Control data and information on computer

The INCAS system ensures that “implementation rights and approval rights” are consistent with the functions of each individual and department in the personal credit granting apparatus at the branch.

The principle of the INCAS system is that only those who register to use the system can participate in operating the system. Each individual in the system is given a BDS access code to access the INCAS system. The password must be changed periodically to ensure safety and security. Employees are allowed to view, edit, and delete information under their responsibility only when they have a valid BDS code and password. Unauthorized people cannot access the operations of other employees, except for superiors who can access the operations of subordinates for monitoring and inspection. The system will automatically record all transactions performed over time, according to each BDS code of each person participating in operating the system (transaction log). Therefore, each person is responsible for the transactions recorded by the system according to his or her authority code.

Maybe you are interested!

-

Current Status of Ksnb Activities for Personal Loan Business at Vib Hue

Current Status of Ksnb Activities for Personal Loan Business at Vib Hue -

Unsecured Personal Consumer Loan Process at Northern Consumer Loan Center - Vpbank

Unsecured Personal Consumer Loan Process at Northern Consumer Loan Center - Vpbank -

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9 -

Evaluation of Financial Indicators in the Credit Scoring System of Asia Commercial Joint Stock Bank for Corporate Customers

Evaluation of Financial Indicators in the Credit Scoring System of Asia Commercial Joint Stock Bank for Corporate Customers -

Current Status of Personal Loan Activities at the Transaction Office - An Binh Commercial Joint Stock Bank.

Current Status of Personal Loan Activities at the Transaction Office - An Binh Commercial Joint Stock Bank.

For external parties: individuals who are not responsible for accessing the system do not have access to the system without the approval and guidance of the system administrator. Thanks to that, information is always highly confidential and ensures information management internally as well as externally.

2.2.1.4 Information and communication

The goal of internal communication is to build, establish and maintain beneficial relationships between the organization and its employees – who determine the success or failure of the business. Realizing that, the Branch Management always focuses on the communication channels used in the business.

The Board of Directors of VietinBank Quang Tri branch issues written orders and instructions stipulating authority, responsibility, specifying the process of performing operations, and handling errors (if any) that arise.

In addition to information communicated in writing, the Board of Directors and superiors provide and convey tasks and information to direct subordinates (orally) when necessary, increasing working contact with subordinates as well as establishing relationships between leaders and subordinates.

management and staff. This way, feedback can be received faster and more promptly.

Adjust accordingly if there is a problem.

VietinBank has established an internal information management system at the Head Office and branches, a website - www.medoc.vn, which specializes in providing internal information as well as information of the Central Bank for each department and officer in the bank. All documents and data are centralized at the database center, all changes are updated online and promptly, helping to manage and search for information effectively. The Board of Directors, leaders of the Science and Technology Department and the risk management team who want to convey any information only need to access the website to convey that information. To ensure confidentiality, each leader and employee of VietinBank is given a BDS code to access the internal network system and can only access the sections according to their own functions and tasks. Using this communication channel helps information to be conveyed quickly and accurately, and employees can update information easily and conveniently.

In addition, the branch also applies Office Communicator software (a type of Yahoo chat software) throughout the branch, each employee, as well as the management board has their own password, convenient for updating and exchanging information with each other. Using this communication channel not only helps to establish and promote the relationship between leaders and employees but also between employees in the branch .

In order to grasp and update external information, customer information before deciding to lend, the Bank registers credit information services at the State Bank's credit information center - CIC (Credit Information Center). CIC shares information between credit institutions to prevent and limit risks in credit activities, contributing to ensuring the safety of banking operations. Information about customers, credit relationships as well as bad cases of customers are consulted by branches through this center.

To ensure that all transactions and activities on the INCAS system and the software programs that the Branch is applying are carried out continuously and smoothly, the Branch has established an Information and Computing Team to carry out management work.

Maintain the system, troubleshoot problems at the branch, ensure smooth operation of the branch's network and computer systems.

2.2.1.5. Monitoring

For regular monitoring activities

For regular monitoring activities

At the branch, there is an Internal Audit and Control Department under the management of the Head Office. The department consists of 2 officers operating according to the regulations of the Vietnam Joint Stock Commercial Bank with the functions and tasks of a specialized internal audit and control department, under the direction and thematic support of the Vietnam Joint Stock Commercial Bank's Internal Audit and Control Department.

Based on the program, plan, and guidance documents of the Inspection and Control Board of Vietnam Joint Stock Commercial Bank and the business performance of the Branch, the Inspection and Control Department has developed an inspection and control program and plan according to the Internal Monitoring Process of Vietnam Joint Stock Commercial Bank , Decision No. 141/QD-BKS-NHCT17.

The Internal Audit Department inspects and supervises the branch's operations in all aspects such as credit, financial accounting, treasury safety, etc., and monitors compliance with legal regulations, mechanisms, and operational procedures of the State Bank and the Central Bank to minimize risks.

If any errors occur, the department will report to the Branch Director on the status of declaration and approval on the machine file for the Director to implement, direct the Science and Technology Department and the Risk Management Team to supplement and edit according to the recommendations. Periodically or suddenly, the Internal Audit Department will prepare a report on the results of inspection, supervision, and report on corrections and corrections of existing problems and errors of the branch and send it to the Internal Audit Department of the Head Office. This ensures independence in the assessment work, without being subject to management from the branch. Therefore, all assessments are objective, contributing to helping the branch perfect the system. (Refer to the Monitoring Report - Appendix 21)

For periodic monitoring activities

For periodic monitoring activities

In addition to implementing the branch director's instructions, every three months the head of the science and technology department requires the credit institutions in the department to carry out self-inspection and cross-inspection among officers on loans, thereby correcting errors and supplementing documents. This inspection and self-inspection must be demonstrated in writing, reported to the head of the science and technology department for review and approval. (Appendix 22)

Through self-inspection and cross-checking, errors were discovered.

often occur as:

o Lack of capital usage inspection records.

o Expired motor vehicle insurance not replenished in time.

o Missing disbursement documents (purchase list without name or address)

seller…).

o The customer has not signed the debt acknowledgement but the CBTD has disbursed the loan.

o Some other errors such as: missing household registration book, not confirming the copy...

Independent monitoring

At the branch, the Internal Audit Team of the Representative Office in Da Nang, in conjunction with the Internal Audit Department at the branch, periodically inspects the branch's operations with various contents, mainly focusing on inspection of compliance with lending mechanisms and procedures.

During the 2010 inspections from March 1, 2010 to March 13, 2010, according to the inspection outline of Decision 022/QD-BKT-NHCT17, the delegation inspected the business operations as well as the lending operations. Through the inspection, the delegation found that the loans were basically processed in accordance with the procedures and met the loan conditions. The loans with complex factors were independently assessed by the Science and Technology Department and the Risk Management Team, and submitted to the Credit Council for consideration and approval.

Regarding loan records managed in accordance with regulations, the branch has arranged management according to ISO standards to keep documents on credit relationship subjects, documents on corporate finance, collateral records, and insurance related to borrowers and collateral.

Regarding credit limit and credit judgment level, the Branch strictly complies with the authorized level. The Branch strictly complies with the judgment level for loans exceeding the judgment level and submits it to the General Director for approval.

Disbursement has been strictly controlled for borrowers. Disbursement of payment transfers to suppliers of goods and services accounts for a high proportion.

However, through inspection of lending activities, the group discovered the following limitations and shortcomings:

- Business registration certificate and documents related to the borrower are copies, not certified, and have been compared with the original by the CBTD/leader of the Science and Technology Department.

- Regarding the business plan of customers, especially individual customers, it is mainly guided by the CBTD, so when appraising, the CBTD refers to the appraisal with limitations, many appraisal items do not calculate the correct input value of the plan.

- Lending according to the HMTD whose limit maintenance period has expired but not considering and analyzing the customer's business situation but signing a new HMTD. Increasing the credit limit but not evaluating the additional loan plan, evaluating and analyzing the reasons for increasing the HMTD.

- In some cases, disbursement of invoices and documents is the basis for disbursement but customers are not required to make a list according to regulations. Invoices proving the use of loan capital are not kept in records scientifically, and it is not possible to determine which disbursement time and which debt receipt (according to the method of borrowing each time).

2.3. Evaluation of internal control system for personal customer lending process

2.3.1. Results achieved

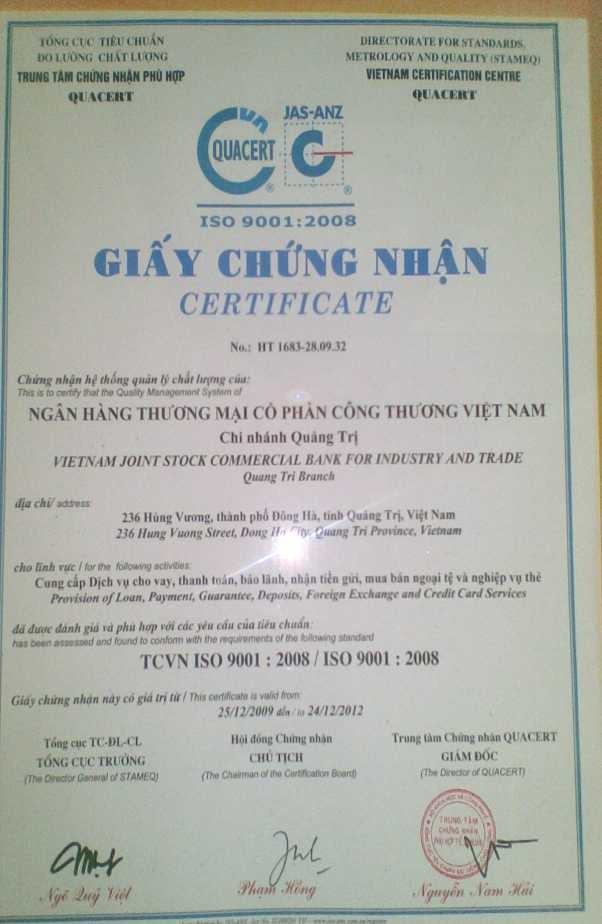

VietinBank - Quang Tri Branch is one of 31 branches nationwide in 2009 of VietinBank, which was granted certificate No. HT 1683-28.09.32 by the Conformity Certification Center - QUACERT, recognizing the quality management system of VietinBank - Quang Tri Branch for the fields of operation such as: providing lending services, payment, guarantee, receiving deposits, buying and selling foreign currencies and card operations, which was assessed and consistent with the requirements of TCVN ISO 9001:2008 standard. The quality management system according to ISO 9001 version 2008 is one of the effective tools, effectively applied by organizations and businesses around the world to manage the quality of operations, improve the quality of products and services, contributing to enhancing the competitive position of businesses. During more than 1 year of implementing the ISO 9001:2008 Quality Management System, the branch has undergone many application guidance sessions, internal assessments and assessments by the Quacert delegation to gradually apply the Quality Management System into the unit's business operations.

Receiving the ISO-standard quality management system has initially demonstrated that the Branch has an effective internal control system. Specifically:

The successful application of ISO quality management system has standardized management in accordance with international standards, helping the branch's Board of Directors to easily control all business activities at the unit, thereby providing timely and appropriate instructions to improve business efficiency, contributing to the completion of assigned tasks, creating a premise for the development and integration of the branch in the following years.

The Board of Directors of VietinBank Quang Tri has always paid attention to the development and consolidation of the internal control system. This is an important basis for effectively managing the lending process for individual customers in particular and lending activities in general, thereby increasing business efficiency, maintaining and enhancing the position of the branch in the province.

First of all, the branch management has created a healthy and highly effective control environment:

The Board of Directors always adheres to the internal control principles, regularly urges and raises awareness for employees to properly implement the branch's lending policy to minimize risks. The Board of Directors as well as leaders of departments and teams always care, share experiences and guide employees to handle difficult situations encountered at work.

In addition, the Board of Directors also sets out common ethical standards throughout the branch, standardizes the relationship between departments, aims to closely coordinate in handling business operations in accordance with VietinBank's procedures and regulations, always strives to maintain integrity and ethics, proper behavior, work effectively, and be an example for subordinates to aspire to and follow.

The branch's personal credit system is reasonably designed and operates effectively. Each department in the system is assigned specific functions and tasks and always monitors each other in their operations.

Human resource policy is always put first by the management board. The branch's staff of managers and supervisors are experienced, highly qualified and receive regular professional training. The management board ensures that employees have stable jobs.

Timely reward outstanding individuals who have contributed to the branch, thereby making employees feel secure in their work and dedicating themselves to the bank. In addition, thanks to the reasonable reward and punishment mechanism, employees work more responsibly.

The branch's personal lending policy system is built according to risk control orientation:

The personal lending policy that the branch has been implementing over the years is consistent with the operating and development conditions. The lending policy system includes specific, complete, and detailed regulations, creating favorable conditions for checking and controlling lending activities. All employees in the entire personal credit system comply with the regulations on credit safety, loan guarantees, and lending interest rates set forth by the State Bank and the Vietnam Joint Stock Commercial Bank, considering it the basis for safe and effective lending.

The control procedures applied in the personal customer lending process at the branch are quite strict:

The branch always complies with the lending procedures, checks, monitors the borrowing process, uses the loan capital and repays the debt of customers, the process of controlling documents and data... according to the regulations set forth by the State Bank of Vietnam. From there, all staff fully implement the steps according to the instructions of the procedure, the procedure specifies the roles, tasks and coordination of activities between individuals and departments, teams in the personal credit granting apparatus of the branch.

Lending decisions are always guaranteed to be objective, with strict inspection and supervision of the entire loan portfolio, only authorized persons are allowed to approve loans. All data related to loans must be entered into the INCAS system. In addition, the implementation of lending activities is always monitored, inspected and approved by a department leader, always closely following the CBTD, ensuring that all activities are carried out effectively. Each lending activity is participated by 2 CBTD, this ensures that no individual can carry out and decide on the work alone. This creates a mechanism for cross-checking and supervision between individuals and departments participating in a lending process.

Risk control for personal lending activities at the branch is very strict because it is participated by two departments: the Risk Management Team conducts inspection and control right in the lending process and the Internal Audit Department conducts regular inspection and supervision after lending at the branch.

In particular, the branch has invested in quite adequate equipment for control: the physical control of assets (secured assets, loan documents, etc.) is applied by the branch with Fujitsu's palm vein identification device - applied to the approval and accounting mechanism of the Board of Directors and the transaction accounting department.

Fujitsu's palm vein recognition technology consists of a small device that can scan and record the veins in the palm of the hand. The device is easy to use, fast and highly accurate. Simply place your hand on the device a few centimeters away, and within a second, the device will read your unique palm vein map. Because in reality, each hand has a different vein map, there are no duplicates even between identical twins. Therefore, no one other than those who have registered their identity at the branch, such as the Board of Directors, the head of the department and the deputy head of the transaction accounting department, can access the information and

carry out approval of activities related to the lending process such as disbursement, collection

debt, import, export of collateral assets...

The branch's information and communication technology system applies the following

Advanced programs and software:

The effective application of the INCAS system, a modern information system with a centralized management model and online transactions, has helped the control work to be carried out in a timely and strict manner. The INCAS system is a highly secure and tightly controlled system. Not only that, the INCAS system has helped the bank manage information in the best way, minimize fraud and limit risks and errors to the lowest level. With CBTD responsible for entering data into the system, the leader of the Science and Technology Department controls the data entry of CBTD, and the staff of the Internal Audit Department checks and supervises the data entry of CBTD (post-loan supervision).

By establishing a website specializing in providing internal information and receiving information from the Vietnam Joint Stock Commercial Bank for Industry and Trade, the branch has ensured an effective communication channel, helping to convey information from the Board of Directors, leaders of departments and teams to departments and each employee quickly and accurately.

To help internal transactions take place quickly as well as contribute to enhancing communication between employees, the branch has applied Office Communicator software.

Image : Office Communicator software interface

This is a product of Microsoft, a software that provides tools and features to help employees in the branch work more effectively by being able to connect with many people in the branch, in different departments, allowing you and your colleagues to work together on Word, PowerPoint, Excel documents as if you were working in the same place. And this can also be considered a relatively effective communication channel that not only helps establish and promote relationships between leaders and employees but also between employees in the branch with each other .

In general, the internal control system for personal lending procedures at VietinBank Quang Tri branch has made great contributions, helping to ensure the safety of the bank's assets, improving the quality of personal lending activities in particular and the bank's credit activities in general.

2.3.2. Problems and causes

The existence

Although the branch's personal customer lending process control system has brought certain results, there are still some shortcomings that need to be overcome:

About human resources:

Most of the branch staff are young, have not worked for a long time, lack experience, and have not received proper on-the-job training. The number of RR managers is still small compared to the amount of work to be done, leading to great pressure at work.

The awareness level of CBTD and CBQLRR in the fields of industry is not deep, thereby causing many limitations in appraising loan plans, checking and monitoring customers' business activities to detect possible risks.

About control procedures:

- The independent appraisal of the Risk Management Team often goes with the CBTD of the Science and Technology Department, so it can be influenced, reducing the independence and objectivity in reviewing and checking credits.

- The inspection and control of capital use by CBTD after lending has not been checked regularly, so risks cannot be detected in a timely manner, and loans are often only checked when there are problems. The inspection work is sometimes not timely or has difficulties in checking the actual customers. The inspection of capital use, although a report on the inspection of loan use has been prepared, has not been signed and approved by the department leader; therefore, the role of post-lending supervision has not been fully promoted for customers who use capital for the wrong purpose, invest in ineffective production and business... to have appropriate handling measures. This affects customers' debt repayment income, leading to banks not being able to recover capital as well as loan interest.

- Banks and credit institutions mainly rely on collateral to lend, which reduces the quality of appraisal and does not fully evaluate the effectiveness of loan use, leading to lending to unreliable customers and increasing overdue debt for banks.