into total revenue is much larger than the general proportion such as VIB 21%, Sacombank 20%, MB 16%, Techcombank 15% [27]

2.2 Current status of credit quality at Vietnamese joint stock commercial banks

2.2.1 Current status of credit quality of Vietnam's sectors through assessment criteria

Joint stock commercial bank

2.2.1.1 Group of indicators on credit scale and growth

a. Outstanding credit balance of Nam

and growth

credit balance

at some Vietnamese commercial banks

Total outstanding credit is an indicator reflecting the amount of money banks have.

Vietnam Joint Stock Commercial Bank for Industry and Trade provides to the economy at a time. Total outstanding debt includes short-term, medium-term and long-term loans. Low total outstanding debt shows that the bank's credit activities are weak and it is unable to expand its customer base.

goods, ability

marketing ability

poor bank, level

staff

worker

low… However, if this indicator is high, it does not necessarily mean that the loan quality is good, and bad debt is likely to occur. However, if the total outstanding debt increases continuously over the years, it shows an upward trend in credit quality. Specifically, the outstanding credit balance of some Vietnamese commercial banks is shown in the figure below:

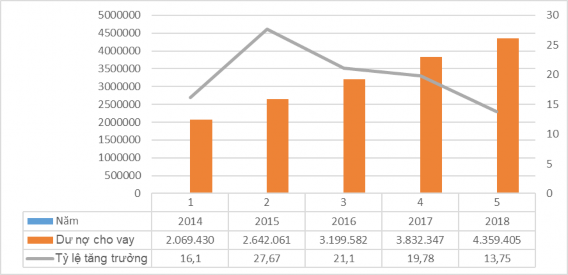

Table 2.5: Outstanding credit balance of 15 Vietnamese commercial banks from 2014-2018

Unit: billion VND

STT

Bank | 2014 | 2015 | 2016 | 2017 | 2018 | |

1 | ACB | 116,324 | 134,032 | 163,401 | 198,462 | 230,527 |

2 | BIDV | 445,693 | 598,434 | 723,697 | 866,885 | 988,739 |

3 | Eximbank | 87,146 | 84,759 | 86,891 | 101,324 | 104,242 |

4 | HDBank | 41,900 | 56,558 | 82,224 | 104,497 | 123,132 |

5 | LienVietPostbank | 51,667 | 64,784 | 84,908 | 100,621 | 119,193 |

6 | Maritime Bank | 22,967 | 27,491 | 34,667 | 35,784 | 48,762 |

7 | MBBank | 100,569 | 121,349 | 150,738 | 184,188 | 159,942 |

8 | Sacombank | 124,576 | 180,593 | 193,098 | 222,947 | 256,623 |

9 | SHB | 104,096 | 131,428 | 162,376 | 196.131 | 216,989 |

10 | Techcombank | 94,894 | 124,032 | 142,616 | 160,849 | 217,138 |

11 | TienPhongbank | 19,839 | 28,240 | 47,325 | 64,007 | 78,458 |

12 | VIB | 18,179 | 47,777 | 60,180 | 79,864 | 96,139 |

13 | Vietcombank | 323,332 | 387,700 | 460,800 | 543,434 | 632,633 |

14 | Vietinbank | 439,869 | 538,080 | 661,988 | 790,688 | 864,926 |

Maybe you are interested!

-

Survey on the Current Status of Improvement in Service Quality Management for Credit Institutions for Managers at Shb Hoan Kiem.

Survey on the Current Status of Improvement in Service Quality Management for Credit Institutions for Managers at Shb Hoan Kiem. -

Current status of short-term lending activities and some solutions to improve the quality of short-term credit services at Vietnam Joint Stock Commercial Bank for Industry and Trade Vietinbank - Branch 12 - 1

Current status of short-term lending activities and some solutions to improve the quality of short-term credit services at Vietnam Joint Stock Commercial Bank for Industry and Trade Vietinbank - Branch 12 - 1 -

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016:

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016: -

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31 -

Current Status of Risk Management of Vietnamese Banks Chapter 3: Perfecting Credit Risk Management of Vietnamese Banks

Current Status of Risk Management of Vietnamese Banks Chapter 3: Perfecting Credit Risk Management of Vietnamese Banks

15 | VPBank | 78,379 | 116,804 | 144,673 | 182,666 | 221,962 |

Total | 2,069.43 0 | 2,642.06 1 | 3,199.58 2 | 3,832.34 7 | 4,359,405 | |

Growth rate | 16.10 | 27.67 | 21.10 | 19.78 | 13.75 | |

(Source: [27])

From 2014 to 2018, outstanding loans of commercial banks increased annually, higher than the average growth rate of credit growth of the entire banking system, the highest in 2015, increasing by 27.67% compared to 2014. Part of the reason came from the merger of banks in the period 2014 - 2015. In 2018, customer loan growth was the lowest in the past 5 years at 13.75% due to the State Bank implementing a tight monetary policy, limiting credit growth.

Unit: billion VND, %

Figure 2.8: Outstanding credit balance of 15 Vietnamese commercial banks from 2014-2018

(Source: [27])

b. Credit growth rate of Vietnam's commercial banking system

0.2

0.18

0.16

0.14

0.12

0.1

0.08

0.06

0.04

0.02

0

18.71%

The average credit growth rate of Vietnamese Joint Stock Commercial Banks from Financial Reports over the years is shown in the figure below:

17, | 29% | 18, | 17% | |||||||

14, | 16% | 14, | 00% | |||||||

1 | 2 | 3 | 4 | 5 | ||||||

Year | 2014 | 2015 | 2016 | 2017 | 2018 | |||||

Growth rate | 14.16% | 17.29% | 18.71% | 18.17% | 14.00% | |||||

Figure 2.9: Credit growth rate of Vietnamese joint stock commercial banks

Male

20142018

(Source:[29])

Credit growth rate increased sharply in the period 2015-2017. During the year

In 2016, credit increased the most due to the monetary policy implemented by the State Bank.

The government has been operating in a cautious easing direction to support economic growth and control inflation. Credit growth in 2016 reached 18.71% compared to the end of 2015.

In 2018, credit growth of Vietnamese commercial banks increased

about 14% compared to 2017 (18.17%), this is the lowest rate in the 5-year period.

years from 2014 to 2018. The reason for low credit growth is that to simultaneously implement two goals of creating conditions for capital support for the economy and controlling inflation is an issue raised in 2018 for the monetary policy management of the State Bank. Right from the beginning of 2018, the State Bank has developed and implemented measures

credit growth control method according to index

both orientation

2018.

The State Bank of Vietnam has directed commercial banks to focus on strictly controlling the credit growth rate and quality of the entire system. In early August, the State Bank of Vietnam decided not to consider or adjust the credit growth target or "lock the credit room" in the

2018 except for special cases, such as some commercial banks participating in restructuring in 2018 for weak credit institutions. Along with that, conduct inspections of banks with high credit growth rates in the fields of real estate, securities, and consumption, accounting for a large proportion of total outstanding debt.

The impact of growth rate on credit quality of commercial banks is very large. Banks must control credit growth rate in accordance with capital mobilization capacity and credit growth target announced by the State Bank, ensuring safe and effective credit growth, creating favorable conditions for businesses and people to access credit capital, especially for businesses assessed to have transparent and healthy financial situation. Banks control credit growth rate to avoid interest rate races, not push interest rates higher than businesses can bear, reduce risks such as: credit quality decline, bad debt increase.

c. Loan/Asset ratio of Vietnamese commercial banks

Lending is the core business of every bank, however, the level of dependence of each bank on lending is different, shown through the ratio of outstanding customer loans/Assets as shown in the following table:

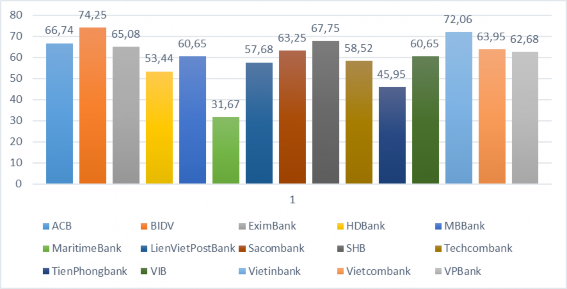

Table 2.6: Customer Loans/Assets Ratio of Vietnamese Joint Stock Commercial Banks from 2014 - 2018

Unit: %

STT

Bank | Year 2014 | Year 2015 | Year 2016 | Year 2017 | Year 2018 | Value medium | |

1 | ACB | 58.87 | 66.4 | 69.27 | 69.17 | 70.00 | 66.74 |

2 | BIDV | 72.15 | 73.91 | 74.34 | 75.55 | 75.3 | 74.25 |

3 | EximBank | 54.17 | 67.58 | 67.47 | 67.83 | 68.35 | 65.08 |

4 | HDBank | 42.98 | 54.23 | 55.86 | 56.36 | 57.79 | 53.44 |

5 | MBBank | 54.79 | 59.45 | 63.59 | 63.44 | 61.98 | 60.65 |

6 | Maritime Bank | 23.2 | 27.74 | 39.06 | 33.23 | 35.1 | 31.67 |

7 | LienVietPostBank | 46.37 | 53.44 | 57.55 | 62.44 | 68.59 | 57.68 |

8 | Sacombank | 67.12 | 64.69 | 60.54 | 60.63 | 63.29 | 63.25 |

9 | SHB | 65.17 | 65.79 | 69.37 | 71.31 | 67.12 | 67.75 |

10 | Techcombank | 48.53 | 61.81 | 64.03 | 64.87 | 53.38 | 58.52 |

11 | TienPhongbank | 39.04 | 37.52 | 44.61 | 51.42 | 57.16 | 45.95 |

12 | VIB | 49.27 | 58.93 | 59.89 | 65.57 | 69.58 | 60.65 |

13 | Vietinbank | 69.06 | 72.76 | 71.14 | 72.71 | 74.64 | 72.06 |

14 | Vietcombank | 63.67 | 65.23 | 66.44 | 59.63 | 64.78 | 63.95 |

15 | VPBank | 52.74 | 61.02 | 64.02 | 66.59 | 69.04 | 62.68 |

(Source: [27]) Unit: %

Figure 2.10: Average Loan/Asset ratio of Vietnamese commercial banks from 2014 to 2018

(Source: [27])

Statistics for the 5-year period (from 2014 to 2018) show that BIDV and VietinBank are the two banks that depend most on annual lending activities. Specifically, on average, BIDV's outstanding loans over the past 5 years accounted for 74.25% of total assets, while VietinBank's figure was 72.06%. These are also the two banks with the largest outstanding loans in 2018, with BIDV having VND 988,739 billion in outstanding loans while VietinBank had VND 864,926 billion. In general, the average loan-to-total-assets ratio of most banks is over 60%. In 2018, Sacombank had this ratio at 63.29%. However, in reality, Sacombank's loan ratio is even larger than the above banks, because there is a large amount of outstanding loans hidden in receivables and accrued interest.

(totaling up to over 46,800 billion VND, accounting for 18% of total assets). In particular,

Vietcombank and Techcombank, the two banks with the largest profits in the system in 2018, are in the group that is less dependent on lending activities. For Vietcombank, the ratio

The average 5-year loan balance to total assets ratio was 63.95%, while Techcombank's was only 58.52%.

The reality is that it is not the least dependent on lending that is

good but not bad

belonging to many is bad and the degree

extra

belong to no

determines bank profits, because there are many other factors such as profits, non-lending income, operating costs, provisioning ratio, etc. With Techcombank, the reason for the low loan balance ratio is because the bank has used most of the credit balance room granted (the State Bank allowed to increase by a maximum of 20% in 2018) to buy corporate bonds, instead of increasing customer loans. By the end of 2018, the amount of corporate bonds that Techcombank held amounted to about 20,000 billion VND [27]. This is the direction

Techcombank's special feature is partly because it wants to retain and cooperate symbiotically with

Big clients are selling bonds, partly because corporate bond profits are typically larger than traditional consumer lending, plus the large profits from bond underwriting.

d. Credit structure over time

Credit balance over time reflects the lending capital of commercial banks.

Okay

head

invest in the foundation

economy at

time

point

identify.

Presently

now residual classification

credit debt

in

Each given moment is expressed in many different criteria.

different such as: by time, by industry, economic sector,.... Determining

Balance sheet at the time to determine scale, investment level and diversity

In bank lending activities, outstanding debt is determined by the loan term.

balance

to

limit

risk management

safe and suitable

with

scale of mobilization

capital

and rules

determine

State Bank, banks have resources

mobilize

medium long term

short

cannot

Take a lot of short-term capital to lend medium and long term. Loan balance structure according to

Time also significantly affects CLTD, if the structure

loan agreement

reason will

promote the following figure:

growth

credit

and minimize

Okay

risk

yes

show

via

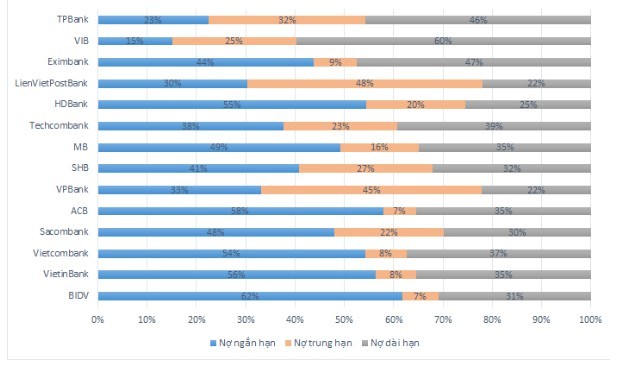

Figure 2.11: Credit structure over time of Vietnamese commercial banks in 2018

(Source: [27])

To ensure stable business operations, commercial banks do not

should practice

too much medium and long term lending,

medium and long term lending

depends on the growth rate of mobilized capital, especially capital

medium and long-term mobilization of customers. In general, at banks, medium and long-term lending is often more attractive than short-term lending, because it brings higher interest rates. However, this also means that the potential risks for the system in the future are greater, leading to a decline in credit quality, because the longer the lending term, the higher the risk of term balance, especially in the condition that the proportion of short-term deposits still accounts for the majority in the structure of mobilized capital in general, the pressure to mobilize is accordingly greater. The more banks focus on short-term debt, the less risk but also have to accept lower profits. The longer the lending term, the higher the profit but also the higher the risk.

Statistics from the Annual Report of Joint Stock Commercial Banks in 2018 show that some banks are choosing a safe direction, namely BIDV with a short-term debt ratio of 62%, VietinBank (56%), Vietcombank (54%), Sacombank (48%), ACB (58%), MB (49%). HDBank also chooses this direction with a fairly high short-term debt ratio of 55%. Meanwhile, SHB and EximBank are somewhat neutral with the ratio of times

Techcombank and VPBank, chose a profit-oriented direction with short-term debt ratios of 38% and 33% respectively. Taking on more risk are LienVietPostBank, TPBank and VIB with 30%, 23% and 15% respectively.

Since 2014, to promote

organizations

credit

growth

outstanding debt,

The State Bank of Vietnam has issued Circular 36/2014/TTNHNN regulating

the worlds

term,

proportion

ensure safety in the operations of credit institutions, thereby loosening the maximum allowable level of short-term capital used for medium and long-term loans.

up to

60% of the

This also helps organizations

credit

push

strong lending

medium and long term to have the level

interest rate

high density

special

is personal loan

and lending to businesses

Micro SMEs,

This is also the trend.

Good

increase

Chief

Okay

effect

loan results if

as bank guarantee

Okay

source

loan capital

stable.

However, to avoid this

invest in medium and long term projects

limit

special

special

are real estate projects

dynamic

product

and avoid repetition

again

risk

risk in period

Previously, the State Bank of Vietnam issued Circular 06/2016/TTNHNN to replace Circular 36 after a period of collecting feedback for the revised draft, according to which the content of Circular 06 has 2 major adjustments; first is the regulation that the risk conversion coefficient of receivables for real estate business is 200% from January 1, 2017 instead of 250% as in the draft, second is the capital usage ratio

Short-term and medium- and long-term loans are reduced according to the roadmap from 60% to 50% from

01/01/2017 and 40% from 01/01/2018. So from the period 2017 2018 banks

must proactively reduce the ratio of short-term capital used for medium and long-term loans

This means that banks need to reduce medium and long-term loans to the prescribed level according to the roadmap.

2.2.1.2 Group of indicators showing profitability from credit activities

a. Net interest margin (NIM)

The indicator to evaluate the profitability of Vietnamese commercial banks is the Net Interest Margin (NIM). Mobilizing capital from customer deposits and lending are the main activities that bring revenue to the bank, however, there are still other activities that bring profit to the bank such as: securities trading, derivatives, foreign exchange, guarantees, etc. Profitable assets are assets that bring profit to the bank such as customer loans, investments, etc.