has been increasing steadily over the past 3 years because MB has expanded lending and has many preferential credit policies for this industry. Specifically, outstanding trade debt in 2012 compared to 2011 increased by 21,172 million VND (or 17.3%); in 2013 compared to 2012, it increased by

47,126 million VND (or an increase of 32.83%). Meanwhile, the proportion of the industrial sector decreased from the highest proportion to the second largest, after the commercial sector. Regarding outstanding debt value, although in 2012 compared to 2011, the industrial sector increased by 13.16%, by the end of 2013, outstanding debt from industry decreased by 16.1%. The reason is that in 2013, the difficult budget situation caused outstanding debt for construction (industry) to decrease significantly, which led to limited industrial lending. In addition, other sectors such as karaoke, services, restaurants, hotels, etc., although increasing over the years due to Hue City developing tourism, still account for a small proportion of the total outstanding debt of the sector because these are not the main target groups that MB targets, so MB does not have many priorities for these sectors but only aims to expand the scale of customers. On the other hand, through table 2.5, it can be seen that the Branch does not conduct agricultural loans because this field is not MB Hue's strength in lending, moreover, the Bank also has limitations in agricultural appraisal.

Classification by debt group

Through table 2.5, we can see that although in 2011 and 2012 the Branch did not incur bad debt, by 2013, bad debt had increased to 14,352 million VND, corresponding to a bad debt ratio of 3.95% of the total outstanding debt of corporate customers. The increase in overdue debt and bad debt has led to an increase in the credit risk provision to 87.53% in 2012 compared to 2011, and an increase of 102.85% in 2013 compared to 2012. The reason for the increase in bad debt is partly due to the general situation of the banking industry during this period, the difficult market affecting businesses in general, but it cannot be denied that another part is due to the control of the lending process of the Bank such as: ineffective implementation plan but still lending, unrecoverable loans, etc. This is a common situation but also an issue that the Bank needs to have a solution to improve the quality of control in the coming time.

Graduation thesis

Table 2.5: Outstanding loan situation of corporate customers by classification at MB - Hue Branch in the period 2011 - 2013

unmarketable

Hu

Unit: Million VND

Target

2011 | 2012 | 2013 | Compare | Compare | ||||||

2012/2011 | 2013/2012 | |||||||||

Value | % | Value | % | Value | % | +/ - | % | +/ - | % | |

Total outstanding debt by business classification | 287,695 | 100 | 338,923 | 100 | 363,377 | 100 | 51,228 | 17.81 | 24,454 | 7.22 |

- Group 1 | 286,670 | 99.64 | 333,887 | 98.51 | 347,599 | 95.66 | 47,217 | 16.47 | 13,712 | 4.11 |

- Group 2 | 1,025 | 0.36 | 5,036 | 1.49 | 1,426 | 0.39 | 4.011 | 391.32 | - 3,610 | -71.68 |

- Group 3 | - | 0 | - | 0 | 14,352 | 3.95 | - | - | 14,352 | - |

- Group 4 | - | 0 | - | 0 | - | 0 | - | - | - | - |

- Group 5 | - | 0 | - | 0 | - | 0 | - | - | - | - |

Bad debt (group 3 + group 4 + group 5) | - | 0 | - | 0 | 14,352 | 3.95 | - | - | 14,352 | - |

Credit risk provision | 1,490 | 0.52 | 2,794 | 0.82 | 5,667 | 1.56 | 1,304 | 87.53 | 2,873 | 102.85 |

Maybe you are interested!

-

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2 -

Discussion on Causes, Limitations and Existing Problems of Short-Term Loan Service Quality Khdn

Discussion on Causes, Limitations and Existing Problems of Short-Term Loan Service Quality Khdn -

Loan Sales Situation of Military Commercial Joint Stock Bank - Hue Branch in the Period 2017 - 2019

Loan Sales Situation of Military Commercial Joint Stock Bank - Hue Branch in the Period 2017 - 2019 -

Indicators for Evaluating the Efficiency of Consumer Lending Activities of NHTM:

Indicators for Evaluating the Efficiency of Consumer Lending Activities of NHTM: -

Capital Mobilization and Lending Situation of Acb Can Tho

Capital Mobilization and Lending Situation of Acb Can Tho

( Source: Customer Relations Department - Corporate Customers at MB - Hue Branch)

SVTH: Sun Nu Trieu Kim41

Graduation thesis

b. Loan turnover

From Table 2.6, we can see that the lending turnover of corporate customers at MB Hue has increased over the years. Specifically, the lending turnover in 2012 compared to 2011 increased by 55,276 million VND, equivalent to an increase of 9.54%; in 2013 compared to 2012 increased by 221 million VND, equivalent to an increase of 0.03%. This shows that customers' trust in the Bank is quite good, more and more customers are coming to the Bank to borrow. It also shows the increasing capital demand of the economy, of the market... In addition, we must also mention the efforts of the Branch in expanding the operating market, improving the quality of credit products and services,... thereby creating customer trust.

Classified by term

Based on the data table, we can see that although there are fluctuations over the years, in general, in the structure of loan sales, short-term loans still dominate (from 87% - 94%). This is because the capital source for lending of the Bank is mainly from short-term mobilization, so the Bank cannot expand too much medium and long-term loans but only focus on short-term loans to maintain liquidity for the Bank. The second reason is due to the risk-averse mentality of banks, medium and long-term loans will create large medium and long-term debt, high risk, clearly the Bank does not want this. While the domestic and world economic situation still has many unpredictable fluctuations, short-term loans are still prioritized because short-term loans have a quick recovery time, limiting risks of interest rates, inflation as well as instability in the economy. Furthermore, the main economic characteristics of Thua Thien Hue province are tourism, developed service industries, economic components in the small business sector, mostly industries with short capital cycles, so short-term loans will be more suitable.

SVTH: Sun Nu Trieu Kim42

Graduation thesis

Table 2.6: Loan turnover of corporate customers at MB - Hue Branch in the period 2011 - 2013

unmarketable

Hu

Unit: Million VND

Target

2011 | 2012 | 2013 | Compare | Compare | ||||||

2012/2011 | 2013/2012 | |||||||||

Value | % | Value | % | Value | % | +/ - | % | +/ - | % | |

Total loan turnover of corporate customers | 579,454 | 100 | 634,730 | 100 | 634,951 | 100 | 55,276 | 9.54 | 221 | 0.03 |

Classified by term | ||||||||||

Short term | 517,981 | 89.39 | 598,520 | 94.30 | 552 . 780 | 87.06 | 80,539 | 15.55 | -45,740 | -7.64 |

Medium and long term | 61,473 | 10.61 | 36,210 | 5.70 | 82,171 | 12.94 | -25.263 | -41.10 | 45,961 | 126.93 |

Classified by business type | ||||||||||

Joint stock company, limited liability company | 528,561 | 91.22 | 586,520 | 92.40 | 588,626 | 92.70 | 57,959 | 10.97 | 2.106 | 0.36 |

Private enterprise | 45,029 | 7.77 | 48,210 | 7.60 | 46,325 | 7.30 | 3.181 | 7.06 | -1.885 | -3.91 |

Other loans | 5,864 | 1.01 | 6,842 | 1.08 | 31,061 | 4.89 | 978 | 16.68 | 24,219 | 353.98 |

By economic sector | ||||||||||

Commerce | 332,474 | 57.38 | 366,797 | 57.79 | 374,248 | 58.94 | 34,323 | 10.32 | 7,451 | 2.03 |

Industrial | 225,946 | 38.99 | 239,994 | 37.81 | 242,775 | 38.24 | 14,047 | 6.22 | 2,782 | 1.16 |

Agriculture | ||||||||||

Other industries | 21,034 | 3.63 | 27,940 | 4.40 | 17,928 | 2.82 | 6.906 | 32.83 | -10.012 | -35.83 |

( Source: Customer Relations Department - Corporate Customers at MB - Hue Branch)

SVTH: Sun Nu Trieu Kim43

Graduation thesis

600,000

500,000

400,000

300,000

200,000

100,000

0

Joint stock company, limited liability company

Private enterprise

Other loans

2011

2012

2013

Classified by business type

Chart 2.5: Loan sales situation by business type at MB Hue over 3 years 2011 - 2013

In total lending turnover of corporate customers, joint stock companies and LLCs always account for a very high proportion and tend to increase.

gradually over the years. Specifically, loan sales

Joint stock companies and LLCs increased from VND 528,561 million in 2011 to VND 588,626 million in 2013. Private enterprise loans increased by 7.06% in 2012 compared to 2011 and decreased by 3.91% in 2013 compared to 2012. Other loan items, although accounting for a small proportion, also tended to increase and contributed to the total loan turnover of corporate customers increasing in 3 years.

By economic sector

In the structure of business revenue by sector, trade and industry always account for the dominant proportion and tend to increase steadily over the years, which is completely consistent with the policies and development directions of the province's key economic sectors. In 2012 compared to 2011, loans to the trade sector increased by 34,323 million VND, equivalent to an increase of 10.32%; in 2013 compared to 2012, loans to the trade sector increased by 7,451 million VND, equivalent to an increase of 2.03%. Industry accounts for the second largest proportion and also increases gradually, in 2012 compared to 2011, loans to the industry increased by 14,047 million VND, or an increase of 6.22%; in 2013 compared to 2012, loans to the industry increased by 2,782 million VND, or an increase of 1.16%. In addition, other sectors account for a smaller proportion, mostly in the service sector, increasing by 32.83% in 2012 compared to 2011 and decreasing by 35.83% in 2013 compared to 2012. In addition, as analyzed, the Bank does not lend to agriculture due to limitations in appraisal capacity and not being the Bank's strength.

c. Debt collection turnover of corporate customers

SVTH: Sun Nu Trieu Kim44

Graduation thesis

Table 2.7: Debt collection turnover table of corporate customers at MB - Hue in the period 2012 - 2013

unmarketable

Hu

Unit: Million VND

Target

2011 | 2012 | 2013 | Compare | Compare | ||||||

2012/2011 | 2013/2012 | |||||||||

Value | % | Value | % | Value | % | +/ - | % | +/ - | % | |

Total debt collection turnover of corporate customers | 768.151 | 100 | 590,344 | 100 | 641,558 | 100 | -177.807 | -23.15 | 51,214 | 8.68 |

Classified by term | ||||||||||

Short term | 626.161 | 81.52 | 486,932 | 82.48 | 544,921 | 84.94 | -139.229 | -22.24 | 57,989 | 11.91 |

Medium and long term | 141,990 | 18.48 | 103,412 | 17.52 | 96,637 | 15.06 | -38.578 | -27.17 | -6.775 | -6.55 |

Classified by business type | ||||||||||

Joint stock company, company Ltd. | 731,144 | 95.18 | 543,620 | 92.09 | 586,376 | 91.40 | -187.524 | -25.65 | 42,756 | 7.87 |

Private enterprise | 32,029 | 4.17 | 39,909 | 6.76 | 44,734 | 6.97 | 7,880 | 24.60 | 4,825 | 12.09 |

Other loans | 4,978 | 0.65 | 6,815 | 1.15 | 10,448 | 1.63 | 1,837 | 36.90 | 3,633 | 53.31 |

By economic sector | ||||||||||

Commerce | 398,952 | 51.94 | 351,741 | 59.58 | 384,935 | 60.00 | -47.211 | -11.83 | 33,194 | 9.44 |

Industrial | 335,638 | 43.69 | 215,396 | 36.49 | 222,407 | 34.67 | -120.242 | -35.82 | 7.011 | 3.25 |

Agriculture | ||||||||||

Other industries | 33,561 | 4.37 | 23,208 | 3.93 | 34,216 | 5.33 | -10.353 | -30.85 | 11,009 | 47.44 |

(Source: Customer Relations Department - Corporate Customers at Military Commercial Joint Stock Bank - Hue Branch)

SVTH: Sun Nu Trieu Kim45

Debt collection turnover reflects the amount of money that the Bank collects from customers who have borrowed money from the Bank over a certain period of time. Debt collection turnover includes all principal payments that customers make during the fiscal year, including capital paid in full under the contract or capital paid in part by customers.

Over the past 3 years, debt collection turnover has fluctuated unevenly. Specifically, debt collection turnover in 2011 at the Branch was quite high, reaching 768,151 million VND, however, by the end of 2012 it had decreased by 177,807 million VND, equivalent to a decrease of 23.15%. By 2013, debt collection turnover had slightly recovered, increasing by 51,214 million VND, equivalent to an increase of 8.68% compared to 2012. The decrease in debt collection turnover at the end of 2012 was due to the fact that at that time the debt collection period had not yet come or at this time only a part of it had been collected. Debt collection turnover reflects the capital turnover and debt restructuring situation of the Bank.

Classified by term

Short-term debt collection accounts for a large proportion of the total debt collection of corporate customers and also has a similar fluctuation to the general debt collection turnover. This is natural when MB mainly lends short-term loans. Specifically, in 2012 compared to 2011, short-term debt collection turnover decreased by 139,229 million VND, equivalent to a decrease of 22.24%; In 2013, short-term debt collection increased by 57,989 million VND, or 11.91% compared to 2012. Meanwhile, over the past 3 years, medium and long-term debt collection turnover has tended to decrease steadily from 141,990 million VND in 2011 to 96,637 million VND in 2013.

Classified by business type

In 2012 compared to 2011, debt collection turnover from joint stock and limited liability companies decreased.

187,524 million VND, a decrease of 25.65%; in 2013 compared to 2012, it increased by 42,756 million VND, or 7.87%. The reason is that joint stock companies and LLCs usually have a fast capital turnover, borrow in large amounts, and the disbursement situation in the year increased, so by the end of 2012, debt collection turnover decreased because the debt collection period had not yet come or by that time the debt had not been fully collected. Meanwhile, the remaining 2 items, private enterprises and other loans, although accounting for a small proportion, increased steadily over the 3 years. Specifically, debt collection turnover from private enterprises increased by 24.6% in the period 2011 - 2012 and

increased by 12.09% in the period 2012 - 2013; revenue from debt collection from other loans increased by 36.9% in the period 2011 - 2012 and increased by 53.31% in the period 2012 - 2013.

By economic sector

Chart 2.6: Debt collection turnover by economic sector at MB Hue over 3 years 2011 - 2013

Commerce and industry are still the key economic sectors, the main subjects of MB Hue and account for a high proportion compared to the remaining sectors. corresponding to the situation of climate change.

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

2011

2012

2013

Trade Industry Agriculture Other

the total revenue from debt collection of business customers, debt collection from

Trade debt collection decreased by 11.83% in 2012 compared to 2011, increased by 9.44% in 2013 compared to 2012. Industrial debt collection turnover decreased by 35.82% in 2012 compared to 2011 and increased by 3.25% in 2013 compared to 2012. Besides, debt collection turnover from other industries, although accounting for a smaller proportion, still had similar fluctuations, decreasing.

10,353 million VND (or a decrease of 30.85%) in 2012 compared to 2011 and an increase of 11,009 million VND (or an increase of 47.44%) in 2013 compared to 2012.

2.2.2. Current status of credit procedures in lending at MB - Hue

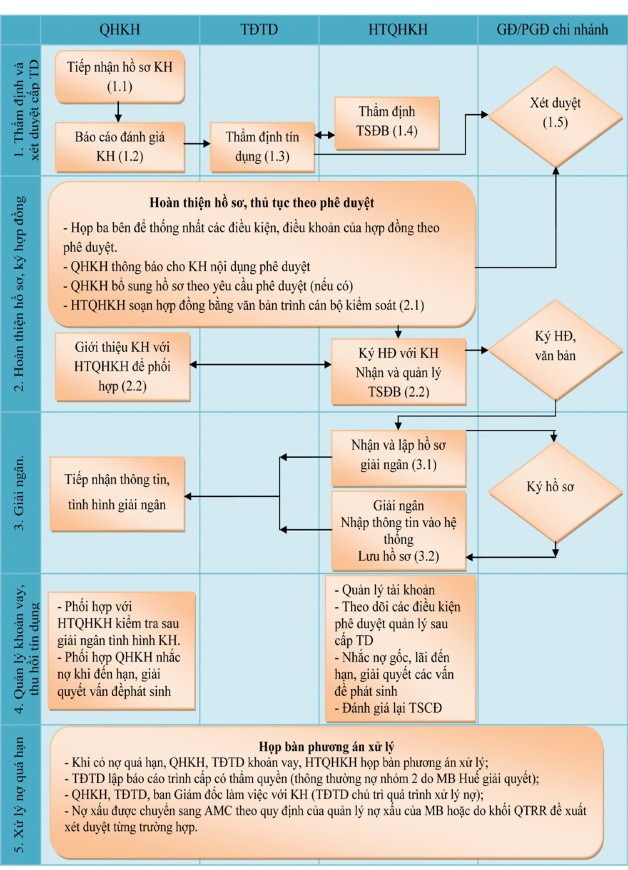

2.2.4.1. Introduction to MB Hue's Credit Process

The credit process is a summary table describing the work of the Bank from the time of receiving a customer's loan application until the decision to lend, disburse, collect debt and liquidate the credit contract. Establishing a credit process and constantly improving it is especially important for a commercial bank. In terms of efficiency, a reasonable credit process will help the bank improve credit quality and minimize credit risks. In terms of management, the credit process has the following effects: as a basis for defining rights and responsibilities for departments in credit activities, as a basis for establishing loan records and procedures.

Flowchart 2.1: Credit process at MB Hue

Flowchart explanation:

Phase 1: Credit appraisal and approval

(1.1) Receiving customer records:

CV QHKH collects loan/guarantee/international payment documents and customer information according to MB's regulations and instructions.

(1.2) Prepare credit proposal report:

CV QHKH prepares credit proposal report for customer (according to MB's Credit Proposal Report form), reports to competent authority for control (Head/Deputy Head/Director of Transaction Office) and transfers to TDTD according to MB's regulations.

Note: CV QHKH is responsible for checking and verifying information before sending it to TDTD; regularly monitoring the process of appraisal and approval of documents, contacting and informing customers about the status of document processing and the expected time to complete the document.

(1.3) Prepare Credit Appraisal report:

- CV TDTD conducts appraisal of customer files (according to the Credit Appraisal Report form - specified in detail for each customer group and product);

- In case of problems that are still unclear due to: lack of information, business plan needs restructuring, etc., TDTD will discuss and request with QHKH to supplement information/ meet with customers, etc.;

(1.4) Asset appraisal:

Before April 2013, the TĐTD CV under the QLTD department was responsible for appraising the collateral according to MB's regulations; After April 2013, the appraisal of collateral was undertaken by MB's debt management and asset exploitation company, MBAMC.

Note: TDTD, HTQHKH, QHKH coordinate flexibly to bring the highest efficiency in the process of granting credit to customers in accordance with the provisions of law and regulations of MB in each period.

(1.5) Review:

The Credit Department sends the Credit Proposal Report, Credit Appraisal Report and documents to the competent authority at the Branch for approval;

Note: Only the approving authority has the right to refuse a loan.

Phase 2: Complete the application, sign the Loan Agreement and related credit documents.

(2.1) Complete documents and procedures according to approval:

- TDTD receives approval from competent authority (with attached documents) and forwards to QHKH, QHKH to carry out next steps;

- QHKH, TDTD, HTQHKH meet to agree on the terms and conditions of the approved Credit Documents (if necessary);

- QHKH notifies customers of loan-related contents; supplements and completes approved documents and procedures (if any);

Note: In case the Customer does not agree with the loan/guarantee/international payment conditions set forth by MB, QHKH shall consider and seek the opinion of the competent authority to reconsider the conditions set forth in order to enhance the benefits in the relationship with the Customer. In this case, the process will be restarted from step 1.1.

(2.2) Signing of Credit Documents:

- QHKH Department drafts credit documents according to MB's regulations in accordance with approved contents;

- QHKH introduces customers to the QHKH Department to coordinate the signing of relevant credit documents, the QHKH Department submits them to the competent authority for signing;

- HT QHKH completes procedures related to TSDB according to the provisions of law and regulations of MB;

Note:

- The Customer Service Department drafts credit documents according to MB's template. In case there is no template, the Branch shall propose to the Business Block management agency at the Head Office to coordinate in drafting credit documents according to MB's regulations.

- In case the Customer does not agree with some terms in the Credit Documents without changing the loan/Guarantee/international payment conditions that MB has set out in the approval, the Customer Relationship Management Office and the Customer Relationship Management Office will discuss and agree and submit to the competent authority to sign the contract for consideration and direction.

Phase 3: Disbursement/Issuance of letter of guarantee/International payment

(3.1) Receiving and preparing documents

- For disbursement records:

- When the customer has a need for disbursement, the QHKH HT CV will receive the documents and check the disbursement conditions (if the QHKH receives the documents from the customer, it will be transferred back to the QHKH KT).

- In case the disbursement conditions are met, the Customer Service Department transfers all disbursement documents (debt acknowledgment contract, disbursement documents, etc.) to the department/division in charge for control signature and submission to the leader for approval of disbursement;

- The competent authority at the Branch is the Branch Director or the authorized person to sign and approve the disbursement;

Note: In case the disbursement conditions are not met, the QHKH system will discuss with the QHKH to supplement and provide information. In case there is a need to change the approved content, the process will be restarted from step 1.1.

- For the letter of guarantee issuance file:

After completing all procedures according to the approved guarantee plan, the QHKH HT CV drafts the guarantee letter and submits the guarantee letter that has been controlled by the content control department/division leader to the competent authority for signature.

- For international payment records

CV HT QHKH completes the documents and sends them to the international payment department/office/center according to MB's import documentary credit regulations;

(3.2) Enter information into the system and save records.