4.2.3.2. Check and review signed export contracts and transportation contracts

- Check and review contracts for exporting goods by sea

An export contract is an agreement between parties in different countries, under which the seller is obliged to transfer ownership of a certain asset called goods to the buyer, the buyer is obliged to pay the seller, receive the goods and receive ownership of the goods according to the agreement.

An export contract includes basic terms such as goods name terms, quantity/volume terms, quality terms, packaging-marking terms, delivery terms, price terms, payment terms, complaint terms, arbitration terms, force majeure terms, sanctions for violations, terms of law applicable to the contract, difficulty and obstacle terms, terms of the time the contract takes effect, and language terms of the contract.

Maybe you are interested!

-

Check Inventory Prices and Economic Contracts

Check Inventory Prices and Economic Contracts -

![Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branchs income.

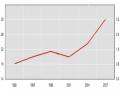

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giangs profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project Restructuring the system of credit institutions in the period 2011-2015 approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services.

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giangs products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Ministers Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giangs treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giangs income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giangs corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giangs card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:Courier New, monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:Times New Roman, serif; font-style: normal; fo](https://tailieuthamkhao.com/uploads/2022/06/06/dich-vu-phi-tin-dung-tai-ngan-hang-thuong-mai-co-phan-dau-tu-va-phat-8-1-120x90.png) Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branch's income.

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giang's profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project "Restructuring the system of credit institutions in the period 2011-2015" approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: "Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services".

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giang's products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Minister's Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers' cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giang's treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giang's income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giang's corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giang's card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:"Courier New", monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:"Times New Roman", serif; font-style: normal; fo

Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branch's income.

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giang's profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project "Restructuring the system of credit institutions in the period 2011-2015" approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: "Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services".

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giang's products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Minister's Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers' cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giang's treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giang's income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giang's corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giang's card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:"Courier New", monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:"Times New Roman", serif; font-style: normal; fo -

Vietnamese law on loan contracts in the field of banking credit - 28

Vietnamese law on loan contracts in the field of banking credit - 28 -

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market:

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market: -

Coffee export activities at Generalexim company - 1

Coffee export activities at Generalexim company - 1

In order to avoid causing errors, confusion, and disputes later, the two parties in the export contract, especially the exporting enterprise, need to clearly and fully record the information in the contract, especially paying attention to unifying the information between the export contract and the contract for transporting goods by sea regarding the goods, loading port, unloading port, method of delivery, freight rates, responsibility for delivery, compensation, and exemption from liability during the transportation process.

When signing an export contract, Vietnamese export enterprises need to pay special attention to the following two terms:

+ Terms on goods: the issue of goods inspection will be agreed upon by the parties, however, usually according to the export contract, goods will be randomly inspected before accepting the order and receiving the goods at the port of destination, so the goods may be damaged and not meet the requirements as stated in the contract due to reasons related to the exemption cases that the sea carrier is entitled to. Therefore, the contract needs to have an appendix with detailed and clear regulations on the quality and quantity of goods in case of damage related to the exemption of the carrier to limit the impact on both the import and export parties in general and the exporter in particular.

+ Terms of transportation and insurance: Normally, import-export companies will choose the basic delivery terms in Incoterms (version 1990, 2000, 2010 or 2020) to regulate transportation and insurance. Normally, Vietnamese enterprises choose FOB terms (delivery on board) when purchasing goods and CIF terms (cost, insurance and freight) when selling goods. However, according to actual changes in the process of international trade transactions as well as what the Arbitration Center

Vietnam International, in addition to the Vietnam Chamber of Commerce and Industry (VIAC), has recommended that it is time for Vietnamese enterprises to abandon the FOB and CIF conditions, and instead use the FCA (delivered to carrier) and CIP (freight and insurance paid to) conditions. Because for containerized goods, the place of delivery to the sea carrier at the loading port is CY (container yard) and CFS (less than containerized freight station), so the process of loading and unloading containers onto and off ships is currently carried out by the sea carrier, making it difficult for exporting enterprises to control. Therefore, the risks during the loading and unloading process when choosing the two FCA and CIP conditions as recommended by VIAC will be transferred to the importing enterprise when the exporting enterprise delivers the container to the shipping line at the container yard (CY) or CFS (less than containerized freight station) at the loading port, not after the goods have been loaded onto the ship at the loading port.

- Check and review contracts for the transport of goods by sea

A contract for the carriage of goods by sea is a contract signed between the parties involved, including the shipping service provider and the shipper, in writing, including commitments and agreements during the carriage of goods. Accordingly, those responsible must properly perform the obligations stated in the terms of the contract. The shipping company collects the freight paid by the customer and transports the goods from the port of receipt to the port of delivery by sea.

The contract for the carriage of goods by sea is the most effective document to resolve disagreements between the carrier and the consignor when disputes arise, including provisions related to compensation for damages to goods in case of damage or loss. If the exporting enterprise charters a ship and signs a contract for the carriage of exported goods by sea, the exporting enterprise and the shipping enterprise will be two parties in the contract for the carriage of exported goods, with opposing interests. Therefore, the exporting enterprise should be careful and carefully consider the terms of the carriage contract before signing, to avoid conflicts later.

Sea freight contracts are usually drafted according to standard forms, issued according to State regulations. Export enterprises need to fully check the following information:

- Shipper, consignee, shipping company: Company name, address, tax code. If the contract is signed by an individual, a power of attorney is required.

- Information about the shipment to be transported: name of item, type of item, quantity, weight, care and preservation methods during delivery and unloading.

- Loading and unloading port

- Means of transport used in sea transport: ship type, engine, ship code, ship name, ship age, registered capacity, tonnage, draft, class certificate.

- Fare, payment method and time.

- Responsibility of each party.

- Disclaimer clause for sea carriers.

- Terms of compensation for damages.

- General average clause.

- Delivery and receipt time.

Thus, in the contract for the carriage of goods by sea, both the sea carrier and the shipper (exporter) need to clearly state the terms of goods name, specifications, quality, quantity, price and especially the delivery terms to avoid unwanted losses for both parties caused by the carrier's exemption. In particular, the terms in the contract for the carriage of goods by sea should be consistent with the terms in the international contract for the sale of goods to avoid disputes.

In addition, the important clause in the contract for transporting goods by sea that Vietnamese exporters need to pay close attention to in order to proactively respond to the clause on cases of exemption from liability that the sea carrier is entitled to. Exporters only sign the contract for transporting goods by sea when the clause on cases of exemption from liability of the sea carrier complies with the provisions of the 2015 Vietnam Maritime Code, the sea carrier is not allowed to add any other exemptions other than the provisions of the 2015 Vietnam Maritime Code to the transport contract.

Sea freight contracts are one of the factors that ensure international trade takes place quickly and smoothly, therefore, we need to ensure that the contracts are presented accurately and completely.

4.2.3.3. Strengthening supervision of the implementation of contracts for the transport of goods by sea

The 2005 and 2015 Vietnamese Maritime Codes have similar provisions on the cases of exemption of the carrier under the contract of carriage of goods by sea and tend to protect the sea carrier quite a lot. In addition, Vietnam applies both the principle of listing (clause 2, article 150) and the principle of presumption of fault in the provision regulating the carrier's obligation to "prove that he has performed his duties diligently". Therefore, Vietnamese export enterprises need to closely monitor the implementation of the contract of carriage of goods by sea.

- Supervise the vessel and check before carrying out the transportation contract whether the vessel is seaworthy or not before departing on the journey.

The carrier is not responsible for loss or damage to the goods due to the ship's unseaworthiness when proving that he has performed his duties diligently. Finding evidence to prove the lack of diligence, making the sea carrier convinced, takes a lot of time, and often the exporting enterprise does not have enough evidence. And if the goods are damaged after the ship has left the loading port, even if the exporting enterprise complains to the sea carrier for the fault of "ship's unseaworthiness", it is difficult to win the case, because the responsibility to ensure the ship's seaworthiness is only the obligation of the sea carrier before the journey begins. Damage to the ship during the sea journey is easily attributed to the ship's latent defect - one of the 17 exemptions that the sea carrier is entitled to under the 2015 Vietnam Maritime Code.

Therefore, the exporting enterprise must ensure that the ship it charters is seaworthy before departure, that is, before leaving the port of loading. That is, the exporting enterprise must monitor whether the ship is seaworthy or not, has a crew suitable for the ship's tonnage and cargo capacity, is fully supplied with equipment and spare parts; and whether the cargo holds, cold storages and other areas used for transporting and preserving goods have adequate conditions appropriate to the nature and characteristics of the goods.

- Review the monitoring of other procedures.

In addition to checking the ship before departure, the exporting enterprise needs to supervise the confirmation of payment of freight; the preparation of goods such as whether the packaging is correct or not, whether the goods have been marked, signed, coded correctly and appropriately or not to avoid damage that the carrier is exempted from liability if the sea carrier is responsible for performing such work according to the provisions of the contract of carriage of goods by sea. The exporting enterprise must check whether the sea carrier has fully prepared the necessary procedures to ensure that the goods as well as the means of transport are exported or imported across national borders.

- Regularly check and monitor goods and sea carriers during the ship's voyage.

During the time the ship is at sea, the cargo owner and the exporting enterprise must request the carrier to provide the ship's location for easy monitoring. And the exporting enterprise must closely monitor and follow the ship's route and activities on the ship to ensure that when damage and loss occur, they are actually due to objective causes, circumstances.

force majeure, regardless of the carrier's subjective will or not. At the same time, the exporting enterprise should also use the bill of lading number to continuously track the cargo's journey through the shipping line's website, knowing exactly which seaport or sea area the cargo is in, or which international territorial waters.

Supervision during the ship's voyage is very necessary, because during the ship's voyage, damage and loss are likely to occur, so exporting enterprises need to carefully monitor the weather, political situation, epidemic situation, etc. at the place where their ship passes through to limit damage and loss to the goods for which the carrier can be completely exempted from responsibility.

In addition, by closely monitoring the time the ship is at sea, the exporting enterprise can limit damage and loss due to natural disasters, epidemics, riots, wars, etc. and can quickly find the most suitable solution, minimizing damage. And the exporting enterprise can also respond more easily when encountering cases of exemption from liability of the carrier according to the contract of transporting goods by sea, thereby helping to promote the export activities of the enterprise in particular and the export turnover of Vietnam in general.

4.2.4. Group of solutions to respond when the carrier is exempted from liability under the contract of carriage of goods by sea.

To effectively respond when the carrier is exempted from liability for losses of goods due to causes falling within the carrier's liability exemption cases under the contract of carriage of goods by sea, the two parties in the export contract must purchase insurance for exported goods transported by sea, depending on the international trade conditions signed in the export contract. Usually, the exporting enterprise must purchase insurance for exported goods if selling goods under the delivery basis conditions CIF, CIP Incoterms 2010, 2020.

Insurance for import and export goods transported by sea is a type of insurance with the insured object being goods and assets transported from the receiving location in one country to the delivery location in another country by sea. The insurance buyer (exporter or importer) commits to pay the insurance premium and the insurance seller (insurance company) commits to compensate the insured party if there is any loss or damage to the goods during the transportation by sea within the space and time of insurance. The insurance space for export goods transported by sea according to the insurance rules of the UK (ICC 1963, ICC 1982) and the insurance rules of Vietnam (QTC 1965, QTC 1990) is from the departure warehouse to the destination warehouse. The insurance period for export goods transported by sea according to the insurance rules

According to the British Insurance Code (ICC 1963, ICC 1982) and Vietnamese insurance rules (QTC 1965, QTC 1990), the period of time from the time the goods are loaded onto the means of transport, brought to the port and loaded onto the ship to carry out the sea transport journey until the goods are safely in the warehouse or after 60 days from the time the goods are unloaded from the ship but have not yet safely entered the warehouse, whichever occurs first.

Many risks can occur to exported goods during the sea journey, so normally, insurance contracts for exported goods transported by sea will have a certain coverage. The scope of insurance for imported and exported goods is the limit of the risks of the goods that the insurance company can pay. This is also the basis for determining the responsibility of the insurance company when risks occur. Only losses caused by insured risks that are the direct cause will be compensated by the insurance company. Insured risks are risks included in the list of insured risks listed in the insurance contract signed between the insurance company and the export enterprise. The wider the coverage, the more risks are insured, resulting in higher insurance premiums, increasing costs for the export enterprise.

Export enterprises can sign insurance contracts for exported goods transported by sea in two types: voyage insurance contracts and cover insurance contracts. Voyage insurance contracts are insurance contracts for exported goods for each shipment. Cover insurance contracts are insurance contracts applied to many shipments of the same export enterprise within a certain period of time, usually 12 months. Export enterprises that regularly export goods will use cover insurance contracts.

The procedure for an exporting enterprise to purchase insurance for exported goods includes the following 6 steps: Submit an insurance request, Fill in all information on the insurance request form, The enterprise purchasing insurance sends a copy of the insurance request form to the insurance company as requested, The insurance company sends the insurance contract back to the enterprise purchasing insurance for exported goods, The enterprise purchasing insurance signs the confirmation on the insurance contract, The customer purchasing insurance pays the export goods insurance premium.

When encountering cases of exemption from liability of the carrier under the contract of transporting exported goods by sea, the exporting enterprise will be affected, possibly leading to the inability to perform its obligations in the export contract. At that time, the exporting enterprise will be exempted from liability if the obligation to perform the export contract is not performed, not fully performed or not performed on time due to force majeure events (here, due to the loss of exported goods transported by sea, the cause of which is the cases of exemption from liability of the sea carrier).

According to Article 294 of the 2005 Commercial Law, the party violating the sales contract: (1) is exempted from liability in the event of a force majeure event. However, this provision only recognizes a force majeure event as a basis for exemption from liability without specifying what a force majeure event is. Therefore, the exporting enterprise needs to prove that: The enterprise could not foresee the obstacle and its impact on the ability to reasonably perform the export contract at the time of signing; The failure to perform was due to a difficulty or obstacle that occurred beyond the control of the enterprise; The enterprise could not reasonably avoid or overcome the difficulties or obstacles or at least their impact; (2) The time limit for performing the export contract is extended if the performance of the export contract is delayed due to a force majeure event.

According to Article 296 of the 2005 Commercial Law, when a force majeure event occurs, the parties may agree to extend the time limit for performing contractual obligations. If the parties do not have an agreement or cannot reach an agreement, the time limit for performing contractual obligations shall be calculated for an additional period of time equal to the time of the force majeure event plus a reasonable time to remedy the consequences.

Article 79, paragraph 4 of the 1980 United Nations Vienna Convention on Contracts for the International Sale of Goods provides as follows: “A party who fails to perform his obligations must notify the other party of the impediment and its effect on his ability to perform. If the notice does not reach the other party within a reasonable time after the party who fails to perform knew or ought to have known of the impediment, he shall be liable for damages resulting from the failure to receive notice.”

However, the exporting and importing parties in the international sales contract need to clearly stipulate the notification period and the consequences of failure to notify. In case the parties do not have a specific agreement on the consequences of failure to notify in the international sales contract, the parties will comply with the applicable law to resolve the issue. Therefore, to ensure their interests, Vietnamese exporting enterprises when encountering force majeure events due to export goods being damaged by the exemption cases of the sea freight carrier need to perform the following tasks:

- Send the importing enterprise a written notice (fax, telegraph, email, telegram, registered letter, etc.) about the force majeure event within the validity period of the export contract or within the period prescribed by the applicable law; if there is no provision, within a reasonable period of time.

- Attached to the notice is a certificate from a competent authority or other legal documents and evidence with evidentiary value. If the exporting enterprise sends it to the other party

Notification of force majeure without supporting documentation will certainly not be accepted.

Then, the exporting enterprise requests the insurance company for the exported goods transported by sea to compensate for the loss of the goods due to the insured risks being the direct cause. And those insured risks are in the cases of exemption from liability of the carrier of exported goods according to the contract of transporting goods by sea. Specifically, the exporting enterprise must do the following:

- Require the importing enterprise to check the condition of the goods when the sea carrier delivers the goods at the port of destination.

- When a loss occurs, it is necessary to immediately notify the insurance company, the importer and coordinate the assessment.