Ordering process, collection process, compensation process... Motor vehicle insurance cases have support to reduce repair time. At the same time, increase investment in equipment, new management software in insurance records management.

It can be emphasized that the application of marketing mix is highly valued by these businesses, thereby increasing business efficiency. The coordination or priority selection combined with different elements of 7P has helped these businesses improve their position in the market. It can be said that these are valuable experiences for Bao Minh in applying marketing mix.

Chapter 2 Summary

Chapter 2 of the thesis focused on presenting and analyzing the theoretical and practical basis for applying marketing mix in insurance business, including the concept, role, and characteristics of insurance business, the concept and content of applying marketing mix in insurance business, and the experience of applying marketing mix of some insurance companies.

Obviously, insurance is a financial service provided by an insurance company to customers and customers have to pay a fee for that service. Customers buy this service to prevent and minimize risks. In essence, it is a way to share risks in life or business to limit possible losses. This sharing method must be done through a contract between the supplier and the customer.

Insurance is classified based on many different criteria, including classification by insurance objects, by management methods, by operational purposes and by insurance techniques. Insurance businesses are established and organized according to the provisions of the Law on Insurance Business.

The main characteristic of insurance is that it is an intangible product, a service product that buyers cannot see but can only feel and evaluate before buying and sellers can only describe the benefits based on experience. This characteristic governs the insurance business activities of enterprises and governs the buying behavior of customers. In order to do business effectively, insurance enterprises must use many different tools, including the application of marketing mix. Reality shows that this is an important tool to create competitive advantage for enterprises if they apply it well.

Applying marketing mix in insurance business is an art in building, operating and implementing seven types of decisions, including products, pricing, distribution, promotion, human resources, operating procedures, means and facilities. And evaluating the effectiveness of applying marketing mix must be based on certain criteria such as increasing the number of customers, return on investment, sales, profit on advertising costs, etc. The application of marketing mix is influenced by many factors, including economics, politics, law, society, technology, business, customers, competition, etc. These factors have many impacts on the application of marketing mix of insurance companies. The effectiveness of applying marketing mix depends on taking advantage of the positive effects and limiting the negative effects of these factors.

Chapter 3

CURRENT STATUS OF BAO MINH'S MARKETING MIX APPLICATION

3.1. Overview of Bao Minh

The year 1986 marked a turning point in the economic development of our country. Vietnam opened its economy, attracting investment from many countries and regions with innovative policies, creating favorable conditions for economic sectors to participate. Production and business activities gradually developed, people's lives were improved, requiring the insurance industry to also innovate to meet the needs and adapt to the new situation. On December 18, 1993, Decree 100/CP on insurance business activities was issued by the Government, opening a new development step for the Vietnamese insurance industry. It broke the existing monopoly, creating the premise for the birth of insurance enterprises with many different forms in all economic sectors.

In that context, under the direction of the Government and the Ministry of Finance, the Ho Chi Minh City Insurance Company Branch (abbreviated as Bao Minh) under the Vietnam Insurance Corporation was separated to operate independently according to Decision No. 1146 TC/QD/TCCB dated November 28, 1994. From then on, Bao Minh became a 100% state-owned enterprise under the Ministry of Finance.

Bao Minh officially started operating in early 1995 with an initial capital of only 40 billion VND and 84 employees. In 2004, Bao Minh Insurance Company equitized and transformed into a joint stock corporation model according to Decisions No. 1691/2004/QD-BTC dated March 3, 2004 and 2803/QD-BTC dated August 30, 2004 of the Ministry of Finance. The company officially operated under the new model based on the establishment and operation license No. 27/GP/KDBH dated September 8, 2004 of the Ministry of Finance. To date, Bao Minh is the third largest enterprise in the non-life insurance market, with a charter capital of 913 billion VND, owner investment capital of up to 2,171 billion VND and a widespread network of operations through 62 branches nationwide [31].

- Bao Minh officially operates under the model of a Joint Stock Corporation.

- Received the Second Class Labor Medal from the President.

1994

1997

1999

2004

2006

Bao Minh was established on November 28, 1994, initiating the formation of the Vietnamese insurance market.

- Bao Minh contributed capital to establish Bao Minh Life Insurance Company.

– CMG

- Received the Third Class Labor Medal from the President.

Main

awake

listed at TT

Deliver

pandemic

Hanoi Securities

- Conduct BEST project - core software application in business management.

- Received the First Class Labor Medal from the President.

- Annual General Meeting of Shareholders to finalize personnel for the 2014 - 2019 term.

- Agreed to increase the actual contributed charter capital by 10% from 755 billion to 830.5 billion VND.

2008

2009

2011

2014

2016

Ancient Congress

Annual General Meeting approved the business strategy for the period 2016 –

2020.

Bao Minh contributed capital to establish United Insurance Company (UIC)

Establishment of BM Securities Joint Stock Company.

Listing BMI shares at Ho Chi Minh Stock Exchange

Ancient Congress

Annual General Meeting approved the 2011 business strategy

– 2015.

Source: Bao Minh, 2018, Annual Report 2018 , Bao Minh Joint Stock Corporation

Diagram 3.1: Important milestones of Bao Minh

Bao Minh operates in the fields of non-life insurance, non-life reinsurance and financial investment. Currently, Bao Minh is providing more than 100 necessary insurance products for individuals, businesses and the economy such as: property insurance, construction insurance, motor vehicle insurance, engineering insurance, human insurance, marine insurance,...

Over the course of more than 25 years of formation and development, Bao Minh has built a clear management structure with a strong workforce spread across the provinces and cities. Bao Minh is operating under a 2-level model: the General Corporation level and the member company level. At the General Corporation, there are 24 departments, offices and functional centers. The member company level includes 62 units with 550 transaction and exploitation departments nationwide. In addition, Bao Minh also has a specialized training center (See the organizational chart of Bao Minh Joint Stock Corporation in the appendix).

Since February 2015, BM has carried out a comprehensive and extensive restructuring of the entire system; reorganizing and rearranging departments, offices, and centers at the Head Office to manage in a professional and specialized manner. Reorganizing the business network of member companies in the direction of developing distribution channels, by opening and relocating district and county-level exploitation offices, to ensure wide coverage of exploitation channels and serving customers anytime, anywhere. Reducing units with small markets and ineffective business operations, ensuring to minimize organizational and cost cumbersomeness.

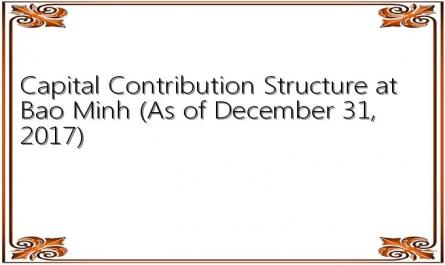

Table 3.1: Capital contribution structure at Bao Minh (as of December 31, 2017)

STT

Shareholder name | Capital contribution (billion VND) | Rate (%) | |

1 | State Capital Investment Corporation | 463,173 | 50.70 |

2 | AXA Insurance Finance Group (France) | 152,097 | 16.65 |

3 | Firstland Company Limited (Group) Chevalier) | 51,626 | 5.65 |

4 | Bao Minh employees and external shareholders | 246,643 | 27.00 |

Total | 913,539 | 100 |

Maybe you are interested!

-

Applying Marketing mix at Bao Minh Insurance Corporation - 16

Applying Marketing mix at Bao Minh Insurance Corporation - 16 -

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Diep Thi Phuong Thao (2011). The Effect Some Marketing Mix Elements On Brand Awareness And Brank Image . Msc. Thesis, Ministry Of Education And Training University Of Economics Ho Chi Minh City.

Diep Thi Phuong Thao (2011). The Effect Some Marketing Mix Elements On Brand Awareness And Brank Image . Msc. Thesis, Ministry Of Education And Training University Of Economics Ho Chi Minh City. -

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28

Source: Bao Minh, 2018, Bao Minh Annual Report 2017 , Bao Minh Insurance Corporation, p. 4.

In 2017, the total original insurance premium revenue of the life insurance market reached 41,344 billion VND, an increase of 11.75% compared to the same period in 2016. The ranking of the leading enterprises in the market in terms of original premium revenue has not changed in recent times. The number 1 position is still Bao Viet with revenue reaching 8,050 billion VND, an increase of 22.6% compared to the same period in 2016. Next is PVI with revenue reaching 6,689 billion VND, equivalent to more than 16% of the market share.

Table 3.2: Original insurance premium revenue of non-life insurance companies in the period 2015 - 2017

Unit: billion VND

STT

Insurance company name | 2015 | 2016 | 2017 | |

1 | Bao Viet | 5,828 | 6,564 | 8,050 |

2 | PVI | 6,457 | 6,527 | 6,689 |

3 | Bao Minh | 2,819 | 3.102 | 3,395 |

4 | PTI | 2,461 | 3,096 | 3.206 |

5 | PJICO | 2,330 | 2,494 | 2,611 |

6 | Other businesses | 12,255 | 15,213 | 17,393 |

Total | 32,150 | 36,996 | 41,344 |

Source: Bao Minh, 2018, 2017, Bao Minh Annual Report 2017 , 2018,

Bao Minh Insurance Corporation.

Bao Minh is currently ranked third with revenue of VND 3,395 billion, up 9.45% compared to 2016 and accounting for 8.22% of Vietnam's non-life insurance market share. Looking at the table above, it is easy to see that Bao Minh's revenue growth is slower than that of Bao Viet, PVI, PTI, PJICO. This is the period when Bao Minh focuses on improving the quality of management, including marketing management and corporate governance. Increasing investment in the field of information technology to serve the purpose of improving business efficiency.

Table 3.3: Market share of insurance premium revenue in 2017

STT

Insurance | Market share (%) | |

1 | Bao Viet | 19.36 |

2 | PVI | 16.08 |

3 | Bao Minh | 8.16 |

4 | PTI | 7.71 |

5 | PJCO | 6.28 |

6 | Other | 42.41 |

Source: Ministry of Finance, 2018, Vietnam Insurance Market in 2017 , Finance Publishing House, p.10

In addition to the leading insurance companies in the market, other companies also had many changes. There were companies that not only maintained their market share but also had a growth rate of original insurance premium revenue of over 50% compared to the same period in 2016 such as QBE (198.2 billion VND, up 50.12%), GIC (1,151 billion VND, up 64.87%). However, there were companies with large revenue decreases such as Groupama (25 billion VND, down 77.38%), AAA (242 billion VND, down 13.35%), AIG (406 billion VND, down 13.35%),

down 19.93%).

Table 3.4: Bao Minh's business situation in 2017

Unit: billion VND

STT

Target | TH 2016 | Business Plan 2017 | % TH 2016/2017 | |||

Plan plan | TH 2017 | % TH/KH | ||||

1 | Total revenue | 3,751 | 3,918 | 4,096 | 104.5 | 109.2 |

2 | Original premium | 3.101 | 3.322 | 3,396 | 102.2 | 109.5 |

3 | Reinsurance premium | 371 | 407 | 429 | 105.3 | 115.5 |

4 | Financial Revenue & other income | 279 | 189 | 271 | 143.4 | 97.1 |

4 | Net revenue from operations KDBH | 2,729 | 2,883 | 3,176 | 110.2 | 116.4 |

5 | Total business expenses | 2,679 | 2,815 | 3.166 | 112.5 | 118.2 |

6 | Total compensation TNGL Insurance | 1,065 | 1.126 | 1,258 | 111.7 | 118.1 |

7 | Contract Exploitation Cost KDBH | 1,430 | 1,494 | 1.801 | 120.6 | 126 |

8 | Large fluctuation reserve | 26 | 28 | -7 | -25 | -26.9 |

9 | Business management costs career | 158 | 167 | 114 | 68.3 | 72.2 |

10 | Net profit from KDBH | 50 | 68 | 10 | 14.4 | 19.5 |

11 | Operating profit finance | 174 | 130 | 188 | 144.8 | 108.2 |

12 | Total accounting profit before tax | 223 | 198 | 198 | 100 | 88.8 |

13 | Total profit after tax | 182 | 163 | 163 | 100 | 89.6 |

Source: Bao Minh, 2018, Bao Minh Annual Report 2017 , Bao Minh Insurance Corporation, p. 5.

Looking at the table above, it is easy to see Bao Minh's business growth rate in the period 2016 - 2017. Specifically, in 2017, Bao Minh's total revenue reached

4,096 billion VND, reaching 104.5% of the plan, up 9.2% over the same period last year. Of which:

- Original insurance premium revenue was VND 3,396 billion, reaching 102.2% of the plan, up 9.5% over the same period last year.

- Reinsurance revenue was 429 billion, reaching 105.3% of the plan, up 15.5% over the same period last year.

- Financial revenue was 271 billion VND, reaching 143.4% of the plan, up 97.13% over the same period last year.

- 3/4 of the original insurance business groups completed and exceeded the average plan such as: marine insurance business reached 112.39% of the plan and 99.47% compared to the same period; Technical property insurance reached 100.1% of the plan and grew 6.84% compared to the same period. The human insurance business group reached 109.68% of the plan and increased 25.93% compared to the same period [31, p. 6].

Table 3.5: Insurance premium revenue of main product groups 2016-2017 of Bao Minh

Unit: billion VND

STT

Karma group service | Perform 2016 | Plan 2017 | Perform 2017 | % refund KH city | % vs. TH 2016 | |

1 | Maritime Group | 374 | 331 | 372 | 112.39 | 99.47 |

2 | Asset Group | 906 | 967 | 968 | 100.1 | 106.84 |

3 | Motor vehicle group gender | 850 | 995 | 831 | 83.52 | 97.76 |

4 | Subgroup People | 972 | 1,116 | 1,224 | 109.68 | 125.93 |

5 | Receive Reinsurance dangerous | 372 | 407 | 429 | 105.29 | 115.2 |

6 | Total | 3,474 | 3,816 | 3,824 | 100.2 | 110.06 |

Source: Bao Minh, 2018, Bao Minh Annual Report 2017 , Bao Minh Insurance Corporation, p. 11

Looking at the data in the table above, we can see more clearly the development of Bao Minh's insurance business in the period 2016 - 2017. Specifically:

Marine Insurance has a high growth rate compared to the insurance market. However, marine insurance is still very difficult because the number and value of Vietnamese ships continues to decrease sharply. Fishing vessel insurance under Decree 67 was only implemented in the last 2 quarters of the year, so revenue decreased significantly. The original compensation rate decreased compared to the same period and mainly focused on fishing vessel insurance under Decree 67. There were some total losses of vessels with VR SB registration level not suitable for coastal operations. Cargo business is still effective due to good control of insurance acceptance and loss prevention.[31, p.48]

In 2017, the human insurance business continued to grow steadily and the most compared to other businesses. The insurance sales channel through credit institutions and banks was also maintained and developed with a strong growth rate compared to the traditional insurance channel. Although products such as student insurance and health care insurance had fierce competition from insurance companies, Bao Minh still achieved revenue of 1,224 billion VND, exceeding 125.93% compared to 2016.