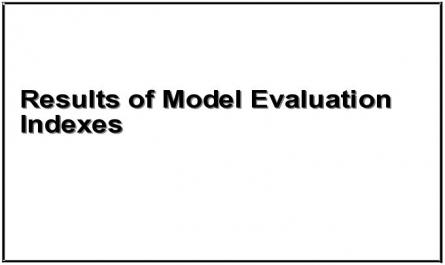

Figure 3: = 1.868 < 3, GFI = 0.944 > 0.9, TLI = 0.978 > 0.9, CFI = 0.989 > 0.9,

RMSEA = 0.078 < 0.8.

Table 4.3: Results of model evaluation indicators

Index

Model 1 | Model 2 | Model 3 | |

Ratio of Chi square to degrees of freedom ( ) | 2,190 | 1,269 | 1,868 |

Goodness of Fix Index (GFI) | 0.953 | 0.942 | 0.944 |

Tucker-Lewis Index (TLI) | 0.978 | 0.991 | 0.978 |

Comparative Fit Index (CFI) | 0.988 | 0.995 | 0.989 |

Root Mean-Square Error of | 0.071 | 0.054 | 0.078 |

Approximation (RMSEA). |

Maybe you are interested!

-

Regression Results of Bank Profitability Model from Interest Rate and Other Profit Determinants

Regression Results of Bank Profitability Model from Interest Rate and Other Profit Determinants -

Management Status of Tcm Results Evaluation Through NCBH Form Table 2.9: Current Status of Evaluation of Professional Team Performance Results Through Form

Management Status of Tcm Results Evaluation Through NCBH Form Table 2.9: Current Status of Evaluation of Professional Team Performance Results Through Form -

Evaluation Results of Quality Indicators and Importance of Each Indicator

Evaluation Results of Quality Indicators and Importance of Each Indicator -

Qualitative Results of Factors Included in the Model

Qualitative Results of Factors Included in the Model -

Evaluation of Land Use Rights Mortgage Results at Vietnam Bank for Agriculture and Rural Development, Dien Bien Province Branch

Evaluation of Land Use Rights Mortgage Results at Vietnam Bank for Agriculture and Rural Development, Dien Bien Province Branch

Source: Author's calculation

Based on the results of Table 4.4, management efficiency and capital structure have positive impacts on profitability. In contrast, market power and bank risk tolerance have negative impacts on profitability. In addition, exogenous variables of concentration and bank size only directly affect bank profitability in model 2 with negative impacts. This shows that banks in Vietnam during the research period generated profits mainly based on management efficiency rather than taking advantage of scale. Small banks (mainly joint stock commercial banks) operate more flexibly and efficiently than large banks (mainly state-owned commercial banks) and thus optimize return on assets (ROA). The results of this study do not support the RMP theory because market power has a negative impact on bank profitability. Model 1 explains 56.5% of bank profitability while model 2 explains 76.5% and model 3 explains 49.6%.

Table 4.4: Model estimation results

Relationship

Model 1 | Model 2 | Model 3 | ||

MAN.EFF <-- | GROW | 0.207** | ||

MAN.EFF <-- | CONC | 0.225* | (0.327)*** | |

MKT.PWT <-- | CONC | 0.458*** | 0.218*** | 0.449*** |

CRL <-- | CONC | 0.269*** | 0.38*** | |

STRCAP <-- | CONC | (0.369)*** | (0.307)*** | |

MKT.PWT <-- | SIZE | 0.814*** | 0.752*** | 0.738*** |

CRL <-- | SIZE | 0.424*** | 0.314*** | 0.542*** |

STRCAP <-- | SIZE | (0.795)*** | (0.724)*** | (0.852)*** |

MKT.PWT <-- | MAN.EFF | 0.19*** | 0.245*** | 0.294*** |

CRL <-- | MAN.EFF | 0.226*** | 0.277** | 0.308*** |

STRCAP <-- | MAN.EFF | 0.222*** | 0.176* | 0.376*** |

MKT.PWT <-- | CRL | 0.166*** | 0.169** | |

PROF <-- | CRL | (0.241)*** | (0.418)*** | |

PROF <-- | STRCAP | 0.369*** | 0.169* | 0.422*** |

PROF <-- | MAN.EFF | 0.481*** | 0.537*** | 0.418*** |

PROF <-- | MKT.PWT | (0.165)** | (0.171)** | |

PROF <-- | CONC | (0.399)*** | ||

PROF <-- | SIZE | (0.399)*** | ||

SMC(PROF) | 0.565 | 0.765 | 0.496 |

***: P < 0.0001, **: P < 0.01, *: P < 0.1

Source: Author's calculation

Bank risk tolerance level (CRL) has a negative impact on bank profitability in model 1 and model 2 with significance level < 0.05 but is not significant in model 3. Hypothesis H1 is accepted in practice. Results

This research result is also similar to the research result of Athanasoglou et al. (2008) and Dietrich and Wanzenried (2011). In reality, bad debt of the Vietnamese banking system always accounts for a large proportion due to the impact of credit growth. However, the debt classification method according to Vietnamese standards (VAS) and international standards (IAS) has a relatively large difference along with the low transparency of the banking system, at the same time, banks use debt restructuring to avoid provisioning, leading to the bad debt ratio always being low in financial reports. The difference is even larger during the crisis period. In fact, the announcement of the debt ratio

The bad of the banking system is different between domestic and foreign organizations 1 .

In addition, the level of risk tolerance has a positive and significant impact on market power in model 1 and model 2. A 1% increase in the level of risk tolerance increases market power by 0.166% and 0.169%, respectively. This can be explained by the fact that during the study period, the bank's assets and the resulting market share increased mainly based on credit growth, so the level of risk increased accordingly.

The capital structure of the bank has a positive and significant impact on the profitability of the bank in all three models. Hypothesis H2 is not accepted in practice. The signs of the factor loadings reject the trade-off theory between costs and profits and support the signaling theory and bankruptcy cost theory. This is also the research result of Bourke (1989), Molyneux and Thornton (1992), Berger (1995), Athanasoglou et al. (2005), Ben Naceur and Goaied (2008). Moreover, the value of the factor loading in model 3 (0.422) is larger than the factor loading in model 2 (0.196). This can be explained by Berger (1995), when bankruptcy costs increase abnormally (for example, during a crisis), banks will quickly adjust their equity-to-asset ratio to an equilibrium level to minimize the cost of capital mobilization and as a result, profitability will be better. At the same time, during a crisis, banks with a lower ratio of high-risk assets will make less provisions than banks with a higher ratio of high-risk assets.

1 http://tapchitaichinh.vn/Trao-doi-Binh-luan/Thuc-trang-no-xau-tai-cac-ngan-hang-Viet-Nam-va-giai-phap-thao-go/16290.tctc

Market power has a negative and significant impact on bank profitability in model 1 and model 3. The research results do not support the RMP theory and hypothesis H3 is rejected in practice.

Management efficiency has a positive and significant impact in all three models. Hypothesis H4 is accepted in practice. The research results show the very important role of bank performance. The more efficient a bank is, the higher its profitability. The ESX hypothesis is consistent with the Vietnamese banking system during the research period. The research results are similar to those of Athanasoglou et al. (2006), Fiordelisi (2009), Dietrich and Wanzenried (2011). In addition, management efficiency also has a positive and significant impact on other endogenous variables in the model, which are capital structure, market power and bank risk tolerance. The positive direction of impact from management efficiency to market power suggests that efficient banks tend to increase their market share. The research results also show that there is a trade-off between variables affecting bank profitability. Management efficiency has a direct positive impact on bank profitability, while management efficiency also increases market power (reducing profitability), increases capital structure (increasing profitability) and increases risk tolerance (reducing profitability). More specifically, in model 1, a 1% increase in management efficiency will lead to a direct increase in profitability of 0.481% but an indirect decrease in profitability of -0.01% through other variables in the model, and thus the total impact of management efficiency on bank profitability is 0.471% (Appendix 2).

Bank size only has a direct impact on bank profitability in model 2. In the remaining two models, bank size affects bank profitability indirectly through the endogenous variables market power, capital structure and bank risk tolerance. The total impact results in all three models are negative (Model 1: -0.541, Model 2: -0.653 and Model 3: -0.486). Hypothesis H5 is rejected in practice. The main reason for the negative correlation between size and profitability can be explained as follows: Large-scale banks in Vietnam are mainly state-owned commercial banks with customers being state-owned enterprises, so the bad debt ratio is higher than that of small-scale banks, which are mainly joint-stock commercial banks, so the profitability is not high.

Similar to the bank size variable, the level of market concentration only directly affects profitability in model 2, the remaining models have no statistical significance. In terms of total impact, the signs of the coefficients are all negative (model 1: -0.284, model 2: -0.253, model 3: -0.249). This shows that there is no collusive behavior based on increasing the level of concentration to increase profitability. The research results do not support the SCP theory and hypothesis H6 is rejected. This is also the research result of Berger and Hannan (1997), Demirgüç-Kunt and Huizinga (1999) and Thao Ngoc Nguyen and Chris Stewart (2013). According to Thao Ngoc Nguyen and Chris Stewart (2013), Vietnamese banks focus on increasing equity, lending, assets, mobilization, operating network and reducing bad debt ratio, so revenue and profit are not the most important tasks in this period. Notably, the level of concentration has a positive impact on management efficiency before the crisis but a negative impact after the crisis. This shows that in the crisis period, large-scale banks find it difficult to ensure management efficiency due to the complexity of the bank's organization.

Economic growth rate has a positive and significant impact on bank profitability in model 1. Hypothesis H7 is accepted in practice. This is also the research result of Demirguc – Kunt and Huizinga (2000), Bikker and Hu (2002) and Dietrich and Wanzenried (2011). However, the impact of economic growth rate on profitability is through bank management efficiency.

In summary, through the analysis of the results of the models, the impact of some factors on the profitability of banks has been shown. Vietnamese banks in the research period mainly generate profits based on management efficiency rather than taking advantage of scale. This is reflected in the direction of the impact of management efficiency on the profitability of banks, which is positive, while the direction of the impact of market power and the level of concentration is negative. In addition, the variables of capital structure and economic growth rate have positive impacts while the variables of scale and risk tolerance have positive impacts on the profitability of banks. In addition, the research results also show that there is a trade-off between the variables affecting the profitability of banks. Management efficiency has a direct positive impact on the profitability of banks, while management efficiency also increases market power (reducing

profitability), increasing capital structure (increasing profitability) and increasing risk tolerance (decreasing profitability).

4.3. Bootstrap Testing

To evaluate the reliability of the above estimation results, Bootstrap test was chosen with 500 replicate samples. The test results are presented in Table 4.5. The absolute value of CR of the estimates is less than 1.96 (except for the relationships CONC STRCAP and CONC MKT.PWT), so it can be said that the bias is small and not statistically significant at the 95% confidence level. Thus, we can conclude that the estimates in the model are reliable (except for the relationships CONC STRCAP and CONC MKT.PWT).

Table 4.5: Bootstrap estimation results with N = 500

Relationship

ML Estimate | Bootstrap Estimation | ||||||||

SE | SE-SE | Mean | Bias | SE- Bias | CR | ||||

MAN.EFF | <--- | GROW | 4.2610 | 1.3020 | 0.0410 | 4.2980 | 0.0360 | 0.0580 | 0.6210 |

CRL | <--- | MAN.EFF | 0.0070 | 0.0020 | 0.0000 | 0.0060 | 0.0000 | 0.0000 | 0.0000 |

CRL | <--- | CONC | 0.0560 | 0.0160 | 0.0000 | 0.0560 | 0.0000 | 0.0010 | 0.0000 |

CRL | <--- | SIZE | 0.0020 | 0.0000 | 0.0000 | 0.0020 | 0.0000 | 0.0000 | 0.0000 |

MKT.PWT | <--- | MAN.EFF | 0.0420 | 0.0080 | 0.0000 | 0.0420 | 0.0000 | 0.0000 | 0.0000 |

STRCAP | <--- | MAN.EFF | 0.0900 | 0.0200 | 0.0010 | 0.0910 | 0.0010 | 0.0010 | 1.0000 |

STRCAP | <--- | CONC | (1.0890) | 0.1310 | 0.0040 | (1.1070) | (0.0180) | 0.0060 | (3.0000) |

MKT.PWT | <--- | CONC | 0.7370 | 0.0930 | 0.0030 | 0.7240 | (0.0120) | 0.0040 | (3.0000) |

MKT.PWT | <--- | SIZE | 0.0270 | 0.0020 | 0.0000 | 0.0270 | 0.0000 | 0.0000 | 0.0000 |

STRCAP | <--- | SIZE | (0.0490) | 0.0050 | 0.0000 | (0.0490) | 0.0000 | 0.0000 | 0.0000 |

MKT.PWT | <--- | CRL | 1.2690 | 0.4340 | 0.0140 | 1.2830 | 0.0150 | 0.0190 | 0.7890 |

PROF | <--- | CRL | (0.3390) | 0.0750 | 0.0020 | (0.3370) | 0.0020 | 0.0030 | 0.6670 |

PROF | <--- | STRCAP | 0.0370 | 0.0090 | 0.0000 | 0.0380 | 0.0010 | 0.0000 | 0.0000 |

PROF | <--- | MAN.EFF | 0.0200 | 0.0020 | 0.0000 | 0.0200 | 0.0000 | 0.0000 | 0.0000 |

PROF | <--- | MKT.PWT | (0.0300) | 0.0100 | 0.0000 | (0.0290) | 0.0010 | 0.0000 | 0.0000 |

Source: Author's calculation

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS

5.1. Conclusion

The thesis uses structural equation modeling (SEM) to examine the impact of some internal and external factors on the profitability of 38 Vietnamese commercial banks in the period 2004 - 2011. At the same time, in order to assess the impact of the 2008 financial crisis on the impact of factors on profitability, the thesis considers two more periods before the crisis (2004 - 2007) and after the crisis (2008 - 2011). The research results show that governance efficiency and capital structure have a positive impact on profitability. In contrast, market power and the level of risk tolerance of banks have a negative impact on profitability. This shows that banks generate profits based on governance efficiency rather than taking advantage of scale. The research results also do not support the SCP and RMP theories in practice.

In terms of influence, management efficiency has the strongest impact, showing the importance of bank performance. Efficient banks will generate more profits than banks with poor performance. Therefore, banks that want to increase profits need to improve management efficiency based on the standards proposed by the Basel Committee. The second most influential variable is the bank's capital structure. Banks with a high ratio of equity to total assets lead to high profits. This is a very important factor for the bank's profitability, especially during a crisis, using equity will have the lowest cost while increasing the bank's stability and competitiveness. Risk tolerance and market power have a negative impact on bank profitability. The higher the risk tolerance, the lower the profitability.

Thus, managing and minimizing credit risk will help increase profits. This can be done through the issuance of reasonable and effective credit procedures and ensuring that they are implemented consistently within the bank and strictly by credit officers.

increased market power will reduce profitability. Therefore, it is necessary to increase competition in the banking market. The exogenous variables of bank size, concentration and economic growth mainly indirectly affect profitability through endogenous variables.

The financial crisis has a real impact on Vietnamese banks and their profitability. For example, the capital structure variable increases its impact as the crisis progresses, risk tolerance has a negative impact on profitability before the crisis but the impact is insignificant after the crisis.

The results also show that there is a trade-off between variables that affect bank profitability. For example, governance efficiency has a direct positive impact on bank profitability, while governance efficiency also increases market power (reducing profitability), increases capital structure (increasing profitability), and increases risk tolerance (reducing profitability).

5.2. Recommendations

Based on the above conclusions, the thesis makes the following recommendations:

Banks should pay attention to improving management efficiency because this is the most important factor affecting the stability and development of the bank. At the same time, banks should also consider the trade-offs between factors affecting profitability.

Increasing equity not only increases profits but also helps banks increase competitiveness, operate stably and absorb unexpected financial shocks.

Effectively control the level of risk acceptance. To achieve this, in addition to the lending regulations of the State Bank, banks must build their own customer credit rating system to accurately assess the risks of loans to set reasonable lending rates. At the same time, it is necessary to build a lending process, a credit risk management process, a credit risk handling process based on the characteristics of each bank and it is especially important to separate the sales function and the operation function.