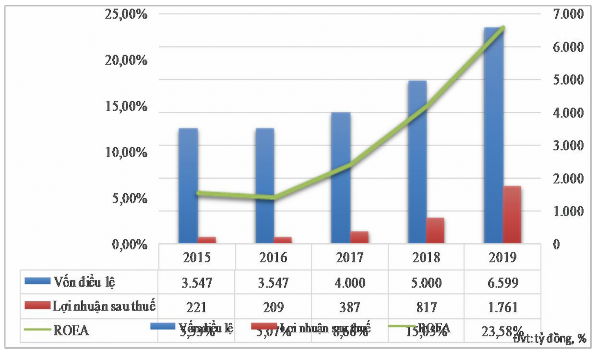

Chart 2.1 Performance of Vietinbank Vinh Long in the period 2015 - 2019

(Source: Annual report of Vietinbank Vinh Long for the period 2015 - 2019)

2.2 Signs of recognition, manifestation and problem identification.

Overall, the credit situation at Vietinbank Vinh Long is showing signs of decline, as the credit growth rate over the years from 2015 to 2019 is gradually decreasing over time. Meanwhile, credit risks are increasing, as bad debt is also increasing rapidly. Even faster than credit growth. All are reflected in the following credit risk assessment criteria: Table 2. 2Some credit risk warning indicators at Vietinbank Vinh Long

STT

ONLY PEPPER | 2015 | 2016 | 2017 | 2018 | 2019 | |

1 | Total balance loan debt | 21,159 | 27,694 | 38,507 | 48,183 | 56,316 |

2 | Overdue limit | 933.0 | 914.9 | 894.3 | 596.0 | 865.1 |

3 | Bad debt | 531.1 | 641.7 | 675.7 | 865.0 | 1.288.1 |

Maybe you are interested!

-

Assessment of Credit Risk Management Status According to Basel II Standards at Vietinbank Vinh Long

Assessment of Credit Risk Management Status According to Basel II Standards at Vietinbank Vinh Long -

Model of the Impact of Credit Risk on the Business Performance of Commercial Banks

Model of the Impact of Credit Risk on the Business Performance of Commercial Banks -

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang -

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016:

Current Status of Factors Affecting Credit Risk at Vietnamese Commercial Banks in the Period 2008 - 2016: -

The impact of credit risk on business performance of Vietnamese commercial banks - 1

The impact of credit risk on business performance of Vietnamese commercial banks - 1

STT

INDICATORS | 2015 | 2016 | 2017 | 2018 | 2019 | |

4 | Residual rate overdue debt | 4.4% | 3.3% | 2.3% | 1.2% | 1.5% |

5 | Debt ratio bad | 3% | 2.3% | 1.54 | 1.48 | 1 |

6 | Efficiency capital utilization (H1) | 88.5% | 93.8% | 89.4% | 90.6% | 93.3% |

7 | Performance capital (H2) | 54.1% | 56% | 60.3% | 57.2% | 56.3% |

8 | Provisions preventive | 304.4 | 241.5 | 331.7 | 404.1 | 565.3 |

(Source: Vietinbank Vinh Long Business Activity Report)

Comment:

Credit risk warning indicators at Vietinbank Vinh Long:

- The total outstanding loans of the Bank over the years from 2015 - 2019 increased by an average of 30%. Showing that credit lending activities with risks in credit activities are inevitable.

- Overdue debt is a sign of financial weakness of customers but this is a warning sign of credit risk for banks. From 2015 - 2018, the ratio of overdue debt of banks tended to decrease from 4% to nearly 1%, but from 2018 - 2019, this ratio returned to 1.5%, showing that banks need to pay attention to credit activities.

- Regarding bad debt index, the bank is still maintaining at 2% over the years from 2015 - 2019.

- Regarding capital utilization efficiency (H1): this is an indicator showing the correlation between mobilized capital and total outstanding loans. In general, the indicator

The closer this ratio is to 100%, the more it proves that the bank is using its capital effectively if the bank mobilizes capital itself, and over the years, from 2015 to 2019, it increased from 88.5% to 93.3%. But when analyzed in two directions:

First: The demand for loans is very large but the bank's ability to mobilize capital is poor, leading to banks having to borrow for use, potentially posing credit risks.

Second: The demand for loans is very low but the bank's capital is abundant, the bank must find ways to lend even though customers do not meet the loan conditions, leading to credit risk.

- Regarding the capital efficiency index (H2): this index is considered perfect when it fluctuates around 70% - 80%, but here the bank is only from 54.1% - 56.3% from 2015 - 2019. The bank has not used this capital source effectively, so the bank must have a management strategy.

- Regarding the bank's provisioning, it is still implementing it in accordance with the regulations of the State Bank and the Head Office is still above the prescribed level. These things together show that the fact that customers do not meet the conditions still exist, leading to risks and the bank needs to pay attention and have measures to manage the provision.

Vietinbank Vinh Long is implementing operational risk management tools and methods to meet Basel II standards to identify, assess, monitor and report operational risk events.

The branch conducts internal credit ratings but they are still inaccurate, do not reflect the reality of customers, and do not measure the level of potential risks, so they do not have a warning effect.

The Branch's focus on excessive risks, classification of problem loans, estimation of additional provisions and the impact on the bank's profitability have not yet been implemented in practice.

In addition, Vietinbank Vinh Long is prioritizing the strategy of advanced approach, improving the quality and availability of data. At the same time, deploying integrated risk management solutions.

Thus, when approaching Basel II standards in credit risk management, Vietinbank Vinh Long will optimize its profits through business strategies based on risk levels and reasonable capital allocation for each customer and product. It helps the bank establish a credit investment portfolio with optimal profit levels. In this way, when transacting, both customers and banks will be more secure when their assets are protected against risks that may arise.

In recent years, Vietinbank Vinh Long has taken positive measures in credit risk management. However, there are still shortcomings such as overdue debt ratio, bad debt ratio, and especially off-balance sheet bad debt. The bank's credit risk management is extremely difficult and the forecasting of risks has not yet met the requirements. The main causes of these shortcomings arise from the bank's credit risk management. Therefore, in the coming time, Vietinbank Vinh Long needs to strengthen its credit risk management activities in a more appropriate and effective manner, in order to better solve the problems that the bank encounters and must face in the period of market economy integration.

CONCLUSION OF CHAPTER II

This chapter presents an overview of the organization and business performance of Vietinbank Vinh Long in the period of 2015-2019. In addition, the author also points out warning signs, manifestations of problems and identifies issues that need to be studied in the work of credit risk management according to Basel II standards.

CHAPTER 3: THEORETICAL BASIS AND RESEARCH METHODOLOGY

3.1 Theoretical basis of credit risk

3.1.1 Concept of credit risk

Credit risk as defined by Basel (2010) and Rose (2002) is the possibility that a bank will lose part or all of its loan due to risks that threaten the solvency of its customers. These unwanted risks include customer bankruptcy or intentional non-payment of customer debts.

State Bank of Vietnam, 2013. Circular 02/2013/TT-NHNN regulating the classification of assets, the level of provisioning, the method of setting up risk provisions and the use of provisions to handle risks in the operations of credit institutions and foreign bank branches, Hanoi, dated January 21, 2013, stated that "credit risk in banking activities is the loss that may occur to the debt of a credit institution or foreign bank branch due to the customer's failure or inability to perform part or all of his/her obligations as committed".

In short, RRTD is the potential loss that can occur during the credit granting process of the bank, due to the borrower not repaying or not repaying the debt on time to the bank as committed in the contract. This can be a risk associated with credit activities and cause financial loss such as reduced net income, reduced market value of capital.

3.1.2 Causes of credit risk

3.1.2.1 Objective causes

Due to changes in government policies : changes in legal institutions, political instability... can threaten the survival and development of any industry. In addition to central laws, businesses must also comply with regional laws, for companies operating internationally these factors will become very complicated. They must analyze the stability of the political system, know the local laws that affect the industry as well as the business. Furda (2014) said that

Macro factors such as inflation, unemployment, and GDP growth rate also affect bank credit risk.

From the legal environment: Wang (2013) believes that the causes of default of loan customers are from the lack of uniform legal policies, from weaknesses in business leading to bank credit risks... Once the socio-economic situation is unstable, leading to difficulties in the customer's business, the customer (borrower) cannot repay the debt to the bank.

Natural environment : changes in weather, climate, natural disasters, etc. can also affect the production and business activities of borrowers, and these impacts are unpredictable factors, occur unexpectedly and often cause great damage. Therefore, when affected by the natural environment, customers will suffer heavy losses, have no source of income, etc. Therefore, lending banks must share the risk with their customers (Wang, 2013)

Socio-economic environment: in a country when the socio-economic environment fluctuates, it is influenced by the world economy. That is also one of the causes of risks in the business activities of the economy in general and the business activities of banks in particular. In addition, changes in international relations and diplomatic relations of the government are also causes of great risks for the business activities of banks (Wang, 2013).

Borrower's weakness: in business, the borrower's business ethics is also a factor leading to the risk of causing loss to the bank. If the bank detects early, the risk will be prevented. This is confirmed in the study of (Wang, 2013).

3.1.2.2 Subjective causes from the Bank.

Bank credit risk is also caused by internal factors of the bank. A typical example of internal factors of the bank is the ethics and professional qualifications of bank employees. Bank employees lack responsibility and poor qualifications, leading to lending to businesses and individuals who are not eligible for loans, such as: ineffective business operations,

Problematic business production plans... (Wang, 2013). In the study of Berger and De Young (1997), it was said that the increase in bad debt was due to the weak pre-, during- and post-loan appraisal process of the bank, leading to the selection of the wrong customers for lending. Or because the bank staff did not have enough capacity to make wrong or incorrect assessments of the value of collateral and the value of mortgaged assets.

3.1.3 Consequences of credit risk

For the economy : Banking business activities are systemic and closely related to many entities in the entire economy, so credit risks can have consequences for the national financial system.

Credit activities are based on the principle of borrowing to lend, so if depositors lose confidence in the bank, they will withdraw money en masse, creating a psychological effect of withdrawing money from other banks, which can cause the banking system to collapse completely.

Credit risks can make banks hesitant in mobilizing and supplying capital to the economy, causing production to stagnate, economic growth to slow down, prices to increase, purchasing power to decrease, unemployment to increase, social instability, and quality of life to decline.

For banks : When facing credit risks, banks cannot collect the principal and interest on loans but still have to pay the principal and interest on mobilized capital due, which causes the bank to fall into a state of imbalance between revenue and expenditure and liquidity risk.

Increased costs due to the need to set aside credit risk provisions, leading to a decline in business results. If the risk occurs at a small level, the bank can compensate with risk provisions (recorded in expenses) and with its own capital: if the risk occurs on a large scale and for a long time, the bank may fall into a state of insolvency and bankruptcy.

The serious consequences that can be caused by credit risks force banks to always pay attention to preventing and limiting credit risks, emphasizing steps such as establishing credit policies and procedures, and organizational models.

credit management, credit risk management process.

For customers : For customers themselves who are unable to repay the principal (interest) to the bank when due, leading to overdue or bad debt, that information is recorded at CIC - the National Credit Center under the State Bank - leading to their inability to access capital sources at other commercial banks. In addition, the opportunity to access bank capital for other borrowers is also more limited when credit risks force commercial banks to either tighten lending or reduce the scale of operations. Subjects who deposit money in banks are at risk of not being able to recover their deposits and interest when banks go bankrupt or have systemic risks.

3.1.4 System of factors affecting credit risk

GDP factor : high GDP growth means the economy is growing, expanding whereas low GDP growth means the economy is in recession. GDP is negatively correlated with bank credit risk ( Louzis et al., 2012). During economic expansion, consumers can generate enough income or cash flow so that borrowers have enough money to repay their debts. During economic recession, household and personal income will decrease, so the ability of consumers to secure debts has decreased. Therefore, bank credit risk will increase.

Interest Rate Factor : According to Kaplin (2009) empirical studies demonstrate a positive relationship between interest rates and credit risk. An increase in interest rates will increase the cost of debt, and thus reduce the borrowing capacity to serve their current needs, thus, it leads to higher credit risk in banking services.

Exchange rate factors : Chaibi and Ftiti (2014) argue that empirical studies have found that an increase in exchange rate can affect external competitiveness. Exchange rate has a positive relationship with non-performing loans (NPLs) in France because monetary policy has made products more expensive, weakening the competitiveness of firms that are mainly manufacturing and trading and unable to repay their debts. However, research in Germany shows a negative relationship with NPLs due to exchange rate