PVcomBank- Dong Do Branch has deployed a number of consumer lending products such as: CVTD with collateral, savings book mortgage loans, auto loans, unsecured consumer loans, loans through credit card issuance... However, CVTD products of PVcomBank - Dong Do Branch only focus on outstanding loans mainly on a number of main products such as unsecured consumer loans, home loans, home repair and mortgage consumer loans...

+ Consumer loan products with collateral

PVcomBank will consider granting credit to customers for the purpose of paying for the consumer needs of the customer himself or/and his/her relatives, in accordance with the provisions of law such as:

- Purchase of household items, appliances, equipment, and furniture;

- Payment of domestic study costs;

- Wedding/travel/scientific research/medical expenses;

- Pay property registration fees/taxes;

- Other essential needs for personal life (if any).

+ Car loan products:

2.2.2. Consumer lending process at Vietnam Public Joint Stock Commercial Bank - Dong Do Branch

The KHCN lending process is issued on the procedures for handling steps in the process of granting credit to an individual customer to ensure consistency throughout the banking system and comply with legal regulations.

The CVTD process at PVcomBank - Dong Do Branch basically includes the following steps:

B1. Search and receive loan needs and guide customers to prepare loan applications.

B2. Loan appraisal and reporting

B3. Loan approval & decision

B4. Draft and sign contract & Complete loan procedures

B5. Disbursement

B6. Post-loan inspection

B7. Debt collection, loan settlement

Step 1 : Contact and receive credit documents : CV QHKH searches for and consults customers/customers who need to borrow capital to go to the bank to apply for a loan. Here, CV QHKH guides customers to complete a complete and correct application. Loan applications usually include:

Loan application: guide customers to follow the bank's prescribed form.

Legal documents: household registration, identity card of individuals, households and other documents as prescribed

Loan security documents (if the loan is secured by assets): are carried out according to the regulations and procedures for receiving security of PVcomBank.

CV QHKH is responsible for guiding customers to provide the above documents according to regulations.

Step 2 : Loan appraisal and report preparation : This is an important step in the loan appraisal process, determining credit quality. If the loan appraisal is incorrect, the loan appraisal will lead to the wrong decision. The appraisal process includes:

- Appraisal of customer information: age, civil legal capacity, civil conduct capacity, social relations, qualifications, personal background of the borrower and those directly related to the loan

- Assessing the customer's financial capacity: assessing the customer's income and assets to know the customer's ability to repay the debt.

- Assessing loan and repayment purposes: comparing customer's income with loan application to assess debt repayment ability.

- Appraisal of collateral: If the loan is secured by collateral (car, land use rights, house ownership rights, etc.), the bank needs to appraise the legality of the collateral and its value.

After completing the loan appraisal, the Customer Service Officer will score the customer and prepare a credit report according to regulations. After the appraisal, if the customer does not meet the loan conditions, the credit officer must immediately notify the customer of the appraisal results.

Step 3 : Review and decide on loan : After the appraisal process, the Customer Service Department will prepare an appraisal report and submit it to the superior for approval, make a loan decision and notify the customer of the content.

At PVcomBank - Dong Do Branch, the branch director is authorized to approve and make lending decisions for loans worth up to 3 billion VND and there are no exceptions regarding loan applications. The remaining cases must be transferred to the Approval Specialist/Credit Council/Credit Committee at the Head Office for loan approval.

Step 4 : Draft, sign contract and complete loan procedures

After reviewing and deciding to grant a loan, the QHKH CV is responsible for completing and supplementing any missing documents according to regulations. Then, the QHKH CV coordinates with the customer to complete the procedures and sign the credit contract, guarantee contract and other related documents.

Step 5 : Disbursement :

After completing the procedures and signing, notarization, authentication, and receiving collateral according to regulations, the file is transferred to the credit control department of the Branch/Headquarters depending on the limit for review and disbursement to the customer.

Step 6 : Check after loan :

After disbursement, the loan officer must check whether the customer uses the capital for the right purpose or not and periodically check the customer's financial capacity to ensure loan quality and debt collection to limit risks for the bank.

Step 7 : Debt collection, loan settlement:

Periodically, the Customer Service Department will remind the customer to collect principal and interest monthly. The contract will be liquidated when the customer completes the debt repayment obligation to the Bank.

2.2.3 Consumer lending results at Vietnam Public Joint Stock Commercial Bank - Dong Do Branch

Table 2.5. Consumer lending results at PVcomBank Dong Do branch from 2018 to 2021

Unit: billion VND

Year

Target

2018 | 2019 | 2020 | 2021 | Comparison 2019/2018 | Comparison 2020/2019 | Comparison 2021/2020 | ||||

Absolute | Relative (%) | Absolute | Relative (%) | Absolute | Relative (%) | |||||

Total outstanding loan balance | 305.22 | 338.13 | 371.52 | 399.69 | 32.91 | 10.78 | 33.39 | 9.87 | 28.17 | 7.58 |

CVTD bad debt ratio | 1.70 | 1.75 | 1.84 | 2.04 | 0.05 | 3.08 | 0.09 | 5.33 | 0.19 | 10.55 |

Profit from CVTD | 2.88 | 3.14 | 3.46 | 3.78 | 0.26 | 9.03 | 0.32 | 10.19 | 0.32 | 9.25 |

Maybe you are interested!

-

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2 -

Consumer lending quality at Vietnam Prosperity Joint Stock Commercial Bank - Northern Consumer Lending Center - 10

Consumer lending quality at Vietnam Prosperity Joint Stock Commercial Bank - Northern Consumer Lending Center - 10 -

Evaluation of consumer lending quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hue Branch - 5

Evaluation of consumer lending quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hue Branch - 5 -

Improving credit quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam in the integration process - 30

Improving credit quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam in the integration process - 30 -

Unsecured Personal Consumer Loan Process at Northern Consumer Loan Center - Vpbank

Unsecured Personal Consumer Loan Process at Northern Consumer Loan Center - Vpbank

(Source: PVcomBank Dong Do branch business performance report 2018-2021)

Firstly, in terms of outstanding consumer loans , compared to the set plan, the branch's consumer loan plan completion rate tends to increase. In 2018, the consumer loan ratio exceeded the set plan by 5.25%, in 2019 this ratio was 6.29%. Due to the impact of the Covid-19 epidemic, in 2020 the branch only achieved 92.88% of the set consumer loan plan and in 2021 the branch completed 88.82% of the plan. Total outstanding CVTD in 2018 reached 305.22 billion VND and grew steadily over the years until 2021, reaching an outstanding balance of 399.69 billion VND, an increase of 30% compared to 2018.

Second, regarding the bad debt ratio , in general, the bad debt ratio of Dong Do branch over the years tends to increase and is quite high compared to other banks. In 2018, the bad debt ratio was only 1.70%, but by 2019, the figure had increased to 1.75%, in 2020, this ratio was 1.84% and by 2021, this figure had reached 2.04%. The reason why the bad debt ratio in 2020 and 2021 is so high is due to the impact of the Covid-19 epidemic, causing the economy to stagnate, businesses and individuals to make losses and have no way to make ends meet.

debt repayment capacity. However, according to the assessment, PVcomBank has promptly restructured the repayment period of principal and interest and reduced interest rates for businesses and individuals affected by the pandemic, while also setting up risk provisions. Therefore, the bad debt settlement work basically met the set plan.

Third, in terms of profit from consumer lending activities, profit from consumer lending activities has grown steadily over the years from 2018 to 2021. In 2019, profit from CVTD activities reached VND 3.14 billion, an increase of 9.03% compared to 2018. In 2020, profit reached VND 3.46 billion, an increase of 10.19% compared to 2019. By 2021, CVTD profit reached VND 3.78 billion, an increase of 9.25% compared to 2020.

Fourth letter on the quality of consumer lending services

- Mostly good reviews about service attitude, transaction space and procedures

- Most people rate interest rate issues as quite good.

- Average rating on processing time and quality of support and consultation.

2.3. Current status of consumer lending development at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Do Branch in the period from 2018 to 2021

2.3.1. Current status of consumer lending development at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Do branch reflected by quantitative indicators

Among the lending activities of PVcomBank – Dong Do Branch, consumer lending contributes an important part to the average outstanding loan balance of the branch. Realizing that this is one of the business activities that brings high profits, the branch has constantly strived to expand its scale and improve the quality of CVTD.

On the scale of consumer lending

Table 2.6. Consumer lending scale at PVcomBank Dong Do branch from 2018 to 2021

Unit: billion VND

Year

Target

2018 | 2019 | 2020 | 2021 | Comparison 2019/2018 | Comparison 2020/2019 | Comparison 2021/2020 | ||||

Amount | % | Amount | % | Amount | % | |||||

Loan turnover | 536.41 | 567.54 | 604.64 | 631.34 | 31.13 | 5.80 | 37.1 | 6.54 | 26.7 | 4.42 |

Debt collection turnover | 440.97 | 461.16 | 483.11 | 497.72 | 20.19 | 4.58 | 21.95 | 4.76 | 14.61 | 3.02 |

Total outstanding loan balance | 305.22 | 338.13 | 371.52 | 399.69 | 32.91 | 10.78 | 33.39 | 9.87 | 28.17 | 7.58 |

(Source: PVcomBank Dong Do branch business performance report 2018-2021)

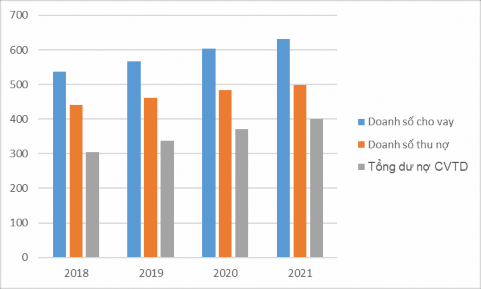

Chart 2.5. Consumer lending scale at PVcomBank - Dong Do Branch from 2018 to 2021

Unit: billion VND

(Source: Summary of credit activities of PVcomBank - Dong Do Branch)

Through the chart above, it can be seen that the scale of CVTD activities of PVcomBank - Dong Do Branch is increasing. Total CVTD turnover in 2018 reached 536.41 billion VND, by 2019 it reached 567.54 billion VND (up 5.80% compared to 2018), in 2020 the total turnover reached 604.64 billion VND, up 6.54% compared to 2019. In which, outstanding consumer loans in 2021 reached 631.34 billion VND, up 4.32% compared to 2020. Such results are due to the branch's efforts in marketing and communication to attract more customers to borrow for consumption, issuing a variety of products to meet customers' needs, and the branch also focuses on and improves service quality.

In addition, the branch has also paid more attention to post-loan control and debt collection. Debt collection turnover in 2019 reached 461.16 billion VND, an increase of 4.58% compared to 2018. In 2020, CVTD debt collection turnover reached 483.11 billion VND, an increase of 4.76% compared to 2019. By 2021, debt collection turnover reached 497.72 billion VND, an increase of 3.02% compared to 2020. Of which, the outstanding balance at the end of the period in 2021 reached

399.69 billion VND.

On the growth rate of outstanding consumer loans

To better understand the development of CVTD activities at PVComBank - Dong Do Branch, we will analyze CVTD outstanding balance over the years. The higher the outstanding balance, the stronger the development of CVTD activities and the higher the reputation of the bank.

Table 2.7. Proportion of outstanding CVTD debt at PVcomBank - Dong Do Branch from 2018 to 2021

Unit: billion VND

Year

Target

2018 | 2019 | 2020 | 2021 | Comparison 2019/2018 | Comparison 2020/2019 | Comparison 2021/2020 | ||||

Amount | % | Amount | % | Value | % | |||||

Total outstanding debt | 1,307.67 | 1,449.65 | 1,531.10 | 1,597.02 | 141.98 | 10.86 | 81.45 | 5.62 | 65.92 | 4.31 |

Total outstanding loan balance | 305.22 | 340.13 | 371.52 | 399.69 | 34.91 | 11.44 | 31.39 | 9.23 | 28.17 | 7.58 |

Proportion (%) | 23.34 | 23.46 | 24.26 | 25.03 | ||||||

(Source: PVcomBank Business Development Department)

From Table 2.7, we can see that, in general, the total outstanding loans and outstanding CVTD at PVcomBank - Dong Do Branch have grown steadily every year, with outstanding CVTD accounting for a significant portion of the total outstanding loans. Total outstanding CVTD in 2019 reached VND 340.13 billion, an increase of 11.14% compared to 2018 (reaching VND 305.22 billion), reaching VND 371.52 billion in 2020, and VND 399.69 billion in 2021. The reason for such growth is that in the period 2018 - 2021, PVcomBank - Dong Do Branch adjusted policies on interest rates and developed a variety of CVTD products to promptly meet all customer needs and optimize loan application processing time, adding many incentive programs to reduce or waive penalties for early repayment.

Outstanding loans from commercial banks are increasingly accounting for a larger proportion and contributing a significant part to total outstanding loans. Specifically, in 2019 compared to 2018, the proportion of outstanding loans from commercial banks increased by 0.12%, total outstanding loans from commercial banks in 2020 accounted for 24.26% of total outstanding loans, in 2021 outstanding loans from commercial banks accounted for 25.03% of total outstanding loans.

Consumer lending is growing and contributing significantly to the branch's business performance. Recognizing the importance of consumer lending activities, the branch's management has continuously improved service quality and trained customer service staff to promote consumer lending activities.

We can compare the development of CVTD among some branches in Hanoi to see more clearly the growth rate of CVTD outstanding loans of PVcomBank - Dong Do Branch.

Table 2.8. Outstanding CVTD debt at some branches of PVcomBank from 2018 to 2021

Unit: billion VND

Target

Branch

2018 | 2019 | 2020 | 2021 | Comparison 2019/2018 | Comparison 2020/2019 | Compare 2021/2020 | ||||

Amount | % | Amount | % | Amount | % | |||||

PVcomBank Dong Do | 305.22 | 340.13 | 371.52 | 399.69 | 34.91 | 11.44 | 31.39 | 9.23 | 28.17 | 7.58 |

PVcomBank Dong Da | 290.14 | 306.75 | 335.28 | 361.95 | 16.61 | 5.72 | 28.53 | 9.30 | 26.67 | 7.95 |

PVcomBank Hai Ba Trung | 299.8 | 331.37 | 365.36 | 389.17 | 31.57 | 10.53 | 33.99 | 10.26 | 23.81 | 6.52 |

(Source: PVcomBank Business Development Department)