-For employees:

One of the most important assets, the driving force behind the development of Maritime Bank, is human resources. The Bank's Board of Directors is committed to:

- Establish a working environment of trust and mutual respect.

- Create opportunities for development of all Maritime Bank members.

-To shareholders:

Shareholders are those who have absolute trust and are willing to share success and failure with the Bank. In response to that trust, we are committed to providing:

- Increasing investment value for shareholders.

- Ensure sustainable growth of the Bank.

-With the whole society

- Develop effective culture commensurate with benefits.

By ensuring the Bank's continuous growth and regularly participating in cultural and charitable activities, Maritime Bank is committed to contributing cultural and economic values to the community and the overall development of the whole society.

2.2 Introduction to Maritime Bank Hue Branch

Maritime Bank TT - Hue Branch was established on March 18, 2011 as a level I branch of Maritime Bank.

Initially, the head office was located at 40 Le Loi, Vinh Ninh Ward, Thua Thien Hue Province. However, realizing that Thua Thien Hue is a province that plays an important role, a bridge between the North and the South, identified as one of the four provinces in the key economic region of the Central region; the economic structure is shifting in the right direction, in which industry and tourism - services account for nearly 78% of GDP; the demand for banking products and services in the development process is very large. Therefore, on December 5, 2011, the Board of Directors

Maritime Bank has decided to expand and convert Maritime Bank Hue headquarters to

a new, spacious and more convenient location at 14B Ly Thuong Kiet, Vinh Ninh Ward, Hue City, with a more spacious and convenient head office. The old head office will continue to serve customers as one of two transaction points of Maritime Bank in Hue City. Thus, up to now, Maritime Bank has had two transaction points:

Branch 14B Ly Thuong Kiet - Hue City Transaction office 40 Le Loi - Hue City

Entering Hue the latest compared to other banks operating in the area, when the market has a fierce division of market share between banks and the banking market always has strong fluctuations, Maritime Bank will have some great opportunities as a latecomer and can understand the market the best, but also some great challenges when the Maritime Bank brand is still not really impressive in the hearts of customers in Hue, this is not commensurate with the reputation and prestige of Maritime Bank. That is the challenge that the staff of Maritime Bank Hue Branch must face and thoroughly resolve in the future.

After nearly 01 year of operation, Maritimebank Hue has developed stably and effectively, and is considered a prestigious bank by local people. By the end of November 2011, Maritimebank Hue has served nearly 2,000 corporate and individual customers using the Bank's products and services, with total capital mobilization estimated at nearly 500 billion VND. This proves that the trust of customers in the locality and neighboring areas for the Branch is increasing.

In the near future, Maritime Bank plans to open more transaction offices in other locations in the city to make it more convenient for customers to conduct transactions at Maritime Bank.

2.2.1 Organizational structure and personnel of Maritime Bank Hue branch

2.2.1.1 Organizational structure

TT – Hue Branch is a first-level branch of Maritime Bank. Decision of the Chairman of the Board of Directors on the organization and functions of the transaction office, branches and affiliated units, accordingly:

TT - Hue Branch is headed by a director, assisted by a deputy director and includes the following Branch departments and affiliated units, shown in the diagram below.

- Customer service department

- Support room

- Accounting and treasury department

- Administration department

- And transaction offices

Branch Manager

Branch Deputy Director

Transaction Office

Business Department

Part

Business Marketing

Enterprise appraisal department

Private room

Support room

Accounting & Fund Department

Administration Department

Credit Management Department

Credit Management Department

Personal Marketing Department

Part

International

Personal appraisal department

Credit Management Department

Transaction Processing Unit

Figure 4: Organizational structure of Maritime Bank Hue

(Source: Administrative Department of Maritime Bank Hue)

2.2.1.2 Functions and tasks of departments

Board of Directors (consisting of 1 director and 1 deputy director)

The Director is the person who directly manages the bank's operations and is responsible for directing and operating general business tasks and credit granting activities in particular within the scope of authorization. He is allowed to authorize employees to sign and operate the bank's operations on his behalf, usually authorized to the Deputy Director or department heads.

Deputy Director: is the person who directly manages and supervises the activities of departments in the bank, performs the tasks of mobilizing deposits, loans and providing appropriate services according to the bank's mechanisms and regulations.

Support room

Transaction processing department: responsible for money transfers and opening payment accounts.

Credit management department: performs the tasks of disbursing loan applications, debt management,

Monitor credit records before, during and after loan.

International payment department: performs tasks of opening L/C, transferring money abroad...

Customer service department: includes Personal and Business credit departments

Act as the focal point for providing all banking products to customers, implementing operations from contact to providing guidance on preparing accounting documents.

Conduct marketing activities to expand market share.

Build monthly business plan.

Provide professional support to affiliated units.

Accounting and Fund Department

Accounting Department: performs tasks related to the payment process, receipts and disbursements according to customer requests, opens accounts for customers, accounts for transfers between banks and customers, between banks and other payment services. It is the place to receive documents directly from customers, store data as a basis for bank operations.

Treasury Department: the place where cash receipts and payments are made based on documents, counterfeit money is detected and prevented, cash, valuable papers, and mortgaged property records are kept.

Administration Department:

Receive, distribute, and archive documents. Purchase, manage, and distribute work tools and stationery according to regulations. Take charge of reception and branch logistics, and monitor personnel status. Develop administrative plans and monitor and evaluate the implementation of the plan.

Transaction office

Service department: marketing (managing the implementation of sales targets for specific products, marketing and customer management, customer care and some other functions); appraisal (appraising credit applications and some other functions).

Support department: transaction processing, credit management (credit support, credit control, debt management); accounting and treasury management (accounting, treasury).

2.2.1.3 Human resources situation

In the process of building and developing, each success of Maritime Bank is associated with the efforts, dedication and contribution of the members of Maritime Bank Hue Branch. Therefore, Maritime Bank has been perfecting its human resources policy and employee treatment policy to retain and attract talented and virtuous people. At the same time, to expand and develop its network of operations, the bank needs a relatively large number of employees. The human resources situation of Maritime Bank Hue in the past 2 years is shown in the following table:

Table 2: Labor structure of MSB Hue in the period 2011-2012

Division criteria

2011 | 2012 | Compare | ||||

SL | % | SL | % | SL | % | |

Male | 13 | 41.9 | 14 | 43.75 | 1 | 7.7 |

Female | 18 | 58.1 | 18 | 56.25 | 0 | 0 |

Total | 31 | 100 | 32 | 100 | 1 | 7.7 |

Maybe you are interested!

-

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch

Organizational Structure of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Bac Ninh Branch -

Organizational Structure of Son Ha Garment Joint Stock Company

Organizational Structure of Son Ha Garment Joint Stock Company -

Organizational Structure of Social Relief Activities in Vietnam.

Organizational Structure of Social Relief Activities in Vietnam. -

Organizational Structure of Management Apparatus: The Organizational Model and Operation of the Nghe An Provincial People's Credit Fund is Shown in Diagram 3.1. Below.

Organizational Structure of Management Apparatus: The Organizational Model and Operation of the Nghe An Provincial People's Credit Fund is Shown in Diagram 3.1. Below. -

Organizational Structure of Agribank Minh Hoa District Branch Note:

Organizational Structure of Agribank Minh Hoa District Branch Note:

(Source: Administrative Department of Maritime Bank Hue)

By gender, we see that the proportion of female workers is higher than that of male workers, but the number of male and female workers is not significantly different, which is explained by the fact that the positions of Teller in the bank are more suitable than female employees. This is probably due to the strategic orientation of Maritime Bank as a retail bank, so it needs many tellers to fully meet the transaction needs of customers.

Because Maritime Bank Hue has only entered Hue for the first year, and has no transaction office, the number of employees of the bank is not large, only including employees working at the Branch. The number of employees has not changed much in the past year, when only one more position was recruited by Maritime Bank in 2012. However, to expand its network and increase its market share in the Thua Thien Hue market, Maritime Bank has been opening more transaction offices at other locations in the area. This will lead to a significant increase in the number of employees of the bank after the upcoming recruitment of Maritime Bank.

2.2.2 General business situation of the branch in early 2012

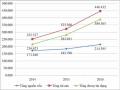

Table 3: General business situation of the branch in the first period of 2012

Unit: VND

Target

January 2012 | February 2012 | Compare | ||||

Value | % | Value | % | Value | +/- (%) | |

A: Total income | 7,507,531,183 | 100 | 9,703,142,547 | 100 | 2,195,611,364 | 29.2 |

Loan interest income | 7,071,522,524 | 94.1 | 8,567,966,372 | 88.3 | 1,496,443,848 | 21.1 |

Revenue from service activities | 68,631,369 | 0.91 | 69,232,636 | 0.71 | 601,267 | 0.87 |

Extraordinary income (loss from foreign exchange trading) | 14,078,919 | 0.18 | -17,000,746 | -0.17 | -31,079,665 | -220.7 |

Other income | 353,298,371 | 4.7 | 1,082,944,285 | 11.1 | 729,645,914 | 206.5 |

B. Total cost | 5,795,651,838 | 100 | 6,843,250,589 | 100 | 1,047,598,751 | 18.07 |

Cost of capital | 5,337,433,686 | 92.0 | 5,912,661,712 | 86.4 | 575.228.026 | 10.7 |

Service operating costs | 21,747,000 | 0.37 | 12,702,733 | 0.18 | -9,044,267 | -41.5 |

Other costs | 0 | 0 | 10,086,727 | 0.14 | 10,086,727 | |

Operating costs | 436,471,152 | 7.53 | 907,799,417 | 13.2 | 471,328,265 | 107.9 |

Profit before TD risk provision expenses | 1,711,879,345 | 2,859,891,958 | 1,148,012,613 | 67.06 | ||

Credit risk provision cost | 0 | 17,291,949 | 17,291,949 | |||

Profit before tax | 1,711,879,345 | 2,842,600,009 | 1,130,720,664 | 66.05 | ||

Corporate Income Tax | 0 | 0 | 0 | |||

Profit after tax | 1,711,879,345 | 2,842,600,009 | 1,130,720,664 | 66.05 | ||

(Source: Maritime Bank Hue Accounting Department)

Although it has just entered Hue with a relatively short life, Maritime Bank has continuously improved the quality of banking products and services and deployed customer service activities quickly and effectively, upgraded infrastructure and information technology to apply to the business process. The development aims at profit, contributing to the economic development of Thua Thien Hue province.

Having just joined Hue in 2011, analyzing the business performance of Maritime Bank in the first 2 months of 2012, we see that the business performance of the branch is on the rise with an increase in after-tax profit of up to 11,307,20664, equivalent to 66.05%. In which, interest always accounts for the largest proportion. In February 2012, Maritime Bank's interest reached 8,567 billion VND, an increase of 1.49 billion VND compared to January 2012, an increase of 21.1%. The strong increase in interest income is due to the fact that recently, lending sales at Maritime Bank Hue branch have increased sharply, and the bank's loan interest is an abundant and main source of income in the bank's business activities.

The revenue that accounts for the second largest proportion after interest income is revenue from other activities, more specifically revenue from provision reversals (4.7%). The remaining revenue from the bank's service activities accounts for a very low proportion (0.91% with 68.6 million VND), which is due to the bank's service provision policy for its customers. With the goal of encouraging customers to use its services, Maritime Bank has minimized service fees for customers, thereby making customers more satisfied and continuing to use Maritime Bank's services. However, that is also a weakness that makes the bank's revenue not reach the desired level.

Regarding costs, in general, Maritime Bank's costs increased in the first months of the year. Last February, the bank's costs increased sharply compared to the first month of 2012, specifically the increase was up to 1.04 billion, accounting for 18.07%. However, in relation to the income growth rate (29.2), this is a smooth and reasonable growth rate, ensuring positive profit growth for the branch.

If in the total income of Maritime Bank Hue, interest income from loans accounts for the highest proportion, then in terms of costs for capital mobilization activities, it accounts for the highest proportion in each month: January accounts for 92%, February accounts for 86.4%. Although the proportion of capital mobilization costs has decreased, it does not mean that Maritime Bank has reduced the current scale of capital mobilization, which is reflected in the growth rate of capital mobilization costs, February is 575 million higher than January, which is an increase of 10.7%. In general, while the market and the State Bank are tending to tighten interest rates, the increase in capital mobilization costs shows that Maritime Bank has significantly increased its mobilized capital. In addition, some other costs of the bank have also increased significantly, leading to a remarkable growth in operating costs, up to 107.9%. These are the cost items: Tax payment costs, employee costs, management and tool operating costs, and basic depreciation of fixed assets.

The profits earned are relatively large over the years, the profits earned in January and February were 1.71 and 2.85 billion respectively, February increased by 66% compared to January. This is a proud achievement of Maritime Bank Hue. Thanks to the correct direction of the branch's leadership, which focused on capital mobilization activities, credit quality has been increasingly improved and business efficiency has increased. In addition, to contribute to the success in the past time, we must mention the wholehearted efforts of the branch's staff. With the criterion of working effectively above all, the branch's staff are always proactive in mobilizing and lending, always excellently completing the set goals, putting Maritime Bank on the way to becoming a strong bank with steady growth over time.

2.3 Assess the level of influence of factors affecting the decision to choose

Select the bank to deposit money for customers in Hue city

2.3.1 Description of survey sample

2.3.1.1 Descriptive statistics of interview subjects

Table 4: Descriptive statistics of interview subjects

Criteria

Frequency (people) | Percent (%) | ||

Sex | Male | 62 | 48.4 |

Female | 66 | 51.6 | |

Age | Under 25 | 6 | 4.7 |

From 25 to 40 | 67 | 52.3 | |

From 40 to 55 | 33 | 25.8 | |

Over 55 | 22 | 17.2 | |

Education level | Middle School, High School | 34 | 26.6 |

Secondary, college | 24 | 18.8 | |

University | 62 | 48.4 | |

Postgraduate | 8 | 6.2 | |

Income | Under 3 million | 20 | 15.6 |

From 3 to 5 million | 38 | 29.7 | |

From 5 to 10 million | 46 | 35.9 | |

Over 10 million | 20 | 15.6 | |

Job | General labor | 14 | 10.9 |

CBCNVC | 42 | 32.8 | |

Business, small business | 36 | 28.1 | |

Housewife | 16 | 12.5 | |

Retirement | 12 | 9.4 | |

Other | 8 | 6.2 | |

Total | 128 | 100 | |

(Source: Results of survey data processing)

Female - 51.6%

Male - 48.4%

Chart 1: Customer Gender

Regarding the gender of the interviewees, the male to female ratio was approximately equal.

There was no significant difference (48.4% vs. 51.6%).

Chart 2: Customer age

The age of the interviewed customers is concentrated from 25 to 40 years old, accounting for 52.3%. Next is from 40 to 55 years old (25.8%) and over 55 years old (17.2%). The age group under 25 years old accounts for the lowest percentage, because at this age, the percentage of customers using bank deposit services is not high.

Chart 3: Education level

The educational level of the majority of the interviewed customers is University (48.4

%) approximately half, more than half of the remaining distribution is concentrated in junior high school, high school (26.6%) and intermediate and college (18.8%). Only a small number of customers have postgraduate education with a rate of 6.2%.

Chart 4: Customer Income

The income of customers is distributed evenly into groups, with a slight increase in the number of groups from 5 - 10 million (35.9%) and from 3 - 5 million (29.7%). The remaining two groups of customers with income levels of less than 3 million and greater than 10 million have similar proportions, each group accounts for 20% of the interviewed customers.