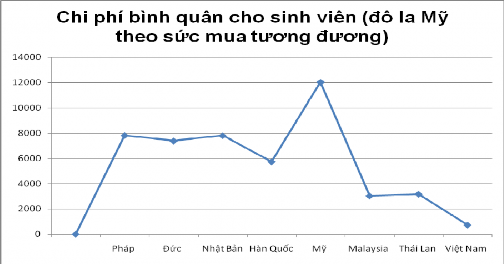

Figure 2.5. Comparison of annual expenditure on sexual education by purchasing power parity

Source: Ministry of Education and Training, Project on innovation of educational financial mechanism for the period 2009-2014 .

Besides, the current financial management mechanism for higher education also reveals shortcomings and limitations, affecting the operation and quality of higher education.

First, the main shortcomings are related to university financial resources.

Public universities are implementing the financial autonomy mechanism according to Decree 43/2006/ND-CP of the Government, but are not really autonomous in terms of tuition revenue: they cannot decide on their own tuition fees but still have to comply with the tuition ceiling stipulated in Decree 49/2010/ND-CP dated May 14, 2010 of the Government, which is not commensurate with current training costs.

For public universities that are partly self-sufficient in regular operating expenses, the State allocates funds according to the budget allocation mechanism for each school. According to Nguyen Truong Giang [27], the current budget allocation for education and training is based on a fixed level, not linked to the number and scale of annual enrollment, but is allocated on average according to budget capacity.

According to the report of the Ministry of Finance [26], the content of the State budget allocation is mainly based on input factors, so it has not linked the results of using State budget resources with the results and effectiveness of performing tasks. At the same time, the State does not have enough criteria to evaluate the results of performing tasks associated with the assigned State budget. This allocation method clearly does not create pressure requiring universities to improve quality to increase competitiveness to attract socialized resources but still rely on the State budget. At the same time, for the State, the use of the State budget has not created a priority orientation for activities.

The activities of quality educational institutions, prioritizing training occupations that the State needs but society is not ready to meet.

Second, the main shortcomings are related to financial spending.

Decree 43/2006/ND-CP stipulates that when the state adjusts salary regulations, schools must ensure their own income from career sources. Thus, every time there is salary reform, schools will have to cut financial resources for direct training activities to increase salaries, directly affecting training quality.

Although schools are financially autonomous, they still have to comply with outdated and unreasonable technical and economic norms and industry standards. Many technical and economic norms are still lacking, but schools are not allowed to develop them themselves.

Assessing the shortcomings of the financial mechanism for higher education, Phung Xuan Nha and the research team [28] stated that "the shortcomings related to financial resource management such as budget allocation and allocation; regulations on tuition fees are considered the most prominent". The outstanding features of the current financial management mechanism for higher education have a decisive influence on the financial management mechanism for high-quality training programs in public universities in terms of budget management and allocation; management of tuition revenue; inspection and supervision mechanisms.

2.2.2. Current status of financial management mechanism for high-quality training programs in public universities

2.2.2.1. Current status of budget management mechanism for CLC training programs

The budget management mechanism is applied to current CLC training programs in a manner approved by the State, assigned tasks and allocated budget to public universities. The budget for implementing CLC training programs is arranged in the budget estimate for the education and training sector and the budget management mechanism is implemented according to regulations for the public finance sector.

The State budget expenditure for the education and training sector is an expenditure item that has been set a ceiling by the Ministry of Finance, the agency responsible for state management of the financial sector, within the total budget expenditure of the Government. In the current period, the Government's commitment to spend the State budget for education and training reaches 20% of the total budget expenditure. The expenditure for high-quality training programs of public universities is arranged within the above-mentioned commitment, which has a direct impact on the budget management mechanism (specifically the investment budget level) for high-quality training programs.

The budget management mechanism for CLC training programs is demonstrated through the following contents:

The first is about the method of budget preparation and allocation.

Step 1: Public universities with CLC training programs prepare budget estimates and send reports to the Ministry of Education and Training or other ministries, governing agencies, and localities (for public universities not directly under the Ministry of Education and Training) (referred to as governing ministries). The budget estimates are based on:

The contents and corresponding expenditures already implemented in the previous year's program;

Technical and economic norms and financial norms have been stipulated in State documents or in approved Projects; number of students enrolled in the budget year; contents and expenditure items that need to be budgeted to implement the program;

The content increased or decreased compared to the previous year and other factors (if any).

Step 2: The Ministry in charge of universities with CLC training programs reviews the budget estimates for affiliated schools; then synthesizes them into the Ministry's education and training sector budget estimates according to the expenditure items submitted to the Ministry of Finance.

Step 3: The Ministry of Finance reviews and discusses with the Ministry/competent agency the budget items prepared by the Ministries/competent agencies and the budget capacity within the controlled ceiling to be able to come up with a reasonable budget. Normally, the agreed budget level ensures a certain percentage increase compared to the previous year and meets part of the spending needs of public universities that have been compiled by the competent ministries.

Step 4: Based on the budget discussed with the relevant Ministries, the Ministry of Finance synthesizes the expenditure budget and reports to the Government for submission to the National Assembly.

Step 5: The National Assembly discusses and decides on state budget expenditures for each expenditure area.

Step 6: The Ministry of Finance, based on the National Assembly's Resolution on the state budget estimate, submits to the Prime Minister a decision to assign the budget expenditure estimate to the managing Ministry, detailing the fields/tasks corresponding to the expenditure items of the high-quality training program.

Step 7: The Ministry of Finance, authorized by the Prime Minister, guides the budget expenditure tasks for the managing Ministry, including details of the CLC training tasks. The budget estimate for CLC training programs is assigned by the Ministry of Finance to the managing Ministries according to separate or joint Projects and is distributed by the managing Ministry.

The funding for universities is included in the total estimated budget for education and training.

Step 8: After receiving the budget estimate from the Prime Minister, the competent Ministry will allocate the budget estimate for the CLC training program to universities.

The budget estimate provided will depend on the initial estimate prepared by the school, calculated based on the expenses for the activities of the CLC training program and adjusted by the Ministry in charge according to the level agreed with the Ministry of Finance. Normally, the estimate received by the school will be higher than the previous year's level. According to the method of allocating and distributing funds stipulated in the 2002 State Budget Law and its implementing documents, universities will be allocated funds once a year according to only one item, and schools are autonomous in using financial resources within a certain scope as prescribed by law.

Government

The process of budgeting and allocating for CLC training programs is described in Diagram 2.1 below.

BKHCN

Ministry of Education and Training

BTC

Ministry of Planning and Investment

Responsible Ministry/Agency (including Ministry of Education and Training)

Provincial People's Committee

Government-run university

Member University

Universities

Department of Finance

CLC Training Program

Local University

Figure 2.1. Budget allocation process for CLC training programs

Source: author developed from document [28]

Through research on the current situation of the method of establishing and allocating budget estimates for CLC training programs in public universities, it is shown that there are still points that are not consistent with the financial management mechanism model for CLC training programs, which is a collection of management tools and methods that are considered to have the most advantages (as described in Chapter 1). Those points are:

Prepare a budget for the CLC training program using the incremental item method. This budget will be compiled by the Ministry of Education and Training or the governing Ministry to negotiate with the Ministry of Finance on the percentage of the budget that needs to be met.

Prepare and allocate budget estimates for the CLC training program based on input (number of students enrolled in the program and pre-approved cost per student).

The second is about criteria and budget allocation norms.

On budget allocation criteria:

The input data used in the financial allocation formula are the number of students according to the registered enrollment quota of the CLC training program and the budget expenditure per student as prescribed. Normally, the student quota used as the basis for budget allocation is only approximate and has deviations compared to the number of students trained and graduated. The investment cost for CLC training programs is calculated based on economic and technical bases and norms (for example, standard hour/lecturer norm; m2/student norm; student/lecturer norm...). However, the financial norms are relatively backward, without distinction according to the characteristics of each training sector.

In addition, the State budget investment criteria generally do not have significant distinctions between training sectors (For example, according to the Strategic Task Project of Hanoi National University, the allocation rate between sectors differs by about 7-10%; the CTTT Projects only differ by about 5%). The allocation criteria do not reflect the difference in cost structure between training sectors/professions; at the same time, they do not take into account the ability to attract social resources between different sectors. For example, the CTTTs in the fields of science and technology, engineering and economics all set the contribution rate of learners at 15%, and that of the school at 25%. The State invests in high-quality training programs but does not differentiate to implement priority policies for some training sectors where the State has a need for high-quality human resources. For example, the State budget is still allocated to implement the high-quality training program in Banking and Finance of the National Economics University; International Economics Department of Foreign Trade University

Commerce, Technology majors of Hanoi University of Science and Technology, Ho Chi Minh City University of Technology,... In reality, these are the majors that receive attention from society, and can mobilize other financial resources to reduce the burden on budget expenditures.

Thus, the use of criteria for budget allocation for CLC training programs is not effective in creating financial incentives to help CLC training programs achieve their set goals.

On budget allocation norms:

The fundamental difference in the budget allocation management mechanism for CLC training programs is that the budget allocation basis is adjusted higher than that for mass training programs. Compare the allocation standards for CLC training programs with those for mass training programs in Table 2.4 and Chart 2.6.

The comparison results in Table 2.4 and Chart 2.6 show that the budget allocation for CLC training programs is much higher than that for mass training programs. Thus, the State has a policy of prioritizing investment in CLC training. The higher budget allocation ensures that CLC training programs are implemented as committed.

Table 2.4. Comparison of budget allocation norms between CLC training programs and mass training programs

Unit: VND/student/year

TT

Programme | Budget allocation/student/year | |

1 | Mass training programs of universities under the Ministry of Education and Training | 6,133,680 |

2 | Mass training programs of universities under VNU | 7,560,000 |

3 | Mass training programs of schools under VNU-HCM | 6,290,700 |

4 | Program to implement the Advanced Training Program Project of the Ministry of Education and Training | 38,000,000 |

5 | The DTCL programs under the NVCL Project of VNU | 24,000,000 |

6 | VNU-HCM's University of Technology and Education programs (under the University of Technology and Education Project with corresponding tuition fees) | 19,000,000 |

Maybe you are interested!

-

Organizing Capacity Training to Develop School Education Programs According to the New General Education Program for Management and Teaching Staff

Organizing Capacity Training to Develop School Education Programs According to the New General Education Program for Management and Teaching Staff -

Evaluation of the Results of Training on Math Teaching Capacity According to the New General Education Program for Teachers in Secondary Schools

Evaluation of the Results of Training on Math Teaching Capacity According to the New General Education Program for Teachers in Secondary Schools -

Measure 2: Tighten Management of the Development and Implementation of Program Content, Teaching Plans, Education and Training in Disaster Prevention

Measure 2: Tighten Management of the Development and Implementation of Program Content, Teaching Plans, Education and Training in Disaster Prevention -

Research on innovation of knowledge of the undergraduate training program in Physical Education, Hung Vuong University, Phu Tho Province - 25

Research on innovation of knowledge of the undergraduate training program in Physical Education, Hung Vuong University, Phu Tho Province - 25 -

Research on innovation of knowledge of the undergraduate training program in Physical Education, Hung Vuong University, Phu Tho Province - 17

Research on innovation of knowledge of the undergraduate training program in Physical Education, Hung Vuong University, Phu Tho Province - 17

Source: author compiled from projects of schools

Figure 2.6. Comparison of budget levels of training programs

Source: author compiled from projects of schools

However, it can be seen that the allocation norms do not reflect the actual costs required to ensure training quality. The State budget for CLC training programs has not paid attention to balancing with socialized revenue sources. Although there is a distinction in the budget allocation level, it is not significant between training sectors. Therefore, in reality, implementing training "programs in the science and technology sector with low attraction and low number of students participating will be more difficult than those in the economic sector" [12]. Obviously, the State has not made good use of financial management tools to regulate CLC training programs to meet management goals and social needs.

Thus, it can be affirmed that the distinct characteristics in the financial management mechanism of the State budget allocated to the CLC training program have not met the State's priority orientations for developing CLC training programs. The management mechanism for allocating budget for CLC training programs does not create a strong driving force to improve the quality of CLC training programs from management technology, training programs and products.

Third, the State budget funds invested in CLC training programs.

Up to now, the CLC training programs invested by the State in public universities have had many graduates. The State has allocated a significant financial resource from the State budget to invest in these programs. Data on the financial resources of the State budget invested in CLC training programs are summarized in Table 2.5 below. The results of the programs need to be evaluated to see the effectiveness of the State budget investment, thereby drawing experience and directions to improve the quality of training.

Table 2.5. Sources and financial structure of CLC training programs invested by the State budget

Unit: thousand dong

STT

Vietnam public university | Program name | Financial resources for investment in CLC training programs | |||||||

Total | State budget | Tuition | Other sources | ||||||

Amount | Proportion | Amount | Proportion | Amount | Proportion | ||||

1 | University Polytechnic, VNU-HCM | Electrical Engineering | 43,086 | 31,116 | 72% | 11,970 | 28% | 0% | |

2 | Hue University | University of Education, Physics | 27,600 | 27,600 | 100% | 0 | 0% | 0% | |

3 | University of Economics, Agricultural Economics - Finance | 33,312 | 25,212 | 76% | 8,100 | 24% | 0% | ||

4 | National Economics University, | Finance | 33,649 | 25,212 | 75% | 8,437 | 25% | 0% | |

5 | Accountant | 33,649 | 25,212 | 75% | 8,437 | 25% | 0% | ||

6 | Hanoi University of Science and Technology | Biomedical Engineering | 34,356 | 31,116 | 91% | 3,240 | 9% | 0% | |

7 | Mechatronics | 32,751 | 31,116 | 95% | 1,635 | 5% | 0% | ||

8 | Physics and technology whether | 32,751 | 31,116 | 95% | 1,635 | 5% | 0% | ||

9 | University of Technology - University of Danang | System dip | 35,856 | 31,116 | 87% | 4,740 | 13% | 0% | |

10 | Telecommunication Electronics number system | 35,856 | 31,116 | 87% | 4,740 | 13% | 400 | 1% | |

11 | University of Science – VNU Hanoi Internal | Chemistry | 29,235 | 27,600 | 94% | 1,635 | 6% | 320 | 1% |

12 | Mathematics | 30,840 | 27,600 | 89% | 3,240 | 11% | 0% | ||

13 | Environmental Science | 30,840 | 27,600 | 89% | 3,240 | 11% | 0% | ||

14 | Can Tho University | Aquaculture | 31,506 | 28,938 | 92% | 2,568 | 8% | 315 | 1% |

15 | Biotechnology | 31,506 | 28,938 | 92% | 2,568 | 8% | 0% | ||

16 | University of Science – VNU HCMC | Computer Science | 49,162 | 27,900 | 57% | 21,262 | 43% | 0% | |

17 | Hanoi University of Agriculture | Agricultural Business Management | 32,178 | 28,938 | 90% | 3,240 | 10% | 0% | |

18 | Plant Science | 30,573 | 28,938 | 95% | 1,635 | 5% | 0% | ||

19 | University Transportation | Construction Engineering | 36,516 | 31,116 | 85% | 5,400 | 15% | 0% | |