environmental taxes, resource taxes, solid waste treatment costs, wastewater discharge costs and costs related to mineral exploitation activities.

+ Fines and compensation costs: Costs related to non-compliance with regulations on control, handling and exploitation of mineral resources, costs related to compensation, compensation for environmental damage, etc.

+ Outsourced service costs: The costs of all outsourced services related to waste control and treatment.

(2) Environmental management and prevention costs

Environmental management and prevention costs are costs to prevent the generation of waste including solid, liquid and gaseous waste and costs to operate management activities for environmental issues arising at the enterprise.

Some of the costs for environmental prevention include: investment costs for installing technology and improving cleaning efficiency, increased differences due to the decision to use more environmentally friendly materials in production, etc.

Expenses for environmental management activities include: expenses for hiring environmental consultants, expenses for training employees to improve their understanding of issues surrounding the enterprise, expenses for operating the environmental management accounting department, environmental auditing, and expenses for propaganda activities to enhance the image of corporate social responsibility.

From the perspective of managers, they always want to minimize costs related to waste control and treatment, but they are always interested in improving the social responsibility of the business. Therefore, managers are always interested in investing in activities related to waste prevention.

(3) Cost of materials generating waste

The main result of the production process is the product, but the amount of waste generated in this process is not small and the treatment of this waste is very expensive and has a negative impact on the environment. Thus, it can be seen that businesses not only spend money on controlling, managing and treating waste but also lose

waste material costs. Waste material costs can be divided into the following groups:

Raw material cost: this is the raw material that participates in the production process but does not create finished products but is in the form of scrap and waste.

Packaging costs: Most product packaging becomes waste when it leaves the business and reaches the consumer.

Energy costs: fuels involved in the production process as well as business operations during the energy conversion process also create useless energy.

Water costs: Water used for production but does not go into the product but becomes wastewater at the end of the production process.

(4) Environmental research and development costs

In businesses, they do not just wait for environmental problems to occur before dealing with them, but they also need to constantly research to find new ideas and solutions to improve environmental problems such as: research costs to reduce mold toxins in aquatic feed, research costs to test new materials to reduce waste, etc. Environmental research and development costs are also very diverse and are also divided into the following groups:

Depreciation costs of research equipment assets

Cost of raw materials, materials, fuel

Labor costs

Outsourcing service costs

Other cash expenses

(5) Other environmental costs: are costs incurred in production such as labor costs and depreciation costs that are wasted due to inefficient production.

b) Based on business activities

According to the Ministry of Environment of Japan, 2015; Environmental costs are classified by business activities as follows:

Business costs: are environmental protection costs to control the impacts of the main production and business activities in the business sector on the environment.

Costs at pre-production and post-production stages: are environmental protection costs to control the impacts of business activities at pre-production (suppliers) and post-production (customers) stages on the environment.

Management costs: are costs arising from management activities such as cleaning, office waste, etc.

Research and development costs: are costs arising from research and development activities of environmentally friendly products or research on the use of clean materials, etc.

Social operating costs: are costs arising from social activities such as tree planting, cleaning, beautifying, improving the environment around the business (building roads, dredging sewers, etc.), sponsoring environmental organizations, etc.

Environmental remediation costs: are costs related to environmental degradation treatment such as contingency costs, environmental degradation insurance, etc.

Other costs: Other costs related to the environment.

Classifying environmental costs by business activities helps businesses identify environmental costs in each of their activities, thereby having effective cost management and control measures for each activity.

c) Based on environmental quality control activities

According to Venturelli & Pilisi 2003 and 2005; Environmental costs include prevention costs, monitoring costs, treatment costs and externalities.

Table 1.1: Cost classification by environmental quality control activities

Prevention costs

Monitoring costs | Processing costs | |

- Design and maintain environmental management systems. - Cost of training employees to prevent pollution - Communication costs - Choose green materials | - Environmental audit - Internal environmental monitoring - Supplier and customer monitoring - Waste analysis, measurement | Internal processing costs - Cost of compliance with legal regulations - Operating costs of wastewater treatment system - Environmental insurance |

Maybe you are interested!

-

General Accounting Diagram of Business Management Costs

General Accounting Diagram of Business Management Costs -

Management accounting for production costs and product prices at handicraft manufacturing enterprises in Nam Dinh province - 2

Management accounting for production costs and product prices at handicraft manufacturing enterprises in Nam Dinh province - 2 -

Management accounting of revenue, costs and business results at Viet Anh Production and Trading Limited Company - 2

Management accounting of revenue, costs and business results at Viet Anh Production and Trading Limited Company - 2 -

Organization of management accounting for freight costs in Vietnamese road transport companies - 27

Organization of management accounting for freight costs in Vietnamese road transport companies - 27 -

Management accounting of revenue, costs and business results at Viet Anh Production and Trading Company Limited - 14

Management accounting of revenue, costs and business results at Viet Anh Production and Trading Company Limited - 14

Prevention costs

Monitoring costs | Processing costs | |

- Cost for environmental accounting system - Research and development costs. - Equipment calibration to reduce environmental impact - Recycling costs, waste reduction - Measures to prevent accidents and fires - Improve the transportation of hazardous waste - Plant trees - Sponsorship and social contribution to environmental protection programs school | noise and vibration measurement - Control tools: maintenance and calibration - Depreciation costs of monitoring equipment - Optimize utilities: provide gas, electricity, water - Waste monitoring (emissions, wastewater, solid waste) - Environmental report to competent authorities - Monitoring of electromagnetic and ionizing radiation | - Cost of waste collection and landfill - Taxes and environmental fees for waste treatment Outsourcing costs - Cost of remedy and compensation for damage to third parties. - Cleaning, sanitation, medical care (social welfare) costs - Land and ecosystem improvement costs |

Source: Le Thi Tam, 2017

1.2.2. Establishing norms and making environmental cost estimates

Establishing environmental cost norms and estimates is an important task that helps managers perform well the function of planning and controlling costs in the enterprise. Establishing norms and estimates requires the smooth coordination of many departments in the enterprise and this is also a tool to encourage effective environmental activities from departments and divisions in the enterprise.

1.2.2.1. Building environmental cost standards

Cost norms are the costs of living labor and materialized labor related to the production and business of a unit of product or service under certain conditions.

Cost norms are the basis for building production and business estimates for each

business period. If the cost norm is built to determine the cost of consumption for a product, the estimate is built on the total output of each department and the entire enterprise. Building norms is an effective tool for cost management based on eliminating unreasonable and ineffective production and business activities by implementing remedial solutions. Environmental costs, like other types of costs, must have cost norms built. Environmental cost norms are the basis for enterprises to make environmental cost estimates. Environmental costs in enterprises include many types, including costs that are very difficult to measure. Therefore, current cost norms are often only built for waste treatment costs. Waste cost norms include raw material cost norms for waste treatment and labor cost norms for waste treatment:

The cost standards for raw materials for waste treatment include the quantity standards and the price standards for raw materials used for waste treatment:

- The standard cost of raw materials for waste treatment is the amount of raw materials consumed to treat a unit of waste, the amount of raw materials allowed to be lost during the waste treatment process, the amount of damaged raw materials allowed, etc. Each type of waste will have its own standard for raw materials.

- The standard price of raw materials is the warehouse price calculated for a unit of raw materials, including: purchase price according to invoice, costs during the purchasing process, loss in the standard (natural loss) and minus deductions (trade discounts, sales discounts).

Waste treatment labor cost norms are built based on the amount of labor time required to treat a unit of waste and the price of labor time.

- The standard number of waste treatment workers includes the direct labor time to treat a unit of waste and the stop and rest time for workers.

- Labor time price standards include salary unit price for a unit of labor time (hour, day, ...), salary allowances and salary deductions at current rates.

Other environmental costs such as: costs of preventing and managing environmental pollution, costs of environmental remediation, etc. are not standardized because the costs do not arise regularly, are highly random and difficult to quantify.

1.2.2.2. Prepare environmental cost estimates

A budget is an estimate of a company's future production and business activities, specifying the work that needs to be done, taking into account the impact of subjective and objective factors.

Based on the environmental cost norms, the enterprise proceeds to make an environmental cost estimate. Environmental cost estimate is also a part of production and business budget, so the process of making environmental cost estimate also follows the principles, procedures and methods of making traditional cost estimates. Environmental cost estimates in the enterprise are made at the beginning of each accounting period. The method of making the estimate is as follows:

- Waste treatment cost estimates include estimates of waste treatment material costs and estimates of waste treatment labor costs. Waste treatment material cost estimates are determined based on the expected amount of waste to be treated and the standard cost of materials to treat a unit of waste. To determine the expected amount of waste to be treated, it is necessary to rely on the material flow balance equation in production, or in other words, the expected amount of waste to be treated is equal to the expected amount of raw materials and input materials used for production minus the expected amount of output products from production.

Similarly, the estimated cost of waste treatment labor is determined based on the expected amount of waste to be treated and the standard cost of labor to treat one unit of waste.

- Estimated costs for environmental pollution prevention and management: these costs are estimated based on statistical experience based on reported costs in previous periods and environmental activity plans for the next period of the enterprise.

1.2.3. Allocation and determination of environmental costs

1.2.3.1. Allocation of environmental costs

How are environmental costs and revenues calculated in the current accounting system? Are they allocated to products or processes? Are they fully disclosed in the cost accounting summary or are they hidden in the total cost accounting? How are costs such as waste, energy, water, raw materials, etc. handled? And can costs be reduced further? Can revenues be increased and bring more effective benefits? Are incentives created for environmental improvement?

Thus, to have an accurate assessment and bring practical benefits to the enterprise, it is necessary to have a reasonable calculation method. This demonstrates the important function and role of environmental management accounting. That is to separate environmental costs from production costs and allocate them to appropriate accounts. Thanks to that, the enterprise can motivate competent managers and employees to find solutions to prevent pollution and can reduce costs and increase business efficiency.

There are two ways to allocate general environmental costs to cost-bearing objects: allocation according to one criterion and allocation according to multiple criteria.

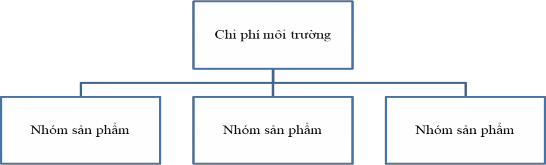

Method 1: Allocation according to 1 criterion - all environmental costs are allocated to objects according to a single standard shown in the diagram below:

Source: Pham Duc Hieu, Tran Thi Hong Mai (2012)

Figure 1.2: Environmental cost allocation model according to a standard

Method 2: Allocate according to multiple standards - accountants choose an allocation standard for costs that are similar in nature and function. Then, to allocate environmental costs to related objects, it is necessary to use many different allocation standards (diagram 1.3):

Environmental costs

Cost Center 1

Cost Center 2

Cost Center 3

Product A

Product B

Product C

Source: Pham Duc Hieu, Tran Thi Hong Mai (2012)

Figure 1.3: Environmental cost allocation model according to multiple standards

Choosing the appropriate cost allocation criteria is decisive for the accuracy of the allocated costs. Choosing to allocate according to method 1 or method 2 depends on the specific situation and must determine the cause of environmental costs. In theory, there are 4 criteria considered for selection in the general allocation of environmental costs: ( Hoang Thi Bich Ngoc, 2017)

- The amount of waste emitted or the amount of waste treated.

- Toxicity of the emission or amount of waste treated.

- Additional environmental impact (Different amount for impact per unit of quantity) of the emission.