at the State-level Thesis Evaluation Council, at the National Economics University in 1996.

The above research focuses on analyzing and evaluating the current situation of credit risk limitation of Commercial Banks (CBs) in the early stages of implementing the reform of banking activities, implementing 2 Banking Ordinances, and expanding lending to non-state economic sectors. At this time, state-owned commercial banks account for over 70% of the credit market share of the entire banking industry, so the solutions and current situation mentioned in the thesis are mainly for state-owned commercial banks. The solutions mentioned in the thesis are no longer suitable for credit activities in the current stage.

- Doctoral thesis, with the topic: " Some banking risk issues in the conditions of a market economy" by PhD student: Nguyen Thi Phuong Lan, working at the Banking Academy, defended at the State-level Thesis Evaluation Council, at the National Economics University in 1995.

The thesis uses quantitative research methods, using mathematical models to quantify bank credit risks when the economy has just shifted to a market mechanism, the legal environment, the credit operating environment still has many risks, credit risk management of commercial banks is almost non-existent. The credit risk management of commercial banks according to the provisions of the 2 Banking Ordinances and the State Bank (SBV) still issues specific credit regulations: short-term credit, medium- and long-term credit... for commercial banks to implement and apply, some contents are no longer suitable for the current situation. Credit risk management of commercial banks according to the provisions of the 2 Banking Ordinances.

- Master's thesis: "Credit risk management at Bac A Joint Stock Commercial Bank" Major : Finance - Money circulation and credit; Code: 60.31.12; By student: Chu Van Son, defended at National Economics University, December 2008.

Maybe you are interested!

-

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development -

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch -

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank -

Current Status of Risk Management in Foreign Exchange Trading in the International Market of Vietnamese Commercial Banks

Current Status of Risk Management in Foreign Exchange Trading in the International Market of Vietnamese Commercial Banks -

Current Status of Loan Portfolio Risk Management at Vietnamese Commercial Banks

Current Status of Loan Portfolio Risk Management at Vietnamese Commercial Banks

The thesis focuses on credit risk management of Bac A Joint Stock Commercial Bank, a small-scale joint stock commercial bank headquartered in Vinh city, Nghe An province. Credit activities of Bac A Joint Stock Commercial Bank mainly lend to urban customers and non-state customers, so the current situation and risk management solutions that the author mentions are mainly for this group of customers within a narrow scope.

- Master's thesis in economics with the topic: " Credit risk management at the Bank for Agriculture and Rural Development of Vietnam in Hanoi"; Major : Finance - Money circulation and credit ; by Student: Nguyen Van Chinh, Director of the Bank for Agriculture and Rural Development Hoang Mai branch, defended at the Banking Academy, October 8, 2009.

The thesis studies credit risk management of branches of NHNo&PTNT in Hanoi, data and current situation up to the end of 2008, the scope is narrow both in space and the limits of a master's thesis. The branches in the area operate lending in urban areas, because the project only studies branches of the old Hanoi, not including Ha Tay province before the merger, so it does not mention much about lending to production households, to risks in the field of Agriculture - Rural areas. The scope of credit risk research of the thesis only stops at the management of each branch in the area.

b- Regarding the activities of Vietnam Bank for Agriculture and Rural Development:

- Doctoral thesis, with the topic: " Solutions to improve the operation of Vietnam Bank for Agriculture and Rural Development to serve the Industrialization and Modernization of Agriculture and Rural Areas " by PhD student: Doan Van Thang, defended at the State-level Thesis Evaluation Council, at the National Economics University, on July 14, 2003.

The research project covers quite broadly the business activities of the Vietnam Bank for Agriculture and Rural Development in the restructuring period according to the Government's project after the impact of the regional financial crisis. The thesis only briefly mentions the management

credit risk management, not going into depth in this field and also not being updated in the current stage of international economic integration, the author tends to propose solutions to improve capital mobilization efficiency, lending efficiency and diversify non-credit services for Vietnam Bank for Agriculture and Rural Development.

- Doctoral thesis, with the topic: " Application of modern banking management technology and business activities of the Vietnam Bank for Agriculture and Rural Development in the current period " by PhD student: Au Van Truong, working at the Vietnam Bank for Agriculture and Rural Development, defended at the State-level Thesis Evaluation Council, at the National Economics University, on July 16, 1999.

The thesis focuses on the study of information technology applied in general banking management at the Vietnam Bank for Agriculture and Rural Development. The content was mentioned and researched when the level and technology of banking management in our country were still backward, credit activities were heavily affected by the regional financial crisis and a number of major economic cases, and credit activities for poor households were not separated from the Vietnam Bank for Agriculture and Rural Development. Through the research of the project, it can be seen that the content at that time did not mention credit risk management in accordance with international practices.

- Doctoral thesis, with the topic: "Solutions for developing and perfecting leasing activities at the Bank for Agriculture and Rural Development of Vietnam" by PhD student Nguyen Quoc Trung working at the Bank for Agriculture and Rural Development of Vietnam, defended at the State-level Doctoral Thesis Evaluation Council, at the Banking Academy, in 2004.

The content of the thesis focuses on the development and improvement of leasing activities, which are only implemented by commercial banks or independent companies. The thesis does not mention much about leasing risk management and is specific compared to credit risk management in general, focusing on 2 financial leasing companies of the Vietnam Bank for Agriculture and Rural Development, namely Financial Leasing Company and Commercial Joint Stock Bank.

Leasing Company I (ALC1) and Leasing Company 2 (ALC2). The research time scope is also in the early stages of restructuring the two commercial banking systems according to the Government's project, but in the current conditions of opening the financial market and international economic integration, the reality has fundamentally changed both risk management in general and risk management in leasing activities in particular.

Some other PhD theses, Master's theses have researched the business activities of the Vietnam Bank for Agriculture and Rural Development as well as mentioned a number of different business aspects, including issues of credit risk of some branches in the Vietnam Bank for Agriculture and Rural Development system. However, in general, up to now, there has not been any topic that comprehensively researches the credit risk management of the Vietnam Bank for Agriculture and Rural Development, updated to the present time.

3. RESEARCH PURPOSE:

- Explain and systematize basic theoretical issues on risk management in general and bank credit risk in particular.

- Research on issues related to credit risk management, experiences of developed countries, international practices and the possibility of lessons that can be referenced and applied to Vietnamese commercial banks in general and Vietnam Bank for Agriculture and Rural Development in particular.

- Based on practical theory combined with analysis of the current situation and specific operations of the Vietnam Bank for Agriculture and Rural Development to build an effective credit risk management strategy, thereby proposing solutions and recommendations to improve and enhance the effectiveness of credit risk management of the Vietnam Bank for Agriculture and Rural Development, contributing to the process of restructuring the agricultural and rural economy towards industrialization and modernization, promoting the integration and development of our country's economy.

Male.

4. OBJECTS AND SCOPE OF RESEARCH:

- Research object: Credit risk management at Vietnam Bank for Agriculture and Rural Development

- Research scope: Focus on credit risk management research in general.

General and assessment of credit risk management at the Vietnam Bank for Agriculture and Rural Development, from which to propose solutions and recommendations to improve and enhance the effectiveness of credit risk management at the Vietnam Bank for Agriculture and Rural Development. The data focuses on the period 2005-2010. Some data tables and sources are taken more broadly than some previous years for comparison and research to clarify the development trends of the current situation.

5. RESEARCH METHODS:

The thesis approaches the research object based on the application of dialectical materialism as the general methodology. The thesis emphasizes the survey and summary of practice, comparing practice with the theoretical framework of credit risk management models of countries in the world and in the country to argue and propose the construction of a credit risk management model of the Vietnam Bank for Agriculture and Rural Development. The specific methods used are:

Analysis and synthesis: This method is first used to evaluate existing domestic and foreign studies, thereby forming a theoretical framework for the thesis. In addition, it is also used to evaluate the quality of credit risks of Vietnamese commercial banks through analyzing risk management models in some developed countries, especially BASEL I and BASEL II standards in credit risk management...

Comparison method: Compare the current status of credit risk management of commercial banks with each other and with the requirements of innovation in credit risk management, thereby finding out the shortcomings and clarifying the causes.

Typical evaluation methods of policy science, especially methods of analyzing and evaluating policy documents :

This method is mainly used to assess the institutional environment in credit risk management, as well as changes in that environment through the issuance of policy documents of the Government and the State Bank through different stages.

Field investigation method using semi-structured interviews: Applied to find out the opinions and views of relevant subjects (State management agencies, socio-political organizations, people, businesses, research agencies... at different levels) to assess the current status of credit risk management models in Vietnam, as well as consider the recommendations for innovation that these subjects put forward.

Method of collecting data and documents issued through official channels. In which, the main data sources are taken from secondary data such as: reports from relevant agencies of the Party and State, relevant agencies (Government, State Bank of Vietnam, Ministry of Planning and Investment, Ministry of Finance, commercial banks in Vietnam, Vietnam Bank for Agriculture and Rural Development, etc.); summary reports from commercial banks as well as published results of conferences, seminars, investigations, surveys and scientific research topics conducted by relevant organizations and individuals at home and abroad. Primary data sources include information and data collected through field surveys at a number of commercial banks in Vietnam.

6. STRUCTURE OF THESIS:

In addition to the introduction, conclusion, list of references, list of tables, diagrams and drawings, the main content of the Thesis includes about 232 pages, structured into 3 main chapters:

Chapter 1: Credit risk management at commercial banks

Chapter 2: Current status of risk management of Vietnam Bank for Agriculture and Rural Development Chapter 3: Perfecting credit risk management of Vietnam Bank for Agriculture and Rural Development

Vietnam

CHAPTER 1:

CREDIT RISK MANAGEMENT AT COMMERCIAL BANKS

1.1. RISKS IN COMMERCIAL BANK'S BUSINESS ACTIVITIES:

1.1.1. Risks in commercial bank business activities:

1.1.1.1. Concept of risk:

Traditionally, risk is defined as an event that could result in loss of assets or incur a liability, which cannot be measured. Modern risk has a broader and measurable meaning, and includes not only financial risk but also risks related to operational and strategic objectives.

According to Frank Knight: “risk is a measurable uncertainty” [24, p.233]. Allan Willet believes that “risk is a specific uncertainty related to the occurrence of an unexpected event” [24, p.6]. According to Peter Rose, risk for a bank means “the level of uncertainty related to some events” [24, p.207]. In general, all views believe that risk is uncertainty, occurring unexpectedly, beyond the subject's will.

Risk can be understood as the possibility that uncertain future events will cause the entity to fail to achieve strategic and operational goals, as well as the opportunity cost of losing market opportunities.

1.1.1.2 .Basic risks of commercial banks:

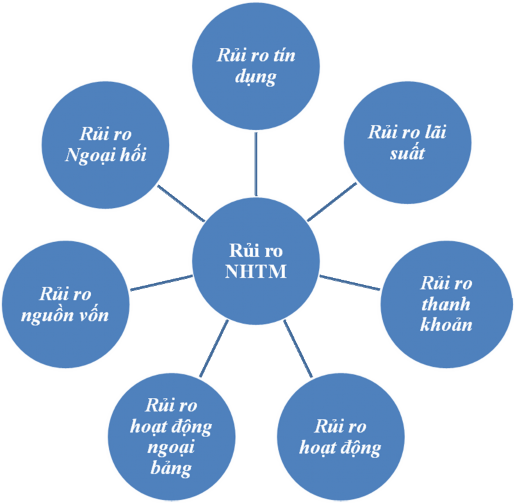

Risks are very diverse, can be analyzed from many different aspects, at the same time, types of risks are closely related to each other, one risk can be the cause of another risk. In the scope of this thesis, only some basic types of risks that a modern bank often encounters and the relationship between some types of risks and credit risks (see diagram 1.2 on the next page) :

- Credit risk: Credit risk arises in the event that the bank does not collect the full principal and interest of the loan, or the customer does not pay the principal and interest on time.

- Interest rate risk: If the bank maintains a structure of assets and liabilities with maturities that are not proportional to each other, it will have to bear interest rate risks in refinancing assets or when the value of assets changes due to fluctuations in market interest rates. In addition, interest rate risk is also reflected when the inflation rate increases faster than expected inflation while the lending interest rate cannot be adjusted, the bank may have to bear the risk if the inflation rate is greater than or equal to the lending interest rate (negative real interest rate).

Figure 1.1. Main types of risks of commercial banks [17]