4.5.4. Challenges for Vietnamese commercial banks in increasing competitive position and stabilizing banking when joining CPTPP

Firstly, the management capacity and scale of Vietnam's banking industry are still quite low compared to countries participating in CPTPP .

In 2018, the operations of Vietnamese commercial banks achieved very encouraging results but still had many weaknesses (a lot of bad debt, low management capacity, and many shortcomings in risk management at banks). Objectively, the restructuring process is still slow, reflected in the results of bad debt handling that are not substantial. Economic experts believe that in order to restructure effectively, the entire banking system must operate very healthily, transparently, and strictly comply with legal regulations, thereby creating standard banking products and services.

In addition, risk management in domestic banks still has many shortcomings. Some commercial banks have weak management capacity, violating risk management principles. The asset quality of the banking system is developing in a negative direction. Many commercial banks have low minimum capital safety ratios, some banks even lower than the rate prescribed by the State Bank of Vietnam (9%). According to estimates, the capital safety ratio of the entire banking system is only at 8.5%.

Table 4.30: Credit granting ratio of CPTPP banking system in the period 2017 - 2018

Unit: %

TT

Nation | Credit/GDP ratio (%) | Capital Adequacy Ratio (%) | |||

2017 | 2018 | 2017 | 2018 | ||

1 | Canada | 129.93 | 129.24 | 14.81 | 15.25 |

2 | Australia | 140.12 | 139.59 | 14.55 | 14.90 |

3 | Singapore | 122.72 | 121.90 | 17.08 | 16.5 |

4 | Malaysia | 118.77 | 121.79 | 17.08 | 17.70 |

5 | Japan | 107.07 | 107.89 | 16.66 | 14.22 |

6 | Vietnam | 130.72 | 133.31 | 12.23 | 11.10 |

7 | New Zealand | 144.65 | 146.55 | 14.40 | 14.80 |

8 | Mexico | 26.89 | 26.78 | 15.57 | 15.80 |

9 | Chile | 78.43 | 81.27 | 13.76 | |

10 | Peru | 42.47 | 43.97 | 15.22 | 14.70 |

Maybe you are interested!

-

Testing the credit risk tolerance of Vietnamese commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Industry and Trade - 21

Testing the credit risk tolerance of Vietnamese commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Industry and Trade - 21 -

The influence of factors belonging to bank characteristics on credit risk at Vietnamese commercial banks - 13

The influence of factors belonging to bank characteristics on credit risk at Vietnamese commercial banks - 13 -

Branch management at multinational banks: Experience of Mizuho Corporate Bank, Ltd and lessons for Vietnamese commercial banks - 17

Branch management at multinational banks: Experience of Mizuho Corporate Bank, Ltd and lessons for Vietnamese commercial banks - 17 -

Branch management at multinational banks: Experience of Mizuho Corporate Bank, Ltd and lessons for Vietnamese commercial banks - 2

Branch management at multinational banks: Experience of Mizuho Corporate Bank, Ltd and lessons for Vietnamese commercial banks - 2 -

The impact of foreign bank penetration on competition and efficiency of Vietnamese commercial banks - 21

The impact of foreign bank penetration on competition and efficiency of Vietnamese commercial banks - 21

11

Brunei | 38.81 | 34.40 | 18.11 | 18.40 |

Source: Author's statistics from Worldbank, IMF, CEIC data (2018)

Under pressure to improve competitiveness and prepare conditions to meet Basel II standards, the need for banks to increase capital is increasingly urgent. Up to 18/34 banks have announced plans to increase capital this year and have been approved by the general meeting of shareholders. Accordingly, it is estimated that the entire commercial banking system will need nearly VND63,000 billion for capital increase needs.

Second, domestic banks face the trend of increasing foreign ownership ratio in Vietnamese commercial banks. There is a risk of being dominated and acquired if they do not operate effectively .

When joining CPTPP, Vietnamese commercial banks will face a wave of acquisitions and mergers from foreign banks. Although the opening up helps domestic banks receive more capital from foreign investors, the pressure of being acquired and controlled also increases. The prospect of listed enterprises in the production and trade sector being controlled and manipulated by foreign investors may repeat itself in the banking sector.

The pressure from foreign banks is enormous, forcing domestic banks to either increase capital by any means, or pave the way for a wave of mergers and acquisitions. However, due to low competitiveness, the removal of barriers in the banking sector after the WTO commitment period has ended, increasing the number of foreign banks with strong financial potential, technology, and management skills, making the competitive pressure even more intense. This is even more likely to happen when there is still no clear solution to the problem of cross-ownership among Vietnamese commercial banks.

Third, competition is increasingly fierce, especially with the participation of foreign banks and foreign investment funds .

When Vietnam implements its commitments in CPTPP, Vietnamese commercial banks also face fierce competitive pressure: The opening up of integration will attract a large number of foreign banks with strong financial potential, technology and management skills to participate in the domestic financial market and fierce competition between domestic banks and foreign banks is inevitable.

Foreign banks with strengths in service quality and service diversity will attract a large number of customers - foreign-invested enterprises and a non-domestic part.

small domestic enterprises and individuals. This leads to an increase in the market share of foreign banks and a decrease in the market share of domestic commercial banks. In addition, it also stems from new requirements for economic restructuring and regulatory policies. Commercial banks will have to face an imbalance in the role of providing capital to the market between the commercial banking system and non-banking institutions, as well as the economic impact caused by this imbalance. The State Bank has issued legal requirements such as capital management, banking fees, foreign exchange trading, asset management and invoice trading.

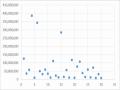

Chart 4.24: Growth rate of total assets of Vietnamese banks in 2018

6,000,000

25.00%

5,000,000

4,863,353

4,554,977

20.00%

4,000,000

19.12%

15.00%

3,000,000

10.00%

2,000,000

1,136,614

1,000,000

5.00%

-

0.00%

State-owned commercial banks, Joint-stock commercial banks, Joint-venture banks,

foreign

Absolute number

Rate of increase

6.42%

13.07%

Source: Author's calculation based on data from the State Bank of Vietnam (2018)

According to the author's synthesis based on statistics of the State Bank of Vietnam, although the total assets of the foreign banking sector at the end of 2018 only reached nearly 1,137 trillion VND, less than 1/4 of the total assets of the joint stock commercial bank sector or the state-owned commercial bank sector, the growth rate was up to 19.12%, 1.5 times higher than the joint stock commercial bank sector and 3 times higher than the state-owned commercial bank sector. Currently, Vietnam has 9 banks with 100% foreign capital. The number of foreign bank branches has also increased to 49 with the participation of Agricultural Bank of China Hanoi and Kookmin Hanoi. Meanwhile, foreign credit institutions in Vietnam are also constantly increasing their financial capacity. The most notable of these is Standard Chartered Vietnam, which increased its charter capital to nearly VND3,534 billion in early 2018, and in early 2019, this bank continued to increase its capital to VND4,215 billion.

In 2018, the State Bank also approved many foreign bank branches to increase capital, such as NongHuyp Bank Hanoi Branch increased capital to 80 million USD; Bank of China Ho Chi Minh City Branch increased capital to 100 million USD; Siam Bank Ho Chi Minh City Branch increased capital to 100.47 million USD. Increased financial capacity has created conditions for foreign credit institutions to continuously expand their operating network in Vietnam.

Not only has the breadth of foreign credit institutions in Vietnam grown, but the depth of their operations has also increased. In the past, foreign banks often only served their own enterprises operating in Vietnam, but now they are expanding to dominate segments where domestic banks have long had an advantage, such as personal consumer loans. According to banking experts, foreign banks are stepping up their operations in Vietnam to take advantage of opportunities from new-generation free trade agreements such as CPTPP or EVFTA, so the market may continue to welcome many new foreign credit institutions. Meanwhile, the fact that domestic commercial banks are focusing on restructuring, handling bad debts, and increasing capital to meet Basel II standards is also an opportunity for foreign investors to take advantage of market share.

Fourth, Legal and institutional fields in perfecting the legal framework and improving indicators according to international standards

Implementing the commitments in CPTPP, Vietnam must cut import taxes, which will reduce budget revenue, but will not have a sudden impact because in the CPTPP bloc, 7/10 countries have signed FTAs with Vietnam (only 3 countries, Canada, Mexico and Peru, have not had FTAs with Vietnam, but trade is still modest). Joining CPTPP, although there are certain limitations for opening the banking market, the conditions for market access in this field will gradually be eliminated. This can be considered a challenge for developing countries in general and Vietnam in particular. [4, p.7].

Fifth, the policy of treating, attracting and training high-quality human resources is not high compared to CPTPP member countries.

According to the results of the survey on banking industry business trends by the Department of Forecasting and Statistics, announced by the State Bank of Vietnam at the beginning of the year, the demand for human resource recruitment of commercial banks in 2018 is very large. 52.1% of credit institutions said they recruited more workers in the fourth quarter of 2017, but 25.3% still

Credit institutions believe that there is a shortage of labor needed for current job demands. With that demand, along with business expansion in 2018, 52.1% of credit institutions plan to recruit more workers in the first quarter of 2018 and 68.7% of credit institutions expect to increase the number of workers in the whole year of 2018.

When opening the financial market to foreign banks, Vietnamese commercial banks are forced to face the pressure of improving the quality and shifting high-quality financial and banking human resources to foreign and regional organizations: During the development period, the financial sector can attract a large workforce and is one of the sectors with high salaries, but during the crisis and recession, workers in the financial sector are also the most vulnerable group, facing pressure to lay off or cut salaries. Even if it is not due to a decline in business trends, a harsh labor migration cycle always takes place in the financial sector. That is, cutting low-skilled workers to replace them with high-skilled workers, which can easily lead to a brain drain of high-skilled workers in the competition process. Therefore, one of the major challenges of the Vietnamese banking system is retaining talent and avoiding the shift of high-quality human resources from Vietnam to regional countries [18]

Sixth, fierce competition with foreign banks on "retail" strategy and strategy to increase non-interest income.

Vietnamese commercial banks, like US banks in the study of Chiarozza et al. (2008), banks in emerging economies in the study of Odesanmi and Wolfe (2007), increase non-interest income will contribute to increasing banking business efficiency. In particular, banks should develop non-credit service activities. In general, profits from non-credit services contribute significantly to the total operating income of commercial banks in the current conditions of credit activities with many potential risks, investment activities and securities trading facing many difficulties. Therefore, developing non-credit services is an effective direction to change the structure of business performance of banks. Increasing the scale of equity will benefit banking operations, create competitive advantages and the ability to exploit non-interest income generating activities. On the contrary, commercial banks need solutions to manage operating costs well. In addition, the mobilized amount

Capital from customer deposits is not always low cost, due to competitive pressure forcing banks to increase the cost of mobilizing deposits and reduce lending interest rates. Therefore, Vietnamese commercial banks need to have an appropriate capital mobilization strategy to save costs and increase business efficiency. The weaknesses of Vietnamese commercial banks compared to developed countries in the CPTPP are the level of application of science and technology, management level, high-quality human resources, and service diversity. Therefore, the entry of foreign banks is a huge challenge for Vietnamese commercial banks in the race for "retail" strategy and increasing revenue from service activities.

CONCLUSION OF CHAPTER 4

In Chapter 4, the author first collects, calculates, and synthesizes data from the Vietnamese commercial banking system and macroeconomic data from 10 CPTPP member countries to assess the current performance in the period 2010 - 2018 using qualitative research methods. From there, the results of 11 countries in the CPTPP bloc are compared, as a basis for drawing appropriate policy implications in Chapter 5.

Next, chapter 4 presents the regression results obtained after implementation in chapter 3 from 31 Vietnamese commercial banks in the period 2010 - 2018 such as: descriptive statistics of variables in 3 models, correlation coefficient matrix between variables, regression estimation results using OLS, FEM, REM, GLS, 2-step GMM methods and related tests. Based on the collected results, the thesis discusses the results and compares them with the initially built hypothesis (in chapter 3).

Finally, based on the results of the actual performance of Vietnamese commercial banks compared to the remaining 10 member countries in CPTPP, the results of empirical measurements of competitiveness, stability, and the direction of impact of factors on competitiveness and banking stability, the thesis lists a number of opportunities and challenges for Vietnamese commercial banks in the context of joining CPTPP.

CHAPTER 5

CONCLUSION AND POLICY IMPLICATIONS

In chapter 5, the author concludes by summarizing the research results at Vietnamese commercial banks from the results achieved in the initial research objectives. Based on the research results, the author makes policy recommendations for bank managers in general and Vietnamese commercial banks in particular. Finally, the author presents some limitations of the topic along with further research directions.

5.1. Main research results of the thesis

Research on measuring the competitiveness and stability of Vietnamese commercial banks when participating in the CPTPP agreement. Based on a comprehensive review of theoretical frameworks related to the research content, the thesis raises controversial issues and economic viewpoints that have not been unified in previous studies. Through determining the general operating status of Vietnamese commercial banks in the context of integration, comparing Vietnamese commercial banks with the remaining member countries in the CPTPP. In addition, the thesis conducts empirical measurements on 31 Vietnamese commercial banks on competitiveness and stability in the context of participating in the CPTPP. From there, the thesis compares, synthesizes and identifies the strengths, weaknesses, opportunities and challenges that Vietnamese commercial banks will face when participating in the CPTPP. From there, through the research results, the author proposes a number of appropriate policy implications for bank administrators in general and Vietnamese commercial banks in particular to promote strengths, overcome weaknesses, promptly seize opportunities and respond to challenges when participating in CPTPP to enhance competitiveness and stabilize banking.

During the data collection process, the thesis selected and processed the data set of 31 commercial banks in Vietnam and 11 foreign banks in Vietnam during the period 2010 - 2018. With the initial descriptive statistics, the reliability and completeness of this data set was proven. Next, the thesis regressed the models and performed a series of tests, then selected the method to handle the phenomena of multicollinearity, variance variation, autocorrelation, and endogeneity to give the most accurate estimation results. These results serve well for answering the questions