- SOEs related to sectors such as national security, defense, high-tech, rare mineral mining, and many other important sectors will not be sold to any foreign investor or private Chinese organization.

- SOEs in key industries such as energy, transportation, and communications will only be partially sold to foreign companies, but the majority of shares in these SOEs must still be held by the Chinese government.

- Any merger and acquisition involving an SOE that is a mainstay in an industry will be subject to scrutiny by relevant Chinese state agencies.

Fourth, M&A activities for “special purpose” companies. In recent years, many Chinese companies have sought to list on foreign stock exchanges to attract capital. These companies do so by acquiring assets or shares of “shell companies”. This method of listing has not been subject to the control of the Ministry of Commerce or the China Securities Regulatory Commission for a long time. However, until 2006, some legal documents mentioned this case. “Shell companies” are considered special purpose companies, which means that a foreign company is directly or indirectly controlled by a Chinese company and this foreign company is considered a vehicle for the Chinese company to list on a foreign stock exchange. Since 2006, similar acquisitions have required approval from the Ministry of Commerce or the Securities and Exchange Commission.

3. ASSESSMENT OF CHINA'S M&A ACTIVITIES.

3.1. Opportunities and challenges for investors when participating in M&A activities in China.

3.1.1. Opportunity

M&A activities in China are growing due to many favorable factors originating from both the Chinese economy itself and the policies of the Chinese government. Opportunities for M&A activities in China include:

On the economic side, a large and developing market like China is an ideal environment for investment activities, including M&A activities. Firstly, the wave of SOE restructuring is one of the great opportunities for foreign companies wanting to penetrate the Chinese market through mergers and acquisitions. As mentioned in the above sections, SOE restructuring has been taking place for many years and has achieved great results, which has partly promoted M&A activities in China in the industrial and service sectors. According to PWC statistics, each year in China there are about 4,000 to 5,000 equitization deals of SOEs. The wave of SOE equitization is an ideal environment for domestic and foreign companies in China to carry out M&A deals to expand their market share in a large market. In addition to SOEs, POEs also bring great opportunities for foreign and domestic investors. In recent years, M&A activities in China have been strong between POEs - especially POEs formed from SOEs - and foreign investors. In addition, the Chinese government has also created favorable conditions to encourage the merger of SOEs in a number of key industries with the aim of creating giant corporations that can compete in the Chinese market in particular and in the international market in general. The general trend in recent years is that M&A activities have been strong in the retail distribution and logistics sectors to expand the distribution channels of investors. Second, the Chinese economy has had a solid foundation for development in recent years, and the living standards of the Chinese people are clearly improving with increasing purchasing power and consumption. According to the UNDP, the personal consumption level of Chinese people increases by an average of 7% - 9% per year. Such a large demand in the Chinese market is a “pie” that any foreign company would like to have a share in. In addition to the previous traditional forms of investment such as 100% foreign capital investment (Wholly foreing-owned enterprise) or joint ventures, investment in the form of M&A is the fastest and cheapest way to penetrate the Chinese market. For this reason, the proportion of FDI capital flows for

M&A activities in China have increased year by year. Third, Chinese private companies or private family businesses have only been in development for more than 20 years and were not supported before the economic reform. The emergence of M&A activities and the support of the government can be said to be a lifeline for many private companies that are facing great difficulties in business operations and are at risk of closing down. These companies are looking for additional capital for their business operations. Therefore, they are willing to merge or sell companies to improve their management skills and expand their business strategies to a new path.

On the Chinese government side, M&A activities have also been created with many favorable conditions. Especially since 2001 when China officially joined the WTO, with commitments in the fields of finance, real estate, and infrastructure, which are potential areas that promise to bring many opportunities for the M&A market to develop. Moreover, the open-door policy, attracting foreign investment capital, also creates favorable conditions for foreign investors to implement their investment plans. Since 2004, the Chinese government has allowed 100% foreign-owned companies to expand their fields of operation, including wholesale and retail, breaking down barriers in these fields, once again, the M&A market in China has the opportunity to develop more strongly.

3.1.2. Challenges.

For the parties involved in M&A activities in China, both domestic and foreign companies encounter certain difficulties. However, a foreign investor will always encounter much more difficulties than a domestic investor when conducting M&A activities. Therefore, in the research on difficulties in conducting M&A transactions in China, the author will focus on analyzing the difficulties that foreign investors encounter when conducting M&A activities in this market. The difficulties in the policies of the Chinese government and domestic Chinese companies themselves that the parties involved in M&A activities often encounter are issues related to: the legal system regulating

M&A, the M&A environment is not really open and dynamic, there is a lack of information and transparency in the M&A environment,

First, the Chinese government's policy on foreign investment in the form of M&A. The legal framework for foreign investment activities is also applied to M&A activities involving foreign elements. In particular, since August 2006, MOFCOM has issued new regulations for foreign investors to conduct mergers and acquisitions of domestic Chinese companies (Provision for Foreign Investors to Merge and Acquire Domestic Enterprise- the M&A “rule”), replacing the M&A law of April 12, 2003. The new M&A law proposed by the Chinese government is related to many issues such as anti-concentration regulations, issues related to exchanges or acquisitions, employee protection, national security, certain restrictions on foreign investors and many other issues. Here are some of the main legal difficulties that foreign investors often encounter when conducting M&A activities in China:

- The parties allowed to participate in M&A in China are limited to FIEs and domestic companies. A foreign company is not allowed to conduct business directly in China; instead, the foreign company must conduct its business through FIEs. Currently, there are four types of FIEs allowed in China: wholly foreign-owned enterprises, equity joint ventures, cooperative joint ventures, and FIEs limited by shares. Although each type of FIE has its own unique characteristics, they all have one thing in common: they are companies with limited liability. Under China's current legal system, cross-border M&A transactions in China between foreign companies as acquirers and Chinese companies as targets are not permitted. The only legally permitted M&A transactions are those between FIEs or between FIEs and Chinese enterprises.

- The approval process for an M&A deal in China is quite complicated and has many stages. In China, foreign investment projects in various sectors are divided into four categories: “Encouraged, Permitted, Restricted, and Prohibited”. For the approval process of M&A deals, the success rate of obtaining a license depends on many factors such as: which of the four types of investors is involved, the size of the deal, the target company, and the transaction value. Table 2.5 shows the relevant state agencies in granting a license for an M&A deal.

Table 2.5. Competent state agencies

Value of a case

M&A (Unit:USD)

Information authority Via | Top List private | |

Less than 100 billion | SDRC and MOFCOM at the local level square or lower | "Encourage" or “allow” |

Less than 50 billion | SDRC and MOFCOM are only at the level local | "Limit" |

From 50 to 100 billion | SDRC and MOFCOM | "Encourage" and “allow”. |

Over 100 billion but less than 500 billion | SDRC and MOFCOM | "Encourage" and “allow” |

Over 500 billion | State Council Council) | "Encourage" and “allow” |

Over 100 billion | Council of State. | "Limit" |

Maybe you are interested!

-

Opportunities and Challenges of International and Regional Economic Integration for Vietnam's Foreign Trade

Opportunities and Challenges of International and Regional Economic Integration for Vietnam's Foreign Trade -

Opportunities and Challenges, Orientation, Viewpoints and Goals of HCMC Tourism Industry in HNQT

Opportunities and Challenges, Orientation, Viewpoints and Goals of HCMC Tourism Industry in HNQT -

Solutions For Vietnamese Enterprises To Seize Opportunities And Overcome Challenges

Solutions For Vietnamese Enterprises To Seize Opportunities And Overcome Challenges -

Mountain People Face Opportunities and Challenges in the Country's Open Door Period.

Mountain People Face Opportunities and Challenges in the Country's Open Door Period. -

Opportunities and Challenges for the Development of Danang Beach Tourism

Opportunities and Challenges for the Development of Danang Beach Tourism

Source: Report of China Economic Research Institute .

For example, M&A deals that fall under the “encouraged and permitted” category will be approved by MOFCOM and SDRC at the national level with transaction value exceeding USD 100 million. Conversely, for provincial level or lower, MOFCOM and SDRC will approve projects with value below USD 100 million. In addition, the set of documents required for submission for approval of an M&A deal also differs for each deal structure and purpose of those transactions.

- In addition, M&A activities in China are regulated by many different laws such as the Enterprise Law, Anti-Monopoly Law, Investment Law and appear in other decrees and documents, which really makes it difficult for investors to research the M&A market in China.

The second difficulty for M&A activities in the Chinese economy is the lack of dynamism and flexibility. The Chinese economy is not yet considered a complete market economy, so domestic Chinese companies themselves are still partly influenced by the remnants of old working habits. Many private companies as well as SOEs when intending to participate in M&A deals still have a reserved and passive mindset. In addition, there are many regulations of domestic Chinese companies that force investors to think carefully before carrying out M&A activities. For example, for SOEs, under the provisions of the Employee Protection of State Restructuring Regulation, the first thing these SOEs need to do when restructuring is to get approval from all employees and unions. So, of course, when an SOE participates in an M&A deal, they will have to propose a reasonable allocation plan for employees to get the approval of all employees in that SOE. For foreign investors, accepting more employees of the Chinese target company is not an attractive thing, however, Chinese companies can rely on this clause as a lever to force foreign investors to try to accept as many employees in the newly established company after the M&A as possible. It can be said that this is also a difficult thing for foreign investors, thereby reducing the dynamism of the M&A market in China.

The third difficulty in conducting M&A activities in China is that the M&A market in China still lacks transparency and information. Before the development of the stock market in China in recent years, investors had real difficulties in accurately valuing a domestic Chinese company. The accounting system of domestic Chinese companies still did not comply with the

international standards, which makes it difficult for investors to check the assets and value of that company. However, in recent years, the Chinese economy has really changed a lot, the stock market has developed more strongly and therefore, the difficulties in M&A activities due to lack of information and transparency are also gradually being overcome.

3.2. Achievements and limitations in China's M&A activities

Country

3.2.1. Achievements.

3.2.1.1. The M&A market in China is the number one choice for investors.

foreign investment in Asia.

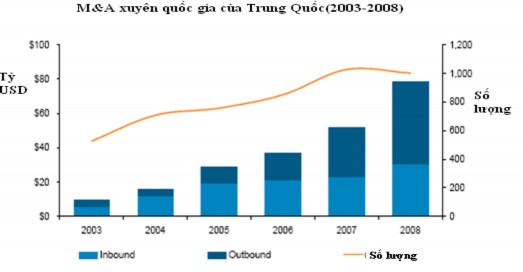

Currently, China is one of the six countries in the world that attracts the most FDI capital, in which the proportion of FDI for M&A activities is increasing. In 2005, that proportion was only over 21%, but by 2007 it had reached over 30%. Especially since 2001, the total value of M&A transactions related to foreign elements in China has increased sharply, however, since 2005, the growth rate has gradually decreased. By 2008, although the world economy was in crisis, the volume of Inbound M&A and Outbound M&A transactions in China continued to increase.

Figure 2.15. China's cross-border M&A activities (2003-2008)

Source: Ministry of Commerce of China.

Despite the economic crisis, cross-border M&A deals in China continued to increase in 2008, with a record transaction value of 78.4 billion USD, up 51.1% over 2007, with a total transaction value of 51.9 billion USD. Of which, inbound M&A activities increased by 34.2% over last year. In recent years, foreign investors have been conducting more mergers and acquisitions in China's financial sector. Currently, the financial sector has the strongest attraction for investors instead of the industrial sector as in a few years ago. In 2008, M&A activities in the financial sector accounted for 34.7% of the total M&A transaction value in China, reaching 10.6 billion USD.

3.2.1.2. China's M&A market ranks third in Asia Pacific.

In Asia Pacific, China's M&A market is second only to Japan and Australia. Compared to Australia and Japan, China's total M&A transaction value is 3 to 6 times smaller. This shows that the Chinese market still has a lot of opportunities to expand and develop strongly, especially when the Chinese economy is developing more and more firmly, GDP and personal consumption index are increasing higher and higher. In 2006, China's M&A activities had a total transaction value of 2.7% of the world, which is still a modest number for a country with great development potential like China. However, by 2008, this number had exceeded 3.2%.

A notable point of the Chinese M&A market is that in the years before 2005, like Korea and India, China still played the role of the target of M&A deals more than the subject of those deals. This means that M&A deals in China were mostly conducted by foreign companies acquiring domestic Chinese companies. Thus, although China ranked right after Japan and Australia in the M&A market, unlike China, Japan and Australia took the initiative in M&A deals. However, from 2005 to now, China's Outbound M&A activities have grown very strongly, quickly accounting for a large proportion of the total value.