2.2. Export added value

The growth rate of leather and footwear exports in recent times can be considered high, but the quality of growth is not really sustainable, the added value of exported leather and footwear is still small in the total export turnover. The low added value comes from the fundamental reason that the main method of the industry is still export processing. Vietnamese export processing enterprises depend too much on foreign partners, leading to not only low added value of the industry but also very low added value of related and supporting industries. Industry development is based only on available resources such as geographical location, labor, use of average components and technology. This is a passive direction and very easy to fail when Vietnam faces fierce competition from countries with the same conditions and advantages.

In 2008, Vietnam's footwear export turnover reached 4,767 billion USD, but its contribution to Vietnam's export value was only about 20% (Ministry of Planning and Investment 2009, p.19). The majority of input materials, materials, chemicals, machinery and spare parts, and even some shoe components must be imported (Kaohsiung 2009).

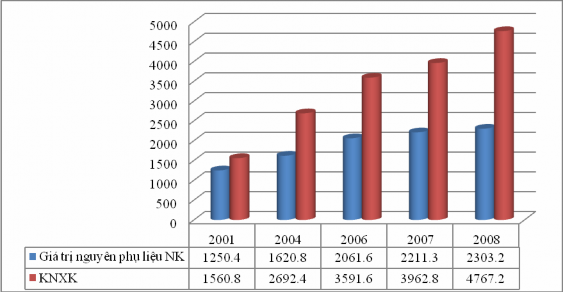

Chart 6: Comparison of imported raw material value and export turnover of Vietnamese leather and footwear

Unit: million USD

(Source: Vietnam Leather and Footwear Association 2007 and 2008b)

The chart above shows the import situation of raw materials of the footwear industry in relation to export turnover over the years. Although the proportion of imported raw materials in the industry tends to decrease, from 80% in 2001 to 48.3% in 2008, accounting for an average of 60% of the industry's export turnover; however, raw materials are still a burning issue for the footwear industry. Although they are also processing products, regional competitors such as China, Thailand, and Taiwan have much more developed raw material production industries for footwear. Not only that, they also set out their own strategies and plans for the development of raw material production industries/regions. A typical example is China with specialized footwear industrial clusters in Guangzhou, Xiamen, and Shenyang. In these "happy" areas, raw material production factories are located right next to major footwear production centers. While these countries have been able to take the initiative in raw materials, the Vietnamese footwear industry still mainly processes in the form of delivering main raw materials and receiving finished products (Hong Quan 2010).

With 60% of input materials imported, this not only creates difficulties for the leather and footwear industry in particular but also increases costs and wastes time for many related industries. Specifically, if imported input materials are delivered late, the delivery of finished products will not be on time, making it easy for businesses to be fined for breach of contract; in addition, customs procedures for importing these materials also take a lot of time and cost customs officers hidden costs. Then, it is necessary to spend a cost to transport these raw materials to manufacturing factories... All of the above reasons lead to the value added retained domestically for businesses producing raw materials and processing finished products only accounting for about 5-10% of the retail price of the product (Cong Thang 2009). Vietnamese leather and footwear businesses face many difficulties in creating finished products. Meanwhile, if raw leather can be processed into refined leather, Vietnam will reduce 15-20% of production costs. Furthermore, the cost of raw materials for shoe production in China is 20% cheaper than in Vietnam, when labor costs are the same.

The 20% gap in input material costs is creating a huge competitive advantage for China (Ha Tuan 2007).

In addition, there is almost no linkage within the industry between manufacturers, suppliers, distributors and logistics. Meanwhile, the stages that create a lot of value are dependent on foreign countries such as design, distribution, trade promotion, etc. (Vietnam Leather and Footwear Association 2009a). Therefore, the indirect added value due to the spillover effect from leather and footwear exports is very low. Typically, in the distribution stage, because the popular form of export processing in Vietnam is indirect processing, the product must go through many intermediary stages before reaching the hands of consumers. If a Vietnamese footwear enterprise signs a processing contract with a Taiwanese manufacturer to export goods to the EU market, the distribution process is usually: Vietnamese enterprise Taiwanese manufacturer Taiwanese trading company EU importer Wholesaler Retail system Consumer. Therefore, prices will be increased due to the cumbersome number of distribution channels, leading to a decrease in product competitiveness. Vietnamese footwear products manufactured for Taiwanese and Korean companies are exported at a price of 4–5 USD/pair, but when these companies distribute these products in foreign markets, the price often goes up to 9–12 USD/pair (Hue Huong 2006).

Another indicator to evaluate added value is profit margin (here measured by the ratio of pre-tax profit in the year to a unit of revenue). Although it is one of the export-oriented industries, the profit margin of the leather and footwear industry has been very low in recent years, even in 2006 it was -0.05% (Ministry of Planning and Investment 2009).

In short , the growth of leather and footwear exports in recent years has been mainly due to increased investment capital and the use of low-cost labor, but lack of investment in building factories to produce raw materials and accessories, and lack of design centers to serve long-term development... This threatens sustainability in the present and the future, creating a contradiction between growth rate (quantity) and growth quality.

2.3. Competitiveness and ability to participate in global value chains

In recent years, despite improvements in competitiveness, the competitiveness of Vietnam's leather and footwear exports is still fundamentally low compared to other countries in the region, especially China.

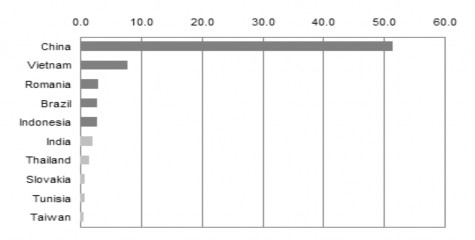

Worldwide, about 6-7 billion pairs of shoes are consumed each year, of which 70% are produced by China, Vietnam, Indonesia, Romania, Bangladesh, Thailand, Cambodia... According to research by the Vietnam Leather and Footwear Association on the competitiveness of footwear from low-cost countries in the total global footwear trade, with a market share of 7.7% in 2006, although Vietnam ranked second, it was still far behind China's market share (51.6%) (Vietnam Leather and Footwear Association 2006).

Chart 7: Market share of footwear exports of low-cost countries

Unit: %

(Source: Vietnam Leather and Footwear Association 2006)

To see more clearly the quality of Vietnam's leather and footwear exports, we can compare some main criteria to evaluate the competitiveness of Vietnamese leather and footwear products with those of other countries in the region.

Regarding footwear export tax to the EU market , among the five largest shoe exporting countries in the world, China and Vietnam are not given GSP preferences by the EU and are subject to tariffs when exporting shoes to the EU (16.5% for Chinese shoes and 10% for Vietnamese shoes). This shows that, just considering the tax, the

Vietnamese shoe exporters not only have to compete with China, but also have to compete fiercely with the remaining three countries in the region such as India, Bangladesh, and Indonesia, as these countries receive many incentives from the EU market.

In terms of raw materials , as analyzed in section 2.4, if China and India have almost all of them available domestically, the Vietnamese footwear industry must import over 60% of raw materials from abroad. This is a significant disadvantage for the entire footwear industry.

Regarding labor costs , China is from 120-180 USD/month, Vietnam is from 100-150 USD/month, the competition between Vietnam and China is equal; but with India, labor costs are only 100-20 USD/month, Bangladesh is from 50-70 USD/month and Indonesia is from 70-100 USD/month, Vietnam still has to try very hard to compete and attract orders (Kaohsiung 2009).

And more than that, currently Vietnam only participates in the midstream, which is processing, but has not participated in the upstream (research, design) and downstream (distribution) stages in the product value chain, which are the stages that create the most added value (Tran Van Tho 2006).

The world's leather and footwear industry continues to shift production to developing countries, especially those with favorable investment environments, stable and safe politics. On the other hand, Vietnam's official accession to the World Trade Organization, tariff barriers are gradually being removed, along with the Government's policies to promote production and export, Vietnam will become an ideal investment destination for leather and footwear manufacturers. However, we still have to face the reality that the export capacity of the Vietnamese leather and footwear industry in the world export market is still weak. If Vietnam does not take the initiative in raw materials, gradually escape the processing position, and cannot create a separate brand for Vietnamese shoes, etc. to participate in stages that create higher added value, the ability to grow exports quickly and continuously in the long term will be very difficult.

In summary , in recent years, although the scale and growth rate of export turnover have increased relatively steadily, the quality of growth in Vietnam's leather and footwear exports has not been truly sustainable. Firstly , the product structure has not changed significantly in increasing the export value of products with high added value.

Second, the main form is export processing, using a lot of labor, low added value. Third, the competitiveness of leather and footwear products is still low, not really standing firm in the world market, especially in the context of many fluctuations in the world market .

II. CONTRIBUTION OF FOOTWEAR EXPORTS TO THE ECONOMY

1. Contribute to the country's export turnover

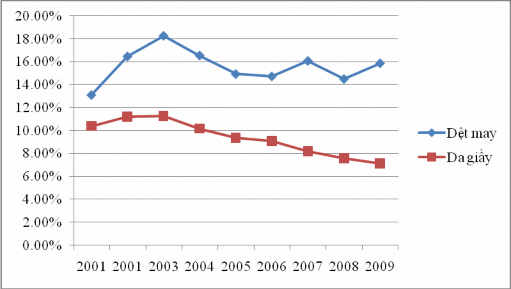

Since 2001, the footwear industry has made impressive progress and is the third largest export industry, accounting for a significant proportion of Vietnam's total export turnover. Table 4 describes the contribution of footwear exports to the country's total export turnover in terms of value and percentage, next to the textile and garment industry.

Table 4: Export turnover and proportion of export turnover in total export turnover of the country of the two leather and footwear and textile industries in the period 2001-2009

Year

Textile Export | Leather and footwear export | Total turnover | ||||

KN (Billion USD) | Percentage | KN (Billion USD) | Percentage | KN (Billion USD) | % | |

2001 | 1,975 | 13.10 | 1,559 | 10.37 | 15,027 | 100 |

2002 | 2,752 | 16.47 | 1,867 | 11.18 | 16,706 | 100 |

2003 | 3,686 | 18.27 | 2,267 | 11.24 | 20,176 | 100 |

2004 | 4,386 | 16.55 | 2,692 | 10.15 | 26.5 | 100 |

2005 | 4,806 | 14.93 | 3.005 | 9.33 | 32.2 | 100 |

2006 | 5,834 | 14.73 | 3,592 | 9.07 | 39,605 | 100 |

2007 | 7,784 | 16.08 | 3,693 | 8.19 | 48.4 | 100 |

2008 | 9.12 | 14.50 | 4,767 | 7.58 | 62.9 | 100 |

2009 | 9,065 | 15.87 | 4,067 | 7.12 | 57,096 | 100 |

Maybe you are interested!

-

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 7

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 7 -

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 5

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 5 -

Improving the efficiency of raw material import activities at C&T Construction and Materials Trading Joint Stock Company - 2

Improving the efficiency of raw material import activities at C&T Construction and Materials Trading Joint Stock Company - 2 -

Ensuring Raw Materials for Production in the Enterprise:

Ensuring Raw Materials for Production in the Enterprise: -

Module curriculum for purchasing, preserving & transporting aquatic raw materials for aquatic product processing and preservation - 2

Module curriculum for purchasing, preserving & transporting aquatic raw materials for aquatic product processing and preservation - 2

(Source: General Statistics Office 2008, Vietnam Leather and Footwear Association 2008c and 2009b, Vietnam Textile and Apparel Association 2009)

The data in the table above shows that, over the past 10 years, the proportion of leather and footwear products has averaged about 9.36% of the country's total export turnover, thereby playing an important role in limiting the trade deficit and stabilizing the macro-economy. However, as an industry with a clear export orientation, leather and footwear exports are still unstable, and the proportion in export turnover has tended to decrease over a long period of time.

Chart 8: Proportion of export turnover in total export turnover of the country of the two leather and footwear and textile industries in the period 2001-2009

Unit: %

(Source: General Statistics Office 2008, Vietnam Leather and Footwear Association 2008c and 2009b, Vietnam Textile and Apparel Association 2009)

It can be seen that from 2003 to 2009, the proportion of leather and footwear exports decreased in the total export turnover of the country without any signs of recovery. Meanwhile, the textile and garment industry has contributed to the total export turnover of the country not only larger than the leather and footwear industry but has also gradually overcome the difficult periods of the whole country, especially in 2009. Despite being heavily affected by the storm of the global economic recession, the textile and garment industry's exports in 2009 reached 9,065 billion USD, rising to the top position, contributing 15.85% to the total export turnover. As for the leather and footwear export industry, the contribution rate has decreased for a long time, and by 2009 it only accounted for 7.12% of the total export turnover.

The country’s exports are the lowest ever. Textiles and footwear are two of Vietnam’s main export industries and are currently only concentrated in the processing stage and mainly rely on simple labor. However, there are some differences between the two industries that can explain why footwear has a greater decline in turnover as follows.

Firstly , the footwear industry is facing significant obstacles due to the European Union imposing anti-dumping duties on leather-cap shoes exported to this market, while leather-cap shoes account for nearly 40% of Vietnam's total footwear exports to the EU. 2009 was also the first year the EU decided to cut the preferential tariff regime (GSP) for all leather and footwear products imported from Vietnam.

It should also be added that while the main market for textiles is the US with a proportion of over 55%, the EU is the main market for the footwear industry, with a proportion of over 53% (Diep Thanh Kiet 2009). Therefore, the above-mentioned obstacles have caused a sharp decrease in the amount of footwear products exported to the EU, leading to a decline in the entire industry.

Second, the proportion of export turnover of foreign direct investment enterprises in the footwear industry is nearly 53%. Meanwhile, in the textile and garment industry, the export proportion of FDI enterprises is below 40% (Diep Thanh Kiet 2009). When the crisis occurs, the FDI enterprise sector is more heavily affected, thus affecting the overall export turnover of the whole industry.

Third , another reason is that leather and footwear products when exported are often bulky and not as easily compressed as textile products. Therefore, when transportation costs increase, the unit price of shipping a pair of shoes or sandals will increase faster than that of textile products.

Fourthly , in 2009, the total import turnover for textile and garment exports was about 5 billion USD, compared to more than 9 billion USD of export turnover, the Vietnamese textile and garment industry had a "trade surplus" of about 4 billion USD, contributing significantly to reducing Vietnam's "trade deficit"; increasing the localization rate of Vietnamese textile and garment products to 44% compared to 38% in 2008 (Le Quoc An 2010). Meanwhile, the footwear industry still cannot take the initiative in raw materials and accessories.