By the end of 2019, the restructuring process of the banking system in Vietnam had basically achieved the following results:

Firstly , the situation of weak joint stock commercial banks has been basically controlled. The solvency of these banks has been significantly improved, State assets and depositors' rights have been guaranteed, the operational safety of the banking system has been controlled, security, politics and social order and safety have been maintained; mass withdrawals have not occurred beyond control, especially in some weak joint stock commercial banks that had to be restructured. Nine weak joint stock commercial banks identified in 2013 have been handled. By June 2019, the number of domestic joint stock commercial banks had decreased by 07 banks compared to 2017 through mergers and consolidations.

Up to now, all restructuring plans for weak commercial banks, including mergers and consolidations, have been carried out on a voluntary basis and the State Bank has not had to apply compulsory intervention measures in any case as prescribed by law. After the merger, consolidation or restructuring plan was approved by the State Bank, banks have been actively implementing comprehensive restructuring solutions in finance, operations, governance and correcting violations under the supervision of the State Bank. Up to now, the weak banks that have been restructured have had stable and improved operations compared to the time of the restructuring. The operational safety ratios and payment capacity have been improved to basically ensure compliance with the State Bank's regulations; capital mobilization from the population continues to increase quite well, bad debts have been actively handled and recovered; violations in the ownership ratio of major shareholders and violations in credit granting are being remedied and resolutely handled; The administrative system and organization of the apparatus and network have been restructured in an important step.

Second , banks that are not weak and are required to restructure have implemented solutions to restructure and handle bad debts; focusing on consolidating and correcting existing shortcomings and limitations and enhancing financial capacity, management, operations and competitiveness. Some banks are merging and acquiring other credit institutions to increase their scale and competitiveness.

For non-bank credit institutions, the State Bank has directed the development and implementation of restructuring plans. Some non-bank credit institutions are too weak, the restructuring costs are too large compared to the benefits from maintaining operations, the State Bank has reviewed, evaluated and proceeded to dissolve and declare bankruptcy. Non-bank credit institutions operating normally are also restructuring to improve safety, business efficiency and competitiveness.

Regarding the People's Credit Fund (PCF), the Central PCF has completed the transformation of its operating model into a Cooperative Bank to effectively implement the goals of system linkage, financial support and capital regulation within the PCF system, contributing to helping grassroots PCFs operate effectively according to cooperative principles.

Third , the financial capacity of the banking system is gradually improving through increasing charter capital and handling bad debts. By the end of December 2018, the total assets of the credit institution system reached VND 11.06 million billion, up 10.62% compared to 2017, loans to market 1 reached VND 7.02 million billion, up 14.16% compared to 2017, capital mobilization from market 1 reached VND 8.28 million billion, up 12.3% compared to the end of 2017. The total outstanding loans to customers increased along with the interest rate level remaining stable, which has really supported production and business enterprises, promoting economic growth.

Despite many difficulties, credit institutions still strive to improve their financial capacity and increase their charter capital to facilitate expansion of operations and enhance their ability to cope with operational risks. The stability and safety of the credit institution system have been maintained. By the end of December 2018, the average capital safety ratio of the system reached 12.1% (the minimum prescribed level is 9%), the average liquidity reserve ratio reached 17.4%, most credit institutions met the safety ratios and limits prescribed by law. In particular, a number of qualified credit institutions have been granted approval by the State Bank to apply early capital safety standards according to the Basel II standard method.

Bad debt handling activities in the banking system have been carried out resolutely and have achieved certain results: Under the resolute direction of the State Bank of Vietnam, together with bad debt handling solutions, as well as measures to control and prevent new bad debts that have been implemented synchronously, have contributed to improving credit quality and efficiency, while reducing bad debts. By the end of 2018, bad debt in the whole system was about 1.89%.

The target of the gross bad debt ratio (including on-balance sheet bad debt, debt sold to VAMC that has not been resolved and potential bad debt) at 3% by 2020 instead of the previously common bad debt ratio target has helped the management of bad debt at management agencies as well as credit institutions become more substantial; in the management work, the Government, the State Bank and relevant agencies and sectors have issued many directive documents, especially Resolution 42, which has helped credit institutions remove many bottlenecks in handling bad debt, so this work has achieved many encouraging results. By the end of 2018, on-balance sheet bad debt decreased from 2.55% in 2015 to

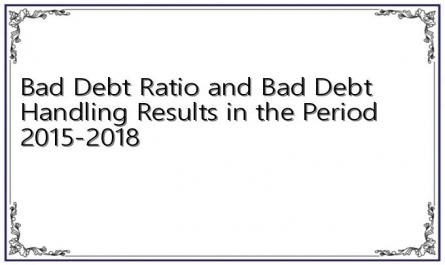

1.89% and the gross bad debt ratio from 10.08% in 2016 to 5.85%. If calculated from 2012 to the end of August 2019, the entire banking system has handled 968.89 trillion VND of bad debt, of which in 2018 alone, the entire system has handled 163.14 trillion VND of bad debt; The ratio of bad debt on the balance sheet, debt sold to VAMC that has not been processed and debt that has the potential to become bad debt of the credit institution system as of the end of August 2019 was 4.84%, a sharp decrease compared to the level of 10.08% at the end of 2016, the level of 7.36% at the end of 2017 and the level of 5.85% at the end of 2018. Regarding the results of bad debt handling according to Resolution 42, accumulated from August 15, 2017 to the end of August 2019, the entire credit institution system has handled 236.8 trillion VND of bad debt determined according to Resolution 42, of which, handling bad debt on the balance sheet reached 137.7 trillion VND. Below is the bad debt ratio and bad debt handling in the period 2015 - 2018:

Table 4.2: Bad debt ratio and bad debt handling results in the period 2015-2018

Target

Unit of measure | 2015 | 2016 | 2017 | 2018 | |

1. Bad debt ratio | |||||

According to the State Bank | % | 2.55 | 2.46 | 2 | 1.89 |

According to the National Steering Committee for Natural Disaster Prevention and Control | % | 2.4 | |||

2. Gross bad debt ratio | |||||

According to the State Bank | % | 10.08 | 7.36 | 5.85 | |

According to the National Steering Committee for Natural Disaster Prevention and Control | % | 8.85 | 11.9 | 9.5 | |

3. Bad debt has been handled | Billion Dong | 95,000 | 70,000 | ||

4. Bad debt at VAMC | Billion Dong | ||||

Cumulative purchase | Billion Dong | 228,416 | 264,755 | 307,932 | 280,000 |

Has been processed | Billion Dong | 20,697 | 30,700 | 100,000 |

Maybe you are interested!

-

On Handling Bad Debt With Market Solutions:

On Handling Bad Debt With Market Solutions: -

Solution Group on Bad Debt Monitoring and Handling Violations of Vietnam's Commercial Banking System

Solution Group on Bad Debt Monitoring and Handling Violations of Vietnam's Commercial Banking System -

Prevention and Handling of Bad Debt at Commercial Banks:

Prevention and Handling of Bad Debt at Commercial Banks: -

Compare Profit Ratio And Bad Debt Credit Xk

Compare Profit Ratio And Bad Debt Credit Xk -

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014

Source: SBV, VAMC, UBGSTCQG

Fourth , perfecting the legal framework on currency and banking, enhancing the role and effectiveness of the State Bank's management, direction and operation in the currency and banking sector to support the restructuring of credit institutions. The State Bank also continues to perfect regulations on handling administrative violations in the currency and banking sector; regulations on safety ratios in banking activities; entrustment, acceptance of entrustment, regulations on risk management of credit institutions.

Fifth , inspection and supervision work has been strengthened, playing an important role in improving the efficiency and effectiveness of state management in the monetary and banking sector and effectively supporting the implementation of the Project on restructuring credit institutions, especially in terms of organizational structure and operations. The results of inspection and supervision work have been increasingly innovated in the direction of inspection and supervision of legal entities, combining inspection and supervision of compliance with inspection and supervision based on risks.

In 2018, Brand Finance announced the 500 most valuable banking brands in the world, including 3 Vietnamese banks (VietinBank, BIDV, Vietcombank); credit rating agency Moody's Investors Service upgraded a number of assessments for 14 Vietnamese commercial banks and adjusted the rating of Vietnam's banking system from B1 "positive outlook" to Ba3 "stable outlook". This is a signal showing that state management in the banking sector, restructuring and handling of bad debts in the system of credit institutions in the period 2016-2020 are on the right track, initially achieving positive results, recognized by international rating organizations.

4.2.2.3. Limitations, problems and causes

Despite the above achievements, the implementation of the Credit Institution Restructuring Project and the Bad Debt Settlement Project still has some shortcomings and limitations as follows:

Firstly, Vietnam does not have a real debt trading market as credit institutions still mainly sell debts to VAMC and the Vietnam Debt and Asset Trading Company (DATC) owned by the State. Resolution No. 42/2017/QH14 stipulates that credit institutions are allowed to sell bad debts and related collaterals publicly, transparently, in accordance with the law and at a selling price consistent with the market price, higher or lower than the principal balance of the debt. In reality, debt trading between credit institutions and between investors, especially foreign investors, has not yet taken place.

Currently, the conditions for debt trading services are quite high (minimum charter capital of 100 billion VND for enterprises engaged in debt trading activities and minimum 500 billion VND for enterprises establishing debt trading floors, internal management requirements). In addition, our country does not yet have a secondary capital market and derivatives for debts, so debt buyers have great difficulty when they want to transfer debts. Derivative products such as asset-backed securities are not yet available, leading to a failure to attract investors to buy and sell debts.

Second, credit risks exist when some corporations have had very large loans from the banking system. Although at the time of borrowing, the financial situation and internal factors of these corporations were stable, the unpredictable developments of the world economic situation have a direct impact on the production and business situation of large-scale corporations, thereby increasing risks for the banking system. For example, Vingroup - considered a "chaebol" controlling a large part of the production and distribution system in Vietnam in recent years - has been expanding its operations to many fields such as real estate, retail, automobiles, motorbikes, telephones, aviation, tourism services, entertainment, education, agriculture, fashion, healthcare,

pharmaceuticals... Vingroup's business in risky fields such as automobile manufacturing poses risks to the banking system and the entire economy when the group mobilizes a large amount of capital from banks through the issuance of corporate bonds. As of August 2018, Vingroup's total loans and debts are estimated at over VND30 trillion. In October 2018, credit rating agency Fitch Ratings downgraded Vingroup's outlook from stable to negative because Vingroup borrowed capital to finance the production of VinFast cars and electric motorbikes, increasing the risk of financial leverage.

Third, one of the biggest difficulties is the seizure of secured assets; according to Resolution 42, the right to seize secured assets must be accompanied by the condition that the mortgage file between the customer and the credit institutions must have an agreement on the terms of seizure of secured assets, but in reality, up to the time Resolution 42 takes effect, most mortgage contracts do not have this clause, so in order to implement it, credit institutions must negotiate with borrowers to sign an addendum to the contract to adjust it, however, for bad debts that have arisen, convincing customers to repay the loan is difficult, convincing customers to sign an addendum to the contract is even more difficult.

Also according to Resolution 42, the regulations on the responsibilities of the police and local authorities at all levels in the process of asset seizure are very general, so there are still many difficulties in coordinating debt settlement; The time to resolve cases is often prolonged, and the implementation of court decisions is slow due to different interpretations; for mortgaged assets such as ships, especially ships operating in international waters or cars, credit institutions cannot determine the location of the mortgaged assets to keep and recover debt settlement, and there are no documents guiding coordination with domestic and foreign authorities in keeping mortgaged assets in specific cases as above to recover debt; Valuation for sale of debts is not unified, one of the difficulties in bad debt cases is that determining the value of debt according to market price as a basis for buying and selling debt is still facing many difficulties when the valuation of debt is carried out by valuation organizations but there is no unified standard, there are many differences in valuation methods, as well as valuation criteria, there are also differences between valuation organizations, leading to the debt seller not daring to decide due to concerns that the selling price offered is subjective and may be lower than the value of the debt, and the buyer also has difficulty choosing the market price as a reference for the debt purchase transaction. In some cases, the property is a house of gratitude, charity or the collateral is the property of a third party guaranteeing the loan for individuals and businesses, the collateral is social housing, in

The money to buy the property is partly from the property owner, the rest is financed from the social security fund, so when enforcing the judgment, it is very confusing because it affects social security work; The transfer or entrustment of debt management for purchases and sales is still facing many difficulties because there is currently no secondary debt market; similarly, there are currently no derivatives such as asset securitization, regular debt securitization and bad debt, leading to low liquidity of debts, etc.

Fourth , the handling of existing financial and operational weaknesses in a number of credit institutions, especially those belonging to economic groups and state-owned corporations, has not been resolutely implemented. The safety and soundness of the banking system has improved significantly but not uniformly among credit institutions, in which some credit institutions are not really safe and stable. The scale and competitiveness of many credit institutions have not been significantly improved; the management and operational capacity of many credit institutions is still limited, and it will take a long time to fully implement international standards and practices.

Fifth , the cross-ownership issue (along with the bad debt issue) is the two biggest barriers to the restructuring process of the Vietnamese commercial banking system at present. Although 24/45 solutions in Project 254 are directly or indirectly related to handling cross-ownership in the system of credit institutions, cross-ownership is still complicated and poses many risks to each credit institution in particular and the financial system in general. The Vietnamese credit institution system currently has 6 different cross-ownership groups: (i) ownership by domestic and foreign commercial banks in joint-venture banks; (ii) foreign strategic shareholders in domestic commercial banks; (iii) shareholders in banks that are fund management companies; (iv) ownership by state-owned commercial banks in joint-stock commercial banks; (v) mutual ownership between joint-stock commercial banks; (vi) ownership of joint-stock commercial banks by state-owned and private corporations and groups. Therefore, the process of dealing with the negative impacts from this cross-ownership network is more complicated and time-consuming.

Sixth, the complicated developments in the global trade tensions and other risks have not been mentioned as an important factor that should be considered in the restructuring of Vietnam's banking system. The risks from the US-China trade war also affect the goal of stabilizing the currency market and Vietnam's export turnover when China began to devalue the yuan from August 8, 2019. In addition, on May 29, 2019, the US Treasury Department released the Semi-Annual Report on the Macroeconomic and Foreign Exchange Policies of Major US Trading Partners, putting Vietnam on the watch list for currency manipulation (according to the US Treasury Department, currency manipulation is defined as a country intentionally adjusting the exchange rate to affect the balance of payments, or gain an unfair competitive advantage in international trade). The United States has

labeling Japan (1988), Taiwan, China (1988-1992), China (1992-1994) as currency manipulators. When accused of currency manipulation, the United States will intervene by negotiating with other countries to adjust their exchange rate policies, or apply sanctions such as higher tax rates to that country.

Causes of the existence and limitations:

Although there are different opinions on the main causes of the limitations in the restructuring process of the credit institution system in recent years, most policy makers and scholars have agreed on the following main causes:

Firstly , the legal framework and policies supporting the restructuring process of credit institutions are still incomplete, especially lacking important mechanisms such as (i) State intervention and handling of weak credit institutions, leading to untimely and indefinite handling of the legal entities of weak credit institutions; (ii) encouragement of credit institutions in handling bad debts and assets securing loans, mechanisms and policies on tax exemption and reduction related to mergers, consolidations and acquisitions of credit institutions.

Second , in the restructuring process, credit institutions must ensure that they rectify and address existing shortcomings and weaknesses while continuing to grow, even supporting the economy to some extent; most of the risks and losses arising in this process must be borne by credit institutions themselves. Therefore, the pressure to achieve credit growth targets and support the economy may affect the progress and results of implementing the proposed restructuring solutions.

Third , the restructuring of state-owned enterprises, especially state-owned corporations and groups, although achieving initial results, is still slow and has not achieved the desired efficiency, especially in divesting investment capital in credit institutions and handling bad debts with credit institutions. Some state-owned enterprises that own credit institutions do not even have enough financial capacity to handle financial losses and restructure credit institutions, causing the handling of credit institutions belonging to these enterprises to take place slower than planned.

Fourth , the centralized bad debt handling agency (VAMC) is still operating with limited financial capacity, human resources and operational infrastructure, an inappropriate financial mechanism, especially the lack of a debt trading market to implement debt trading according to market mechanisms and handle purchased bad debts.

Fifth , some stakeholders have not been proactive and active in implementing solutions for restructuring and handling bad debts within their assigned responsibilities.

4.3. RECOMMENDED SOLUTIONS FOR REFORMING THE BANKING SYSTEM IN VIETNAM FROM THE PERSPECTIVE OF EXPERIENCE IN REFORMING THE BANKING SYSTEM IN JAPAN

From the perspective of theory and experience in reforming the Japanese banking system from 1990 to 2005, it can be seen that the process of reforming the banking system and handling bad debts in the banking system of Vietnam is still in its early stages and mainly focuses on short-term solutions. In the coming time, Vietnam needs to further accelerate the process of handling current bad debts in the commercial banking system (through perfecting the legal framework and enhancing the capacity of VAMC; developing the debt trading market...) as well as paying more attention to handling systemic causes (through measures to restructure banks, apply modern risk management standards; combine with reforms in other economic sectors...) to prevent new bad debts from forming in the future, ensuring the sustainability of the restructuring process and solutions.

4.3.1. Solutions to improve the capacity to regulate the economy through policy tools

4.3.1.1. For the State Bank

- Build a legal basis to ensure that the State Bank can proactively choose to use tools and solutions, etc. to achieve its operational goals.

- Perfecting the organizational structure and improving the quality of human resources of the State Bank.

- Innovation in organizational management and operation mechanisms: It is necessary to build and gradually apply a new management system to improve the effectiveness and efficiency of the State Bank's operations.

Promote the application of information technology in professional and management work. Complete management information systems, coordination mechanisms, and information sharing.

Perfecting the appropriate decentralization and authorization mechanism to standardize and optimize the decision-making and decision-implementation process and enhance the flexibility of the State Bank.

4.3.1.2. Creating a legal framework for commercial banks to carry out reforms

Based on the experience of applying financial support policies, cost reduction and roadmap for compliance with safety regulations of Japan in the process of reforming the banking system of this country, Vietnam can consider applying:

Firstly, there should be policies and regulations on reasonable tax and fee exemptions and reductions related to the purchase and sale of bad debts and assets securing loans; exemptions and reductions of corporate income tax for a number of years for commercial banks after acquisitions, mergers and consolidations; exemptions and reductions of taxes and fees to encourage commercial banks to actively participate in the development of the banking system.

actively participate in the process of handling "weak" commercial banks, supporting these commercial banks to reduce financial burden in the process of restructuring and handling bad debt.

Second , there is a lending policy, supporting capital with reasonable interest rates in the form of recapitalization for commercial banks participating in restructuring "weak" commercial banks from the money supply of the State Bank to ensure payment capacity and create capital for expanding operations.

Third , allow commercial banks to participate in handling "weak" commercial banks to implement a roadmap for setting up risk provisions according to regulations to support commercial banks in overcoming financial problems as well as supporting commercial banks in restructuring, merging, and consolidating to reduce pressure on time for handling losses.

Fourth , allowing commercial banks to participate in handling "weak" commercial banks (through mergers and consolidations) is maintained and there is a roadmap to handle some violations arising from mergers, consolidations, and restructuring such as ownership of shares, credit granting, etc. exceeding the limit, not fully meeting the operational safety ratios.

4.3.2. Solutions to improve the banking system's response capacity when a crisis occurs

4.3.2.1. Inspection and supervision of weak commercial banks

Japan's experience shows that strengthening inspection and supervision of weak commercial banks is an important condition in preventing crises and the risk of crisis spreading leading to systemic collapse. Applied to the current situation in Vietnam, to enhance the effectiveness and efficiency of inspection and supervision, it is necessary to note:

Firstly, build and publicize a system of inspection and supervision indicators. This system of indicators needs to be public and transparent to commercial banks so that banks can self-evaluate the efficiency and safety of their operations from the perspective of the State Bank. This system of indicators must be consistent with international practices and risk-based supervision, because currently, periodic inspections based on the principle of compliance inspection do not fully reflect the risks that commercial banks may encounter and this new approach helps identify, measure, and control the types and levels of risks that banks may encounter.

Second, strengthen the information coordination mechanism between the Inspection and Supervision Agency with commercial banks, the Banking Information Technology Department and the Credit Information Center. The SBV Inspectorate will directly exploit information and receive reports from the Head Offices of State-owned commercial banks, joint-stock commercial banks, foreign banks, joint-venture banks, finance companies, financial leasing companies, etc. with the support of the Banking Information Technology Department and the Credit Information Center (CIC). Accordingly,

The provincial and municipal branches of the State Bank only receive information from grassroots credit funds and exploit other unified information from the CIC, to ensure accuracy and timeliness for monitoring work, while also ensuring consistency in statistical data for the entire industry as well as for each credit institution.

Third , perfect the mechanism of remote monitoring and post-restructuring monitoring. Accordingly, the remote monitoring unit has the capacity to perform well the following functions: (i) receive data on banks' financial statements and confirm their validity; (ii) assess the general situation of the banking system and propose scenarios of financial changes observed at each bank; (iii) detect banks that will have problems in early warning reports; (iv) provide data and calculate the situation of banks for rating assessment reports; (v) design and monitor inspection activities and take timely remedial measures for each bank after inspection.

Fourth , in the long term, there needs to be a roadmap to build a unified financial supervision model. To limit the weaknesses of the commercial banking system in particular and promote the role of effective supervision in the development of the financial market in general, Vietnam needs to build a system of solutions including both short-term and long-term solutions to ensure the safe and sustainable development of the financial market through the construction of an effective national financial supervision system.

4.3.2.2. Enhancing the role of deposit insurance agencies

Experience from Japan and many other countries shows that it is necessary to enhance the role of the deposit insurance agency (DIA) in dealing with weak commercial banks. Applied in the case of Vietnam, the DIA needs to move towards a payment model with expanded authority and reduced risks. Specifically as follows:

Firstly , adjusting the deposit insurance payment limit in accordance with international practices and helping to maintain depositors' confidence, thereby contributing to maintaining the stability of the financial system. Specifically, there needs to be a mechanism to flexibly adjust the deposit insurance limit corresponding to the state of the banking and financial system, increasing the deposit insurance payment limit during the crisis period and returning it to normal when the system stabilizes again. In particular, there needs to be an unlimited insurance mechanism that also needs to be considered in the event of a financial crisis.

Second, innovate the deposit insurance premium system according to the risk level. It is necessary to quickly research and complete the deposit insurance premium framework according to the risk level to create motivation for credit institutions to operate more safely, ensuring the stability and sustainability of the entire system (the ranking of credit institutions must be conducted periodically so that the Vietnam Deposit Insurance has a basis to apply the premium rate to the participating institutions). In the event of a banking crisis, there must be a mechanism to allow the institution to

The deposit insurance organization should raise the deposit insurance premium rate to an appropriate level. The experience of Japan, Korea, and Taiwan has allowed their deposit insurance organizations to collect additional special fees when a systemic crisis occurs. However, if this rate is low, it will not meet the capital needs of the deposit insurance organization, but if the rate is too high, it will also reduce profits, making it more difficult for credit institutions to operate.

Third , it is necessary to institutionalize the coordination between the Vietnam Deposit Insurance Corporation with the State Bank, the Ministry of Finance, the State Audit and relevant agencies to effectively develop and implement a risk-based insurance premium system; especially in developing regulations and rules for rating credit institutions, and in the process of preventing and handling the failure of credit institutions.

Fourth , it is necessary to develop an information sharing mechanism for the Deposit Insurance. The Law on Deposit Insurance stipulates that the Deposit Insurance organization “synthesizes, analyzes and processes information on organizations participating in deposit insurance in order to detect and recommend the State Bank of Vietnam to promptly handle violations of regulations on safety of banking operations and risks causing insecurity in the banking system” – to carry out this task, the Deposit Insurance needs to have timely, accurate and complete information sources on organizations participating in the Deposit Insurance. Therefore, the information sharing mechanism between the Deposit Insurance, the State Bank, relevant agencies, domestic and foreign information providers, and organizations participating in the Deposit Insurance needs to be completed (especially sensitive information such as credit institutions having problems that need to be restructured).

Fifth , it is necessary to develop a mechanism for the Deposit Insurance to participate in handling the failure of credit institutions for the Deposit Insurance. In order for the Deposit Insurance of Vietnam to be more proactive in managing and liquidating the assets of organizations participating in deposit insurance, there should be regulations guiding the authority of the Deposit Insurance to handle the failure of each group of credit institutions. For example, for small-scale failed credit institutions, the Deposit Insurance of Vietnam has full authority to handle. For larger credit institutions, the Deposit Insurance needs to have a mechanism to actively participate in the process of handling this failure.

Sixth , build a mechanism to expand the investment field for the deposit insurance. In addition to the current purchase of government bonds, when the target fund is achieved, the deposit insurance can consider other investment channels to increase capital while still ensuring system safety. When there is a regulation on credit rating of credit institutions, the deposit insurance can invest in credit institutions with qualified credit ratings (thus in the investment structure, the main weight is still government bonds, and the investment ratio in other high-safety channels will be decided by the deposit insurance of Vietnam).

Seventh , build a mechanism for the deposit insurance to mobilize capital to cover the deposit insurance fund deficit in case of crisis. It is necessary to soon have regulations in specific conditions on the maximum time for reviewing applications for financial support from the deposit insurance organization to meet the urgent capital needs of the deposit insurance organization, especially in cases where:

In case of sudden withdrawal of deposits causing a risk of banking system crisis, it is possible to consider granting the deposit insurance organization a reserve credit limit proportional to the total amount of insured deposits (this reserve credit limit needs to be studied to ensure that the deposit insurance fund can cope well with the phenomenon of mass withdrawals at many credit institutions at the same time). In addition, there should be a mechanism for the deposit insurance organization to issue bonds to compensate for the deposit insurance fund deficit during the crisis period (the main source of payment is the deposit insurance premium paid by the participating deposit insurance organizations later) and a mechanism allowing the deposit insurance organization to request the participating deposit insurance organizations to pay premiums in advance during the period of systemic crisis and the deposit insurance fund is in deficit (this is the solution applied by the FDIC (USA) at the end of 2009 to compensate for the deposit insurance fund deficit).

Eighth , determine the target deposit insurance fund (the ratio of the deposit insurance fund capital calculated on the insured deposit balance that needs to be achieved to ensure that the deposit insurance organization can fulfill its payment responsibility). It is necessary to clearly define the target deposit insurance fund of Vietnam in order to implement the best international practices on deposit insurance and ensure that the deposit insurance fund is large enough to effectively implement business activities. However, the appropriate ratio of the deposit insurance fund calculated on the insured deposit balance needs to be carefully studied to ensure that the deposit insurance organization has enough resources to handle the situation well in case of bank failure (the target deposit insurance fund is often determined in the Law regulating deposit insurance activities of countries with developed deposit insurance systems such as the US, Canada, Taiwan, Indonesia, Philippines, etc.; the ratio of the deposit insurance fund calculated on the insured deposit balance fluctuates between countries and ranges from 0.25% to 5%.).

4.3.2.3. Establishing a solid financial infrastructure

Financial infrastructure includes: Standards, rules, regulations on accounting, auditing, corporate governance; payment systems; legal framework for regulating and supervising financial market activities in particular,... aiming to support the financial system to fulfill its role as a financial intermediary, ensuring the speed and cost of capital circulation, the ability to transmit and disperse financial risks. A strong financial infrastructure is clearly an important premise to ensure that financial institutions (most importantly commercial banks) operate well and financial markets (including the money market) operate smoothly. Thanks to that, financial and banking regulatory and supervisory agencies have the necessary operating environment to fully promote their roles. On the contrary, without a solid financial infrastructure, financial and banking regulatory and supervisory agencies, despite their efforts, may still fail in carrying out their missions. No one else but the Government and related advisory agencies such as state-owned enterprises, the Ministry of Finance, ... must take responsibility.