warehouse. Applying this method to manual accounting is quite complicated and difficult. However, the company has applied Misa software, so determining the average unit price after each import becomes easier and more convenient. This method will give results with higher accuracy than the weighted average method at the end of the period. At the same time, the accountant's workload will not be accumulated at the end of the month and will meet the timely requirements of accounting information. Note that when the company changes the method of calculating the warehouse price, it must comply with the principle of consistency.

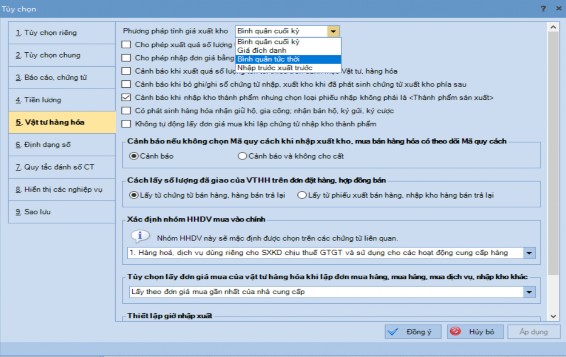

For example, at the end of the 2019 accounting year, the company changes the method of calculating the cost of goods sold from the weighted average at the end of the period to the instantaneous average. The accountant changes the method of calculating the cost of goods sold on the Misa software by the following operation: Select System/Options/Goods and materials. Then, the accountant selects the instantaneous average method. Finally, click the OK button.

Figure 3.1: Interface for changing the method of calculating the warehouse price

(Source: Dong Duong Equipment and Spare Parts Joint Stock Company)

- Complete the allocation of purchasing costs (warehouse fees) for each imported item:

The company should allocate purchasing costs for each imported item more flexibly. This means that depending on the characteristics of each shipment, the company

Cost of purchasing fertilizer complement to item i | = | Total cost of purchase | x | The value of item i |

Total value of purchased goods |

Maybe you are interested!

-

Perfecting the Organization of Applying the Production Cost Accounting Method to Serve Cost Management Accounting

Perfecting the Organization of Applying the Production Cost Accounting Method to Serve Cost Management Accounting -

Perfecting cost accounting with enhanced cost management in animal feed processing enterprises - 44

Perfecting cost accounting with enhanced cost management in animal feed processing enterprises - 44 -

Accounting for Revenue, Expenses and Business Results from a Management Accounting Perspective

Accounting for Revenue, Expenses and Business Results from a Management Accounting Perspective -

Perfecting management accounting in forestry companies in Tuyen Quang province - 2

Perfecting management accounting in forestry companies in Tuyen Quang province - 2 -

Perfecting the organization of accounting to strengthen financial management in administrative units of the Labor - Invalids and Social Affairs sector - 35

Perfecting the organization of accounting to strengthen financial management in administrative units of the Labor - Invalids and Social Affairs sector - 35

Choose the allocation criterion as the quantity of purchased goods or the value of purchased goods. For shipments with similar purchase values of each item, the allocation criterion should be the quantity of purchased goods. For shipments with very different purchase values of each item, the allocation criterion should be the value of purchased goods. This will be more reasonable and will help the company accurately determine the actual value of each imported item because the purchase cost for the company's imported goods is quite large. The company can allocate the purchase cost for each imported item according to the following formula:

For example, in May 2019, the company imported a shipment of 400 pieces of non-alloy steel concrete pump pipes (OBBT13) and 200 pieces of non-alloy steel heating concrete pump pipes (OGN04) with unit prices of 36 USD and 53 USD respectively, the tax calculation exchange rate is 24,007 VND/USD, the selling exchange rate announced by MBbank - where the company opened a transaction account is 23,460 VND/USD, both items are subject to import tax at a rate of 0%, the total purchase cost is 12,875,455 (VND). At that time, the converted purchase value of OBBT13 and OGN04 into VND is 337,824,000 (VND) and 248,676,000 (VND), respectively. The accountant allocates the purchase cost to two types of goods:

Allocation for OBBT13

Purchase cost12,875,455 | |||

= | x | 337,824,000 | = 7,416,262 (VND) |

337,824,000+248,676,000 | |||

for OGN04

Allocated purchasing costs12,875,455 | |||

= | x | 248,676,000 | = 5,459,193 (VND) |

337,824,000+248,676,000 | |||

At that time, the actual value of the two types of goods in stock is determined as follows: OBBT13 = 337,824,000 + 7,416,262 = 345,240,262 (VND)

OGN04 = 248,676,000 + 5,459,193 = 254,135,193 (VND)

* Complete inventory accounting:

- Complete accounting documents:

The company should establish a document delivery book when transferring documents between departments. Each time a document is transferred, the parties delivering and receiving the document must sign the document delivery book. This makes it easy to assign responsibility to the right person and department if a document is lost so that appropriate measures can be taken. In addition, establishing a document delivery book will help the company closely manage the company's documents, and further enhance the sense of responsibility of officers and employees for work in general and document management in particular. The company can establish a document delivery book according to the following form:

Form 3.1: Document delivery book

DOCUMENT DELIVERY BOOK

STT

Document | Amount above document | Sign | |||

Number | Date | Delivery person | Receiver | ||

In addition, the company should collect, preserve and store all accounting documents related to imported goods. Import business uses documents to record information including documents arising domestically and internationally. The set of payment documents for imported goods, depending on the terms of the letter of credit, includes the following main documents:

+ Commercial invoice (Invoice)

+ Bill of lading

+ Insurance Policy

In addition, according to the import-export contract documents and the provisions in the letter of credit, the payment documents also include:

+ Certificate of Quality

+ Packing Lits

+ Certificate of Original

+ Tax receipts, customs declarations, warehouse receipts, fee receipts, VAT invoices, payment vouchers, debit and credit notes from banks, etc.

+ Other accompanying documents such as settlement report with vehicle owner, damage report, etc.

- Complete the inventory price reduction provision:

Currently, the goods of Dong Duong Equipment and Spare Parts Joint Stock Company are very diverse and rich in types, designs, properties and many of them are of high value. In addition, the prices of the goods that the company is trading in the market fluctuate frequently. Therefore, the provision for inventory devaluation is really necessary for the company. The company should set up a provision for inventory devaluation to compensate for actual losses caused by inventory devaluation, and at the same time help the company reflect the true realizable net value of the inventory when preparing the annual financial statements. At that time, the company will use account 229(4) - "Provision for inventory devaluation" to reflect the provision or reversal of inventory devaluation. According to Article 4 of Circular 48/2019/TT-BTC, the level of provision for inventory devaluation is determined as follows:

= | Actual inventory quantity at the time of preparing annual financial statements | x | Original price of inventory according to accounting books | - | Net realizable value of inventory |

In which, the net realizable value of inventory is determined by the company itself as the estimated selling price of inventory in the normal course of business at the time of preparing the annual financial statements minus (-) the estimated cost to complete the product and the estimated cost necessary for consuming them.

The inventory price reduction provision is calculated for each inventory item that is discounted and summarized in a detailed list. The detailed list is the basis for accounting for the company's cost of goods sold.

- When preparing the financial statements, compare the inventory devaluation reserve that must be established this period with the inventory devaluation reserve that was established in the previous period. If the inventory devaluation reserve that must be established this period is greater than the amount set aside from the previous period, the accountant will set aside the difference by recording an increase in the cost of goods sold in the Debit side of Account 632 and an increase in the inventory devaluation reserve in the Credit side of Account 229(4). In the opposite case, the accountant will reverse the difference by recording a decrease in the inventory devaluation reserve.

Inventory price is debited to account 229(4) and cost of goods sold is reduced to credit to account 632.

For example, on December 31, 2019, the company's inventory of item code GCS12 - "Soft rubber gasket, used to line the hydraulic cylinder of a concrete pump" is 62 pieces, the inventory unit price of GCS12 is 1,085,559 (VND/piece). Suppose that the provision for item code GCS12 before 2019 is zero and at December 31, 2019, the market price of item GCS12 is 956,000 (VND/piece), the estimated selling cost is 0 VND. Based on the above information, the accountant determines the provision for inventory price reduction for GCS12 as: (1,085,559 - 956,000) x 62 = 8,032,658 (VND). At that time, the accountant recorded an increase in cost of goods sold of 8,032,658 (VND) and an increase in inventory price reduction provision of 8,032,658 (VND).

Accounting: Debit account 632 8,032,658

Credit account 2294 8,032,658

3.2.2 Perfecting inventory accounting from the perspective of management accounting

* Perfecting the management accounting organization model:

The company should pay more attention to management accounting and enhance the role and importance of management accounting. Based on the business characteristics and specific management requirements of the company, scientifically develop the content, tasks and powers of management accounting for the accounting department. If this is done, the company will save time and human resources in accounting work, avoid duplication of work, and harmoniously and consistently combine financial accounting and management accounting. At the same time, the accounting apparatus will be streamlined and maximize the role of each accounting staff.

* Complete the construction of inventory standards and estimates:

Building inventory norms and estimates is very important in organizing, managing, and effectively using the company's materials, goods, and capital. Inventory estimates must be built accurately, in accordance with the company's capabilities and conditions. To make inventory estimates, the company must not only rely on empirical statistical methods but also consider the company's management requirements, market demand, and factors affecting the company's business operations. Currently, the company has not built inventory estimates. Therefore, the author

boldly propose that the company should make an inventory budget and build a number of inventory budgets according to the form presented in Appendix 1.20; Appendix 1.21; Appendix 1.22 .

* Complete inventory information collection:

- Regarding accounting documents, the company needs to apply principles and methods of creating, circulating, managing and using accounting documents in accordance with its specific conditions. Specify and supplement necessary contents into each prescribed accounting document form to serve the purpose of collecting internal management information.

- Regarding accounting accounts, the company bases on the accounting account system issued by the Ministry of Finance to detail according to the levels in accordance with the established plans and estimates and the requirements for providing management accounting information to managers.

- Regarding accounting books, the company bases on the accounting book system issued by the Ministry of Finance to design book templates suitable for management requirements according to inventory types, each department, each job and other requirements of management accounting.

* Complete inventory information analysis:

In the coming time, the company should conduct inventory information analysis. This will help the company promptly grasp unusual fluctuations in inventory; thereby proposing effective inventory management solutions.

- Analysis of inventory ratio in total assets:

in total assets

Inventory ratio= | Inventory value | x 100% |

Total assets |

Based on this indicator, the company will know what proportion of total assets inventory accounts for, whether it is high or low, whether it tends to increase or decrease by comparing this indicator between years to see unusual fluctuations in inventory, thereby having appropriate solutions.

For example, in 2019, the company had total assets of 18,634,905,728 (VND), inventory of 5,997,123,618 (VND), then the proportion of inventory in total assets in 2019 = (5,997,123,618/18,634,905,728) x 100% = 32.18%. For a

For a trading enterprise specializing in goods trading such as Dong Duong Equipment and Spare Parts Joint Stock Company, the proportion of inventory in total assets in 2019 as above is quite low. Compared to the proportion of inventory in total assets in 2018

={(11,316,005,845/24,860,287,971)x100%} = 45.52% then the proportion of inventory in total assets in 2019 is on a sharp downward trend. The company needs to consider the cause and have appropriate solutions for the following years.

- Analysis of inventory turnover ratio:

Coefficient of rotation of inventory | = | Cost of goods sold |

Average inventory |

Analyzing the inventory turnover ratio helps companies know the inventory turnover rate, thereby helping managers analyze factors affecting inventory reserves and make decisions to adjust inventory levels appropriately and ensure effective use of working capital.

In which, average inventory is the average of last year's inventory and this year's inventory.

For example, in 2019, the company's average inventory was 8,656,564,729 (VND), the cost of goods sold was 13,238,497,587 (VND), then the inventory turnover ratio in 2019 = 13,238,497,587/{(11,316,005,845 + 5,997,123,618)/2} =

1.53. Thus, in 2019, the company turned over its inventory 1.53 times. This ratio is quite low, showing that there are many goods stagnant in the warehouse. The company needs to take measures to promote consumption and reduce purchases during the period.

The company can calculate the inventory turnover ratio for each item to know whether different items are selling quickly or slowly to make decisions about which items to sell more and which items to sell less.

- Inventory cost analysis: This is necessary for managers to come up with appropriate inventory storage plans, decisions on building inventory levels, and correct purchasing decisions. Inventory cost analysis includes: ordering costs, storage costs, and costs due to inventory shortages.

* Complete inventory information provision:

To truly become a management tool for administrators, inventory management accounting reports need to be built in accordance with the requirements for providing information to serve internal management of the enterprise and the content of the reports must ensure that they fully reflect the information serving the requirements of management, operation and

economic decision making of the enterprise. Therefore, the author would like to propose some inventory management report templates as follows:

Form 3.2: Inventory Report

INVENTORY REPORT

Month: ………

STT

Code row | Name row | Unit | Existing head | During the period | Existing last | Single price | Value inventory | ||

Enter | Export | ||||||||

Form 3.3: Report on goods supply situation

REPORT ON GOODS SUPPLY SITUATION

Month: ………

Product name

Quantity actual import | Quantity to buy as planned | % refund plan | |

Form 3.4: Report on timeliness of goods supply

REPORT ON TIMELINESS OF GOODS SUPPLY

Month: ………

Import times

Date of entry | Quantity | Guarantee the need | End of month inventory | Note | ||

Quantity | Number of days | |||||

3.3 Conditions for implementing the solution

* On the state side: