This published information will help users of the Financial Statements understand important information in the Balance Sheet, as well as outside the Balance Sheet, thereby determining the financial situation, current status of the enterprise, and cash flow in the enterprise.

MASB 24 sets out the requirements for the presentation of financial instruments in the Balance Sheet, clearly identifying information that must or must not be presented as a financial instrument. The standard requires an enterprise to:

- Classify financial instruments as financial liabilities or equity instruments.

- Presentation of interest, dividends and economic losses

- Situations where a financial asset or financial liability is derecognised and the entity must disclose this information

- Factors affecting the scale, timing and stability of cash flows related to financial instruments.

- Accounting policies applied to financial instruments

- Purpose of using financial instruments

- Risks associated with financial instruments

- Management's policy to control risks

MASB 24 is a financial instruments standard that helps companies prepare reports and provide high-quality financial instrument information. The disclosure requirements for financial instruments in Malaysia are presented in Appendix 2.20: Disclosure requirements for financial instruments in Malaysia

2.5.2 Lessons learned from accounting for financial instruments for non-financial enterprises in Vietnam

The development of financial instrument accounting is an important step in the process of economic transformation and financial market development in Vietnam. Therefore, when building and promulgating financial instrument accounting standards in enterprises, it is necessary to

Non-financial businesses need to pay attention to the following issues:

- To ensure the provision of truthful and useful information while complying with the principle of consistency, it is necessary to clearly define the classification and initial identification of basic financial instruments and derivative financial instruments in order to have appropriate accounting procedures for each type.

- It is required that all financial instruments, including underlying financial instruments and derivative financial instruments, must be recorded at fair value. If the instruments are traded on the market, the fair value is the current market price, if the financial instruments are not traded on the market, the fair value is determined based on future cash flow valuation techniques such as discounted cash flow techniques.

- When developing accounting standards for financial instruments, the focus should be on the requirements for recording and presenting financial instruments, and should not go into detailed regulations on accounting methods for each type to avoid making the regulations complicated.

- When making regulations on presenting and disclosing information about financial instruments, it is necessary to take into account the different needs of users: business administrators, investors, shareholders, partners... Information needs to meet the following requirements: Information needs to be concise (financial instruments need to be presented in groups with the same economic nature or purpose of use); Information helps readers assess the liquidity and financial flexibility of the enterprise.

In summary, the principles of identification, classification, measurement, recording, presentation and disclosure of information on financial instruments need to be built on the economic nature of financial instruments, the purpose of using financial instruments, the objectives of financial risk management in enterprises and must be consistent with international accounting practices.

CHAPTER 2 SUMMARY

In the widespread development trend of the world economy, international economic integration is a trend in most countries. The inevitable result of the integration process is the formation of multinational companies, parent companies and subsidiaries with mutual control. Therefore, there needs to be a common language in controlling and managing the financial situation of the enterprise - that is accounting. Financial instrument accounting aims to provide information to help enterprises come up with an optimal capital mobilization structure in each period, establish a reasonable profit sharing policy, control the use of assets, capital, and risk management.

Based on the theory of financial instrument accounting in non-financial enterprises and the experience of financial instrument accounting in some countries, chapter 2 of the thesis draws lessons for Vietnam in building a theoretical framework for financial instrument accounting. The content of financial instrument accounting in non-financial enterprises is presented in the thesis according to the accounting process including from Identifying and classifying financial instruments; Measuring financial instruments; Recording financial instruments; Presenting and disclosing information about financial instruments. From the above theoretical framework of financial instrument accounting, the author compares it with the current situation of financial instrument accounting in non-financial enterprises in Vietnam (chapter 3) to find out the inappropriate points and propose solutions to improve. In chapter 2 of the thesis, three hypotheses are proposed to be tested to find the relationship between the level of presentation and disclosure of information about financial instruments and the specific characteristics of the enterprise.

CHAPTER 3

ACCOUNTING STATE ANALYSIS

FINANCIAL INSTRUMENTS IN NON-FINANCIAL ENTERPRISES IN VIETNAM

3.1 Overview of non-financial enterprises and financial instruments in non-financial enterprises in Vietnam

3.1.1 Overview of non-financial enterprises

In the trend of integration and development of the national economy, in addition to promoting the role of bringing value to society from production and business activities, non-financial enterprises in Vietnam also play an important role in restructuring the economy, arranging and reorganizing industries, promoting the integration process of the economy. In that integration process, Vietnamese enterprises have had continuous development in all aspects:

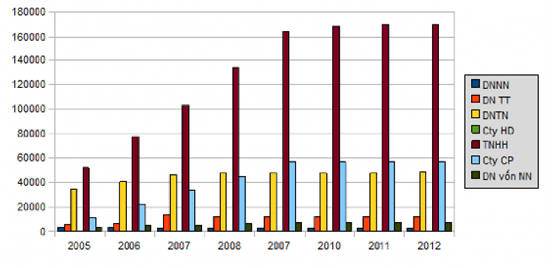

Regarding types of enterprises: Vietnam has 7 basic types of enterprises reflecting methods of ownership and capital investment: State-owned enterprises; Collective enterprises; Private enterprises; Partnerships; Limited liability companies; Joint stock companies; Enterprises with foreign investment capital.

Chart 3.1 Types of enterprises in the period 2005-2012

(Source: Statistical Yearbook 2005, 2006, 2007, 2010, 2011, 2012, Publishing House)

Statistics, Hanoi)

Along with the general development of the economy and the stock market, non-financial enterprises in Vietnam have grown strongly through the equitization process of state-owned enterprises, creating favorable conditions for other types of enterprises to participate in the stock market.

Statistics show the economic sector structure in Vietnamese enterprises.

Table 3.1 Number of enterprises by economic sector as of December 31, 2011

Business type

2005 | 2010 | 2011 | ||||

SL | % | SL | % | SL | % | |

1. Non-financial enterprises | 105 923 | 99.35 | 277 698 | 99.41 | 323 116 | 99.51 |

Agriculture, forestry and fisheries | 2 296 | 2 569 | 3 308 | |||

Extractive | 897 | 2 224 | 2 545 | |||

Processing and manufacturing industry | 20 843 | 45 472 | 52 587 | |||

Production and distribution of electricity, gas, steam, hot water and air conditioning | 663 | 910 | 1 045 | |||

Water supply, management activities, waste treatment waste, wastewater | 322 | 850 | 928 | |||

Build | 13 332 | 42 901 | 44 183 | |||

Wholesale and retail, repair of cars, motorcycles, vehicles machines and other motorcycles | 41 981 | 112 601 | 128 968 | |||

Transportation, warehousing | 5 014 | 14 424 | 17 876 | |||

Accommodation and food services | 4 643 | 10 225 | 12 855 | |||

Information and communication | 1 338 | 4 570 | 7 021 | |||

Real Estate Business Activities | 1 389 | 5 400 | 6 855 | |||

Professional and scientific activities | 5 992 | 20 766 | 27 778 | |||

Administrative activities and support services | 3 513 | 8 374 | 9 790 | |||

Education and training | 1 026 | 2 308 | 2 547 | |||

Health and social assistance | 234 | 839 | 913 | |||

Arts, entertainment | 1 178 | 1 015 | 1 366 | |||

Other service activities | 1 262 | 2 250 | 2 551 | |||

2. Financial and banking enterprises | 693 | 0.65 | 1 662 | 0.59 | 1 575 | 0.49 |

Banking, finance, insurance activities | 693 | 1 662 | 1 575 | |||

Add | 106 616 | 279 360 | 324 691 | |||

Maybe you are interested!

-

Experience in Organizing Management Accounting of Some Developed Countries in the World and Lessons Learned for Application to Vietnamese Enterprises

Experience in Organizing Management Accounting of Some Developed Countries in the World and Lessons Learned for Application to Vietnamese Enterprises -

General Theoretical Basis of Corporate Finance and Corporate Financial Analysis.

General Theoretical Basis of Corporate Finance and Corporate Financial Analysis. -

Completing the work of auditing cash capital in auditing financial statements performed by An Phat Auditing and Accounting Consulting Co., Ltd. - 13

Completing the work of auditing cash capital in auditing financial statements performed by An Phat Auditing and Accounting Consulting Co., Ltd. - 13 -

Lessons Learned That Can Be Applied to Vietnam

Lessons Learned That Can Be Applied to Vietnam -

Lessons Learned From Community Tourism Development Models

Lessons Learned From Community Tourism Development Models

(Source: Statistical Yearbook 2005, 2010, 2011, Statistical Publishing House, Hanoi)

Regarding listed enterprises, in order to mobilize capital for the economy and implement the policy of building and developing a market economy, since the early 90s, the Government has directed the Ministry of Finance and the State Bank to study the project of building and developing the stock market in Vietnam. Based on the project of the Ministries and Branches, on November 28, 1996, the Government issued Decree No. 75/1998/ND-CP on the establishment of the State Securities Commission and assigned this unit to prepare the necessary conditions for the establishment of the stock market.

On July 11, 1998, with Decree No. 48/CP on Securities and Securities Market, the Vietnamese Stock Market was officially born. On the same day, the Prime Minister also signed Decision No. 127/1998/QD-TTg establishing the Ho Chi Minh City Securities Trading Center. Two years later, on July 28, 2000, the first trading session with 2 listed stocks was officially held at the Ho Chi Minh City Securities Trading Center, marking a historic turning point of the Vietnamese Stock Market.

In 2005, the market structure was clearer and more specialized with the separation of the independent operation of the Vietnam Securities Depository Center. At the same time, the securities trading system listed at the Hanoi Stock Exchange was officially put into operation from July 14, 2005. Full name: Hanoi Stock Exchange. International trading name: Hanoi Stock Exchange. Abbreviation: HNX.

On May 11, 2007, the Prime Minister signed Decision No. 599/QD to convert the Center into Ho Chi Minh City Stock Exchange (HOSE). Full name: Ho Chi Minh City Stock Exchange. International trading name: Hochiminh Stock Exchange. Abbreviated name: HOSE.

The number of listed enterprises on the two exchanges HOSE and HNX is shown in the following table:

450

400

350

300

250

200

HOSE

HNX

150

100

50

0

December 2005 December 2006 December 2007 December 2008 December 2009 December 2010 December 2011 December 2012 June 2013

Chart 3.2 Number of listed enterprises on HOSE and HNX

(Source: State Securities Commission)

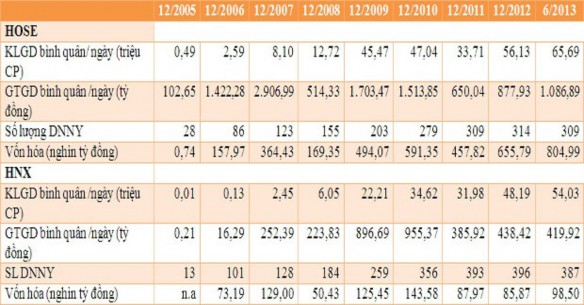

Comparison of average daily trading volume (million shares/day), average daily trading value (billion/day), capitalization (trillion VND) on HOSE and HNX in the period 2005-2013 as follows:

Table 3.2 Comparison of HOSE and HNX

(Source: State Securities Commission)

The stock exchange is a place for investors to meet and buy and sell securities. Each stock exchange has its own regulations and advantages for certain subjects, specifically: A company with a minimum charter capital of 10 billion VND (equivalent to 1 million shares) can be listed on the HNX, while on the HOSE the charter capital must be from 80 billion VND or more. The minimum transaction on the two exchanges is also different: 100 shares/transaction on the HNX, while on the HOSE it is 10 shares/transaction.

The author chose listed companies on HOSE to investigate and collect data to write the thesis because research shows that this is a floor that concentrates many typical companies, has a large scale, many business lines, accounts for a larger capitalization ratio than HNX, and at the same time, the liquidity of the companies is assessed to be higher.

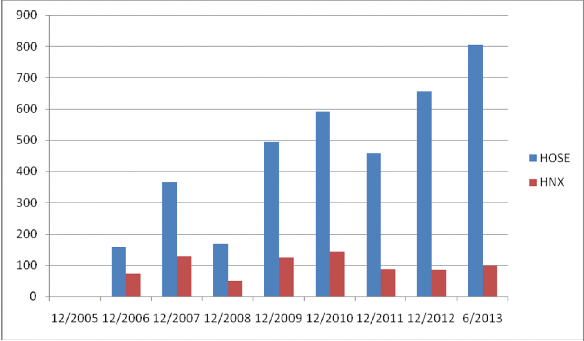

Table comparing capitalization (trillion VND) of HOSE and HNX over the period 2005-2013

Chart 3.3 Market capitalization (trillion VND) on HOSE and HNX

As of December 31, 2012, the total capitalization value of stocks listed on the HOSE reached VND678,403 billion (about USD32.6 billion), up 49.5% compared to 2011, accounting for 24% of the estimated GDP for the year. As of December 31, 2012, there were 308 stocks, 6 fund certificates, and 39 bonds listed for trading on the HOSE with a total listing value of VND258,720 billion, up 27.72% compared to 2011.