of the study groups. For example, in a situation where there are three different states (groups) and we are interested in the differences between each pair of groups, we can perform t-tests for each pair of groups, for example, to find the difference between groups 1 and 2, groups 1 and 3, and groups 2 and 3. If each t-test uses a significance level of 0.05, then each test will have a 5% probability of incorrectly rejecting the null hypothesis H0 (a type 1 error). Therefore, the probability of not making a type 1 error is 0.95 for each test. If we assume that each test is independent, then the overall probability of not making a type 1 error is (0.95) 3 =

0.857; from this we can deduce that the probability of at least one type 1 error is 1 – 0.857

= 0.143. Therefore, by conducting 3 separate tests, the probability of making a type 1 error has increased from 5% to 14.3%. If there are many pairs of tests performed separately, the probability of making an error is even higher. Therefore, when there are more than 2 groups, people conduct ANOVA analysis (analysis of variance) to find the difference between the groups while the overall probability of making an error is only 5%. The assumption in the analysis of variance is that all groups have the same mean value. After calculating the F statistic, it will tell us whether the groups have the same mean value or there is a difference. In the thesis, the author will conduct ANOVA analysis to find the difference between different demographic groups for each component of debit card service quality.

2.2.2.3. Regression method

Correlation analysis can be a useful research tool, but correlation coefficients do not tell us about the predictive ability of variables. In regression analysis, we fit a predictive model to the collected data and use the model to predict the values of the dependent variable from one or more independent variables. Simple regression predicts a result variable from a single independent variable, and multiple regression predicts the result variable from multiple independent variables. In linear regression, with the collected data, there will be many “straight lines” that can be used to summarize the trend of the data and we have to choose the best one. The selection of the best line is based on the popular method of least squares. The straight line summarizing the data is represented by the slope and the intercept, and through the method of least squares we will find these two parameters. For multiple regression when there are many independent variables to predict the dependent variable, we will evaluate the model's suitability through indicators such as R 2 , the significance level of

t-statistics related to the independent variables and the values of the estimated parameters (standardized and unstandardized). In the thesis, the author will use regression analysis to examine the factors affecting the quality of debit card services.

CONCLUSION OF CHAPTER 2

The thesis research on the quality of debit card services of Vietnamese commercial banks will be conducted on two aspects: (1) Conditions to ensure the quality of debit card services of the commercial banking system; (2) Quality of debit card services according to customers' perceptions.

Service quality as perceived by customers is carried out through the following steps: research overview, building a questionnaire to collect data, running a measurement model, principal component analysis model, variance and regression, synthesizing results and conclusions.

The scale used was 5-point Likert, the questionnaire was distributed to customers of commercial banks using debit card services. The number of eligible questionnaires collected was 228.

The model variables are tested for reliability by calculating the Cronbach's Alpha coefficient. After calculation, all variables have a Cronbach's Alpha coefficient > 0.8, proving that they are reliable enough to perform the principal component analysis, variance and regression steps. The software used is SPSS 22.

Chapter 3

EVALUATION OF DEBIT CARD SERVICE QUALITY AT VIETNAMESE COMMERCIAL BANKS

The quality of banking services in general and debit card services in particular is recognized and evaluated based on the benefits of banks and customers - the service providers and users, who simultaneously benefit from that service.

Commercial banks will evaluate service quality based on sustainable development criteria, which means increasing bank benefits based on customer satisfaction. Chapter 3 of the thesis will examine and evaluate the results of sustainable development - the quality of debit card services of the Vietnamese commercial banking system.

3.1. Overview of the operations of Vietnamese commercial banks

3.1.1. Bank size, total assets and equity

The Vietnamese commercial banking system has been playing a key role in the system of credit institutions, including state-owned commercial banks and joint-stock commercial banks, with continuous expansion in quantity and scale of operations, remarkable development in both quantity and quality, and diversified ownership forms. This has made an important contribution to promoting economic development.

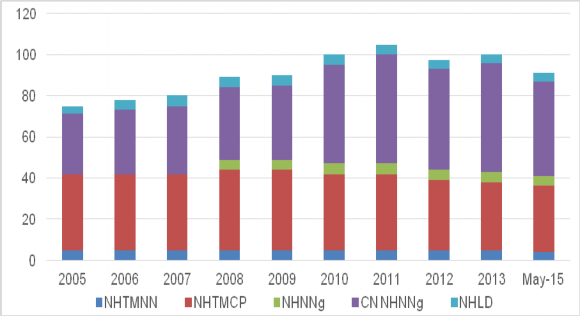

Figure 3.1. Number of banks in Vietnam in the period 2005 - 2015

Source: State Bank Annual Report

During the period 2005 - 2011, the banking system in Vietnam has grown strongly in quantity (in 2011, it increased by about 40% compared to 2005). From 2012 to present, the number of commercial banks has tended to decrease due to the implementation of the project to restructure credit institutions in the period 2011 - 2015.

Owner's equity greatly affects the quality of service, because it is the basis for investing in infrastructure (network, ATM, POS, and modern information technology systems). Commercial banks with large capital often have greater capacity to develop retail banking services in general and card services in particular. By 2015, all commercial banks had fully met the requirements for charter capital. As of September 2015, Vietinbank was the leading bank in the system in terms of charter capital with VND 37,234 billion. In terms of the current charter capital of banks, they can be divided into 3 groups:

Group 1: Banks with charter capital greater than 10,000 billion VND including Vietinbank, BIDV, Agribank, Vietcombank, Sacombank, Eximbank, SCB, Maritimebank, MB;

Group 2: Banks with charter capital from 5,000-10,000 billion VND including ACB, Techcombank, SHB, HDBank, VPBank, LienVietPostBank, TPBank, Seabank, DongABank;

Group 3: Banks with charter capital under 5,000 billion VND include ABBank, Bac A Bank, VIB, OCB, VietABank, NamABank, NCB, BaoVietBank, NamABank, VietcapitalBank, KienLongBank.

The charter capital scale has increased gradually over the years, in which, in 2014 compared to 2013, the charter capital scale of State-owned commercial banks increased by 4.77%, the charter capital scale of joint-stock commercial banks increased by only 1.10%. These are the lowest growth rates in many recent years. Although meeting the legal capital level and the CAR ratio is mostly above 8%, Vietnamese commercial banks are still classified as small and medium-sized banks in the region. This negatively affects the participation of Vietnamese commercial banks in card alliances, purchasing modern payment technology (good security software) to increase the utility of card products.

Table 3.1. Charter capital of the banking system in the period 2012-2015

Unit: Billion VND

Bank

April 30, 2012 | December 31, 2012 | December 31, 2013 | December 31, 2014 | April 30, 2015 | |

State Commercial Bank | 102,605 | 111,550 | 128,094 | 134,206 | 134,206 |

Joint Stock Commercial Bank | 169,321 | 177,624 | 193,536 | 191.115 | 193,115 |

Joint Venture Bank, Foreign | 74,298 | 76,138 | 81,529 | 86,625 | 87,224 |

Whole system | 372,824 | 392.152 | 423,983 | 435,650 | 438,828 |

Maybe you are interested!

-

Research on the impact of e-banking services on the performance of Vietnamese commercial banks - 1

Research on the impact of e-banking services on the performance of Vietnamese commercial banks - 1 -

Research on the impact of international banking services on the performance of Vietnamese commercial banks - 23

Research on the impact of international banking services on the performance of Vietnamese commercial banks - 23 -

Challenges for Vietnamese Commercial Banks in Increasing Competitive Position and Banking Stability When Joining CPTPP

Challenges for Vietnamese Commercial Banks in Increasing Competitive Position and Banking Stability When Joining CPTPP -

Characteristics of the Board of Directors and the performance of Vietnamese commercial banks - 9

Characteristics of the Board of Directors and the performance of Vietnamese commercial banks - 9 -

Overview of the Activities of Vietnamese Commercial Banks

Overview of the Activities of Vietnamese Commercial Banks

Source: State Bank

Except for some banks with negative or decreasing charter capital, many commercial banks, especially large commercial banks, have had impressive charter capital growth such as Vietinbank, BIDV, Vietcombank, Sacombank. Increasing capital is both a condition to ensure capital safety and a condition to expand branches, transaction offices as well as invest in technology, ATM, POS, and a condition to increase the quality of banking services in general, and the quality of debit card services in particular.

In terms of network size and total assets, the Bank for Agriculture and Rural Development always leads the entire system of commercial banks in Vietnam. The total number of branches and transaction offices of Agribank is estimated at over 2,300 points nationwide, followed by Vietinbank with 1,152 points. BIDV is currently the bank with the third largest number of branches and transaction offices nationwide with 127 branches and 584 transaction offices. The number of branches and transaction offices of Vietcombank and ACB is 440 and 345 respectively. It can be seen that expanding branches and transaction points to get closer to customers is one of the important strategies of commercial banks. This will facilitate the implementation of the plan to expand distribution channels in the coming time to promptly meet the needs of residents and businesses in all localities. In addition, the application of information technology in banking activities has created favorable conditions for people and investors to access modern banking products and services, especially card services. It can be seen that, in addition to diversifying and developing transaction channels with customers, modernization and synchronization in each bank as well as in the whole system are increasingly being focused on by banks. Most commercial banks have well developed transaction activities, information lookup... through debit card networks, the internet and recently developed mobile banking. That shows that banks have and

is increasing investment in technology to serve the increasingly diverse and modern needs of customers.

Table 3.2. Total assets of commercial banks in the period 2010-2014

Unit: Billion VND

Target

2010 | 2011 | 2012 | 2013 | 2014 | |||||

% | |||||||||

% increase | % increase | increase | % increase | ||||||

Billion VND | Billion VND | 2011 compared to | Ratio copper | 2012 compared to | Ratio copper | 2012 so | Ratio copper | 2013 vs. with | |

2010 | 2011 | with | 2014 | ||||||

2013 | |||||||||

Whole system system | 4,361,023 | 4,968,316 | 113.93 | 5,657,150 | 113.86 | ||||

Vietcombank | 307,621 | 366,722 | 119.21 | 414,488 | 113.03 | 468,994 | 113.15 | 576,989 | 123.03 |

Agribank | 534,987 | 562,245 | 105.10 | 617.213 | 109.78 | 697,037 | 112.93 | 762,869 | 109.44 |

BIDV | 366,268 | 405,755 | 110.78 | 484,785 | 119.48 | 548,386 | 113.12 | 650,340 | 118.59 |

Vietinbank | 367,731 | 460,420 | 125.21 | 503,530 | 109.36 | 576,368 | 114.47 | 661.132 | 114.71 |

ACB | 205.103 | 281,019 | 137.01 | 176,308 | 62.74 | 166,599 | 94.49 | 179,610 | 107.81 |

Source: Annual reports of Banks, State Bank and Statistics

Author's math

The size, structure and quality of assets determine the existence and development of a bank. Asset quality is a synthetic indicator that reflects the quality of management, solvency, profitability and sustainable prospects of a bank. In general, the total asset size of the 5 research banks is uniform, and has increased over the years during the research period. Table 3.2 shows that the total asset size of Agribank is larger than other commercial banks, followed by Vietinbank, only ACB has a large difference with other banks. In 2012 and 2013, ACB's total assets decreased, although in 2014, there was an improvement in ACB's total assets with 179,610 billion VND, but it was still only approximately equal to

¼ of Agirbank's total assets. However, in terms of total asset growth rate, especially in the last two years (2013 and 2014), Agribank and ACB are not as high as other commercial banks and are always lower than the industry average growth rate.

Figure 3.2. Total assets of commercial banks as of July 2015

Source: BizLive

Compared to 2014, total assets of commercial banks in 2015 increased significantly due to low inflation and attractive deposit interest rates compared to other investment channels. Steady growth in deposits is the basis for commercial banks to increase credit growth and other activities, including payment activities.

3.1.2. Balance between capital mobilization and credit balance

Good capital mobilization is a manifestation of the ability to occupy and expand the market share of commercial banks through various types of products that attract deposits from customers. Moreover, when the capital size is large and the structure is reasonable, it will allow commercial banks to develop business activities such as lending, investing and providing other financial services. The ability to mobilize capital is determined by the size and growth rate of the capital source over time.

During the period 2010-2014, banks had relatively stable capital mobilization growth. ACB in particular, capital mobilization in 2012 and 2013 was lower than previous years, but this situation improved in 2014. In addition, the growth of outstanding loans of Vietcombank, Agribank and BIDV was relatively stable and approximately equal to the average growth rate of outstanding loans of the whole industry. In particular, the growth rate of outstanding credit loans of Vietinbank was always higher than the average growth rate of outstanding loans of the whole industry; Meanwhile, the growth rate of outstanding credit loans of ACB was always below the average level.

Table 3.3. Growth in outstanding credit and mobilized capital of commercial banks in the period 2010 - 2014

Target

(%) Growth in outstanding credit | (%) Growth in capital mobilization | |||||||

2011 | 2012 | 2013 | 2014 | 2011 | 2012 | 2013 | 2014 | |

System average (industry) | 112.52 | 114.16 | ||||||

Vietcombank | 118.40 | 115.16 | 113.73 | 117.85 | 142.63 | 125.75 | 109.97 | 126.31 |

Agribank | 107.02 | 108.24 | 110.44 | 114.08 | 106.61 | 110.02 | 113.91 | 110.20 |

BIDV | 115.64 | 115.64 | 115.04 | 113.98 | 97.19 | 146.23 | 116.40 | 120.44 |

Vietinbank | 125.29 | 138.27 | 113.39 | 117.95 | 123.70 | 109.49 | 111.21 | 116.30 |

ACB | 117.91 | 100.01 | 104.26 | 108.52 | 128.05 | 68.02 | 94.66 | 108.63 |

Source: Annual Reports of Banks; State Bank and Calculation

Author's math

Table 3.4. Ratio of outstanding credit/mobilized capital of commercial banks in the period 2010-2014

Unit: %

Target

2010 | 2011 | 2012 | 2013 | 2014 | |

Vietcombank | 104.38 | 86.65 | 79.35 | 82.07 | 76.57 |

Agribank | 87.33 | 87.67 | 86.25 | 83.62 | 86.57 |

BIDV | 100.90 | 120.05 | 94.95 | 93.84 | 88.80 |

Vietinbank | 68.94 | 69.83 | 88.19 | 89.92 | 91.19 |

ACB | 47.61 | 43.84 | 64.46 | 70.99 | 70.92 |

Source: Annual Reports of Banks; State Bank and Calculation

Author's math

It can be seen that the safety level in outstanding loan growth of the commercial banking system in the period 2010-2014 is relatively high. Although the credit growth rate of commercial banks is high, the capital mobilization growth rate also increases accordingly, meeting the capital demand for credit activities, so the above 5 commercial banks still ensure liquidity with the average credit balance/mobilized capital ratio always at approximately 82%. In which, BIDV's credit balance/mobilized capital ratio is at the highest level (approximately 99.7%) but still lower than 100%. Meanwhile, the ratio of outstanding credit/mobilized capital of ACB in 2010-2011 was low, approximately 45.7%, which proves that ACB's ability to use capital was not effective. However, in the next three years, this ratio increased to approximately 70%, showing a positive change in ACB's capital use.

3.1.3. Risks

Banking is a risky business, or in other words, banking activities always face risks such as credit risk, interest rate, exchange rate, liquidity, operations... In the period of 2007 - 2010, the Vietnamese commercial banking system was under pressure of macroeconomic instability (hot growth of the real estate market, reduced liquidity, high interest rates...), and from 2010 to 2014, bad debt increased due to the recession of the real estate market and the losses of thousands of businesses. Bad debt has pushed the banking system into an extremely difficult situation.

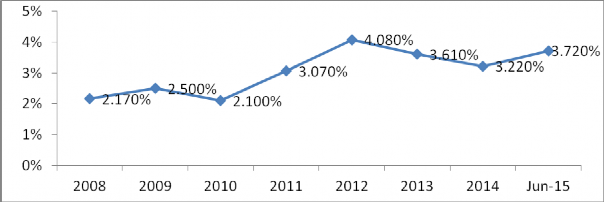

Figure 3.3. Bad debt ratio of the whole system over the years

Source: State Bank

From 2010 to June 2015, the bad debt ratio of the entire banking system increased rapidly from 2.1% (2010) to 3.72% (June 2015), of which in 2012 this ratio was the highest at 4.08% while the general threshold set by the State Bank was 3%. Some banks had this ratio above 6%. Many banks revealed poor management, low profitability, even losses, forced to merge or were bought by the State Bank for nothing.

3.1.4. Profitability of commercial banks

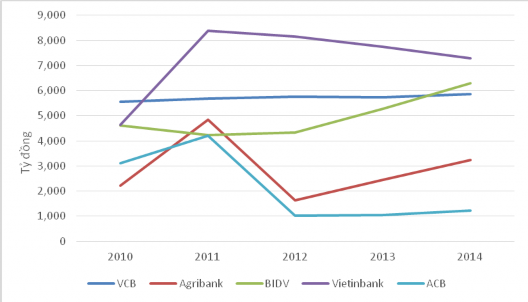

Profit is a synthetic indicator reflecting business efficiency as well as assessing the sustainable development of a bank. The operational efficiency and profitability of a bank are closely related. Figure 3.4. shows that except for Vietcombank, which maintained a stable profit level over the years from 2010 to 2014, the pre-tax profits of commercial banks fluctuated strongly due to the impact of economic instability. Specifically, the pre-tax profits of most commercial banks increased dramatically in 2011 and decreased sharply in 2012. The reason for the sharp decrease in pre-tax profits of commercial banks in 2012 was partly due to the input-output difference of cost of capital gradually decreasing this year and partly because commercial banks had to make large provisions for bad debt risks.

Figure 3.4. Pre-tax profits of commercial banks in the period 2010-2014

In the period 2010-2014, Vietcombank's profit growth was stable but at a low level, while Vietinbank's broke through and excelled. Although there was a slight decrease in Vietinbank's profit since 2010, in terms of absolute value, Vietinbank's total profit was always higher than other commercial banks. Meanwhile, from 2012 to present, the total pre-tax profit of the remaining banks has shown signs of growth, however, the pre-tax profit of Agribank and ACB is still low compared to other commercial banks in the group.

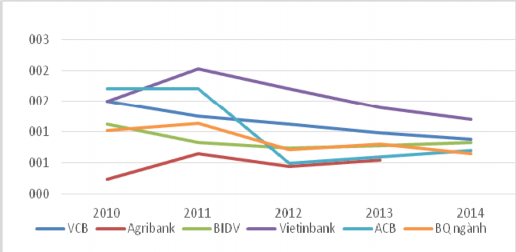

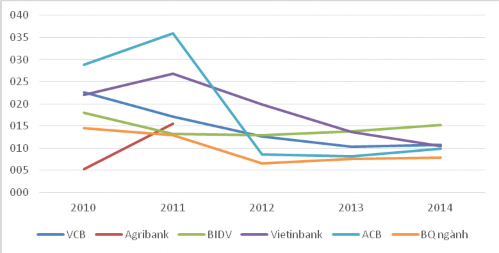

Besides, when analyzing the profitability of commercial banks, we cannot ignore two basic indicators: return on equity (ROE) and return on assets (ROA).

Figure 3.5. Profitability index ROA (%)

Figure 3.6. ROE profitability index (%)

During the period 2010-2014, the operations of the commercial banks studied were always highly effective with ROA and ROE profitability indexes always higher than the industry average, except for Agribank. This proves that the profitability of these banks from equity capital is quite stable. Specifically, the ROA and ROE indexes of Vietinkbank were always high and stable throughout the research period. Meanwhile, compared to the remaining banks, Agribank had a lower ROA index but maintained a relatively stable growth rate.

3.2. Analysis and evaluation of debit card service quality at Vietnamese commercial banks

3.2.1. Increasing the number of cards contributes to reducing cash payments

In the early 1990s, the large-scale wave of tourism, business and investment pouring into Vietnam created a need for credit cards. Some Vietnamese banks with strong financial potential quickly stepped in to exploit this potential market. Card acceptance services in Vietnam began to appear in 1992 and the first bank to provide credit card withdrawal services was Vietinbank (previously known as Incombank in 2008). During the period 1996-2001, the Vietnamese card market was still in its infancy, card products were mainly international cards that only met the needs of the high-income population when purchasing goods and services abroad. Since 2002, the first domestic debit card product was issued in Vietnam, people have begun to know a convenient, fast, easy-to-register, easy-to-use payment method that operates on the basis of personal accounts.

In 2003, the two types of domestic cards used on ATMs (debit cards) were Connect 24 of Vietcombank and F@asAcess of Techcombank, the total number of cards issued (including

The number of domestic and international cards has only reached 234,000 cards. However, card services only really became active in 2006-2007 when the Government issued Decision No. 291/2006/TTg on implementing the Project on non-cash payments for the period 2006-2011 and especially the birth of Decision No. 20/2007/NHNN of the Governor of the State Bank of Vietnam adjusting regulations on issuance, payment, use and provision of support services for bank card activities. This has contributed to creating a very important legal corridor for payment and card issuance activities.

Table 3.5. Number of bank cards classified by payment nature

Unit: Million cards

Year

2010 | 2011 | +/- (%) | 2012 | +/- (%) | 2013 | +/- (%) | 2014 | +/- (%) | |

Prepaid Card | 1.14 | 1.47 | 1.79 | 2.66 | 3.51 | ||||

Credit card | 0.44 | 1.05 | 1.60 | 2.43 | 3.29 | ||||

Debit card | 30.11 | 39.48 | 31.12 | 50.90 | 28.92 | 61.10 | 20.9 | 73.59 | 20.44 |

Total | 31.69 | 42.00 | 32.53 | 54.29 | 29.26 | 66.19 | 21.92 | 80.39 | 21.45 |

Source: State Bank of Vietnam

Table 3.6. Proportion of card types

Year

2010 | 2011 | 2012 | 2013 | II/2014 | |

Prepaid Card | 4% | 4% | 3% | 4% | 4% |

Credit card | 1% | 3% | 3% | 4% | 4% |

Debit card | 95% | 94% | 94% | 92% | 92% |

Total | 100% | 100% | 100% | 100% | 100% |

Source: State Bank of Vietnam

The proportion of debit cards still accounts for more than 90% over the years. However, this proportion is gradually decreasing, instead the proportion of credit cards is increasing. The number of cards has grown quite rapidly, the total number of cards in 2010 was 31.69 million cards, then by 2014 increased to 73.59 million cards, more than 2 times. In 2010, there were more than 30 million debit cards, then by mid-2014, that number had increased to 66.3 million cards, more than 2.3 times. As of December 31, 2014, the total number of cards issued was over 80.39 million, a growth of more than 21% compared to 2013 and a sharp increase of 3 times compared to 2010. In the third quarter of 2015, the number of cards increased significantly, reaching 96.26 million cards. Thus, with Vietnam's current population of about 92 million people, on average each person has used more than 1 bank card.