quickly and promptly, contributing to the implementation of exchanges between regions and countries. With such a motto, the ACB Can Tho website has also contributed to the purpose of providing information, news, prices... regularly to the people, as well as introducing its potential, strengths, and typical products.

4.1.1.5 Competitive environment

a). General competitive environment of the entire banking industry

In the domestic market, ACB is competing with over 40 commercial banks, including 5 large State Bank of Vietnam (Vietcombank, BIDV, Incombank, Agribank, Mekong Delta Housing Bank), 1 policy bank, 1 development bank, 37 joint stock commercial banks... Domestic commercial banks currently hold nearly 90% of the market share (both deposits and loans), of which state-owned commercial banks alone account for 70%. Foreign banks (including 4 joint venture banks, 28 foreign bank branches, 43 representative offices) account for less than 10% of the market share.

Thus, competition in the banking and finance sector will become increasingly fierce and intense, especially with the presence of foreign banks such as HSBC, ANZ, Citibank, etc. They are very strong in finance, global management capabilities, and professional staff. Domestic banks face many great challenges such as competitive pressure in aspects such as financial capacity, technology, management level, product systems, service quality, safety standards according to international practices, risk provisions, debt classification. And Vietnamese banks also face increased risks in the state-owned enterprise customer segment because integration puts enterprises in a fierce competition, high possibility of losing market share, and merger trends.

In short, in the context of integration and market opening taking place vigorously along with the policy of encouraging private economic sectors to participate in the banking and finance sector, this requires ACB to promote its inherent strengths, at the same time actively innovate, improve financial capacity, management and administration, technology level, diversify financial products and services to meet the increasing demands of customers and competition.

b) Competitive environment in Can Tho City

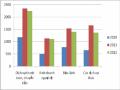

As of the end of 2007, Can Tho city had a total of nearly 40 credit institutions operating, including 7 state-owned commercial banks, 18 joint-stock commercial banks, 01 joint-venture bank, and 02 foreign banks with representative offices. In addition, there were 02 finance leasing companies and 3 credit funds in the area. The situation of capital mobilization and lending in the area of credit institutions in 2007 was shown as follows:

Table 7: CAPITAL MOBILIZATION AND LENDING SITUATION OF ACB CAN THO

COMPARED WITH CREDIT INSTITUTIONS IN THE AREA IN 2007

Unit: Billion VND

INGREDIENT

CAPITAL MOBILIZATION | Outstanding balance | |||

Amount | % | Amount | % | |

1. Credit institutions in Can Tho | 10,200 | 100.00 | 17,500 | 100.00 |

2. Asia Commercial Bank Can Tho | 430 | 4.22 | 568 | 3.35 |

Maybe you are interested!

-

Capital Mobilization Situation At Mb Viet Tri Branch

Capital Mobilization Situation At Mb Viet Tri Branch -

Developments in Capital Mobilization, Investment, Deposits, and Lending on the Interbank Market Up to September 2012

Developments in Capital Mobilization, Investment, Deposits, and Lending on the Interbank Market Up to September 2012 -

Analysis of Capital Situation Through Balance Sheet

Analysis of Capital Situation Through Balance Sheet -

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1 -

Capital Mobilization Management of Commercial Banks

Capital Mobilization Management of Commercial Banks

(Source: Business performance report of ACB Can Tho)

* Evaluate the performance of ACB Can Tho compared to other credit institutions.

used in the area:

In general, the mobilization and lending situation of credit institutions in the area has grown quite well. Of which, VND deposits accounted for 89.22% of mobilized capital and 78.68% of outstanding loans in 2007. The reason is that credit institutions with headquarters in large cities such as Hanoi and Ho Chi Minh City have expanded their operating networks, so a series of branches have been opened and put into operation in Can Tho City. On the other hand, rural commercial banks have simultaneously increased their charter capital and transformed into urban commercial banks.

Capital mobilized in the area as of December 31, 2007 of ACB Can Tho branch is

430 billion VND, accounting for 4.22% of the total mobilized capital of credit institutions.

and accounts for 15.2% of the total mobilized capital of the commercial banking sector.

In 2007, the branch's capital mobilization increased by nearly 169 billion VND, equivalent to 64.75% compared to 2006. This rate increased higher than the general growth rate of all commercial banks (29.15%) and also higher than the growth rate of joint stock commercial banks (68.57%).

Outstanding loans in the area as of December 31, 2007 at the branch reached 568 billion VND, accounting for 3.35% of the total outstanding loans of credit institutions and 1.42% of the total outstanding loans of joint stock commercial banks. In 2007, outstanding loans of the branch increased by nearly 164 billion VND, equivalent to 51.6% compared to 2006. This rate increased higher than the general rate of all commercial banks (15.43%) and was equivalent to the increase rate of joint stock commercial banks (52.96%).

4.1.2 Analysis of the operating environment

4.1.2.1 Analysis of customer consumption behavior

a) Consumer habits

Table 8: RELATIONSHIP BETWEEN CUSTOMERS AND IMPORT-EXPORT FINANCE NEEDS

TARGET CUSTOMERS

SAMPLE COMPONENTS | KH CHARACTERISTICS | PRODUCT DEMAND | |

State-owned enterprise | 13.33 % | Traditional customers. Have cross-industry relationships. Care about after-sales service. | Long term loans with fixed interest rates. |

100% foreign owned company | 6.67 % | Focus on brand. Care about service quality and utility services. Quick and simple procedure. Modern trading style. | Guarantee services, tax consultancy. Short and medium term loans. |

Private enterprise, LLC | 46.67 % | Working capital constraints. Pay attention to the financing interest rate. Care about service attitude staff. | Discounting of valuable papers. Short-term loans in the form of credit or mortgage with future assets. Consulting services. Contract performance guarantee. |

Joint Stock Company | 33.33 % | Pay attention to the funding limit. Diversified business fields. Stocks and bonds can be collateral. Focus on service quality | Medium and long term loans with high limits. Guarantee services. Full banking services. |

(Source: 2008 interview results)

b) Customer expectations for import-export financing

Table 9: CUSTOMER EXPECTATIONS FOR SERVICE

IMPORT-EXPORT FINANCE

EVALUATION CRITERIA

RESULT | |||

Number of times select | % | Sort class | |

Competitive interest rates (loans, discounts) | 29 | 97 | 1 |

Diverse service forms | 12 | 40 | 7 |

High level of funding | 26 | 87 | 2 |

Simple and quick procedure | 18 | 60 | 5 |

Dedicated and attentive staff | 20 | 67 | 4 |

Reputation and size of the bank | 16 | 53 | 6 |

Convenient location | 2 | 7 | 8 |

Competitive service fees | 25 | 83 | 3 |

(Source: 2008 interview results)

From the table above, we can see that the four factors that customers care about most when transacting import-export financing at banks are interest rates, financing limits, service quality of staff and competitive service fees. In particular, the factor that businesses pay the most attention to is the low lending and discount rates of the bank (97%); 87% think that a high financing limit is very important, because the financing limit is not enough to carry out the project or contract, businesses have to apply for financing from different banks at the same time, causing difficulties for production activities. In addition, competitive fees and service quality of bank staff are also factors that businesses are very interested in. Therefore, in addition to creating flexibility in interest rate policies and service fee schedules, considering the possibility of increasing the funding limit for reputable enterprises with effective production and business activities, branches also need to train a team of highly qualified, enthusiastic and attentive staff in dealing with customers to both attract more new customers and create a loyal customer base.

Table 10: NUMBER OF CUSTOMERS FINANCE IMPORT-EXPORT TRANSACTIONS

AT BRANCH

YEAR

NUMBER OF CUSTOMERS | |

2005 | 4 |

2006 | 8 |

2007 | 12 |

(Source: Credit Department)

The number of enterprises transacting import-export financing at the branch over the years has not increased significantly, mainly large customers with long-term relationships of 5-8 years, some customers have just transacted in recent years. In particular, the branch's largest customer is Binh An Seafood, accounting for nearly 45% of the total transaction volume. This proves that there is still a large number of banks that only participate in transactions of a few individual services and do not use the entire import-export service package as expected.

4.1.2.2 Competitor analysis

Competitor analysis is an important step in strategic development planning. Because when you grasp basic information or generally have an overview of the charter capital, branch scale, services, strategies, ... of competitors to be able to consider the impact, learn from their success or draw lessons from failures and also determine your position. From there, you can develop the service in the best way.

a) Foreign banks:

With the event of Vietnam joining the WTO, many foreign financial institutions have researched and determined the ability and timing to access the Vietnamese financial and monetary market, to participate in this market in different forms. Due to the application of the roadmap to loosen regulations for foreign financial institutions, their activities are increasingly vibrant.

*The performance of foreign banks in recent times

Since Vietnam opened up in the banking sector, foreign credit institutions have

In addition, joint venture credit institutions operating in Vietnam are always an important part.

important in the system of credit institutions in our country. Specifically, by the end of 2007:

+ There are 39 bank branches, 7 joint venture banks, 4 financial leasing companies with foreign investment from 14 countries and territories licensed to operate in Vietnam.

+ In terms of value, in 2007, total assets of foreign bank branches and foreign-invested credit institutions reached over VND 270,000 billion, pre-tax income accounted for over 20.14% of total income.

+ The market share of foreign bank branches in terms of outstanding loans increased by nearly 1% to 9%. The total outstanding loans of all foreign bank branches increased by nearly 30% compared to last year, with a total loan value of up to 49,000 billion VND; in which, the overdue debt ratio decreased from more than 0.1% to only 0.06%.

+ Besides, capital mobilization of foreign bank branches also increased by more than 20%, mainly from deposit mobilization, especially from deposits of organizations and enterprises (about 70 - 100%).

In general, foreign financial institutions have stable growth rates, are safe and comply with legal regulations. These institutions are potential competitors of domestic commercial banks, including Asia Commercial Bank.

Regarding foreign bank branches: foreign bank branches are a group of banks that operate dynamically and effectively. Many foreign bank branches have strategies to build and expand their customer network. With management experience and technological advantages, foreign banks are always at the forefront of developing and applying modern technology as well as new products to the Vietnamese market such as: electronic banking, factoring, and business brokerage.

Currently, international banks are choosing the least expensive method of market penetration by cooperating with domestic banks (strategic shareholders through the acquisition of shares in local banks). Therefore, saving on marketing costs and infrastructure construction (establishing branches).

In a recent survey by the United Nations Development Program (UNDP) in collaboration with the Ministry of Planning and Investment, a surprising figure was found: 42% of businesses and 50% of the population surveyed answered that they would choose to borrow from foreign banks rather than domestic banks. The reason is that these banks are highly professional and have simple procedures.

simpler, better service and higher reliability. However, that is not as worrying as the information that 50% of businesses and 62% of the population surveyed said that they would choose foreign banks to deposit money. In the current competitive context, the bank that holds the deposits in hand will have the advantage. Therefore, our banks are facing great difficulties, on the one hand having to face domestic banks that are rapidly equitizing, on the other hand having to endure pressure from the massive influx of foreign banks. Each bank must have its own strategy to utilize its strengths and limit its weaknesses in order to survive and develop.

Currently, the direct pressure on this market is not yet evident. But in the future, with the rapid development of TP CT leading to the creation of a large and attractive enough market, foreign banks will compete directly with domestic banks in this market. That is why foreign banks are the number one threat in the future.

It can be seen that, in the import-export market, the main competition for Asia Can Tho is still domestic joint stock commercial banks, not foreign banks.

However, in the near future, once foreign banks have understood the market and the legal corridor is expanded, they will be big competitors for Asia Commercial Bank Can Tho.

* Limitations of foreign competitors

Foreign credit institutions have difficulties in operating in terms of market share and thin branch network, limited capital contribution ratio ceiling, and many technical barriers are still erected to reduce foreign banks' participation in the market.

Also included:

+ Foreign banks all have their own strategies depending on the market segment they want to exploit in Vietnam, but they will face many difficulties if they intend to provide services in market segments targeting Vietnamese companies. The reason is that they do not know this segment thoroughly, but this is a very lucrative market in Vietnam today and is also the strength of domestic banks such as Asia Commercial Bank. They cannot understand Vietnamese culture as well as Vietnamese banks, as well as other banks.