Phase 1 Phase 2

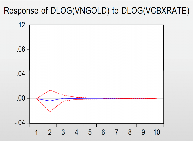

Figure 3.4: Impulse-Response results of VCBXRATE to VNGOLD in phase 2

Figure 3.4 shows that in both periods, the impact of exchange rate shocks on domestic gold prices is quite weak and often has a short impact cycle.

(ii) Relationship between CPI and domestic gold price

Phase 1 Phase 2

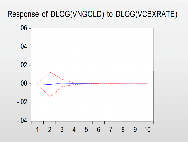

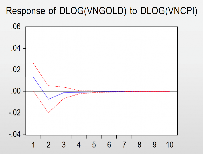

Figure 3.5: Impulse-Response result of VNGOLD to VNCPI

Figure 3.5 shows that when there is a shock in gold price, CPI does not fluctuate immediately but tends to increase to a peak in 2 months, then gradually decrease within 6-7 months. However, in phase 2, CPI fluctuations tend to be smaller.

Phase 1 Phase 2

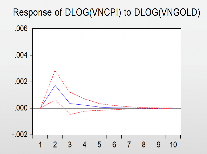

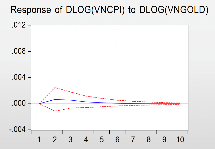

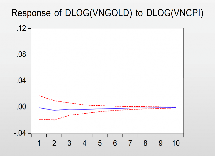

Figure 3.6: Impulse-Response result of VNCPI to VNGOLD

In phase 1, when the CPI increased by 1 standard deviation, the gold price increased by 1.3%, but then decreased and returned to equilibrium. However, in phase 2, when the CPI increased by 1 standard deviation, the gold price decreased by 0.3% and then stabilized within 6 months.

(iii) Relationship between interest rates and domestic gold prices

Phase 1 Phase 2

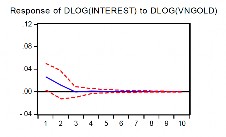

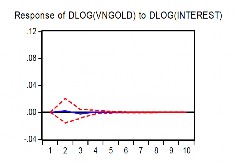

Figure 3.7: Impulse-Response results of VNGOLD to INTEREST

Figure 3.7 shows that when there is a 1 standard deviation gold price shock, the average deposit interest rate increases by 2.6% in period 1. However, in period 2 cents, the interest rate remains almost unchanged.

Phase 1 Phase 2

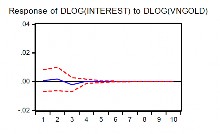

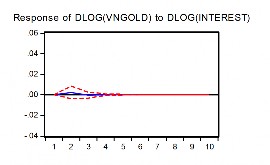

Figure 3.8: Impulse-Response results of INTEREST to VNGOLD

On the contrary, the shock in average deposit interest rates does not have an immediate impact on gold prices, and the subsequent impact is also insignificant.

(iv) Relationship between foreign exchange reserves and domestic gold prices

Phase 1 Phase 2

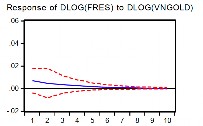

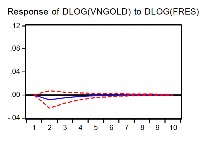

Figure 3.9: Impulse-Response results of VNGOLD to FRES

Figure 3.9 shows that when there is a shock in gold price increasing by 1 standard deviation, in phase 1, the average mobilization interest rate increases by 0.7%. However, in phase 2, it does not change immediately, with an increasing trend from 3 to 6 months.

Phase 1 Phase 2

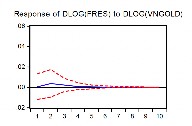

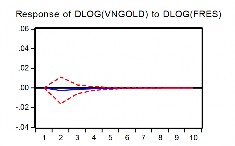

Figure 3.10: Impulse-Response results of FRES to VNGOLD

On the contrary, the shock to the national foreign exchange reserves has almost no effect.

immediate impact on gold prices, which is evident in both periods.

(v) Relationship between domestic gold price and domestic and world gold price shock

Phase 1 Phase 2

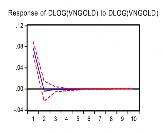

Figure 3.11: Impulse-Response results of VNGOLD by VNGOLD shock

Figure 3.11 shows the impact of domestic gold price shock on domestic gold price itself. In phase 1, the impact of the shock is very large and occurs quickly in the short term of 1 month. When the shock of VNGOLD increases by 1 standard deviation, VNGOLD increases by 7.7%. In phase 2, the impact of the shock is longer but the level is smaller. The impact level when the shock of VNGOLD increases by 1 standard deviation, VNGOLD increases by 4.7%, the impact gradually decreases within 4 months.

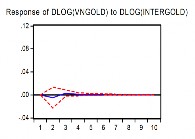

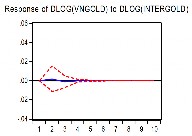

Phase 1 Phase 2

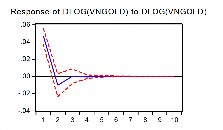

Figure 3.12: Impulse-Response results of VNGOLD due to INTERGOLD shock

The reaction of domestic gold prices to the shock of international gold prices in the two stages was quite weak in the first cycle and had an impact within 3-4 months. This shows that domestic gold prices are greatly affected by the psychology of speculators. Speculators often overreact to gold prices. At the same time, in stage 2, when the domestic gold market was not connected to the international market, the impact of the gold shock decreased significantly, which shows that the psychology of investors was more stable in stage 2 than in stage 1.

3.3.4. Results of running variance decomposition of domestic gold price

(i) Variance decomposition of domestic gold price in period 1

Table 3.10: VNGOLD variance decomposition phase 1

Period

SE | DLOG (VNCPI) | DLOG (VNGOLD) | DLOG (INTERGOLD) | DLOG (VCBXRATE) | DLOG (FRES) | DLOG (INTEREST) | |

1 | 0.007262 | 0.005900 | 99.99410 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

2 | 0.008838 | 0.383956 | 97.80115 | 0.395714 | 0.241299 | 1.110514 | 0.067366 |

3 | 0.009513 | 0.518597 | 97.03809 | 0.519251 | 0.249591 | 1.520517 | 0.153956 |

4 | 0.009805 | 0.691375 | 96.75673 | 0.529643 | 0.250728 | 1.616705 | 0.154817 |

5 | 0.009934 | 0.781328 | 96.63532 | 0.539395 | 0.250638 | 1.637287 | 0.156034 |

6 | 0.009990 | 0.831612 | 96.57889 | 0.542842 | 0.250713 | 1.639509 | 0.156438 |

7 | 0.010013 | 0.857015 | 96.55214 | 0.544254 | 0.250731 | 1.639152 | 0.156711 |

8 | 0.010023 | 0.869141 | 96.53946 | 0.544779 | 0.250735 | 1.639028 | 0.156862 |

9 | 0.010027 | 0.874640 | 96.53351 | 0.544964 | 0.250735 | 1.639208 | 0.156938 |

10 | 0.010029 | 0.877022 | 96.53078 | 0.545025 | 0.250734 | 1.639460 | 0.156975 |

Maybe you are interested!

-

Evaluation of Land Use Rights Mortgage Results at Vietnam Bank for Agriculture and Rural Development, Dien Bien Province Branch

Evaluation of Land Use Rights Mortgage Results at Vietnam Bank for Agriculture and Rural Development, Dien Bien Province Branch -

Customer Satisfaction Survey Results on International Payment Activities at Anz Bank Vietnam

Customer Satisfaction Survey Results on International Payment Activities at Anz Bank Vietnam -

Correlation Coefficient Results and Significance Level of Correlation Coefficient Test for Joint Stock Commercial Bank Group

Correlation Coefficient Results and Significance Level of Correlation Coefficient Test for Joint Stock Commercial Bank Group -

Results of Lending Activities for Employment at the Vietnam Bank for Social Policies, Hanoi Branch in the Period 2018-2021

Results of Lending Activities for Employment at the Vietnam Bank for Social Policies, Hanoi Branch in the Period 2018-2021 -

Results of Exploratory Factor Analysis of Factors Related to Employee Motivation at Quang Binh Military Commercial Joint Stock Bank

Results of Exploratory Factor Analysis of Factors Related to Employee Motivation at Quang Binh Military Commercial Joint Stock Bank

(ii) Variance decomposition of domestic gold price in period 2

Table 3.11: VNGOLD variance decomposition phase 2

Period

SE | DLOG (VNCPI) | DLOG (VNGOLD) | DLOG (INTERGOLD) | DLOG (VCBXRATE) | DLOG (FRES) | DLOG (INTEREST) | |

1 | 0.003645 | 7.433076 | 92.56692 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

2 | 0.004665 | 8.915331 | 90.44945 | 0.157723 | 0.028636 | 0.257691 | 0.191169 |

3 | 0.004794 | 8.941034 | 90.24957 | 0.214253 | 0.056233 | 0.339386 | 0.199519 |

4 | 0.004828 | 8.957908 | 90.20619 | 0.215246 | 0.056929 | 0.364217 | 0.199512 |

5 | 0.004835 | 8.960109 | 90.19662 | 0.215680 | 0.057326 | 0.370774 | 0.199492 |

6 | 0.004836 | 8.960536 | 90.19484 | 0.215677 | 0.057401 | 0.372058 | 0.199490 |

7 | 0.004837 | 8.960623 | 90.19445 | 0.215680 | 0.057414 | 0.372345 | 0.199489 |

8 | 0.004837 | 8.960638 | 90.19437 | 0.215681 | 0.057417 | 0.372401 | 0.199489 |

9 | 0.004837 | 8.960642 | 90.19436 | 0.215681 | 0.057418 | 0.372412 | 0.199489 |

10 | 0.004837 | 8.960642 | 90.19436 | 0.215681 | 0.057418 | 0.372414 | 0.199489 |

The results of variance decomposition for 2 periods with domestic gold price show that: in both periods, the impact of variables VCBXRATE, FRES, INTEREST on domestic gold price VNGOLD is low. Period 1 is 0.25%, 1.63%, 0.15% respectively; period 2 is 0.05%, 0.37%, 0.19% respectively. At the same time, the impact of world gold price on domestic gold price tends to decrease from 0.54% to 0.21%. The impact of international gold price on domestic gold price often has a lag of 2 months. Looking at Tables 3.11 and 3.10, the variable VNGOLD is subject to its own internal influence, thereby reflecting the operating mechanism of the State Bank. The operating mechanism and State management policy of the State Bank are the main causes leading to fluctuations in domestic gold price. In phase 1, the fluctuation of VNGOLD was affected by its own shock with an impact coefficient of 99%, phase 2 was 92%. Therefore, it shows that domestic gold prices are more stable due to external impacts when the State Bank strictly controls the gold market. Thus, the results of the thesis are consistent with the study of Nguyen Duc Trung (2013) on the more stable gold prices with external impacts when the State Bank has strong measures to intervene in the gold market.

3.3.5. Discussion of results and policy recommendations

The results of running the VAR model in 2 periods from 01/2006 to 04/2012 and 05/2012 to 12/2016 are statistically significant because they have passed the basic tests: the variables are stationary at the first difference with a significance level of 1%, the LM Test has a significant correlation between the residuals, the model ensures stability.

Firstly, the research results of the thesis are consistent with some previous empirical studies such as: Gold prices in Vietnam are little affected by inflation when the State Bank controls the gold market, which is consistent with the research results of Bui Kim Yen, Nguyen Khanh Hoang (2014), and Chua and Woodward (1982) and Tkacz (2007) in which the psychological factor of investors is one of the factors affecting domestic gold prices.

At the same time, the domestic gold price in phase 1 has a very high correlation with the USD exchange rate, which is consistent with Sherman (1983), Dooley, Isard and Taylor (1995), Tully & Lucey, (2007), but in phase 2, this correlation is very low because the Vietnamese gold market is no longer closely connected to the world gold market.

Second, the Vietnamese gold market is very specific, the variables of exchange rate, inflation, and interest rate have very little impact on the gold price. The level of explanation and reaction of the above variables on the gold price is very low. This is explained by the unique characteristics of the Vietnamese gold market such as:

- Vietnamese people have a very high preference for gold, gold buying and selling is influenced by psychological factors. Investors often overreact to fluctuations in gold prices.

- The Vietnamese gold market has existed for a long time, however the gold mining industry is not yet developed, so the amount of gold consumed in Vietnam is mainly imported fuel gold from abroad.

- The State Bank is implementing tough measures to control the gold market in order to contribute to stabilizing the macro economy, thereby significantly affecting market operations.

Third, the influence of exchange rate, inflation and interest rate variables tends to decrease gradually on gold prices. In particular, the relationship between exchange rate and international gold price after the State Bank controlled the gold market is inversely related. The impact cycle of the above variables is usually 2-3 months, however, the opposite impact of gold price on these variables is larger and has a longer impact period of 5-6 months. At the same time, domestic gold price is greatly affected by the management policy of the State Bank. Therefore, the State Bank's gold market management policies need to be stable and consistent to further stabilize gold price, contributing to macroeconomic stability.

CONCLUSION OF CHAPTER 3

In chapter 3, the thesis presented the following contents:

- Using VAR econometric model in 2 periods from January 2006 to December 2016 to evaluate the gold market management policy in Vietnam.

- The thesis uses 6 variables to enter into the model: VNGOLD, INTERGOLD, VNCPI, VCBXRATE, INTEREST, FRES.

- The suitable model has passed the basic testing criteria, specifically: ADF Test for the VAR model, all variables VNGOLD, INTERGOLD, FRES, INTEREST, VNCPI, VCBXRATE are all at the first difference with a significance level of 1%. Next is the FPE SC, HQ and Portmanteau test, the test result of the suitable lag is 1 with the collected data and is used to estimate the variables. LM Test and AR ROOT TEST, both VAR models of the 2 stages 1 and 2 with lag of 1 are guaranteed, can be applied in analysis and forecasting.

- The Vietnamese gold market is very specific, the variables of exchange rate, inflation, and interest rate have very little impact on the gold price. The level of explanation and reaction of the above variables on the gold price is very low.

Through the model, it has been shown that the gold market management policy has a great impact on the variables VNCPI, VCBXRATE, INTEREST, especially the relationship between the exchange rate and the world gold price after Decree 24 is inversely related and the exchange rate reacts faster to the international gold price than the domestic gold price. At the same time, the domestic gold price (VNGOLD) is greatly affected by the shock itself, which is the operating and management mechanism of the gold market of the State Bank. From the results of the verification, the researcher gives the following discussion opinions and suggestions for related policies: the State Bank's gold market management policy needs to be stable and consistent to further stabilize the gold price, contributing to stabilizing the macro economy.

CHAPTER 4

SOLUTIONS TO IMPROVE STATE MANAGEMENT POLICY

FOR GOLD MARKET IN VIETNAM

4.1. Goals, viewpoints and orientations for gold market development in Vietnam

The socio-economic development strategy for the period 2011 - 2020 has highlighted the following main ideas: “Enhancing proactiveness and flexibility in operating monetary policy with the aim of promoting sustainable growth, stabilizing the macro-economy, strengthening inflation control, contributing to stabilizing the value of the domestic currency. Synchronously creating corridors and legal frameworks for the organization and operation of credit institutions and commercial banks. Forms of payment through banks are encouraged while oriented to limit and gradually replace non-cash payments. Actively and flexibly operate monetary policy and monetary policy according to market principles. Research and innovate policies related to foreign exchange and gold management; depending on market realities, carefully expand the scope and scale of capital transactions; strengthen inspection and control to eliminate the situation of foreign currency as the means of payment in Vietnam. Strengthen and enhance the role of the State Bank in planning, orienting and implementing monetary policy. Ensure coordination between fiscal policy and monetary policy. Develop a complete and strict inspection and supervision process for financial and monetary activities.”

Create a corridor with synchronization and smoothness in operation, regulate all types of markets, and liberalize the service and goods markets. The financial market is developed in the direction of completing the structure, expanding the scale and scope of operations, ensuring the safety of the operating system, perfecting the organization and management work, and improving the effective supervision process. The stock and gold markets are developed in both breadth and depth, under strict control. The real estate market is developed healthily and sustainably, speculation is controlled and prevented; real estate trading floors need to improve their mechanisms and methods of operation. Further develop the science and technology market on a fast and comprehensive basis; support and encourage science and technology activities to operate according to market rules and mechanisms.

4.1.1. Goals of developing Vietnam's gold market

Based on the reality of the gold market, based on the assessment of the Vietnamese and world gold markets in the future and to match Vietnam's economic conditions, the basic requirements for long-term market development goals are: