(ii) Capital Adequacy Ratio (CAR):

According to statistics of the State Bank and annual reports of commercial banks, most commercial banks

Currently, all have achieved a capital adequacy ratio of over 8%. This ratio is also equivalent to

Commercial banks of countries in the region. This shows that commercial banks are also aware of the importance of complying with standards on safety in banking operations.

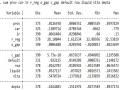

Chart 2.11: CAR ratio of commercial banks in the period 2004-2006 and comparison with the region

CAR 2004-2006

15.40%

10.49%

9.80%

9.45%

12.00%

11.04%

11.87%

11.82%

10.90%

9.10%

6.86%

5.90%

2004

VCB

2005 2006

STB BIDV ACB

CAR 2005

15.40%

15.64%

12.38%

11.04%

12.00%

6.86%

VCB STB BIDV ACB ASEAN OECD

At the end of 2006, BIDV's CAR ratio reached 9.86%.

Source: BankScope Database (12/2005), 2005 Financial Reports of Commercial Banks.

In general, the capital safety ratio of state-owned commercial banks is still lower than that of joint-stock commercial banks, partly because the revenue structure of banks is still heavily oriented towards credit. Meanwhile, the customers of state-owned commercial banks are mainly state-owned enterprises without collateral, while the customers of joint-stock commercial banks mostly have collateral, so when converting risky assets, the risk level in the assets of state-owned commercial banks is higher, leading to a lower capital safety ratio.

(iii) Ratio of medium and long-term loans to total short-term mobilized capital

According to Decision No. 457/2005/QD-NHNN dated April 19, 2005 of the State Bank of Vietnam, the maximum ratio of short-term capital for medium and long-term lending to commercial banks is 40%. Meanwhile, most commercial banks lend at a much lower ratio than the prescribed level, about under 20%. With the development of the stock market, enterprises can mobilize medium and long-term capital through this market, so the pressure to use short-term capital for medium and long-term lending by commercial banks is reduced.

2.2.1.4 On the level of development of banking products and services

It can be said that the banking service market in recent times has been a playground for domestic banks and the leading position is still held by foreign commercial banks. In most traditional operations such as deposits and loans, foreign commercial banks always hold an overwhelming market share. However, in just the past few years, the joint stock commercial bank sector has been encroaching on significant market share, especially in the retail sector with dynamic development. However, in the coming time, not only joint stock commercial banks but also foreign banks are likely to be factors of rapid and strong development when the conditions for opening up the financial market in Vietnam are becoming more and more open.

a) Market share of capital mobilization

The capital mobilization market share is still dominated by state-owned commercial banks. State-owned commercial banks, with the advantage of long-term operation and prestige as a type of state-owned enterprise, still gain the trust of many individuals and organizations that deposit money, but this proportion is gradually changing, the market share of joint-stock commercial banks and foreign bank branches is increasing significantly.

Chart 2.12: Market share of capital mobilization of commercial banks

2005

7.0% 1.4%

1.0%

16.7%

73.9%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

2006

7.1%

1.0%

1.4%

21.8%

68.7%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

Source: Annual Report of State Bank of Vietnam 2006

The strong and stable development of joint stock commercial banks over the past time, combined with higher capital mobilization interest rates than foreign commercial banks, joint stock commercial banks are gradually gaining the trust of the public to deposit money. In addition, foreign bank branches with professional services, targeting high-end customers, are also increasingly attracting customers' attention.

Within the next 5 years, according to the commitment when joining the WTO, the restrictions on mobilizing VND for foreign banks in Vietnam will be completely removed, at that time foreign banks will increase their ability to mobilize and lend in VND and attract customers from domestic banks. Therefore, the competition in mobilizing deposits of commercial banks in the coming time will be very fierce.

b) Lending market share

Similar to capital mobilization, the lending market share of state-owned commercial banks also accounts for the largest proportion in the entire system, followed by joint-stock commercial banks, foreign bank branches and finally the commercial banks. At the same time, this market share has also shifted towards increasing the market share of joint-stock commercial banks and decreasing the market share of state-owned commercial banks. This shows the result of the dynamism in expanding the network as well as diversifying the products and services of joint-stock commercial banks in recent years.

Chart 2.13: Lending market share of commercial banks

2005

8.31% 4.96%

1.17%

14.76%

70.80%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

2006

8.04%

3.83%

3.48%

21.16%

63.49%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

Source: Annual Report of State Bank of Vietnam 2006

The current lending market share of commercial banks also reflects the general situation of the economy. Although the lending market share of state-owned commercial banks is the largest, the main target of this group of banks is state-owned enterprises, which is a disadvantage for state-owned commercial banks today because:

- Most state-owned enterprises are assessed as operating inefficiently, while large enterprises such as corporations and general companies are likely to switch to relationships with foreign banks with lower interest rates and more professional services.

- Besides, with cumbersome procedures and bureaucratic service style, state-owned commercial banks are unlikely to be able to expand retail credit to small and medium enterprises and individual customers like joint-stock commercial banks.

Thus, in fact, loans of the group of State-owned commercial banks are riskier than those of other banking groups. In the long term, State-owned commercial banks need to have comprehensive reforms to be able to compete and maintain their market share.

c) Market share of other services

If considered separately, each commercial bank has its own strengths in banking services. For example, HSBC or ANZ are strong in foreign exchange trading and premium services, Vietcombank is strong in international payments, Dong A is known by many as a bank with the best remittance services, ... but in general, foreign banks have strengths in providing import-export payment services and foreign exchange trading, which are services that require an international network system. Because the parent foreign banks have a global technology network, sharing that network with branches in Vietnam does not incur many additional costs. Previously, these services were dominated by state-owned commercial banks, but in recent years, this market share has been shared between both joint-stock commercial banks and foreign banks.

Chart 2.14: Market share of commercial banks in services

2005

10.20%

4.80%

1.10%

16.30%

67.60%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

2006

12.30%

2.85%

1.05%

18.10%

65.70%

State- owned commercial banks Joint-stock commercial banks Foreign-owned commercial banks Other

Source: Annual Report of State Bank of Vietnam 2006

For card issuance and payment services, which are of interest to many banks, there are currently 17 card issuing banks and over 20 banks acting as card payment agents. Card services require good infrastructure and a network of transactions.

International card services are the strengths of foreign banks but have been limited in the past, so domestic commercial banks are still dominating this market share. However, since joining the WTO in late 2006, foreign banks have been allowed to issue credit cards and this will be a strong competitive service between domestic and foreign banks.

Table 2.6: Growth of card services of the commercial banking system

2006 figures | Growth rate compared to 2005 | |

Number of ATMs (units) | 2,154 | 21% |

POS Peripherals (piece) | 14,000 | 17% |

Number of cards in circulation (million cards) | 3.5 | 30% |

Maybe you are interested!

-

Correlation Coefficient Matrix Model Impact of Monetary Policy, Prov to Car

Correlation Coefficient Matrix Model Impact of Monetary Policy, Prov to Car -

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Results of Testing Cronbach's Alpha Coefficient of Independent Variable

Results of Testing Cronbach's Alpha Coefficient of Independent Variable -

Comparison of Geographical Conditions, Structure of Culture and Tourism Activities

Comparison of Geographical Conditions, Structure of Culture and Tourism Activities -

Comparison of Distribution by Number of Cesarean Sections Between Studies

Comparison of Distribution by Number of Cesarean Sections Between Studies

Source: Annual Report of the State Bank of Vietnam 2006

development of financial markets is certain | it will generate greater demand and are services |

The State Bank has a tradition in | provide these services. |

Currently, the number of banking services that Vietnam provides is only about 300 services while a large bank in the world is capable of providing up to 6,000 services. Many services have been the strengths of foreign banks for decades but are still quite new to domestic banks such as investment consulting services, factoring, derivatives, etc. Modern services such as currency options, investment trusts, e-banking and derivatives have been implemented by some domestic commercial banks but most of them are still not interested. These services in the future with the development

services that domestic commercial banks must pay attention to if they do not want to give up completely to foreign banks.

2.2.1.5 On the level of application of banking technology

Up to now, all domestic commercial banks have been equipped with internal computer systems, local area networks (LANs) to serve business and management activities. In addition, many commercial banks have developed wide area networks (WANs) to connect branches. This network system of commercial banks is also connected to the network system of the State Bank so that the State Bank can manage and provide customer data to the entire banking system. The biggest success of the commercial bank technology system is that almost all commercial banks have completed the Core Banking system program, which is the system

Basic technology system, focusing on managing the entire bank's data system, thereby helping the bank develop electronic transaction service utilities.

Table 2.7: Technology deployment at domestic commercial banks

Commercial Bank

Initial cost (million USD) | Implementation partner | |

VCB | 5.1 | Malaysia |

ACB | 4 | Unisys |

Techcombank | 2 | Temenos |

EIB | 2.6 | Hyundai |

East Asia | 2.67 | Flexcub |

Sacombank | 3.2 | Temenos |

Source: Survey of Ho Chi Minh City Institute of Economics in 2004

Although domestic commercial banks have realized the importance of applying technology in banking operations, due to limitations in capital and experience, the implementation has not been effective and the level of modernity is still inferior to that of foreign banks. Specifically, Vietcombank's Silverlake program, considered one of the most modern retail management programs in the Vietnamese commercial banking system, is just an old version of its Malaysian partner that has been applied since the early 90s, modified to suit the characteristics of the Bank.

Vietnam. This program has just been implemented by Vietcombank.

above

whole system

system

In 2001, the new version had to be upgraded in 2003 because it could not meet all the arising needs of the bank.

In addition, domestic commercial banks also lack linkage to reduce investment costs, typically the ATM system. Each bank invests in its own ATM system, customers who open a payment account at a bank can only withdraw money at that bank and cannot withdraw at ATMs of other banks. This lack of linkage leads to the division of market share among banks, the total investment cost for ATMs of the banking system is also much higher and is not effective compared to synchronous investment and connection between banks. Currently, commercial banks have also established 3 card alliances, but the ability to move towards connecting the entire banking system will still be difficult.

This is one of the experiences that domestic commercial banks need to pay attention to in the process of competing with foreign banks because the strengths of foreign banks are capital and technology. Domestic commercial banks have low capital levels while requiring very high investment costs for technology, so banks need to link together to reduce costs and expand market share instead of dividing as is the case now.

In addition to traditional services that have applied electronic technology such as import-export payments, money transfers, credit card payments, domestic commercial banks need to focus on upgrading technology to develop modern banking services such as e-banking, mobile-banking, ... which are services that have the potential to develop strongly in the near future.

2.2.1.6 About reputation and ability to build brand

Brand valuation company Brand Finance (UK) has just announced the list of the 100 most valuable banking brands in the world, with Citigroup at the top with a brand value of nearly 35.2 billion USD. In second place is HSBC with a brand value of nearly 33.5 billion USD, Bank of America and America Express occupy the following positions. In this list, Asia contributes 17 faces, especially noteworthy is that Singapore has 3 banks in the ranking including DBS (Development Bank of Singapore, brand value of 1.4 billion USD, ranked 77th), UOB (United Overseas Bank ranked 87th with brand value of 1.1 billion USD) and OCBC (Oversea - Chinese Banking Corporation Ltd., ranked 93rd with brand value of 670 million USD), the total brand value of these 3 Singaporean banks is 3.2 billion USD, only 9% of the brand value of Citigroup, the group leading the list.

For Vietnamese commercial banks, branding has not been given due attention through the quality of service and culture of the bank, but is often only concerned with the name of the brand such as the logo or slogan of the bank. Brand building has not focused on the factor of building trust and customer loyalty to the bank.

In fact, Vietnamese commercial banks are currently investing heavily in network development and launching new products, especially non-credit services and derivative services. This is part of the bank's strategy to build and enhance its image, creating a certain position in the market before having more

Many competitors are participating. However, in their efforts to compete, banks still lack or have not had an appropriate focus on building customer trust and how to improve professionalism, while these are the most important factors that customers care about when choosing a bank as a survey report by UNDP recently conducted in 2006 has shown (project VIE/02/009 May 2006).

Observations show that the advertisements and promotional information of banks today still mainly focus on the benefits and convenient features of the services that the bank can bring to customers, how to ensure customer trust in the service or the bank is rarely mentioned.

However, the effort to achieve prestigious awards can be considered a good way to promote the bank's brand. For example, banks such as VCB and ACB have been voted the best bank in Vietnam by The Banker magazine from 2000 to present; the Bank for Agriculture and Rural Development and the Vietnam Joint Stock Commercial Bank for Industry and Trade have also received the Vietnam Gold Star award for their brands. However, commercial banks need to note that self-advertising or being voted for are only measures to support banks in building and developing their brands. For the brand itself to have the power to make customers always think of it when they have a need, banks must make efforts to comprehensively reform in accordance with what the bank advertises or has been voted for. Only then can banks create trust with customers and imprint their brands in the minds of customers, thereby retaining customers and bringing new products to customers more easily.

2.2.1.7 On the development of the branch and transaction office network system

Joint stock commercial banks have been the pioneers in expanding their networks in the past two years. However, joint stock commercial banks have mainly developed in big cities such as Hanoi and Ho Chi Minh City, while state-owned commercial banks have expanded to provinces across the country.

Expanding the branch network in the current period is a right direction for domestic commercial banks to gain market share before foreign banks penetrate the market.