The ability to meet export credit conditions is shown in the following aspects:

Production capacity of customers: First of all, customers borrowing capital must have legal status and then must have the ability to carry out the project to ensure that the bank can recover capital and interest. Production capacity is reflected in the value, available machinery and equipment, specifically the product manufacturing process, production technology... inherent. By studying production capacity, commercial banks can determine the production and business content of the enterprise as well as the scale and nature of that production and business activity. In addition, production capacity is also reflected in the level of managers and the executive apparatus. All of these things create the ability to seek profits. To obtain a good quality export credit, customers must have stable production, profitable business, and production and management skills to ensure the export credit project.

Market capacity of export products : Shown in aspects such as product consumption volume, product quality, number of familiar customers, potential output, product position in the market. At the same time, it is also shown in the development and expansion process of the enterprise's production, consumption network system and reputable customers. Market capacity is quantified through the increase in product consumption sales, from which it can be shown whether or not the export credit investment project is feasible.

Financial capacity of the customer : The financial situation of the customer is an important part that needs to be analyzed when making export credit decisions. The bank needs to consider the basic aspects: quality of assets, nature of debts, equity and financial autonomy. The best sign to ensure the quality of an export credit is a business with a stable profit-making process. The ratio of capital for production and business to generate income in total assets is as high as possible, the assessment of the commercial bank must be realistic, in addition, it must consider the total debt and its relationship with assets. Heavy dependence on export credit or export financing shows that the business's capacity is not high and will not be an ideal customer for high-quality export credits.

Maybe you are interested!

-

Orientation and Viewpoints on Improving the Quality of Export Credit Activities of Vietnam Bank for Agriculture and Rural Development

Orientation and Viewpoints on Improving the Quality of Export Credit Activities of Vietnam Bank for Agriculture and Rural Development -

Improving credit quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam in the integration process - 30

Improving credit quality at Joint Stock Commercial Bank for Foreign Trade of Vietnam in the integration process - 30 -

Experience of Some Countries in the Region in Improving the Quality of State Administrative Civil Servants

Experience of Some Countries in the Region in Improving the Quality of State Administrative Civil Servants -

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31 -

Export Credit Development Experience of Some Vietnamese Commercial Banks and Lessons for Agribank

Export Credit Development Experience of Some Vietnamese Commercial Banks and Lessons for Agribank

- Enterprise management capacity : The requirement is to have a unified and regulated accounting and financial management system. In addition,

It is necessary to consider and master the management structure of the enterprise as well as its ability to adapt to market fluctuations because that will ensure the enterprise operates effectively, repays both capital and interest to the commercial bank, bringing high quality results for export credit.

- The situation of pledging and mortgaging assets of the enterprise as well as of the guarantor: This is a decisive issue to ensure the loan of commercial banks. Enterprises must have a certificate of ownership of assets associated with the legal capacity of the enterprise and the ability to use those assets to implement export credit measures. The ownership and value of the assets must be guaranteed until the maturity of the export credit, and must be highly liquid. For the guarantor, in addition to the requirement of legal status, they must also have collateral and ownership of the assets as for the borrower. In particular, for mortgages and pledges, they are often adjusted downward because the sale value and net proceeds from the mortgaged assets are often less when a loan becomes a debt collection. This is also to ensure the safety of the export credit capital that commercial banks spend.

- Customer ethics : The first quality required of a borrower (customer) is to be completely honest. When a commercial bank has doubts about the borrower's ethics or intentions, the commercial bank should not make a loan to ensure the safety of export credit. Therefore, for each customer, the commercial bank often has measures to check the customer's qualifications. Ethical deception often occurs due to the following behaviors of the borrower: Creating fake evidence to be able to borrow money, intentionally appropriating capital from lenders, or borrowers using loans for the wrong purposes... In reality, especially when there are many forms of export credit as today, the quality of export credit depends largely on the customer's ethics.

With the conditions of a newly developed market economy, which is not yet complete in all aspects, as well as the current situation of massive establishment of private companies, the issue of export credit management for commercial banks is really difficult. While waiting for a more complete and strict legal mechanism, the quality of export credit can only be guaranteed if commercial banks choose the right customers with full capacity and good moral character, that is, customers must have full and accurate information to avoid adverse selection and moral risks.

2.3. EXPERIENCE IN IMPROVING EXPORT CREDIT QUALITY AND LESSONS LEARNED FOR THE BANK FOR AGRICULTURE AND RURAL DEVELOPMENT OF VIETNAM

In addition to researching and synthesizing theories on export credit for research purposes; this section 2.3 is designed by the author to research, review and compare with theories on actual export credit activities that have been implemented domestically and internationally; thereby gaining a comprehensive understanding of the problem and drawing practical lessons in the credit development of Vietnamese commercial banks, especially Agribank Vietnam. The review of practical export credit activities is studied on two groups of issues:

- Export credit activities of some typical commercial banks in the world such as EximBank China, UOB Singapore, Eximbank Malaysia.

- Export credit activities of some typical Vietnamese commercial banks such as: ACB, Sacombank, BIDV.

2.3.1. Export credit activities of commercial banks in the world and in Vietnam

2.3.1.1. Operations of the Export-Import Bank of China (EXIMBANK China)

The Export-Import Bank of China (EXIMBANK) is a policy institution directly under the State Council, established and operating since 1994. It is a policy financial institution under the direct management of the State Council. The Export-Import Bank of China operates on the principles of independence, capital preservation and management as a business organization.

The main tasks of this bank are to implement the State's foreign trade and monetary policies, provide monetary assistance to promote the export of electromechanical products, integrated equipment, high-tech products, and promote economic and technical cooperation between China and the outside world. The Export-Import Bank of China is owned by the State of the People's Republic of China. The main business activities of the Export-Import Bank of China are export credit for sellers, export credit for buyers, and preferential loans to foreign countries.

a. Export credit for sellers

The subjects eligible for loans in this business are foreign trade enterprises, industrial and commercial enterprises, manufacturing enterprises and qualified scientific research institutes.

Independent legal entities licensed by the competent authority to conduct business in the export of electromechanical products, synchronous equipment and high-tech products; enterprises with independent legal status, capable of undertaking foreign construction contracts, exporting labor and other economic and technical cooperation sectors. These entities can borrow capital in the following cases:

Loan categories: Loan objects are products such as complete equipment, ships, aircraft, information and sanitation equipment, components of the above products and general electromechanical products, high-tech products, computer software.

Medium and long-term loans: Loan objects are export contracts for electromechanical products and high-tech products with small turnover, short implementation time but large total volume.

Loans for overseas construction contracts : Loan recipients are domestic enterprises that undertake overseas construction contracts.

Foreign processing trade loans : Loan objects are domestic enterprises investing abroad using existing domestic equipment to conduct processing and installation.

Loans for overseas investment : Loan objects are enterprises investing overseas to build factories with synchronous equipment and domestic techniques.

b. Export credit for buyers:

This business is aimed at stimulating China's exports of goods and capital abroad. The borrower is the buyer, the buyer's bank or the Ministry of Finance of the buyer's country.

The scope of the loan is that the borrower uses the loan to purchase electromechanical products, synchronous equipment and high-tech products and services from China.

Loan conditions include: Sales contract of not less than 2 million USD; Chinese products and turnover account for 70% of the turnover in the sales contract, for ships, it accounts for 50%; The deposit rate of the importer is usually not less than 15% (for ship sales contracts, the prepayment rate of the buyer is not less than 20%); The sales contract must comply with the legal regulations of the two countries, be permitted by the Government or competent agencies, and must present a document from the foreign exchange management agency of the importing party allowing the transfer abroad of the entire loan, interest and costs. In principle, it is necessary to implement the regulations

Regulations of the Export-Import Bank of China on procedures for securing export credit loans.

Loan amount, term, interest rate and loan currency: In principle, the loan amount shall not exceed 85% of the value of the contract for exporting electromechanical products, synchronous equipment and high-tech products and services, and shall not exceed 80% of the value of the contract for exporting ships; The loan term is calculated from the date of loan to the final repayment date specified in the loan contract/agreement. The repayment term is based on the implementation status of the items but shall not exceed 12 years; The reference interest rate is based on the interest rate announced monthly by the OECD. The loan currency is USD or other currencies determined by the Export-Import Bank of China.

c. Preferential foreign loans

The Chinese government has provided low-interest preferential loans as aid to other developing countries. Since 1995, the Export-Import Bank of China has been the only bank designated by the Chinese government to provide such loans, which mainly include processing and approving projects, signing loan agreements and guarantee contracts, performing lending operations, supervising management, collecting capital and interest, etc.

Preferential loans from the Chinese Government are mainly invested by recipient countries in projects with high economic efficiency, production projects with the ability to repay, or projects that purchase and use Chinese electromechanical products and synchronous equipment, and can also be used for other projects with payment guarantees.

In addition to export credit activities for sellers, export credit for buyers and preferential foreign loans, the Export-Import Bank of China previously also performed export credit insurance. However, since the establishment of the China Export Credit Insurance Company (in 2002), the Export-Import Bank of China no longer has the function of performing this activity.

2.3.1.2. Operations of United Overseas Bank Singapore

a. Brief introduction about United Overseas Bank Singapore

United Overseas Bank (UOB) was originally established on 6 August 1935 by Datuk Wee Kheng Chiang, as United Chinese Bank; the bank served mainly the Hokkien community in its early years. It was later formally renamed

UOB was established in 1965; over the past 76 years, UOB has grown to become a leading bank in Asia; holding capital of $145 billion in Singapore; a leading bank in personal loans, card issuance and SME lending in the global banking system; UOB provides a wide range of financial services through a network of 500 branches and subsidiaries globally in 19 countries and territories. UOB is rated by Moody's as one of the world's Top Banks, Aa1 and 1st for short-term and long-term deposits.

b. UOB products and services for exporters

UOB products act as a bridge between buyers and sellers of goods and services across national or regional borders, allowing both buyers and sellers to expand their markets. UOB Bank currently provides a full range of solutions for companies involved in international trade transactions including the following services: Letters of Credit, Banker's Guarantee, Standby Letter of Credit, Open Account transactions, Documentary Collection. Some typical export credit support services of UOB:

Export Letter of Credit Confirmation: When the exporter does not grasp the financial capacity of the buyer or cannot predict the risks of the political environment, credit risks of the importer... then L/C becomes extremely meaningful. UOB will ensure that the exporter does not encounter payment risks when there are unusual incidents, then UOB will stand up to fulfill payment obligations for the exporter.

Export Letter of Credit Discounting/ Negotiation: Is a form of advance payment from UOB to the exporter after deducting and discounting a part of the fee; when the exporter's goods have been transferred to the buyer but the payment date has not yet arrived. It helps the exporter to be proactive in his capital plan.

Banker's Guarantee: A bank guarantee is an undertaking given by UOB to pay a beneficiary a certain amount within a specified period of time if the applicant (principal) fails to perform its contractual obligations or underlying transactions. It is typically used to secure financial obligations or principal performance. There are two types of UOB guarantees:

- Performance Bond

- Financial Guarantee

c. UOB products and services for importers

Import Letter of Credit: An import letter of credit is a written undertaking given by the Issuing Bank (UOB), for the account of the buyer (applicant), to pay the seller (beneficiary) the value of the import contract.

Import Documentary Collection: Importers can obtain credit support by exchanging documents of title to the goods shipped with a detailed request for the opening of a letter of credit. These documents can also support exports by guaranteeing payment, only when this payment is approved by the Bank will the goods be released.

Shipping Guarantee: Allows an importer to take possession of the goods from a shipping company when the goods arrive at the port prior to receipt of shipping documents such as Bill of Lading. It is a written commitment from the Bank to the shipping company for payment. The shipping guarantee granted helps importers avoid unnecessary time wastage and storage costs caused by delays in clearing the goods.

Import Invoice Financing (TR): Import Invoice Financing provides customers with short-term financing to ease their cash flow by financing the purchase of goods. The funds are paid directly to the supplier. This is also known as Trust Receipt (TR); Under a TR arrangement, the Bank holds the documents of the goods but allows the buyer to take possession of the goods on trust for resale before paying the Bank on the due date. TR financing is applied to imported goods under documentary credit.

Standby Letter of Credit (SBLC): Standby Letter of Credit (SBLC) is used to secure repayment of loans, ensure performance of contracts and secure payment for goods supplied by third parties. The beneficiary of the SBLC can be declared upon request. The SBLC is less complicated and involves fewer documentation requirements than an irrevocable letter of credit.

d. UOB's import-export support technology system

UOB has deployed a modern Core Banking system to actively support importers and exporters through the UOB eAlerts system, helping importers and exporters manage

more efficient finance. Currently, UOB eAlerts system alerts include SMS or Email notifications of the following:

- Letter of Credit Advice: The importer/exporter will receive notification of the status of their L/C.

- Inward Bills: Importers and exporters will receive notifications about whether L/C and NON L/C have been settled or not, allowing importers and exporters to have better cash flow management measures.

- Incoming Trade Receipts: Importers and exporters will receive notifications about the status of the corresponding import and export procedures.

- Letter of Credit Issuance: Importers and exporters will receive notification of import/export L/C, helping importers and exporters better understand the suppliers of their respective input products.

- Account Balance: Importers and exporters receive account balance notifications twice a day.

- Account Balance Below Threshold: When the importer's account balance falls below the threshold, the importer will receive notifications twice a day, once in the morning and once in the afternoon. This allows the importer to make timely decisions to manage your account and disburse funds.

- Incoming Funds: Importers and exporters will receive notifications (whether from overseas or Singapore) of movements in their trade fund accounts. This saves importers and exporters time and effort in monitoring incoming funds.

- Debit Notification: Importers and exporters will receive this notification when their accounts exceed the limit. It helps importers and exporters manage their cash flows more securely.

e. UOB participates in the Singapore Government's export support program

The Singapore Government's Export Credit Insurance Scheme was launched in March 2009 with the aim of providing Government support to businesses in arranging export credits. Under this scheme, the Singapore Government supports Singapore businesses with 50% of the premium for insurance against payment defaults (non-payment or late payment) from foreign customers for credits granted to businesses. The maximum level of support is not more than

SGD 100,000/eligible business.

However, due to the impact of the global economic crisis, the risk of not being able to collect money or being late is increasing, so insurance companies are becoming more and more strict in providing services, leading to a decrease in insurance value. Therefore, the Singapore Government has added a form of insurance premium support, essentially increasing the level of support compared to before, called "Top-Up Arrangement" - roughly translated as "increasing insurance value". Under this additional form, the Singapore Government will arrange with a number of insurance companies to double the value of payment risk insurance for businesses that are eligible for support and have purchased credit insurance. The increased insurance value does not exceed 2 million SGD/business. The export support program through credit insurance premiums is expected to support about 1,000 Singaporean businesses in transactions with a total value of about 4 billion SGD.

In export insurance support programs, UOB has acted as a bridge and financial intermediary between exporters, importers and the Government to ensure safe, smooth and effective export activities.

2.3.1.3. Operations of Export-Import Bank of Malaysia Berhad

a. General introduction about Export-Import Bank of Malaysia Berhad

Export-Import Bank of Malaysia Berhad (EXIM Bank) was established on 29 August 1995 and is a wholly owned bank under the Ministry of Finance of Malaysia. EXIM Bank's role is to provide credit facilities and insurance services to support the export and import of goods, services and overseas investment in non-traditional markets as well as to provide export credit insurance, export finance insurance, overseas investment insurance.

Exim Bank Malaysia currently provides two lines of conventional credit and Islamic credit for import-export financing, venture capital, and credit insurance globally. The only difference between these two lines of credit is that Islamic credit only supports a narrow range of import-export activities of an Islamic nature, serving Islamic work, needs, Islamic activities or strengthening facilities and infrastructure for the Islamic system. This is a unique feature of Malaysia's financial system because this country has a majority Muslim population.

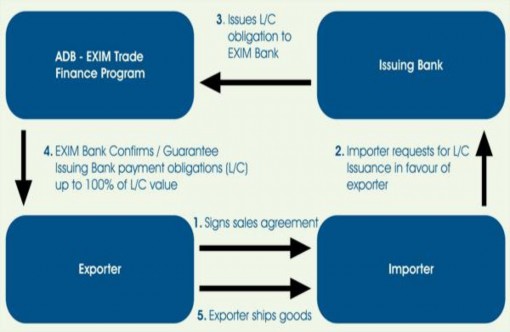

b. Regular export-import credit products of Exim Bank Malaysia ADB - EXIM Trade Finance (Asian Development Bank - EXIM Trade Finance Program). EXIM Bank is the first local bank in Malaysia

has participated in the ADB Trade Finance Program to support export business activities. The program allows Exim Bank Malaysia to confirm and accept payment obligations issued by 78 members of the ADB organization in 16 countries with a guarantee value of up to 100% of the value of the export contract. The goal of this program is to promote import and export activities of Malaysian enterprises with 43 developing ADB member countries. With ADB - EXIM, L/C of importers and exporters will be approved without prior request, thus reducing problems, saving time and effort.

Overseas Project/Contract Financing Facility: Provides financial support to Malaysian investors, contractors’ overseas projects such as infrastructure, manufacturing and other development projects. The purpose of this service is to finance the development, upgrading or expansion of infrastructure, construction plants and the purchase of fixed assets such as machinery and equipment with support of up to 85% of the project cost or contract value; term up to 10 years.

Buyer Credit Facility: Is a financing scheme extended to foreign buyers/importers to purchase Malaysian goods and services. These include goods produced in Malaysia and services rendered in Malaysia or abroad.

Figure 2.1: L/C issuance guarantee

Export of Services Facility: Support for Malaysian Companies specializing in providing services such as Information Technology, Mechanical Architecture and other professional services to have the opportunity and conditions to participate in the supply chain of services to the global market.

Supplier Credit Facility: Malaysian manufacturers and traders can take advantage of this service to support their export trade finance requirements through Exim Bank Malaysia’s trade finance facility. The purpose is to provide financial support for the purchase of raw materials, components, and production costs of finished goods during the pre-shipment period.

Guarantee Facility: Purpose is to facilitate the issuance of bonds for overseas contracts undertaken by Malaysian contractors and also to enable Malaysian investors to raise funds overseas.

Export Credit Refinancing Scheme : Provides short term pre and post shipment credit to direct/indirect exporters. Export Credit Refinancing is suitable for Manufacturers or Trading Companies who have availed valid credit limit provided with any Commercial Bank.

EXIM Overseas Guarantee Facility (EOGF): The EOGF is to assist Malaysian companies in obtaining financing for their participation in secured tendering activities for overseas contracts. EXIM Bank provides financial guarantees to financial institutions exposed to clients. The financing will be provided by the financial institution involved in lending to the client who is a contractor or subcontractor, or involved in the provision, construction or sale of goods, services or such purely service contracts as long as they are owned and controlled by the Malaysian Company.

Malaysia Kitchen Financing Facility: This is a facility to assist Malaysian entrepreneurs with financing for the purpose of establishing or expanding existing Malaysian restaurants overseas or opening new restaurants overseas, developing Malaysian food products with international brands.

2.3.1.4. Asia Commercial Bank (ACB) implements the program "Preferential interest rate credit for import-export enterprises"

One hundred million USD is the limit that Asia Commercial Bank (ACB) has just implemented the program " Preferential interest rate credit for import-export enterprises ", focusing on

Industries such as rice, seafood, cashew, petroleum, plastic, iron and steel,... from February 8, 2012 to June 30, 2012.

Import-export businesses that need additional working capital to make export goods or to pay for imported goods will be financed by ACB with preferential interest rates, lower than regular bank loans.

In addition to preferential interest rates, this Bank also applies a pre-shipment export financing mechanism with a high financing rate:

- Pre-shipment export financing: Up to 98% of L/C value.

- Export financing after delivery: Up to 100% of the value of the set of documents.

- Financing for import payment: Up to 100% of shipment value.

- Accept financing in many different forms of payment (L/C, D/P, D/A, T/T, CAD,..).

- Simple and quick procedures. Financing without collateral for import-export enterprises with many years of experience and good payment reputation with ACB.

2.3.1.5. Joint Stock Commercial Bank for Investment and Development of Vietnam (BIDV) with export credit support solution package

From November 29, 2011, the Joint Stock Commercial Bank for Investment and Development of Vietnam (BIDV) has implemented a credit support package worth 5,000 billion VND for the Export Financing Program by industry to provide timely support to enterprises producing and exporting seafood, textiles, footwear, wood, coffee and other agricultural products...

The purpose of the Program is to support enterprises to overcome difficulties and challenges in production and business activities under the pressure of: Searching for and stabilizing export markets; Increasing surcharges related to production and export activities; Impact from increasing interest rates, exchange rates, etc. In particular, the Program is designed to provide timely seasonal support for customers who are coffee enterprises, production and export of seafood, textiles, footwear, wood and agricultural products (Preparing for Christmas, New Year 2012 and Spring-Summer fashion season).

The export sponsorship program by industry consists of 4 components, specifically: "With BIDV to support Vietnam's seafood industry"; "With BIDV in the coffee export season"; "With BIDV to accompany Vietnamese textile, garment and footwear enterprises" and