No. 53/2006/TT-BTC guiding the application of management accounting in enterprises. According to this circular, management accounting aims to provide information on internal operations of enterprises. This is also the job of each enterprise, the State only guides the principles, methods of organization, and the main contents and calculation methods to facilitate the implementation of enterprises. The recipients of management accounting information are the enterprise's board of directors and those participating in the management and operation of production and business activities. Enterprises are not required to publicly disclose information on management accounting except in cases where the law provides otherwise. Enterprises are allowed to use all information and data of the financial accounting section to coordinate and serve the management of management accounting.

Thus, Circular No. 53/2006/TT-BTC dated June 12, 2006 will be the framework for implementing CPKD management in enterprises because the Circular provides detailed instructions on the organization of the CPKD management apparatus, the CPKD management staff, tasks, content, scope, calculation period and CPKD management. However, to effectively implement the CPKD management model, it is necessary to consider the specific situation of each enterprise.

2.2.2. Production organization in Vietnamese wood processing enterprises

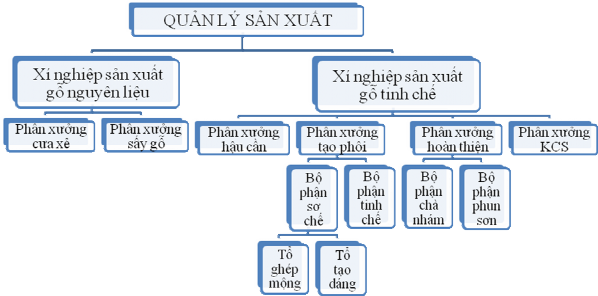

Wood processing is the process of transforming raw materials under the influence of equipment, machinery or tools, chemicals to create products with shapes, sizes, and chemical compositions that are completely different from the original materials [8, p.21]. Wood industry products, whether indoor or outdoor furniture, are all assembled products, meaning that a product consists of many detailed clusters or many assembled details, which is different from a single product. Based on the report on the current status of the Vietnamese wood processing industry [9, p.37], the business and production model of wood processing enterprises is mainly based on the "make to order" business model, and the type of mass production (can be small or medium, but may not be large series) and from this characteristic, the design will also change frequently. In addition, another characteristic that can be mentioned is that the product design can be owned by the customer. In addition, the production technology process model in wood processing enterprises is a mixed model, with many stages and production stages, each stage performs specific production tasks and uses specialized production equipment depending on each wood processing enterprise, especially

Product specifications that have customizations. However, regardless of whether the enterprise has a modern or simple production technology process, the enterprises organize production activities according to the chain method in a scientific and reasonable way to specialize labor and create high labor productivity. Through actual surveys at wood production and processing facilities, it is shown that wood production and processing enterprises often use two types of production technology lines: the type of production technology line that uses processed wood as raw material (refined wood) and the type of production technology line that uses unprocessed wood as raw material (raw wood). Normally, refined wood production facilities often perform the task of producing high-end household wooden products and exported wooden products (including both interior and exterior products). The production process of a refined wood production facility follows a closed chain and is often divided into main production departments including: logistics workshop, blank making workshop, finishing workshop, quality control workshop, packaging and bringing finished products to the warehouse. Each production department is equipped with production equipment with all the necessary features and functions to be able to mass produce many different types of interior and exterior products. Meanwhile, raw wood production facilities mainly perform the task of sawing and processing raw wood blanks. The production process of these facilities also follows a closed chain and is often divided into two main production departments: the wood sawing department (cutting trees in planted forests, transporting them back to saw them according to specifications) and the department of chemical impregnation, treatment and drying of wood. The production organization in the DNCBG is summarized in diagram 2.1.

However, in reality, based on the business registration of the enterprises, there are enterprises that either produce raw wood or produce wooden furniture; based on the production scale of the enterprises, the production structure of these enterprises will have the following levels: production workshop - departments - production teams or production workshop - production teams.

The above relatively stable production organization method helps enterprises more simply in setting up a job order costing system (in English). This system is used for products made according to orders and according to the needs of each individual customer. In addition, this organization method also helps enterprises easily identify the object of cost aggregation, which is the product or unit.

order. However, the limitation of this process will occur if enterprises do not clearly separate the functions of each department, which makes it difficult to manage CPKD.

Diagram 2.1 Organization of product production in wood processing enterprises

Source: Synthesis of the author's survey results and inheritance of research results on

DNCBG

2.2.3. Organization of the administrative apparatus in Vietnamese wood processing enterprises The organizational structure is a synthesis of different departments (or stages) that are specialized and have certain responsibilities and powers, arranged at many levels to ensure the implementation of administrative functions and serve the identified common goals.

determined

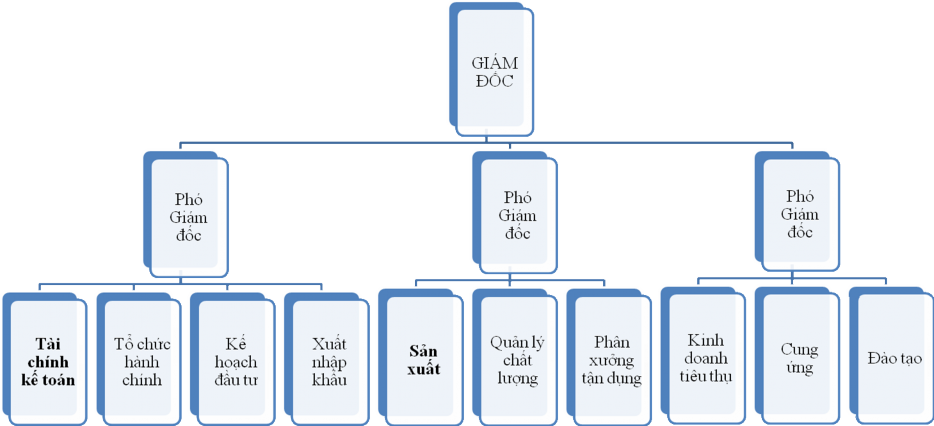

According to statistics from the Department of Processing, Trade of Agro-Forestry-Fisheries and Salt and the Vietnam Timber and Forestry Products Association, as of 2009, Vietnam had about 2,526 enterprises specializing in the production and trading of wooden furniture nationwide with different scales (over 50% of small-scale enterprises) so the way of organizing the administrative apparatus also has many different features; however, the general organizational structure of the administrative apparatus of the current enterprises is still the organization of the administrative apparatus in the form of online - function, dividing the administrative apparatus into functional departments with independent professional responsibilities. Indeed, the online - function organizational structure is a mixed organizational structure of both types of structures: online and functional. This organizational structure has the characteristics

Basically, functional departments still exist but only in terms of expertise, without the right to direct online departments. Online leaders are responsible for the results of operations and have full authority to make decisions in their departments. The typical administrative organization of the DNCBG is summarized in the diagram.

2.2. Organizing the administrative apparatus in Vietnamese state-owned enterprises in an online manner - a function that helps ensure that in enterprises, the production and business functions of each department are clearly defined. With the above organizational structure of the administrative apparatus, it will create favorable conditions for the management of business operations; that is:

Create unity, high concentration, and clearly attach personal responsibility;

Attracting the participation of good experts (in each function), creating conditions for young/new leaders to work and mature early.

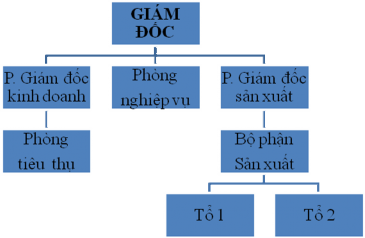

However, this type of organization will have many disputes, so managers often have to resolve them. This type of structure also limits the use of specialized knowledge and still has the intervention of functional departments. Moreover, there is an important problem in the above type of organization: small-scale enterprises with a compact organizational structure, each functional department can take on many jobs. This will cause obstacles when implementing CPKD calculation. For example, the Export Packaging Production Enterprise was established in 1996, a unit under the Packaging and Export Goods Production Joint Stock Company. The enterprise's administrative apparatus is simple and compact. The head is the Director of the Enterprise, appointed (and dismissed) by the General Director of the Company, who is responsible for operating all activities of the Enterprise; is the representative of the rights, obligations and responsibilities of the Enterprise before the General Director of the Company and the State's legal management agency.

The Company has two Deputy Directors appointed (or dismissed) by the Company Director upon the recommendation of the Company General Director. They are:

Deputy Production Director is the assistant to the Factory Director, manages production, is responsible for technical aspects, product quality, and setting standards.

The Deputy Sales Director is responsible for market research, production and business planning, and product consumption...

70

Diagram 2.2 Organization of management apparatus in wood processing enterprises

Source: Author's survey results synthesis and inheritance of research results on DNCBG

In addition, there is a functional department of 3 people in charge of all accounting tasks and other tasks such as statistics, warehouse keeping, sales, etc. The management system of the factory is illustrated in diagram 2.3.

Diagram 2.3 Management apparatus of export packaging production enterprise

Source: Author's field research at the Enterprise

With the above streamlined management structure, an important problem in the model is that the factory has not separated the functions between the production planning department (including the preparation and management of raw materials) and the product consumption department. In other words, the factory does not have a "raw materials management department". Why is it necessary to separate them into two departments like that? Because if following the above model, when implementing CPKD management, there will be some difficulties. Specifically, to carry out the production of products according to received orders, which department is responsible for preparing raw materials and managing raw materials, and where are the expenses incurred for this preparation stage counted? This is an issue that needs to be clarified, otherwise it will be difficult for managers to know where the "loss" expenses arise. For that reason, when implementing CPKD management, we need to clearly separate the boundaries between the two departments. According to the organization and operation regulations of the enterprise, the function of the Deputy Director of Sales is to be responsible for planning production, business and product consumption. Therefore, when implementing CPKD management, it is necessary to separate the consumption department into two: the raw material supply department and the consumption department.

2.2.4. Organizing economic information provision departments in Vietnamese Wood Processing Enterprises

In each enterprise, there are many departments that provide information for managers to make decisions. In this thesis, the author mentions the department that provides economic information mainly for enterprises, which is the accounting department. The accounting department in the current enterprises is a functional department of the management apparatus. Through the author's information collection (surveying enterprises in Hanoi and Bac Ninh; in-depth interviews with 04 chief accountants and the General Secretary of the Vietnam Timber and Forest Products Association) and inheriting the research results (42 enterprises representing the whole country in the "Summary report on the results of the investigation of the current situation of Vietnamese enterprises" of the Vietnam Timber and Forest Products Association and 60 enterprises in Binh Dinh in "What we see through the survey of 60 enterprises in Binh Dinh" by Le Khac Coi), it shows that:

The number of accounting staff is from 3 to 10 people depending on the size of the business. Each accountant is assigned to be in charge of a specific part of the business. Usually, each unit has its own accountant in charge of detailed accounting of production costs and product pricing.

Although there are many large-scale enterprises with many branches nationwide, or production areas in different locations, all large-scale or small-scale enterprises organize their accounting apparatus according to the centralized accounting apparatus model, also known as a one-level accounting organization (shown in diagram 2.4). At the branches or production areas, enterprises only arrange accounting staff or statistical staff to collect documents, enter them into detailed lists, and then transfer those documents and lists to the central accounting department for processing.

All Vietnamese enterprises apply the Vietnamese Enterprise Accounting Regime; the accounting forms applied at the enterprises are very diverse, including the form of Bookkeeping vouchers, the form of Journal - vouchers and the form of General Journal; the basis for preparing financial statements is presented according to the original cost principle.

Chief Accountant

Accountant onion | Cost accounting and price | Accountant onion | ||

Accounting at sales branch | ||||

Maybe you are interested!

-

Current Status of Business Cost Management in Vietnamese Wood Processing Enterprises

Current Status of Business Cost Management in Vietnamese Wood Processing Enterprises -

Perfecting the Organization of Applying the Production Cost Accounting Method to Serve Cost Management Accounting

Perfecting the Organization of Applying the Production Cost Accounting Method to Serve Cost Management Accounting -

Organization of cost management accounting in Vietnamese confectionery manufacturing enterprises - 13

Organization of cost management accounting in Vietnamese confectionery manufacturing enterprises - 13 -

Organization of cost management accounting in Vietnamese confectionery manufacturing enterprises - 21

Organization of cost management accounting in Vietnamese confectionery manufacturing enterprises - 21 -

Management Organization, Production Process and Production Operations

Management Organization, Production Process and Production Operations

Diagram 2.4 Organization of accounting apparatus in wood processing enterprises

Source: Author's survey results synthesis and inheritance of research results

about DNCBG

Among the surveyed enterprises, only about 50% of SMEs have or are building accounting system software or have only a separate part (in which the Southeast region and Ho Chi Minh City, the accounting system of enterprises has been softwareized and internetized accounting for the highest rate: 61.5%). All SMEs that do not have accounting software and have unclear books are small-scale enterprises with products for domestic consumption or processing.

It is worth noting that most of the surveyed enterprises have not yet distinguished between financial accounting and cost accounting (management accounting) from an organizational perspective. If there are enterprises that organize a management accounting department to perform functions of future financial orientation, exploiting market potential... Through the accounting estimates, the calculation methods are not based on the principle of ensuring the preservation of physical assets but still mainly rely on experience to predict. This makes the calculation data still subjective and imposed.

In summary, with the above comments, the accounting department of Vietnamese SMEs is relatively simple, compact and follows the centralized accounting organization model.