Figure 4.2: Credit approval process

(Source: Vietinbank Vinh Long)

Credit appraisal : Vietinbank Vinh Long ensures that credit appraisal is carried out in compliance with the regulations of the State Bank during the credit granting process. The credit appraisal results are based on the customer's credit rating, the completeness of the documents, the legal status, the customer's ability to repay the debt and the ability to recover the debt of the secured assets.

Credit approval : Vietinbank Vinh Long's credit approval process specifically stipulates individuals and councils with the authority to approve credit grants according to specific criteria and clear judgment levels. The approval or disapproval results (stating the reasons) are the responsibility of the individual or member of the approval council.

Collateral management : According to Vietinbank Vinh Long, the loan guarantee business specifies the types of collateral that banks accept as collateral in accordance with the provisions of law. For collateral with high risk levels, the Credit Committee at all levels will consider and approve to control risks. Asset valuation will be directly carried out by the Valuation Center or will re-examine the valuation results assessed by the business unit. Methods

The method of valuation of collateral assets is carried out in accordance with the regulations of the Ministry of Finance on valuation with periodic or ad hoc valuation frequency depending on each type of asset and fluctuations in asset value on the market.

Problematic loans : Vietinbank Vinh Long has established a process and complete reporting for problematic loans to ensure that these loans are closely monitored and supervised from the time of disbursement. Overdue loans of less than 10 days, group 2 loans and above are monitored and reported to have timely handling measures to avoid bad debts. Vietinbank Vinh Long has established a bad debt warning system with full risk identification signs to promptly handle problematic loans.

4.1.2.3 Internal ranking system

Vietinbank Vinh Long has applied the internal credit rating system to evaluate customers in the lending process. The bank has built a complete credit scoring and rating system for credit products and customer segments by 2015. From 2015 to present, the Bank has completed the criteria and credit rating process for individual and corporate customers.

Currently, the credit rating system for customers of Vietinbank Vinh Long includes 10 rating scales with risks from low to high, from Grade 1 to Grade 10. For the credit rating system for customers of enterprises, the regulations are A3 to A5, B1 to B5, C1 to C2 and the subjects of credit restriction are from C3 to C5.

Vietinbank Vinh Long's credit rating tool is based on a set of quantitative and qualitative criteria:

- The quantitative criteria set includes financial criteria from the Financial Report and the qualitative criteria set includes qualitative questions based on the objective assessment of the appraisal officer and the credit approval appraisal department. This criterion is calculated proportionally for 2 subjects: customers who have had credit relationships and new customers at Vietinbank Vinh Long.

- The corporate credit rating system is divided into 2 levels as follows:

- Customers are legal entities with revenue of 1,500 billion VND/year or more and individuals borrowing to serve the business activities of private enterprises (owned by that individual) with revenue of 1,500 billion VND/year or more

- Customers are legal entities with revenue of less than 1,500 billion VND/year or more and individuals borrowing to serve the business activities of private enterprises (which the individual owns) with revenue of less than 1,500 billion VND/year or more

- The personal credit rating system is also divided into 2 levels as follows:

- Customers are individuals borrowing to serve business activities, except in cases where individuals borrow to serve business activities of private enterprises (of which the individual is the owner).

- Individual customers borrow to serve their living needs.

4.2 Assessment of the current status of credit risk management according to Basel II standards at Vietinbank Vinh Long

4.2.1 Meet the minimum capital adequacy ratio

Basically, Vietinbank Vinh Long has met Basel II regulations on minimum capital safety ensuring a high level of 8%, specifically:

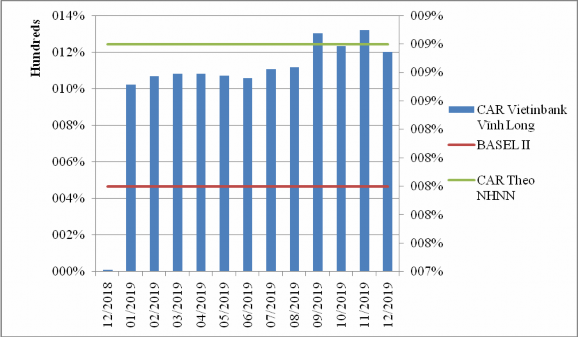

Chart 4.1. Capital adequacy ratio (Car) of Vietinbank Vinh Long

(Source: Vietinbank Vinh Long)

According to the chart above, Vietinbank Vinh Long always maintains a higher capital safety ratio than the Basel II regulations (8%), which shows that Vietinbank Vinh Long always focuses on ensuring capital sources for business activities, especially when credit growth is on the rise. Ensuring the minimum capital safety ratio will help Vietinbank Vinh Long operate more healthily and effectively.

Table 4.3. Consolidated capital adequacy ratio – implementation of pillar 1

Target

December 31, 2018 | December 31, 2019 | |

(1). Equity = (1.1) + (1.2) – (1.3) | 6,404,402 | 9,107,898 |

(1.1). Tier 1 capital | 6,138,678 | 8,795,750 |

(1.2). Tier 2 capital | 298,672 | 337,148 |

(1.3). Amount to be deducted from equity | 32,948 | 25,000 |

(2). Credit risk assets = (2.1) + (2.2) | 58,883,120 | 69,032,907 |

(2.1). Credit Ratio | 58,255,083 | 68,584,496 |

(2.2). Partner credit TSCRR | 628,038 | 448,411 |

(3). Capital required for market risk = (3.1) + (3.2) + (3.3) + (3.4) + (3.5) | 238,138 | 43,791 |

(3.1). Interest rate risk | 236,961 | 40,186 |

(3.2). Stock price risk | - | - |

(3.3). Commodity price risk | - | - |

(3.4). Foreign exchange risk | 1,176 | 3,605 |

(3.5). Risks for options contracts | - | - |

(4). Capital required for operational risk = (4.1) + (4.2) + (4.3) | 289,533 | 501,489 |

(4.1). Capital required for IC index | 352,248 | |

(4.2). Capital required for SC index | 84,156 | |

(4.3). Capital required for FC index | 65,085 | |

(5). Total risk-weighted assets {=(2)+12.5*[(3)+(4)]} | 65,479,008 | 75,848,899 |

(6). Capital adequacy ratio (CAR) (= (1)/(5)) | 9.78% | 12.01% |

Maybe you are interested!

-

General Assessment of Credit Risk Management Status at Vietnam Joint Stock Commercial Bank for Investment and Development - Trang An Branch

General Assessment of Credit Risk Management Status at Vietnam Joint Stock Commercial Bank for Investment and Development - Trang An Branch -

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development -

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch -

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank

General Comments on the Current Status of Credit Risk Management and Factors Affecting Credit Risk Management at Vpbank -

Assessment of credit risk management according to Basel II Agreement at Vietnam Joint Stock Commercial Bank for Investment and Development - 1

Assessment of credit risk management according to Basel II Agreement at Vietnam Joint Stock Commercial Bank for Investment and Development - 1

(Source: Vietinbank Vinh Long)

4.2.2 Database requirements for credit risk management according to Basel II standards

Vietinbank Vinh Long develops a tool to calculate the capital safety ratio automatically and directly connects to the Bank's Data Warehouse. The tool allows calculating Risk Assets of each different risk group (RRTD, RRTD partner, RR Market, RR Operation...) and Risk Assets of business blocks. The capital credit tool ensures the requirements of the State Bank as follows:

All data used to calculate the capital adequacy ratio are available and complete in the Bank's Data warehouse.

The Bank has an organizational structure and processes; tools for data management to ensure data quality and completeness requirements; processes for data collection, comparison (internal and external), storage, access, supplementation, backup, and destruction of data to ensure capital safety ratio (Attached document: Regulations on management, operation and maintenance of Capital calculation tools).

The information technology system connects and centrally manages the entire system, ensuring security, safety and efficiency when calculating the capital safety ratio;

There is a tool connected to other systems to calculate Equity, Total Assets by credit risk, capital requirements for each type of risk and capital adequacy ratio accurately and promptly.

By 2019, Vietinbank Vinh Long's IT system basically meets Basel II standards. Vietinbank Vinh Long has conducted an analysis of IT operational disaster risks - implementing ITSCM regulations including: Risks of external impacts; Risks from partners, third parties, risks from within Vietinbank Vinh Long.

Regarding the server system and data synchronization, the Basel II system is located in a separate network partition, including the application server and the server containing files received from the data warehouse. The financial network partitions are separated, and other systems are synchronized in real time to the backup data center.

4.2.3 Compliance with governance and credit risk management mechanisms according to Basel II standards

The management mechanism of Vietinbank Vinh Long always ensures compliance with Basel II standards on independence in responsibility, authority, and power. Supervision and inspection activities are organized according to an advanced model with 3 layers of defense in accordance with Basel II standards.

Vietinbank Vinh Long's operations ensure 3 layers of defense, which are reflected in the organizational structure and management methods through the system of policies and daily instructions in the system, including:

The first layer of protection : includes customer relations officers and operational departments that comply with procedures and system regulations in customer service such as: credit disbursement control, credit monitoring, collateral valuation, re-appraisal and credit approval.

The second layer of protection : includes the staff departments of the Corporate and Personal Banking Departments, the Debt Management Department, the Executive Board, and the Risk Management Department, which are built with independence in assessment and decision making. These units operate the system through the issuance of policies, procedures, and regulations to control the system.

The important point in the organization and operation of Vietinbank Vinh Long is the independence of the Risk Management Department with veto power in recognizing and assessing risks. Recommendations and policies shaping the system's operations, especially those related to credit granting and management of key risks of the system, are consulted by the Risk Management Department to the Board of Directors for promulgation and decentralization of implementation to subordinates. The Head of the Risk Management Department is also a member with veto power in the operating mechanism of the Credit Council, bringing transparency and independence in the decision-making mechanism.

Third layer of protection: the auditing function and mechanism at Vietinbank Vinh Long has been improved under the consultancy of KPMG since 2015. Periodic thematic reports according to the audit plan built annually are implemented.

Report to the Board of Supervisors and make recommendations and independent assessments for the entire management and operation system, draw lessons, and develop a plan to improve operations.

4.3 Consulting experts on the current status of risk management at Vietinbank Vinh Long according to Basel II standards

To have more reliable information channels about the necessity as well as the results achieved of the research, the author conducted interviews with a group of experts who are directly involved in approaching Basel II standards in credit risk management according to the orientation of Vietinbank Head Office. The group of experts that the author approached has 13 members including: Board of Directors of Vietnam Joint Stock Commercial Bank for Industry and Trade, Vinh Long branch, Heads/Deputy Heads of relevant departments and divisions, and Heads/Deputy Heads of transaction offices in Vinh Long City and districts in the province. ( Attached is the List of Experts and the survey questionnaire in Appendix 1 and Appendix 2 )

Below are the results obtained when surveying experts as follows:

Table 4.4 Summary of expert opinion survey results

STT

STATEMENTS | SURVEY RESULTS CLOSE | Percentage | |

LEVEL OF AWARENESS OF BASEL II | |||

1 | Level of awareness of Basel II | Experts are all there Good insights into Basel II | 100% |

2 | The necessity of applying Basel II in the operations of Vietinbank Vinh Long | Experts agree that it is very necessary. | 100% |

3 | The rationality of capital adequacy ratio regulation Minimum as required by Basel II (8%) | Most experts agree reasonable | 92% |

4 | The effectiveness of the State Bank in monitoring compliance Capital safety enforcement at Vietinbank Vinh Long | Majority opinion is necessary | 92% |

STT

STATEMENTS | SURVEY RESULTS CLOSE | Percentage | |

5 | The need for an internal monitoring approach on the basis of Basel II supervisory framework | Most opinions are that it is necessary. design | 92% |

6 | The banking market in Vietnam is transparent enough to Basel II implementation | The majority opinion is sufficient. transparent | 92% |

ADVANTAGES OF IMPLEMENTATION BASEL II | |||

1 | Clear legal framework from the Government to the Ministries | Majority of opinions agree | 92% |

2 | Supported by the State Bank and international organizations | Majority of opinions agree | 92% |

3 | Supported by shareholders/board of directors | Majority of opinions agree | 92% |

DIFFICULTIES IN IMPLEMENTATION BASEL II | |||

1 | High initial investment and operating costs | Majority of opinions agree | 92% |

2 | Lack of historical data for measurement methods risk assessment | Majority of opinions agree | 92% |

3 | Lack of specialized credit rating organizations industry to reference results | Majority of opinions agree | 92% |

4 | Lack of knowledgeable personnel to build and operate Basel II | Majority of opinions agree | 92% |

5 | Lack of business capital due to provision ratios high reserve | Majority of opinions agree | 92% |

(Source: Data processing from survey)

Through the above summary table, we see that 100% of experts agree that the application of Basel II standards in credit risk management is extremely urgent and necessary. Because only when strictly following international practices, the credit risk management system can identify potential risks, from which the system will overcome to minimize the costs incurred to handle risks, ensuring the efficiency of capital and profits for the bank. Compliance with standards