2.2. Current status of credit risk management at Vietnam Bank for Agriculture and Rural Development

2.2.1. Credit risk management model

In recent years, Agribank's RRTD management model has been constantly innovated according to the requirements of sustainable, safe operations and integration with the region as well as the world. The responsibilities between the Head Office and branches/affiliated units are clearly defined. Currently, Agribank's Credit Department (including the Enterprise Credit Department and the Household Credit Department) is responsible for developing general management policies and rules for credit management throughout the system, credit departments (at the Operations Center and branches) based on those policies and rules directly carry out credit transactions, manage and control RRTD.

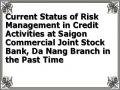

BRANCHES TYPE 1, 2

CENTER

OPERATION

Figure 2.3. Credit risk management model at Agribank

CREDIT COMMITTEES

INTERNAL CONTROL INSPECTION COMMITTEE | Prevention and Control Center | ||

Maybe you are interested!

-

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch -

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank -

Current Status of Risk Management in Credit Activities at Saigon Commercial Joint Stock Bank, Da Nang Branch in the Past Time

Current Status of Risk Management in Credit Activities at Saigon Commercial Joint Stock Bank, Da Nang Branch in the Past Time -

Current Status of Risk Management of Vietnamese Banks Chapter 3: Perfecting Credit Risk Management of Vietnamese Banks

Current Status of Risk Management of Vietnamese Banks Chapter 3: Perfecting Credit Risk Management of Vietnamese Banks -

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1

Source: Agribank, 2000-2014

At each type 1 and 2 branch, there is an internal control inspection department that implements work programs under the direct professional direction of the Internal Control Inspection Department at the Head Office. The internal control inspection department at the branch has the function of inspecting and controlling compliance with credit procedures, preventing and warning of risks. The Internal Control Inspection Department develops credit control procedures, develops work programs, and inspection plans according to the requirements of each period, ensuring that risks are limited and prevented at an acceptable level.

The Risk Prevention and Handling Center is a center that processes and provides customer information to serve the work of preventing credit risks, monitoring debt classification, debt handling and debt collection at branches.

Currently, the risk management organization model at Agribank is built with three levels:

Level 1 (First line of defense) - At the Branch: Self-responsible for risk management, including the front block (credit department) and the back block (credit appraisal department and internal inspection and audit department performing risk inspection and control). In addition, there is a specialized XLRR department.

Floor 2 (Second line of defense) - Units performing risk management at the Head Office include: Risk Management Committee; Risk Prevention and Handling Center (PN&XLRR Center) and Internal Inspection and Control Department.

- The Risk Management Committee has the function of advising the Board of Members on developing a roadmap and plan to implement Agribank's risk management activities, and promulgating policies, regulations and procedures related to risk management in Agribank's business activities.

- The PN&XLRR Center is a unit under the management and operation apparatus at the Head Office, responsible for advising the Board of Directors and General Director in collecting, providing, storing and analyzing risk prevention information; synthesizing and XLRR in the business activities of the entire Agribank system.

- The Internal Control and Inspection Department inspects the implementation of internal regulations on credit granting, loan management, security measures and asset management, risk management policies; inspects the implementation of debt classification, off-balance sheet commitments, provisioning, use of risk management provisions and other internal regulations throughout the Agribank system.

Floor 3 (Third Protection Ring) - Board of Directors' Supervisory Board

- The Board of Supervisors monitors and evaluates the implementation of Agribank's risk management strategies, policies, procedures and limits in accordance with the provisions of law and Agribank.

- The Internal Audit Department (under the Board of Supervisors) conducts independent reviews and assessments of the appropriateness and compliance with internal policies, regulations, legal provisions and the effectiveness of Agribank's risk management system and the effectiveness of the control system.

Through the implementation process, Agribank's risk management model has had many innovations, meeting common standards such as:

Firstly, the bank has initially separated and independent the front-end departments (loan origination department, proprietary trading and portfolio management department, etc.) and the back-end departments (credit appraisal department, payment and control department, etc.).

Second, the risk management organization model from the 2nd floor - Risk Management Unit at Head Office to the 1st floor - Branches, Departments, Transaction Points is synchronized with the internal inspection and control system.

Third, a Control Department has been established under the Board of Directors with the independent function of monitoring and evaluating compliance with risk management policies and procedures in the bank.

Fourth, the Bank established a Debt Trading Company under the Bank to meet the need to sell bad debts of the Branches to a more professional department. In addition, it also established bad debt handling steering groups at the Head Office with leaders of the Board of Directors and Board of Management as team leaders for the Branches with high bad debts according to the bank restructuring project.

Fifth, there is clear decentralization and authorization through the credit authorization process for each department.

(Source: Agribank, 2000-2014).

2.2.2. Credit risk management policy and process system of Vietnam Bank for Agriculture and Rural Development

2.2.2.1. Internal credit rating and scoring system (RMS)

a. Scoring object

Agribank has piloted customer scoring and ranking since 2007 and officially applied it in 2011, as shown in Document No. 197/QD-NHNo-XLRR dated August 20, 2012 of Agribank on Issuing guidelines for using and operating customer scoring and ranking throughout the Agribank system. The internal ranking system is considered a support tool for Agribank in credit activities, customer policies and risk management policies from a system-wide perspective. The steps for implementing customer scoring will be presented in turn as follows:

Agribank's internal credit rating system is built to apply to the following scoring subjects: Enterprises; individuals; farming households; households

business; bank; securities company; finance company/financial leasing company.

Figure 2.4. Scoring process for corporate customers

Choose a business line

Set of indicators to determine the size of the Enterprise

Non-financial indicators

main

Talent Point

main

Phi point

finance

Business Type

Client

Financial report

Financial indicators

Total score and ranking (10 ranks)

Source: Agribank, 2000-2014

b. Scoring principles for all customers

In the credit scoring process, there will be an initial score and a combined score to rank customers. The initial score is the score of each credit scoring criterion that the credit officer determines after analyzing that criterion. The combined score to rank customers is the initial score multiplied by the weight. The weight is the level of importance of each credit scoring criterion (financial indicator or non-financial factor) in terms of its impact on RRTD.

Normally, a financial or non-financial indicator will have 5 standard value ranges corresponding to 5 score levels: 20, 40, 60, 80, 100 (initial score). Thus, for each indicator, the customer's initial score is one of the 5 levels above, depending on which of the 5 standard value ranges the customer actually achieves.

The overall score for customer ranking will be the product of the initial score multiplied by the weight, taking into account the influencing factors: Type of ownership and

Whether the client's financial statements (quarterly, annually) are audited or not.

Some other contents regulating Agribank's internal credit scoring and rating, see Appendix 09.

Through the customer credit scoring and rating system (RMS), customer information is updated regularly, accurately and promptly, thus ensuring customer ratings. This tool also contributes to improving the ability to analyze and evaluate customer capacity of leaders and credit officers. Most branches have performed customer scoring and rating, meeting the basic requirements of the debt classification policy issued in Decision 493. However, after a period of operation, the customer scoring system has revealed shortcomings such as: Because the scoring results are only updated at the end of the quarter, some important information has not been recorded regularly, leading to the rating results not reflecting the corresponding risks in a timely manner; the internal rating system has only been built for single ratings, and has not designed early warning signs and appropriate decentralization policies; The current software is built to allow credit officers to understand the operating mechanism of the internal rating system, so credit officers have the conditions to edit customer information according to their subjective opinions, leading to customers' scores and ratings not being accurately reflected.

c. Customer scoring and ranking in credit risk management

By the end of 2014, Agribank had basically completed customer scoring in accordance with the regulations of the State Bank of Vietnam and basically approached international practices.

Due to the characteristics of individual customers, the new system will score and rank individual customers with outstanding debt of 500 million VND or more and businesses.

In the immediate future, the enterprise ranking is only for risk management purposes and to support the credit decision-making process, which is reflected in the credit officer's appraisal report and customer information storage. After a period of stable implementation, Agribank will develop specific policies for each customer group. Based on the actual implementation results report of the lending units, the Head Office will be responsible for evaluating, drawing experience and adjusting the process to ensure compliance with reality and moving towards the technology of the scoring program to automate.

The decision-making process and the delegation of judgment levels to branches. Specifically, the process at Agribank's type 1 and type 2 branches is as follows: Credit officers directly score credit and rank customers; Head and deputy head of credit department are responsible for controlling and approving the scoring and ranking of credit officers.

- Purpose of credit scoring and customer rating:

+ Credit scoring and customer ranking are carried out to support in making credit decisions, including determining: credit limit, term, interest rate, loan security measures, approval or disapproval (?); monitoring and evaluating credit customers when the credit has outstanding debt; customer ranking allows Agribank to anticipate signs that the loan quality is deteriorating and take timely countermeasures.

+ From the perspective of managing the entire credit portfolio, the credit scoring and customer rating system also aims to: Develop marketing strategies to target customers with lower risks; estimate the amount of capital that has been lent that will not be recovered to set up provisions for credit losses.

- Credit scoring principles: During the credit scoring process, credit officers will collect initial scores and total scores to rank customers, specifically: Initial score: Is the score of each credit scoring criterion determined by the credit officer after analyzing that criterion. Total score: Is the score to rank customers by multiplying the initial score by the weight. Weight: Is the level of importance of each credit scoring criterion (financial index or non-financial factor) in terms of credit risk impact.

- Customer grouping: Due to the different nature of customers, in order to accurately and scientifically score credit, Agribank divides borrowers into two groups: Group of business customers; group of individual customers (including individuals and households).

- Credit scoring tools:

+ Standard table for evaluating criteria for credit scoring. For each type of customer as classified above, Agribank uses a standard table for evaluating criteria for credit scoring. This table scores each customer's credit based on qualitative standards (non-financial criteria) such as: Capacity and experience of the Board of Directors, position in the market, relationship with customers, with the bank, etc.

+ Standard financial ratios table. Standard financial ratios table is a tool for credit scoring based on some basic financial indicators such as current payment ratio, debt ratio, etc.

- Credit scoring and rating of corporate customers:

Agribank classifies corporate customers into 10 risk levels from low to high: AAA, AA, A, BBB, BB, B, CCC, CC, C, D. The process of credit scoring and ranking corporate customers in risk management at Agribank is carried out in specific steps (see Appendix No. 11).

- Reassessment of customer ratings: Customer ratings must accurately reflect the risk profile of each customer. Therefore, customer ratings are reassessed once a year. In addition, credit officers must reassess customer ratings whenever an event occurs that could affect the customer’s ability to repay, and if necessary, customer ratings must be adjusted promptly.

(Source: Agribank, 2000-2014)

d. Credit risk prevention information

At Agribank, the Risk Prevention and Handling Center is the place to focus on processing and providing information about customers of the entire system. Through specific and close guidance measures such as: Issuing directive documents, reminders for branches that have not done well, on-site inspections, direct guidance for staff at branches, etc. Up to now, the Risk Prevention and Handling Center has collected and updated data of type I and type II branches with the number of updated customer records of about one million customers, the number of credit contracts monitored is more than one million contracts. Branch data has been updated regularly and the quality of collected information has been improved, especially information on credit balances. In addition, to meet the information needs of branches in the credit approval process such as: Information on technology, market, price, etc. In addition, the Risk Prevention and Handling Center has also contacted and worked with relevant ministries, branches, and experts to provide necessary information to branches. In addition, the Center also issues internal newsletters with increasingly high quality to the Board of Directors, Departments at the Head Office and Agribank branches as reference documents for business activities.

2.2.2.2. Credit policies and procedures

Agribank has issued documents related to credit policies from the perspective of each loan. However, these policies are issued sporadically and do not ensure systematicity in documents and regulations.

Agribank's goal is to become a leading credit institution, playing a leading and dominant role in the monetary market in rural areas, identifying: "rural areas are the market, farmers are the lending subjects, farmers and rural residents are the main customers" (Source: Agribank, 2000 - 2014). Therefore, the goal of credit policy for the agricultural sector is to continue to maintain its position and market share in the role of providing credit for investment in agricultural development in accordance with the policies and goals of the Party and the State; expand operations, apply modern information technology, provide convenient services and constantly develop the brand, enhance reputation in the market, quickly adapt in the process of international economic integration.

Pay attention to capital mobilization, identify capital mobilization as the foundation for expanding lending, pay special attention to capital mobilized from the population, especially medium-term and long-term capital. At the same time, take advantage of capital sources for investment trust, meet the development needs of the economy, focus on mobilizing capital in urban areas to transfer capital to lend in the agricultural sector.

Promote investment redirection, prioritize capital allocation for economically efficient projects in order of priority and select customers, namely: Production and business households, small and medium enterprises, taking rural areas as the main areas to serve and develop business. Focus on investment in the direction of economic restructuring. Diversify credit products as well as diversify customer groups to increase income and minimize risks in credit activities.

The branch's capital investment growth aims to meet customers' demand for loans to develop production, create jobs, shift the agricultural economic structure, increase farmers' income, and contribute to the industrialization and modernization of agriculture. At the same time, ensure full and timely collection of principal and interest to ensure the branch's credit business is profitable and develops stably and sustainably.

2.2.2.3. Credit approval policies and procedures

Agribank has met the requirement of considering the customer's ability to repay as a key factor in the credit approval process. According to Decision No.