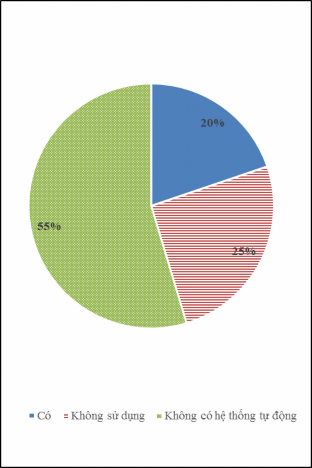

Regarding technology infrastructure, automatic reporting and data synthesis systems, 56% of respondents said that they only meet average work requirements. And 28% of respondents said that they only meet a very small part of work requirements. Meanwhile, less than 6% of respondents said that they meet above average work requirements. This shows that the technology infrastructure and automatic reporting systems serving the inspection and supervision of banks do not meet high work requirements. Reports are still mainly semi-automatic instead of automatic.

Chart 2.18: Using automatic system to synthesize reports and data

| |

Source: Survey results |

Maybe you are interested!

-

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development -

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1 -

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch -

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank -

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016:

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016:

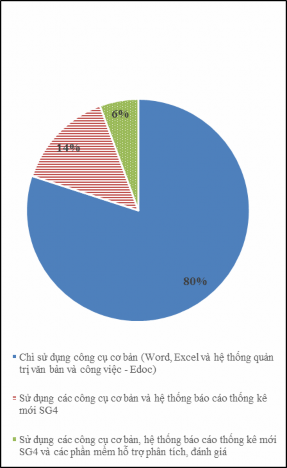

The application of software to support the professional work of the staff of the State Treasury is still very limited: 80% of opinions said that they are currently only using basic tools (Word, Excel and Edoc electronic document system), 14% of opinions said that they are using the new SG4 statistical reporting system and basic tools, only 6% of opinions said that they are using software to support analysis and evaluation.

At the same time, the application of automatic data synthesis reporting system in banking inspection and supervision activities is also not high. This shows that only 20% of the surveyed officers use the automatic data synthesis reporting system, while 25% of the surveyed officers do not use it and 55% of the surveyed officers answered that there is no automatic data synthesis reporting system that can be used.

2.2.1.5. Risk management at credit institutions

As subjects of banking inspection and supervision, in order to implement the risk-based inspection and supervision method, credit institutions must have the ability to manage risks. During the research period, in general, credit institutions were aware of the importance of implementing risk management in general, according to Basel II standards in particular, and took measures to improve management capacity, build systems and document processes and regulations. However, the current implementation still has some limitations such as:

- Regarding risk management structure: in general, banks have now partly applied the 3-line-of-defense model, however, there are still some limitations in the coordination mechanism such as the lack of regular exchange between the 1st line of defense and the 2nd line of defense, the reporting of risks between the lines of defense is slow or incomplete. In addition, at some banks, the 2nd line of defense is currently only specialized in compliance inspection and control, without paying attention to building frameworks, policies, procedures and risk management tools as directed by Basel.

- Regarding risk management tools/methodologies: many banks have assessed the current situation, identified gaps as well as a roadmap for building risk management tools and methodologies according to common practices. However, the implementation has not been consistent, mainly focusing on building tools for credit risk management and capital calculation (credit rating system, etc.), while many important areas of other risk components have not been given priority. This limitation partly stems from banks' awareness (For example, bad debt does not only come from credit risk, but the nature of most bad debt can come from operational risks in credit activities).

- Regarding technology and data systems: although there has been a certain investment, current risk management activities of Vietnamese banks are still quite manual without a support system, or if there is investment in the system, most of it arises from

compliance needs (For example, investing in the construction and implementation of anti-money laundering (AML) systems or implementing risk-weighted asset (RWA) calculations). Some top banks with better resources and personnel have initially upgraded their systems and more advanced risk management models to serve proactive risk management such as early warning systems for credit risks (EWS), loan origination systems (LOS), credit rating systems, loss data collection systems for operational risks... However, most banks have major problems with the availability, completeness and quality of data to serve the construction of the above tools and systems. As a result, the implementation results of risk management information technology models or systems are not high and have not been widely applied in operations and decision making.

- Regarding human resources: Human resources with knowledge of implementing risk management in accordance with international practices are still lacking in all three layers of protection.

- Survey results are as follows:

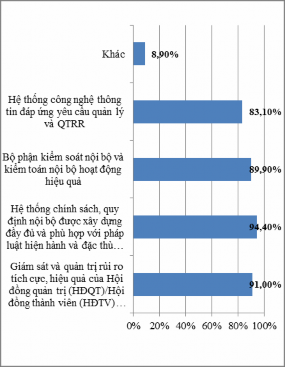

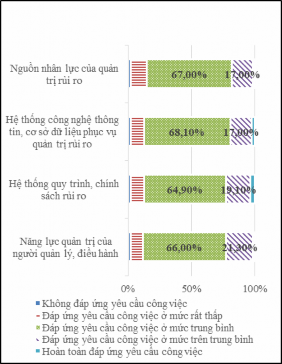

Chart 2.20: Assessment of current risk management of Vietnamese credit institutions

| |

Source: Survey results |

Regarding risk management activities at credit institutions, the survey results show:

- Most opinions believe that an effective risk management system must include the following criteria:

(1) The system of internal policies and regulations is fully developed and in accordance with current laws and the characteristics of the credit institution (rate 94.4%).

(2) Active and effective risk monitoring and management by the Board of Directors (BOD)/Board of Members (BOD) and Executive Board (rate 91.0%).

(3) Internal control and internal audit departments operate effectively (rate 89.9%).

(4) Information technology system meets management and risk management requirements (rate 83.1%).

- Most survey opinions agree that the current risk management work of credit institutions in Vietnam meets the job requirements at an average level. In which the level of meeting the job requirements of each criterion is in the following order:

+ Management capacity of managers and executives: 66% of opinions said that the response was average and 21.30% of opinions said that the response was above average.

+ Risk policy and process system: 64.90% of opinions said the response was average and 19.10% of opinions said the response was above average.

+ Information technology system, database serving risk management: 68.10% of opinions said the response was at an average level and 17% of opinions said the response was above average.

+ Information technology system, database serving risk management: has the lowest level of job response (67% response is at average level and 17% response is at above average level).

The survey results show that all credit institutions have recognized the basic elements to establish an effective risk management system and have paid attention to this work in the process of managing and operating their business activities. However, the level of meeting the requirements of risk management work is not really high.

2.2.2. Current status of risk-based inspection and supervision by the State Bank of Vietnam towards credit institutions

2.2.2.1 Risk-based inspection and supervision method

a) Risk-based inspection method

Currently, inspection work in Vietnam is carried out using two methods: compliance inspection method and risk-based inspection method. In which, for domestic credit institutions, the State Bank's inspection mainly applies the compliance inspection method and begins to apply some contents of risk-based inspection (applied in part and according to each inspection object). For foreign credit institutions, the State Bank has converted the compliance inspection method to the compliance inspection method combined with risk assessment (can be called the risk-based inspection method).

- When conducting risk-based inspections, the methods applied are: (i) Studying the system of processes, management policies and professional guidelines, policy issuance and implementation, management capacity of managers and operators; Assessing whether the risk management system is suitable for the scale and complexity of business operations, business model, and scale of operations; Ability to adapt to changes in policies and markets; Assessing the effectiveness and efficiency of the internal control system, internal audit, and management information system; (ii) Requesting the inspected credit institution to report on its self-assessment and provide documents related to the content of the inspection; (iii) Select samples for inspection, focusing on large transactions, large outstanding debts or at sensitive times, borrowers with loss-making business activities, transactions with signs of abnormality but must ensure diversity (by industry, by customer; by product; by type/form of transaction...), focusing on detecting systemic risk issues, how to handle and limit risks; (iv) Interview/dialogue with senior management personnel/Heads of departments to exploit information about the current status of the management structure - working environment; survey/work with each Department/Office - where inspectors conduct on-site inspections; Use questionnaires, internal control questions,...; (v) Evaluate and perceive the inspection subjects from a comprehensive, multi-dimensional perspective; combine the actual inspection of sample files with the study of internal policies and regulations of credit institutions; (vi) Based on legal documents; Referring to the Inspection Handbook, the State Bank uses the Basel Committee's banking supervision and risk management practices in assessing the risk management of credit institutions. From there, the State Bank has made recommendations to strengthen risk management at credit institutions...

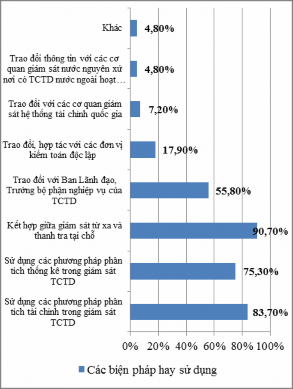

- Survey results are as follows:

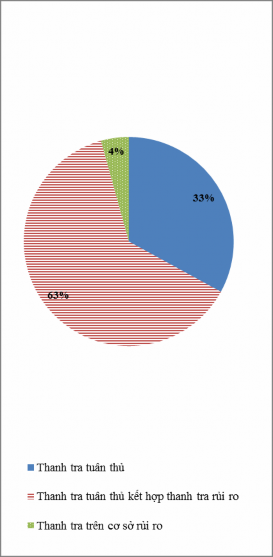

Figure 2.22: Risk-based inspection methods in use

Source: Survey results |

According to the survey results, 63% of opinions stated that the inspection method currently used is compliance inspection combined with risk inspection (mainly opinions of officers working in foreign credit institution inspection); 33% of opinions stated that compliance inspection method is being applied (mainly opinions of officers working in domestic credit institution inspection); 4% of opinions stated that risk-based inspection method is being applied.

The above results reflect the fact that currently the risk-based inspection method is only applied to foreign credit institutions, while domestic credit institutions mainly still implement the method of inspecting compliance with legal regulations.

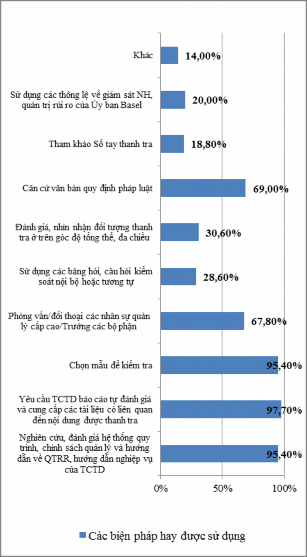

More than 90% of surveyed inspectors and supervisors responded that they often use the three most basic methods when conducting inspections:

- Research and evaluate the system of procedures, management policies and guidelines on risk management and professional guidance of credit institutions.

- Require credit institutions to report self-assessment and provide documents related to the inspected content.

- Select sample to test.

In addition, more than 60% of surveyed staff used the following measures:

- Interview/dialogue with senior management/Department heads.

- Based on legal documents.

b) Risk-based monitoring method

As of November 2017, the State Bank of Vietnam (SBV) has been monitoring the credit institution system at two levels: Macro-supervision and Micro-supervision for each group of credit institutions periodically (monthly, quarterly, annually). Macro-safety monitoring activities at this stage are still at a rudimentary level, mainly based on financial safety indicators and macroeconomic indicators, market parameters, quantitative information as well as various qualitative analysis methods to assess systemic and comprehensive risks for the risk status of credit institutions, control the financial situation to identify and detect potential or existing problems of the credit institution system. Micro-supervision activities for each credit institution are still mainly based on the compliance monitoring method and combined with the risk-based monitoring method based on the analysis of quarterly and annual financial statements submitted by credit institutions. Based on the reports of credit institutions, supervisors will synthesize and analyze the operational situation as well as unusual developments in operations to provide early warnings and provide a basis for the inspectors' assessments and proposed solutions for each credit institution.

From December 1, 2017 onwards, in terms of law, risk-based supervision has made great strides with the introduction of Circular 08 and the Banking Supervision Handbook coming into effect. Accordingly, in addition to compliance supervision, legal regulations on limits, ratios

In addition to ensuring the safety of banking operations, regulations on statistical reporting regimes, and other regulations of the law on currency and banking, the State Bank also conducts risk-based supervision through analyzing and evaluating the types of risks of credit institutions along with assessing the operational situation, management capacity, management, derivatives, financial forecasting, and credit ratings of credit institutions. In addition to the content of micro-safety supervision, there is also the rating of credit institutions according to the CAMELS rating and assessment system, with the rating results according to 05 levels: A, B, C, D, E (good, fair, average, weak, poor).

The results of credit institution inspections are one of the main bases for conducting supervision. In addition, supervision information is obtained through the analysis of financial indicators from credit institution reports, through statistical methods and other information access methods such as: information exchange with the State Securities Commission, with independent auditors...

The survey results are as follows:

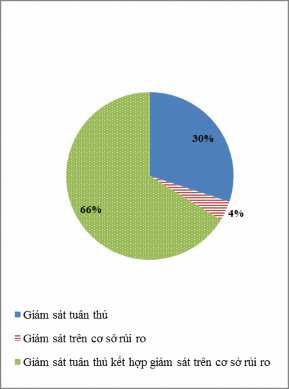

Figure 2.24: Monitoring methods currently in use

| |

Source: Survey results |