Registration procedure:

- Loan application form according to VPBank's form.

- Copy of ID card/ Household registration book/ Equivalent documents.

- Copy of Decision/Labor Contract.

- Salary statement/Salary confirmation/Payroll.

2.2.1.2 Unsecured personal consumer loan process at Northern Consumer Loan Center - VPBank

To conduct unsecured personal consumer loans, each bank must comply with strict procedures because this product is highly risky. At the Northern Consumer Lending Center - VPBank, the lending process is carried out as follows:

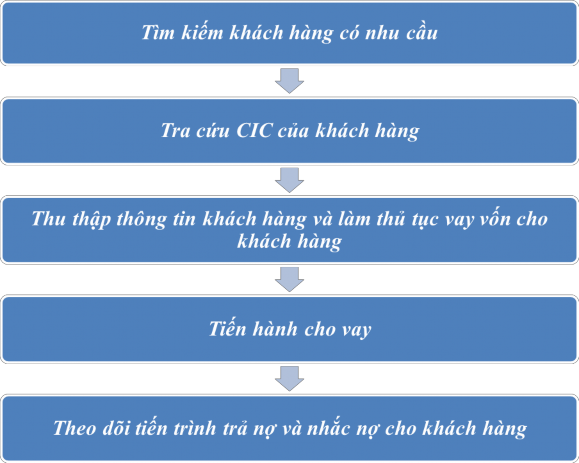

Figure 2.2: Lending process of the Northern Consumer Lending Center

(Source: VPBank Northern Consumer Lending Center 2017-2019)

Step 1: Find customers with needs

This is considered the first step in the lending process. After having a good understanding of the product, customer relations staff will search for customers in need in the market through various approaches such as calling for consultation or directly contacting potential customers or through online marketing programs. Gather a list of customers, collect some basic information such as ID card, citizen ID card, passport, household registration book, labor contract, health insurance, employee card... of customers. Preliminary check the accuracy of documents and information provided by customers, instruct customers to sign and save customer images via the phone sales app to send to the appraisal system for preliminary analysis.

Step 2: Look up customer's CIC

After having basic information of the customer, the bank staff will look up the customer's information on the national information portal. This work is to verify the customer's debt and loan situation in the recent period at credit institutions. For a customer with a bad debt relationship: debt group 2 or higher, bad debt, debt with attention in the recent period... these cases with the product regulations of VPBank's product department will not be able to borrow capital. Because when the customer has not fulfilled the loan obligations with other organizations, it is not an exception with VPBank.

Step 3: Collect customer information and process loan applications for customers

After ensuring the customer's CIC and the customer's reliable source of repayment, the bank staff will proceed with the registration procedure for the customer. In parallel with the process of collecting basic documents, the bank staff must prepare a form

The process of analyzing the customer's needs, purpose and loan term, making a preliminary assessment and submitting it to the centralized appraisal department, then the approval experts will announce a reasonable interest rate and loan limit based on the loan terms and conditions set by the product department and also based on the personal risk perspective of the approval experts.

Step 4: Proceed to loan

After the central appraisal department approves the customer's loan application, the application is sent to the operational stages to control the accuracy and compliance with the regulations set by the bank. Customer relations staff guides customers to the transaction office to complete the procedures to receive the loan as well as instruct customers on payment methods and self-monitoring of the loan.

Step 5: Track debt repayment progress and remind customers

Whether it is a simple unsecured loan or through a credit card, each bank employee must regularly monitor the customer's loan to avoid the situation of customers being late in paying their debts or jumping into debt groups, affecting the business situation of the center. At the same time, this process ensures process control and anticipates risks, if any, to come up with timely solutions.

2.2.2. Analysis of the current status of unsecured personal consumer loans quality at the Northern Consumer Lending Center - VPBank in the period 2017 - 2019

Currently, personal consumer loans without collateral are a form that brings a lot of profit to the Northern Consumer Lending Center - VPBank. Through the collected documents, the current situation of personal consumer loans without collateral is analyzed under the following criteria:

a, Scale

Number of customers

Table 2.4: Summary table of customers using non-secured consumer loan products at TTCVTDMB-VPBank in the period 2017-2019

INDICATORS

2017 | 2018 | 2019 | Difference 2018/2017 | Difference 2019/2018 | |||

Great opposite to | % | Great opposite to | % | ||||

Number of old customers | 17120 | 20160 | 32616 | 3040 | 17.8 | 12456 | 61.8 |

Number of new customers | 20160 | 32616 | 49920 | 12456 | 61.8 | 17304 | 53.1 |

Total number of customers loan | 37280 | 52776 | 82536 | 15496 | 41.6 | 29760 | 56.4 |

Maybe you are interested!

-

Consumer Loan Process at Vietnam Public Joint Stock Commercial Bank - Dong Do Branch

Consumer Loan Process at Vietnam Public Joint Stock Commercial Bank - Dong Do Branch -

Quality of Unsecured Personal Consumer Loans of Commercial Banks.

Quality of Unsecured Personal Consumer Loans of Commercial Banks. -

Current Status of Personal Loan Activities at the Transaction Office - An Binh Commercial Joint Stock Bank.

Current Status of Personal Loan Activities at the Transaction Office - An Binh Commercial Joint Stock Bank. -

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2 -

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks

(Source: VPBank Northern Consumer Lending Center 2017-2019)

Thanks to the effective business strategy of constantly increasing the number of customers as well as increasing outstanding loans from the unsecured consumer lending sector set by VPBank as well as the leaders of TTCVTDMB, in recent years the number of customers using unsecured consumer lending products at the center has increased significantly. In 2017, the total number of customers was 37,280 people, in 2018 it was 52,776 people, by 2019 this number had reached 82,536 people, an increase of 56.4% over the same period in 2018. Of which:

- The number of new customers tends to increase rapidly. If in 2018 the number of customers increased by 17.8% compared to the same period in 2017, then in 2019 the number of customers increased sharply by 61.8% due to the period from 2017 to 2018 due to the improvement of technology in the credit processing and management system using modern information technology combined with the increase in personal customer service staff and the relaxation of credit risk scoring.

-

In contrast to old customers, which decreased in the period 2017-2018 but increased sharply by 156.09% compared to the same period last year in 2019.

- The number of old customers also tends to fluctuate continuously. In 2018, the number of customers increased by 61.8% compared to the same period in 2017, then in 2019, the number of customers increased sharply by 53.1% due to the period from 2017 to 2018.

It can be seen that the majority of customers come from new customers and this proportion is constantly increasing. The characteristics of unsecured products require short loan terms, maintaining outstanding debt therefore requires increasing the number of new customers in need. This shows that credit activities at CVTDMB centers are getting better and better, attracting many customers, especially new customers using the product. However, with the rapidly increasing customer volume, this is raising the issue of better management of existing customers and exploiting the cross-selling ability from this existing customer group is very large.

Loan balance situation

- Fluctuations in outstanding value of personal consumer loans without collateral

Table 2.5: Fluctuations in outstanding personal consumer loans without collateral at the Northern Consumer Lending Center - VPBank in the period 2017-2019

(Unit: Billion VND)

Target

Year | Compare 2018/2017 | Compare 2019/2018 | |||||

2017 | 2018 | 2019 | Absolute | Soy sauce opposite to (%) | Absolute | Soy sauce opposite to (%) | |

Consumer loans no TSDB | 1896 | 2112 | 3069 | 216 | 11.39 | 957 | 45.31 |

Credit card | 384 | 411 | 635 | 27 | 7.03 | 224 | 54.5 |

Total outstanding debt loan from center | 2280 | 2532 | 3704 | 252 | 10.66 | 1172 | 46.3 |

Proportion (%) (Non-secured loans/total outstanding loans of center) | 83.2 | 83.4 | 82.9 | - | |||

(Source: VPBank Northern Consumer Lending Center 2017-2019)

Comment:

In the period 2017-2019, the total outstanding balance of non-secured personal consumer loans of CVTDMB Center - VPBank increased significantly. In 2017, the outstanding loan value was 1,896 billion VND, by 2019 this figure had reached 3,069 billion VND, increasing sharply in 2019 with a growth rate of 45.31%, equivalent to an increase of 957 billion VND compared to the previous year. Part of the reason is that in 2019, TTCVTDMB began to loosen the criteria for assessing debt repayment ability, increased consumer lending products such as additional unsecured loans for customers who are mortgaging houses and apartments, added a group of customers with cash salaries who pay social insurance who can also borrow and expanded the sales area to provinces such as Lang Son, Ha Nam, expanded the sales exploitation area to a radius of 50km from VPBank transaction offices instead of a radius of 30km from VPBank transaction offices as before.

In addition, the outstanding loans of TTCVTDMB from credit cards also account for a modest proportion but are growing strongly. This is an important indicator that needs to be promoted to grow more, because the characteristics of this market, although it does not bring immediate profits like non-secured consumer loans, it also brings a significant proportion of profits in the future and the risk index of this market is much lower than non-secured consumer loans. Although the value is not large, the growth rate of this product is very encouraging. In 2018, the growth rate of this indicator was 7.03%, but in 2019, the growth rate was 54.5%. The reason is that in 2019, VPBank's unsecured product department added a credit card product for customers who received loan disbursements. This is a product that initially has no card limit and when the customer repays the bank, the principal will be transferred to the credit card limit with this loan, which causes the outstanding balance of the credit card to increase significantly.

The ratio of outstanding personal consumer loans without collateral to the total outstanding loans of the entire center is almost unchanged.

Strong lending without collateral attracts customers, leading to a gradual increase in outstanding loans. In 2017-2019, the proportion of personal consumer loans without collateral was 83.2%, 83.4% and 82.9% respectively. With the increase in loan forms, stimulating the demand for loans for customers in recent years, VPBank has loosened lending conditions. The consequence of this problem is an increase in outstanding loans, however, the rapid increase in outstanding personal consumer loans without collateral contains many risks for lending activities at VPBank in the coming time.

- Term of personal consumer loan without collateral.

Table 2.6: Outstanding unsecured personal consumer loans over time

(Unit: Billion VND)

Target

2017 | 2018 | 2019 | ||||

Outstanding debt | % | Outstanding debt | % | Outstanding debt | % | |

Short term | 1,317 | 69.53 | 1,587 | 75.18 | 2256 | 73.5 |

Medium and long term | 579 | 30.47 | 525 | 24.82 | 813 | 26.5 |

Outstanding consumer loans individuals without fixed assets | 1896 | 100 | 2112 | 100 | 3069 | 100 |

(Source: VPBank Northern Consumer Lending Center 2017-2019)

Comment:

In the period 2017-2019, the amount of outstanding personal consumer loans without collateral increased significantly. In 2019, this figure was 3,069 billion VND, an increase of 957 billion VND compared to the same period last year. Due to the nature of the product with high risk, most of the lending period is short-term. The ratio of short-term/medium and long-term loans in 2017 was 69.53%/30.47%, but by 2019, there was a slight shift, which was an increase in short-term loans and a decrease in medium and long-term loans. With the goal of minimizing loan risks to avoid bad debt in the future, the center director has instructed the staff to prioritize short-term loans, and cooperated with Global Insurance Joint Stock Company.