It is necessary to further strengthen specialized training courses for specialized staff in the banking sector in the coming time, ensuring that these staff are all trained in relevant courses, always updated and supplemented with new knowledge, keeping up with modern technology and being able to answer customer questions as quickly and accurately as possible.

In addition, the Bank needs to continue training employees and optimizing customer care functions in the customer relationship management (CRM) software system, including:

- Gather all customer information into one system, store all information and transaction history with customers. This helps the bank avoid the situation where each employee manages and takes care of their own customers, leading to loss of customer information when the employee leaves the job.

- Control what employees are doing and how customer care is progressing for each customer. This ensures that employees will implement sales and customer care processes according to standards, avoiding losing customers due to poor care.

Maybe you are interested!

-

Proposing Solutions to Improve the Effectiveness of Protecting Industrial Property Rights by Civil Measures

Proposing Solutions to Improve the Effectiveness of Protecting Industrial Property Rights by Civil Measures -

Testing the Necessity and Feasibility of Measures to Improve Teaching Capacity in the Field of Science and Technology for High School Teachers

Testing the Necessity and Feasibility of Measures to Improve Teaching Capacity in the Field of Science and Technology for High School Teachers -

Measures to Improve Selection Efficiency

Measures to Improve Selection Efficiency -

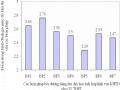

According to you, which electronic service distribution channel has the most development potential in Vietnam today: ATM, Pos, Internet Banking, Mobile Banking?

According to you, which electronic service distribution channel has the most development potential in Vietnam today: ATM, Pos, Internet Banking, Mobile Banking? -

Comparison of Traditional Banking Services and Electronic Banking Services

Comparison of Traditional Banking Services and Electronic Banking Services

- Helps managers know the potential of each customer as well as analyze and evaluate transactions with customers. Which transaction groups and customer groups need to be focused on promoting, which stages are having problems, which customers need “special” care… With this information, managers can evaluate the business situation, the ability to achieve the plan, the set goals and come up with timely solutions.

- Finally, the CRM system helps banks collect and effectively exploit accumulated business knowledge and "inherit" it for future generations. Banks will not spend much time training new employees, deploying promotions to the right customers, and the right programs to promote.

In addition, Sacombank can add to the service registration contract

The terms of dispute resolution and dispute resolution should any arise to create a legal basis for customers to feel secure in using the service. It should be noted that the bank should make commitments in a way that is beneficial to the customer.

6.2.5. Measures to comprehensively improve ease of use, usefulness and customer service

First, ensure customer experience across channels

- Omni-channel Digital Banking platform, including eKYC across all channels

- New website platform, analyze customer behavior for marketing and sales

- Smart transaction counter – VTM

Second, understand your customers deeply.

- Data management – DG phase 2

- Improved Data Warehouse

- Forecasting analysis

- Behavioral analysis

- Provide real-time reporting data

Third, optimize operations

- Smart process and form digitization platform.

- Robotic Process Automation (RPA). RPA works with other software such as Excel, accounting software, banking, and artificial intelligence applications to perform large-volume, repetitive tasks in cycles such as: data entry, order creation, access authorization, and tasks that require continuous communication with many different systems. Simply put, RPA is a robot that operates continuously 24/7/365, automatically processing work on the computer, helping to minimize errors, helping businesses optimize resources at the most reasonable cost.

- ECM – electronic document and content warehouse helps manage unstructured information

structure in the enterprise. ECM provides strategies and methods to manage, store and secure enterprise documents. EMC information can be in the form of paper documents, data files, databases or even emails.

- ITSM – effective IT operations and service management tool that ensures the right combination of technology, people and processes are used to deliver the right value. It includes all the individual activities that support services throughout their lifecycle.

Fourth, sustainable infrastructure, and security

- Unified hardware

- Cloud - Cloud computing

- DLP - Data Protection

- PAM - privileged account management

- IAM - Identity Management

- NAC - Network Access Control

6.3. Limitations of the Thesis and future research directions

Although the researcher has made great efforts in the process of implementing the thesis, due to limited resources, the thesis still has some limitations as follows: Firstly, the researcher has not been able to survey all individual customers at all branches of Sacombank due to time constraints and relationships with bank branch leaders. Secondly, due to the unavailability of secondary data sources, some issues have not been deeply analyzed in the process of researching the conditions for developing e-banking services in Vietnam.

After this Thesis, further studies can be conducted more comprehensively and the research sample will be more representative. On the other hand, further studies can also continue to expand this research direction by supplementing and editing the research model of the Thesis to perfect the research model to be more and more suitable to the characteristics in Vietnam and find other factors that can

affecting the intention to use electronic banking services.

Chapter 6 Summary

Chapter 6 presents the conclusions of the PhD student on the main results that have been summarized during the implementation of the thesis. Based on these conclusions, the PhD student has presented specific recommendations for Sacombank so that the bank's managers can study and use the recommendations in the process of planning business strategies and making business decisions related to e-banking services. The recommendations focus on specific measures to improve the ease of use of e-banking services, improve the usefulness of e-banking services, impact on customers' subjective standards and improve the quality of customer service, thereby maintaining and promoting the intention to use e-banking services in the future.

LIST OF PUBLISHED SCIENTIFIC WORKS

1. Nguyen Quang Tam (2020), "Factors affecting the intention to use e-banking services of individual customers at Sacombank", Industry and Trade Magazine, (No. 1 - January 2020), 284-293.

2. Nguyen Quang Tam (2020), “Developing e-banking services in Vietnam in the coming time”, Economics and Forecast, (No. 07 - March 2020), 33-36.

3. Citation: Le DT, Nguyen HP, Ho VN, HO TPY, Nguyen QT, Le

NNA (2018) Technology Acceptance and Future of Internet Banking in Vietnam. Foresight and STI Governance, vol. 12, no 2, pp.36-38.

4. Citation: Le DT, Nguyen HP, Nguyen QT, Nguyen NT, Le QM (2020) Research on Factors Affecting to Customers' Intention to Online Shopping: Empirical Evidence in Vietnam Emerging Economy. WSEAS TRANSACTIONS on BUSINESS and ECONOMICS, ISSE / E-

ISSE: 1109-9526 / 2224-2899, Volume 17, 2020, Art. #43, pp. 441-453

LIST OF REFERENCES

Vietnamese

1. Nguyen Thi An Binh (2016). Research on factors affecting customer loyalty in the retail sector at Vietnamese joint stock commercial banks, PhD thesis .

2. Ministry of Information and Communications (2017). Vietnam Information and Communications Technology White Book 2017 .

3. Ministry of Information and Communications (2018), Report on Readiness Index for Development and Application of Information and Communications Technology in Vietnam in 2017.

4. Bui Pham Thanh Binh, Do Van Ninh, Nguyen Thu Thuy (2016). Research on customer satisfaction with card service quality of Saigon Thuong Tin Commercial Joint Stock Bank (Sacombank) - Khanh Hoa Branch. Journal of Fisheries Science and Technology, No. 1 .

5. Ha Nam Khanh Giao & Ha Minh Dat (2014), Evaluation of factors in choosing commercial banks in Ho Chi Minh City for the elderly. Economic Development Journal , No. 280, pp. 97 - 115.

6. Pham Thi Bich Duyen (2016). Debit card service quality at Vietnamese commercial banks, PhD thesis .

7. Pham Thuy Giang (2012). Comparative study on retail banking service quality between 100% foreign-owned banks and Vietnamese joint stock commercial banks . PhD thesis .

8. Ha Nam Khanh Giao & Ha Minh Dat (2020). Evaluating factors in choosing commercial banks in Ho Chi Minh City for the elderly. Journal of Economic Development , 97-115.

9. Vietnam E-commerce Association (2018). Vietnam E-commerce Index Report 2018 .

10. La Thi My Hoa (2015), Analysis of factors affecting the decision to choose

Choosing a commercial bank to deposit savings of individual customers in Ho Chi Minh City. Master's thesis in economics, University of Finance - Marketing.

11. Le Phan Hoa (2016), Research on the impact of trust on the intention to use ATM services of students in Hanoi. Journal of Economics and Development , No. 227(II), May 2016, pp. 81-90.

12. Le Thi Thu Hong (2014). Evaluating customer satisfaction with the quality of payment card services of Vietinbank - Can Tho Branch. Can Tho University Science Journal .

13. Nguyen Hoang Bao Khanh (2014), Research on acceptance and use of internet banking services by individual customers in Hue city. Hue University Science Journal . Vol 101.

14. Nguyen Minh Kieu (2007). Banking operations. Statistical Publishing House.

15. Le Van Huy, Truong Thi Van Anh (2008). Research model of E-banking acceptance in Vietnam. Journal of Economic Research, No. 7.

16. Do Thi Nhu Ngan (2015). Research on factors affecting the acceptance of BIDV E-Banking service by individual customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Da Nang Branch .

17. Pham Thi Tam & Pham Ngoc Thuy (2010), Factors affecting individual customers' tendency to choose a bank. Journal of Banking Science and Training , No. 103, December 2010.

18. iPrice Group (2018), Southeast Asia E-commerce Landscape 2017 .

19. Nguyen Duy Thanh, Cao Hao Thi (2011). Proposing a model for accepting and using e-banking in Vietnam. Journal of Science and Technology Development, No. 2.

English

13. Alalwan, AA, Dwivedi, YK, Rana, NP, & Williams, MD (2016). Consumer adoption of mobile banking in Jordan. Journal of Enterprise Information Management .

14. Alam, SS, & Rashid, M (2012). Intention to use renewable energy: Mediating role of attitude. Energy Research Journal, 3 (2), 37-44.

15. Anouze, ALM, & Alamro, AS (2019). Factors affecting intention to use e-banking in Jordan. International Journal of Bank Marketing .

16. Ajzen, I. (1991). The theory of planned behavior. Organizational behavior and human decision processes, 50(2), 179-211.

17. Ajzen, I., & Fishbein, M. (1975). Belief, attitude, intention and behavior: An introduction to theory and research. In: Reading, MA: Addison-Wesley.

18. Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior.

19. Akturan, U., & Tezcan, N. (2012). Mobile banking adoption of the youth market: Perceptions and intentions. Marketing Intelligence & Planning, 30 (4), 444-459. doi:doi:10.1108/02634501211231928

20. Alsajjan, B., & Dennis, C. (2010). Internet banking acceptance model: Cross-market examination. Journal of business research, 63 (9), 957-963.

21. Amin, A., Mahmoud-Ghoneim, D., Syam, M.I., & Daoud, S. (2012). Neural network assessment of herbal protection against chemotherapeutic- induced reproductive toxicity. Theoretical Biology and Medical Modeling, 9 (1), 1. doi:10.1186/1742-4682-9-1

22. Anderson, J.C., & Gerbing, D.W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological bulleting, 103 (3), 411.

23. Bandura, A. (1977). Social learning theory Englewood Cliffs. In: NJ: Prentice-Hall.