities |

Political organization | Central agencies of the State, Party and other socio-political organizations | Local agencies |

Subsidy | Central programs | Types of subsidies according to national policies |

Pay off debt | Paying off government debt | Paying off local debts |

Other expenses | By law | By law |

Investment development | Central level infrastructure programs Investment and business support National investment and development programs | Basic infrastructure works Support businesses according to the law |

Subsidy | Subsidies for local governments | Statutory benefits |

Maybe you are interested!

-

The Impact of Fiscal Decentralization on Economic Growth in Vietnam - 15

The Impact of Fiscal Decentralization on Economic Growth in Vietnam - 15 -

Choosing a Policy Framework to Change Fiscal Decentralization to Promote Economic Growth in the Condition of Economic Restructuring

Choosing a Policy Framework to Change Fiscal Decentralization to Promote Economic Growth in the Condition of Economic Restructuring -

GDP and GDP Growth Rate of Hanoi as of December 31, 2006, by Economic Sector - Calculated at 1994 Prices

GDP and GDP Growth Rate of Hanoi as of December 31, 2006, by Economic Sector - Calculated at 1994 Prices -

Economic Growth Rate of Thua Thien Hue Province in the Period 2005 - 2016

Economic Growth Rate of Thua Thien Hue Province in the Period 2005 - 2016 -

The Role of the State in Economic Growth

The Role of the State in Economic Growth

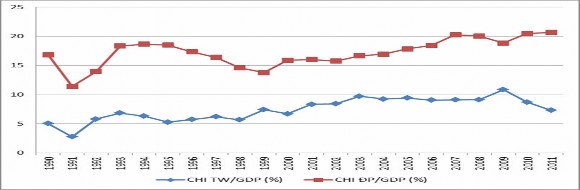

(2) It must be admitted that since the promulgation of the 1996 Budget Law, the level of fiscal decentralization in Vietnam has expanded quite rapidly. The proportion of local budget expenditure in total budget expenditure has increased rapidly, leading to an increase in the ratio of local budget expenditure to GDP. The figure below depicts the ratio of local budget expenditure to GDP in relation to central government expenditure to GDP.

Figure 2.1 : Ratio of state budget expenditure to GDP (%)

(Source: General Statistics Office & Ministry of Finance, 1990 - 2011)

Figure 2.1 shows that compared to GDP, in the period 1990 - 1995, the average expenditure ratio of local government accounted for about 16.2%, while that of the central government accounted for 5.35%. In the period 1996 - 2000, due to the impact of the regional economic crisis, with the Government's stimulus policy, central government expenditures tended to increase. In the period 2001 - 2005, local government expenditures accounted for an average of 13.88% of GDP, while central government expenditures accounted for 7.5% of GDP. Thus, local government expenditures tended to increase during this period, especially after the 2002 State Budget Law. In the period 2006 - 2010, local expenditures tended to move in the same direction as central government expenditures. However, from 2009 to present, local government expenditures compared to GDP have tended to increase, while state expenditures have decreased.

The central government's expenditure tends to decrease, which shows that the decentralization of expenditure tasks, especially development investment expenditure for localities, has tended to increase.

2.3.2. Budget autonomy of local governments

The State Budget Laws of 1996 and 2002 were consistent with the theoretical principle in spending tasks. Tasks assigned at government levels were commensurate with the geographical location of benefit (Le Chi Mai, 2006).

(1) Classification of regular expenditure

Recurrent expenditure is a group of expenditures that arise regularly and are necessary for the daily operations of public sector units. Local recurrent expenditures include salary, professional and management expenditures for the fields of economic, educational, health, social and cultural affairs, national security and defense, social insurance, subsidies, etc.

Normally, the financial resources to finance local recurrent expenditures are taken from 100% local revenue, revenue from the distribution according to the regulation ratio and a part of the balance or targeted supplement from the Central Government. Due to the limited local revenue, many localities have to rely on the supplement from the higher-level budget to balance their budgets, including the regular expenditure.

Table 2.2 : Percentage of provinces with revenue sources regulated to the central government during the stable period 2004-2006 and 2007-2010 and the estimate 2011-2015

(Unit:%)

STT

Conscious | Distribution ratio divided into stages 2004 - 2006 | Distribution ratio divided into stages 2007 - 2010 | Distribution ratio divided into stages 2011 - 2015 | |

1 | Hanoi | 32 | 31 | 42 |

2 | Quang Ninh | 98 | 76 | 70 |

3

Hai Phong | 95 | 90 | 88 | |

4 | Vinh Phuc | 86 | 67 | 60 |

5 | Bac Ninh | 100 | 100 | 93 |

6 | Danang | 95 | 90 | 85 |

7 | Khanh Hoa | 52 | 53 | 77 |

8 | Ho Chi Minh City | 29 | 26 | 23 |

9 | Dong Nai | 49 | 45 | 51 |

10 | Binh Duong | 44 | 40 | 51 |

11 | Ba Ria – Vung Tau | 42 | 46 | 44 |

12 | Long An | 99 | 100 | |

13 | Tien Giang | 99 | 100 | |

14 | Vinh Long | 99 | 100 | |

15 | Can Tho | 95 | 96 | 91 |

(Source: General Statistics Office)

Table 2.2 shows that by 2015, it is expected that 15 provinces will have budget autonomy, while most of the remaining localities will have to rely on additional central budget. This clearly shows that the current local revenue capacity is barely able to cover expenditures and many localities will have to rely on additional central budget.

The 1996 State Budget Law stipulates that when a superior assigns its expenditure tasks to a subordinate, it must transfer funds to the subordinate to carry out these tasks. In reality, there are still cases where superiors assign additional expenditure tasks to subordinates without providing additional funds, which leads to superiors piling up tasks onto subordinates. Therefore, the 2002 State Budget Law strictly prohibits superior authorities from assigning expenditure tasks to subordinate authorities without providing additional budget. The 2002 State Budget Law also clearly stipulates that when issuing new policies that increase costs, the issuing agency must: