professional ethics of staff and employees as well as the shortcomings that still exist in the bank's salary and bonus mechanism. However, on the other hand, it also shows Vietinbank's ability to identify and control relatively effectively the signs of risks arising from fraud and internal crimes, to minimize to the lowest possible level the actual risk events occurring due to this group of signs.

The group of risk signs related to mechanisms, policies and regulations is decreasing, in 2019 there were only 138 signs, equal to 42% compared to 2015. This proves that Vietinbank has continuously improved its system of internal documents, policies and procedures to limit the signs of related risks.

Based on the probability of occurrence of risk signs

Table 2.6. Probability of risk signs appearing at Vietinbank from 2015-2019

Unit: %

STT

Type of risk sign | 2015 | 2016 | 2017 | 2018 | 2019 | |

1 | Organizational model, staff and workplace safety | 0.05 | 0.047 | 0.032 | 0.028 | 0.017 |

2 | Mechanisms, policies, regulations | 0.021 | 0.029 | 0.023 | 0.016 | 0.009 |

3 | Fraud and external crime | 0.0027 | 0.0038 | 0.0025 | 0.0018 | 0.0012 |

4 | Fraud and internal crime | 0.0014 | 0.0016 | 0.0013 | 0.0009 | 0.0007 |

5 | Workflow | 0.067 | 0.066 | 0.054 | 0.049 | 0.038 |

6 | Information technology | 0.0027 | 0.0026 | 0.0018 | 0.0015 | 0.0016 |

Maybe you are interested!

-

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12 -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13 -

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12 -

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1 -

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32

(Source: [39])

The probability of occurrence of risk signs is calculated as a percentage of the number of SKRRs arising over the number of transactions performed by the entire Bank. This indicator is calculated for each type of risk sign.

The probability of occurrence of risk signs belonging to the six risk groups presented above at Vietinbank all tended to decrease in the period from 2015 to 2019. In particular, the probability of occurrence of the risk group related to mechanisms, policies and regulations was the lowest at 0.009% in 2019. The rate of decrease in the probability of occurrence of the risk group related to organizational model, staff and workplace safety

Vietinbank's work is the highest, in 2019 the probability of this group of risk signs appearing is only 34% compared to 2015.

The above figures demonstrate that Vietinbank's risk management work has helped reduce many errors and risk events, initially bringing positive results, especially in monitoring suspicious and unusual transactions.

Based on the number of incidents occurring during the period

The number of SKRRs occurring at Vietinbank according to each typical risk group has continuously decreased over the years in the period from 2015 to 2019. In 2019, the total number of SKRRs occurring was 74,403 events, down 35.4% compared to 2018 and down more than 73% compared to 2015. The average rate of reduction of SKRRs at Vietinbank in the period 2015-2019 reached more than 14%/year.

Table 2.7. Number of SKRRTN arising in the period from 2015-2019

Unit: SKRRTN

STT

Type of risk | 2015 | 2016 | 2017 | 2018 | 2019 | |

1 | Organizational model, staff and workplace safety | 3,963 | 3,327 | 2,698 | 2,398 | 2.141 |

2 | Mechanisms, policies, regulations | 287 | 137 | 87 | 28 | 16 |

3 | Fraud and external crime | 16,169 | 17,953 | 12,047 | 12,719 | 11,395 |

4 | Fraud and internal crime | 14,134 | 12,356 | 11,865 | 9,378 | 7,367 |

5 | Workflow | 239,512 | 174,797 | 118,165 | 89,154 | 52,157 |

6 | Information technology | 2.015 | 1,854 | 1,580 | 1,508 | 1,327 |

Total | 276,080 | 210,424 | 146,442 | 115,185 | 74,403 | |

(Source: [39])

Of which, the number of SKRR related to work processing in 2015 accounted for the largest number of 239,512 SKRR, but by 2019, this number had decreased significantly but was still at a high level, at 52,157 errors. The number of errors related to Vietinbank's mechanisms, policies, and regulations had the largest decrease rate, nearly 19%/year with the number of 16 errors in 2019 compared to 287 errors in 2015.

SKRR arising from fraud and internal crimes tends to decrease, but is still at a high level, accounting for 9.9% of the total amount of SKRR arising in 2019, compared to this figure of 5.12% in 2015. SKRR arising from fraud and internal crimes

Internal breaches have the potential to cause huge losses to banks both financially and in terms of reputation. The requirement for banks is to have measures to limit and overcome the losses caused by this type of risk.

Although the SKRR due to fraud and external crimes of Vietinbank has decreased over the years, the absolute number is still relatively high, especially the increasingly diverse and sophisticated nature. Partly because the number of transactions with customers has increased over the years with an average growth rate of 23%/year, partly because of lax management of the bank, overloaded transaction officers and the increasing sophistication of external crimes leading to difficulties for the bank in identifying and preventing risks.

The remaining risk groups are all at acceptable levels, based on the probability of occurrence of risk signals and the number of risk signals detected.

Based on the total loss (in money) that occurred during the reporting period

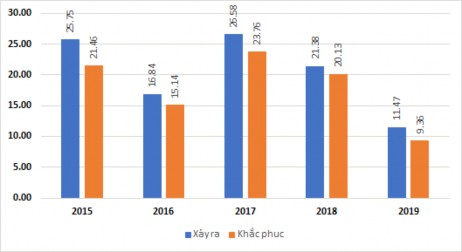

According to the total loss index in cash, in the period from 2015 to 2019, Vietinbank recorded a loss of more than 102 billion VND, of which the recoverable loss value was 89.8 billion VND and the unrecoverable amount was 12.16 billion VND. The average loss value of Vietinbank in the period from 2015 to 2019 caused by SKRRTN was more than 2.4 billion VND.

Chart 2.5. Vietinbank's loss recovery results from 2015-2019

Unit: billion VND

(Source: [39])

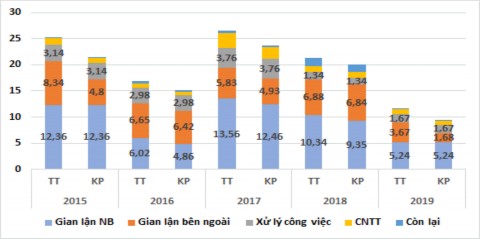

Vietinbank's loss value in 2019 reached VND 2.1 billion, only 49.3% of that in 2015. Of the total loss value that occurred at Vietinbank during this period, the largest proportion of losses belonged to the group of internal fraud risks, followed by risks due to fraud and external crimes with average figures of 45.94% and 31.72% of the loss value, respectively. With only a few cases related to fraud and internal crimes, the loss value caused to the bank has reached hundreds of millions or billions of VND.

In addition, the loss caused to banks by external criminal activities, although decreasing over the years, is still high. Only in 2019 did this loss decrease significantly, at 31.99% of the total loss value caused by operational risks, with an absolute number of 3.67 billion VND, of which the value of the recovered loss was 1.68 billion VND. Of which, the largest loss caused by this type of risk comes from bad guys forging stamps, signatures, and documents in order to appropriate money and assets of customers and banks (accounting for 94% of the loss value caused by fraud and external crimes).

Chart 2.6. Losses by risk group of Vietinbank from 2015-2019

Unit: billion VND

(Source: [39])

It can be seen that losses caused by risk groups related to organizational models, staff and workplace safety and risks related to processes and regulations always account for a low proportion of the total value of operational risk losses caused to banks, at less than 1%, and in 2018 alone, this number increased dramatically to 7.7%.

with an absolute amount of up to 1.65 billion VND in loss value and 1.46 billion VND in recovered loss value. The reason is that this year a series of ATMs and other tangible assets were seriously affected and damaged by heavy rains and floods in the northern mountainous provinces and the Northern Delta, forcing Vietinbank to replace the above tangible fixed assets, causing financial losses to the bank.

For losses caused by IT, the value is generally not too large and the number of fixes accounts for about 75-80% of the loss value, but overall, this loss is a warning sign for the bank about the safety and solidity of the technology platform in risk management in general and operational risk management in particular. In the period from 2015-2019, the losses caused by IT of Vietinbank can be considered acceptable when compared to the scale of the bank and the number of transactions incurred.

In general, the value of losses caused by operational risks to Vietinbank in the period from 2015 to 2019 is relatively low with the value of losses recovered being equivalent, this is the result of operational risk management, and at the same time is a factor that helps the bank not only reduce operating costs but also enhance reputation and trust in customers. The problem is that this loss figure needs to be compared and considered with the amount of capital allocated to operational risks according to Basel II guidelines, from which it can be concluded whether the bank has effective contingency measures or not in overcoming possible losses caused by operational risks.

2.3. Current status of operational risk management of Vietnam Joint Stock Commercial Bank for Industry and Trade

2.3.1. Legal basis for operational risk management of Vietnam Joint Stock Commercial Bank for Industry and Trade

2.3.1.1. System of policy documents on operational risk management of the State Bank

In recent years, the system of Vietnamese commercial banks has made many advances and breakthroughs in both scale and quality of operations, contributing greatly to the development of the economy.

economic development of the country. However, with the results achieved in business performance, commercial banks have also suffered a lot of losses and are gradually recovering, and in the immediate future, they still have to face many risks in all business activities. Statistics on risk events, especially operational risks, are increasing, causing huge losses to banks in the system.

Realizing that, and at the same time assessing that the operational risk management of commercial banks to be effective requires a transparent, strict and consistent legal corridor, the State Bank of Vietnam has gradually issued policy documents, regulations, decisions, circulars guiding policies, instructions and support to promptly manage and adjust the operations of banks, specifically as follows:

Decision No. 457/2005/QD-NHNN dated April 19, 2005 of the Governor of the State Bank of Vietnam on promulgating “Regulations on safety ratios in the operations of Credit Institutions”. Compliance with these safety limits helps commercial banks control their operations in accordance with their risk management and control capacity. In 2010, this Decision was replaced by Circular No. 13/2010/TT-NHNN dated May 20, 2010 of the Governor of the State Bank on regulations on safety ratios in the operations of credit institutions. This Circular has added many contents that are more suitable for the operations of credit institutions. The Circular also amends/supplements the concepts of credit limits, payment capacity ratios, credit granting ratios compared to mobilized capital sources... In 2014, the Governor of the State Bank of Vietnam also issued Circular No. 36/2014/TT-NHNN (amended by Circular No. 06/2016/TT-NHNN dated May 27, 2016) regulating limits and safety ratios in the operations of credit institutions and foreign bank branches, replacing Circular No. 13/2010/TT-NHNN. By November 15, 2019, Circular No. 22/2019/TT-NHNN was issued, amending and supplementing many contents of Circular 36/2014/TT-NHNN and will officially take effect from January 1, 2020.

Decision 35/2006/QD-NHNN dated July 31, 2006 of the Governor of the State Bank of Vietnam on "Regulations on risk management principles in e-banking activities" with quite strict regulations on risk management due to IT systems in banking activities such as: Regulations on building risk management policies within credit institutions such as building e-banking operation plans, risk management principles for third parties, risk management in transactions with customers, risk management for third parties, risk management in transactions with customers, risk management in cases of incidents... the regulated risk management contents ensure safety for commercial banks when conducting transactions in e-banking activities.

Circular 35/2018/TT-NHNN dated December 24, 2018 amends and supplements a number of articles of Circular 35/2016/TT-NHNN dated December 29, 2016 regulating the safety and security of providing banking services on the Internet. Accordingly, in addition to ensuring the confidentiality and integrity of customer information and the availability of the Internet Banking system to provide continuous services, the Circular also requires credit institutions to regularly check and evaluate the security and confidentiality of the system, identify risks, potential risks and determine the causes of risks, promptly take measures to prevent, control and handle risks in providing banking services on the Internet.

In addition, there are also a number of documents related to risk management and control of activities in the Bank to ensure that risks do not occur, such as Decision No. 36/2006/QD-NHNN on Regulations on internal inspection and control; Decision No. 37/2006/QD-NHNN on Regulations on internal audit of credit institutions; Circular No. 44/2011/TT-NHNN on regulations on internal control inspection and internal audit systems of credit institutions and foreign bank branches. Most recently, Circular No. 13/2018/TT-NHNN issued on May 18, 2018 (amended by Circular No. 40/2018/TT-NHNN) regulating the internal control system of commercial banks and foreign bank branches. On March 17, 2014, the State Bank issued Official Dispatch No. 1601/NHNN-TTSGNH regulating

10 Banks are scheduled to pilot Basel II on capital adequacy (the first pillar of Basel II) - which was later specified in Circular No. 41/2016/TT-NHNN (Circular 41) by the end of 2016, including Vietinbank. To apply Basel II, banks must prepare carefully and increase investment in human resources, technology and operating costs to standardize risk management according to international standards - which are much stricter than Vietnamese standards. Applying this standard, the capital adequacy ratio (CAR) of banks can decrease by about 1.5% to 3%, meaning that the current CAR is from 10-11% or more, but according to the new standard, it can reach over 8% - the minimum required level.

In the context of the financial system being affected by many negative impacts, the State Bank has issued many directives to strengthen the control of deposit safety and payment activities, limiting the impact of fraud risks on customers and banks. The State Bank has issued official dispatches such as: Official dispatch 386a/NHNN-TTGSNH, dated May 8, 2017; Official dispatch 2245/TTGSNH dated July 12, 2017... In which, the State Bank has issued close instructions on the issue of ensuring safety in banking activities, including the issue of internal fraud, causing losses to people's deposits.

In early 2018, the State Bank continued to issue Document No. 1126/NHNN-TTGSNH dated February 23, 2018 (after the incident of losing hundreds of millions of VND of customer deposits at a commercial joint stock bank), in which it made seven requests for banks to implement to ensure the safety of deposit and savings transactions at credit institutions, focusing on groups of solutions on technology, regulations/processes, organizational structure, personnel work, communication/information to customers, interaction with the State Bank and competent authorities when violations arise.

It can be said that the State Bank is increasingly actively supporting the commercial banking system in risk management in general and operational risks in particular, by issuing legal documents and establishing a legal corridor that is increasingly clear, strict and consistent with the general trend of the world as well as the specific characteristics of Vietnam.