officially sold outside the bank at a higher rate than the official rate. This supply only accounts for a small proportion of sales on TTKCT.

2.3.4.3. Foreign currency demand in the informal foreign exchange market

Residents who need foreign currency: international students, people who travel abroad, visit relatives, seek medical treatment, etc. As economic life develops, people tend to improve their quality of life, from food, clothing, travel, material and spiritual needs, and therefore the need for foreign currency to study, travel, receive medical treatment, etc. abroad increases.

Foreign currency demand of international students : Vietnam is one of the countries with an increasing number of international students every year. According to statistics from the Australian International Education Agency under the Australian Consulate General in Ho Chi Minh City, there were more than 21,000 Vietnamese students studying at high schools and universities in Australia in the first 8 months of 2009 alone, an increase of 58% compared to the same period in 2008. Meanwhile, according to statistics from the Institute of International Education under the American Institute of International Education, the number of Vietnamese students studying in the US in the 2008-2009 school year was 12,830, an increase of 46% compared to the previous school year, ranking 9th in the total number of international students studying in the US, an increase of 11 places compared to two years ago[69]. Thus, only counting the two countries with the largest number of international students, the US and Australia, in 2009 there were more than 33,000 international students and with an average growth rate of 50%, it is estimated that in 2010 the number of Vietnamese students studying abroad will be 100,000 people and if the average cost for each international student is about 20,000 USD/year, the amount of foreign currency needed will be about 2 billion USD/year, this amount of foreign currency is almost not enough to meet the banks while the demand for studying abroad is increasing continuously every year.

Maybe you are interested!

-

Balancing Supply and Demand of a Country's Currency in the Foreign Exchange Market

Balancing Supply and Demand of a Country's Currency in the Foreign Exchange Market -

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market:

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market: -

The Role of Currency Swaps in the Foreign Exchange Market:

The Role of Currency Swaps in the Foreign Exchange Market: -

![Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branchs income.

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giangs profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project Restructuring the system of credit institutions in the period 2011-2015 approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services.

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giangs products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Ministers Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giangs treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giangs income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giangs corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giangs card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:Courier New, monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:Times New Roman, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:Times New Roman, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:Times New Roman, serif; font-style: normal; fo](https://tailieuthamkhao.com/uploads/2022/06/06/dich-vu-phi-tin-dung-tai-ngan-hang-thuong-mai-co-phan-dau-tu-va-phat-8-1-120x90.png) Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branch's income.

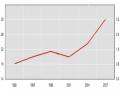

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giang's profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project "Restructuring the system of credit institutions in the period 2011-2015" approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: "Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services".

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giang's products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Minister's Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers' cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giang's treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giang's income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giang's corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giang's card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:"Courier New", monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:"Times New Roman", serif; font-style: normal; fo

Pre-tax Profit of Bidv Tien Giang in the Period 2011-2015

zt2i3t4l5ee

zt2a3gsnon-credit services, joint stock commercial bank

zt2a3ge

zc2o3n4t5e6n7ts

At that time, the Branch had to set aside a provision for credit risks, which reduced the Branch's income.

Chart 2.2. Pre-tax profit of BIDV Tien Giang in the period 2011-2015

Unit: Billion VND

140

120

100

80

60

40

20

0

63.3

80.34

89.29

110.08

131.99

2011 2012 2013 2014 2015

Profit before tax

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, through chart 2.2, it can be seen that BIDV Tien Giang's profit is still increasing continuously, and its operating efficiency is currently leaking. This is a contribution of non-credit services, and this service segment will be increasingly focused on growth by BIDV Tien Giang to ensure the highest profit safety because credit activities have many potential risks. At the same time, focusing on developing non-credit services is consistent with one of the contents of restructuring the financial activities of credit institutions in the project "Restructuring the system of credit institutions in the period 2011-2015" approved by the Prime Minister in Decision No. 254/QD-TTg dated March 1, 2012 [14]: "Gradually shifting the business model of commercial banks towards reducing dependence on credit activities and increasing income from non-credit services".

2.2. Current status of non-credit service development at BIDV Tien Giang.

2.2.1. BIDV Tien Giang has deployed the development of non-credit services in recent times.

Along with the development of the Head Office, BIDV Tien Giang's products and services are constantly improved and deployed in a diverse manner to ensure provision for many different customer groups in the area: individual customers, corporate customers, and financial institutions. Typical services are as follows: Payment services, treasury services, guarantee services, card services, trade finance, other services: Western Union, insurance commissions, consulting services, foreign exchange derivatives trading, e-banking services,...

2.2.1.1. Payment services:

In accordance with the Prime Minister's Project to promote non-cash payments in Vietnam [15], banks in Tien Giang province have continuously developed payment services to reduce customers' cash usage habits through card services and electronic banking services such as: salary payment through accounts, focusing on developing card acceptance points, developing multi-purpose cards, paying social insurance by transfer, paying bills through banks, etc.

Chart 2.3. Net income from payment services in the period 2011-2015

Unit: Million VND

6000

5000

4000

3000

2000

1000

0

3922 4065

4720 5084 5324

2011 2012 2013 2014 2015

Net income from payment services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Along with the technological development of the entire system, BIDV Tien Giang has a payment system with a fairly stable transaction processing speed, bringing many conveniences to customers. The results of observing chart 2.3 show that the income from payment services that the Branch has achieved has grown over the years but the speed is not high and the products are not outstanding compared to other banks. Domestic payment products such as: Online bill payment, electricity bills, water bills, insurance premiums, cable TV bills, telecommunications fees, airline tickets, etc. bring many conveniences to customers. Regarding international payment, this is an indispensable activity for foreign economic activities, BIDV Tien Giang is providing international payment methods for small enterprises producing agriculture, aquatic food and seafood that have credit relationships with banks in industrial parks in Tien Giang province such as: money transfer, collection, L/C payment.

2.2.1.2. Treasury services:

BIDV Tien Giang always focuses on ensuring treasury safety and currency security, always complies with legal regulations, and minimizes risks in operations such as: counting and collecting money from customers, receiving and delivering internal transactions, collecting from the State Bank (SBV) or other credit institutions, receiving ATM funds, bundling money, etc. BIDV Tien Giang's treasury service management department is always fully equipped with modern machinery and equipment such as: money transport vehicles, fire prevention tools, money counters, money detectors, magnifying glasses, etc. to ensure absolute safety in treasury operations, immediately identifying real and fake money and other risks that may affect people and assets of the bank and customers. In addition, implementing regulation 2480/QC dated October 28, 2008 between the State Bank of Tien Giang province and the Provincial Police on coordination in the fight against counterfeit money, in the 3-year review of implementation, BIDV Tien Giang discovered, seized and submitted to the State Bank of Tien Giang province 475 banknotes of various denominations and was commended by the Provincial Police and the State Bank of Tien Giang province [17].

Chart 2.4. Net income from treasury services in the period 2011-2015

Unit: Million VND

350

300

250

200

150

100

50

0

105 122

309 289 279

2011 2012 2013 2014 2015

Net income from treasury services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

However, as shown in Figure 2.4, income from treasury operations is not high and fluctuates. Specifically, in the period 2011-2013, net income increased and increased most sharply in 2013, then in the period 2013-2015, there was a downward trend. This fluctuation is due to the fact that fees collected from treasury services are often very low and can even be waived to attract customers to use other services.

2.2.1.3. Guarantee and trade finance services:

BIDV Tien Giang, thanks to the advantages of the province and the favorable location of the Branch, has continuously focused on developing income from guarantee services and trade finance.

Chart 2.5. Net income from guarantee and trade finance services in the period 2011-2015

Unit: Million VND

14000

12000

10000

8000

6000

4000

2000

0

5193 5695

2742 3420

8889

3992

11604 12206

5143 5312

2011 2012 2013 2014 2015

Net income from guarantee services Net income from Trade Finance

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.5, we can see that BIDV Tien Giang's income from guarantee services and trade finance has grown over the years. The reason is: Among BIDV Tien Giang's corporate customers, the construction industry is the industry with the highest proportion of customers after the trading industry, this is a group of customers with potential to develop guarantee services. The second group of customers is corporate customers in the fields of agricultural production, livestock and seafood processing with high import and export turnover in the area.

are the target of trade finance development. In addition, BIDV Tien Giang also focuses on continuously developing these customer groups to increase revenue for many other products and services in the future.

2.2.1.4. Card and POS services:

As a service that BIDV Tien Giang has recently developed strongly, it can be said that this is a very potential market and has the ability to develop even more strongly in the future. Card services with outstanding advantages such as fast payment time, wide payment range, quite safe, effective and suitable for the integration trend and the Project to promote non-cash payments in Vietnam. Cards have become a modern and popular payment tool. BIDV Tien Giang early identified that developing card services is to expand the market to people in society, create capital mobilized from card-opened accounts, contribute to diversifying banking activities, enhance the image of the bank, bring the BIDV Tien Giang brand to people as quickly and easily as possible. BIDV Tien Giang is currently providing card types such as: credit cards (BIDV MasterCard Platinum, BIDV Visa Gold Precious, BIDV Visa Manchester United, BIDV Visa Classic), international debit cards (BIDV Ready Card, BIDV Manu Debit Card), domestic debit cards (BIDV Harmony Card, BIDV eTrans Card, BIDV Moving Card, BIDV-Lingo Co-branded Card, BIDV-Co.opmart Co-branded Card). These cards can be paid via POS/EDC or on the ATM system. In addition, with debit cards, customers can not only withdraw money via ATMs but also perform utilities such as mobile top-up, online payment, money transfer,... through electronic banking services.

In order to attract customers with card services, BIDV Tien Giang has continuously increased the installation of ATMs. As of December 31, 2015, BIDV Tien Giang has 23 ATMs combined with 7 ATMs in the same system of BIDV My Tho, so the number of ATMs is quite large, especially in the center of My Tho City, but is not yet fully present in the districts. Basic services on ATMs such as withdrawing money, checking balances, printing short statements,... BIDV ATMs accept cards from banks in the system.

Banknetvn and Smartlink, cards branded by international card organizations Union Pay (CUP), VISA, MasterCard and cards of banks in the Asian Payment Network. From here, cardholders can make bill payments for themselves or others at ATMs, by simply entering the subscriber number or customer code, booking code that service providers notify and make bill payments.

Chart 2.6. Net income from card services in the period 2011-2015

Unit: Million VND

3500

3000

2500

2000

1500

1000

500

0

687

1023

1547

2267

3104

2011 2012 2013 2014 2015

Net income from card services

(Source: Report on the implementation of the annual business plan of the General Planning Department of BIDV Tien Giang [24])

Through chart 2.6, it can be seen that BIDV Tien Giang's card service income is constantly growing because the Branch focuses on developing businesses operating in industrial parks, which are the source of customers for salary payment products, ATMs, BSMS. Specifically, there are companies such as Freeview, Quang Viet, Dai Thanh, which are businesses with a large number of card openings at the Branch, contributing to the increase in card service fees [25].

Table 2.6. Number of ATMs and POS machines in 2015 of some banks in Tien Giang area.

Unit: Machine

STT

Bank name

Number of ATMs

Cumulative number of ATM cards

POS machine

1

BIDV Tien Giang

23

97,095

22

2

BIDV My Tho

7

21,325

0

3

Agribank Tien Giang

29

115,743

77

4

Vietinbank Tien Giang

16

100,052

54

5

Dong A Tien Giang

26

97,536

11

6

Sacombank Tien Giang

24

88,513

27

7

Vietcombank Tien Giang

15

61,607

96

8

Vietinbank - Tay Tien Giang Branch

6

46,042

38

(Source: 2015 Banking Activity Data Report of the General and Internal Control Department of the Provincial State Bank [21])

Through table 2.6, the author finds that the number of ATMs of BIDV Tien Giang is not much, ranking fourth after Agribank Tien Giang, Dong A Tien Giang, Sacombank Tien Giang. The number of POS machines of BIDV Tien Giang is very small, only higher than Dong A Tien Giang and BIDV My Tho in the initial stages of merging the BIDV system. Besides, BIDV Tien Giang has a high number of cards increasing over the years (table 2.7) but the cumulative number of cards issued up to December 31, 2015 is still relatively low compared to Agribank, Vietcombank, Dong A (table 2.6).

div.maincontent .content_head3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; }

div.maincontent .s1 { color: black; font-family:"Courier New", monospace; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13.5pt; }

div.maincontent .s8 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; }

div.maincontent .s9 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -2pt; }

div.maincontent .s10 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; }

div.maincontent .s11 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -5pt; }

div.maincontent .s12 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -3pt; }

div.maincontent .s13 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: -4pt; }

div.maincontent .s14 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 7.5pt; }

div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s16 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s17 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9.5pt; }

div.maincontent .s18 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s19 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s20 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -2pt; }

div.maincontent .s21 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; }

div.maincontent .s22 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s23 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -3pt; }

div.maincontent .s24 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -5pt; }

div.maincontent .s25 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s26 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s27 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -6pt; }

div.maincontent .s28 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -1pt; }

div.maincontent .s29 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s30 { color: black; font-family:Calibri, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s31 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; }

div.maincontent .s32 { color: black; font-family:.VnTime, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; }

div.maincontent .s33 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; }

div.maincontent .s34 { color: black; font-family:Cambria, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10.5pt; vertical-align: -4pt; }

div.maincontent .s35 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11.5pt; }

div.maincontent .s36 { color: black; font-family:Arial, sans-serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; }

div.maincontent .s37 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 13pt; }

div.maincontent .s38 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; }

div.maincontent .s39 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 15pt; }

div.maincontent .s40 { color: black; font-family:"Times New Roman", serif; font-style: normal; fo -

Strengthening Control, Restriction and Gradually Eliminating Activities of the Unofficial Foreign Exchange Market

Strengthening Control, Restriction and Gradually Eliminating Activities of the Unofficial Foreign Exchange Market

Foreign currency demand of people going abroad for work, tourism, medical treatment ...: The foreign currency demand of this group also increases every year and they often buy foreign currency at the official exchange rate of the bank, so most of them turn to TTKCT with a quick way of buying and selling that does not require documents but almost meets their needs.

The foreign currency needs of import companies , private or state import enterprises, they often encounter situations when they need to buy foreign currency to pay for imported goods, but the bank does not have enough foreign currency to meet this demand in time, which greatly affects production and business activities and there is a risk of having to compensate for the contract, or they have to bear additional costs when the goods have arrived at the port such as storage fees, yard fees, etc. without foreign currency to pay for receiving the goods, so by all means they must buy foreign currency and they turn to TTKCT.

And finally, the demand for foreign currency of smugglers, smuggling activities certainly cannot be carried out without foreign currency provided by TTKCT. Smuggled goods such as gold, foreign currency, luxury goods, alcohol, motorbikes, etc. have a very large demand for foreign currency and the exchange rate on the unofficial market is most affected by this demand for foreign currency. During periods when the domestic gold market fluctuates, the domestic gold price is higher than that of foreign countries, smugglers will collect foreign currency to import goods from abroad to sell for a profit difference, this activity has clearly affected the foreign currency price because the amount of foreign currency for each gold import is millions of USD. In an article on the Government's website, Governor of the State Bank of Vietnam Nguyen Van Binh stated: "Smuggling of gold across the border is very common and on an increasingly large scale, the average annual import of smuggled gold is from 20 to 40 tons." [ 77]

Thus, the supply and demand factors for a foreign exchange market to exist are real and in fact, the foreign exchange market in Vietnam has developed strongly for a long time, estimated to account for about 20% of the market share [14] and this market is increasingly competing strongly with the official market.

In summary, the existence of TTKCT is due to the following reasons: (1) The difference in exchange rates on the official foreign exchange market and the exchange rate on TTKCT ; in a country where there are different exchange rates, there will be a foreign exchange market that exists in parallel with the official market. (2) In conditions where the macro economy is unstable, people are not confident when holding VND, they want to store it.

The existence of an unofficial foreign exchange market causes a large amount of dollars to float uncontrolled among the population and increases the dollarization of the economy. This is also a fertile ground for underground economic activities and other illegal business activities. This shows that the existence of an unofficial foreign exchange market not only destabilizes the banking system, makes it difficult for the State Bank to operate monetary and exchange rate policies, but also contributes to hindering the authorities in controlling underground economic activities and preventing other illegal business activities.

2.4 The role of the State Bank of Vietnam in the Vietnamese banking system in the recent period

2.4.1 Performing the role of intervening in the foreign exchange market and operating exchange rate policy

The deeper the international integration process, the more the banking market is affected, with positive and negative impacts on the market. The State Bank, with its role in implementing monetary policy through intervention in the banking market and using the exchange rate management mechanism, thereby performs the ultimate role of the State Bank in the banking market, to take advantage of favorable impacts and overcome negative impacts on the market, ensuring stable market operation and development.

When it began to open its economy, Vietnam faced its first financial crisis, the financial-monetary crisis that occurred in Southeast Asia in 1997, starting from Thailand, then spreading rapidly throughout the region and

has a global influence, Vietnam is not exempt from that influence. These are difficult and challenging years for the Vietnamese economy, due to the impact of natural disasters and the financial and monetary crises of countries in the region. With such an economic context, the State Bank has adjusted the exchange rate mechanism to be relatively more flexible than in the previous period. Specifically:

In 1997, the trading band was expanded to +/- 5%, then increased to +/- 10%, and the official exchange rate was increased once at the end of the year. In 1998, there were two important adjustments to the official exchange rate: Phase 1 increased the exchange rate by 5.59%; Phase 2: increased by 10% and loosened the fluctuation band from +/- 5% to +/- 10% and then decreased.

+/-7%.

The strong devaluation of VND in 1998 was considered reasonable because the USD increased sharply and currencies in the Southeast Asian region all depreciated due to the impact of the financial and monetary crisis and these countries have similar export products to Vietnam, so the increase in exchange rate will increase the competitiveness of Vietnam's exports and is considered the reason why Vietnam's exchange rate does not have strong fluctuations like the exchange rate of Southeast Asian countries.

On February 25, 1999, the State Bank issued Decision 64/1999/QD_NHNN7 on the announcement of the exchange rate of the Vietnamese Dong, according to which: "Every day, the State Bank announces the average transaction exchange rate on the Interbank Foreign Exchange Market of the Vietnamese Dong against the US dollar, instead of announcing the official exchange rate and the average interbank buying and selling exchange rate on the Interbank Foreign Exchange Market." This decision shows the change in the State Bank's exchange rate management before the economic integration process. The wide announcement of the BQLNH exchange rate on the mass media creates conditions for entities with foreign currency transactions to easily access official information on exchange rates to develop business strategies and implement exchange rate risk insurance.

Since joining the WTO, there have been significant changes in exchange rate management. The BQLNH exchange rate has been changed more often and not fixed for too long (like before, in 2005, there were only 2 exchange rate adjustments, the first in January).

1/2005, 2nd phase in December 2005). In early 2007, the State Bank adjusted the margin from 0.25% to 0.5% and with the exchange rate increasing by 1.38% since the end of 2006, the exchange rate was expected to continue to increase. However, in 2007, when FDI, FII and remittance flows increased sharply, causing pressure to increase the VND price, the State Bank circulated 200,000 trillion VND to buy foreign currency, increasing foreign exchange reserves to 20 billion USD and encouraging commercial banks to buy USD, but commercial banks could not buy much because they were controlled by foreign currency status limits and affected business results. This is the stage that requires the intervention of the State Bank to buy foreign currency, but how much to buy to match the monetary policy and the determined exchange rate, the State Bank has not intervened appropriately with the market's requirements and as a result, the exchange rate on the official market is higher than the free market.

Statistics show that from June 2008 to February 2011, the State Bank adjusted the interbank exchange rate 6 times: In 2008, there were 2 adjustments with an increase rate of 1.99% and 3%, with 2 times changing the amplitude from +/- 1% to +/- 2%. Based on the forecast of the world economic situation in 2009, the State Bank raised the average exchange rate on the interbank market by 3%. This is a sudden change in exchange rate management compared to previous times, which was only around less than 1% and the following years, the exchange rate was adjusted higher than before, in 2009 it increased once by more than 5%, in 2010 it increased twice by more than 3% and more than 2% and in early 2011, after a period of restraint, the State Bank strongly devalued VND by 9.3% compared to USD[71]. This move shows that the State Bank believes that the exchange rate on the interbank market does not accurately reflect the market price, so no matter how much the margin changes, it still does not reduce the difference between the exchange rates of the two markets. Therefore, the issue is to review the exchange rate determined by the interbank market where the turnover only accounts for a small proportion of the foreign currency turnover of the entire economy, does it reflect the real value of VND or not?

Synchronously combine measures to impact foreign currency supply and demand during periods of foreign currency shortage, one of the reasons being that enterprises with foreign currency revenue continue to hoard foreign currency without selling it to banks. The State Bank has implemented measures such as: (1) raising the margin

(2) strictly control foreign exchange trading activities of credit institutions to ensure that credit institutions strictly implement foreign exchange management regulations on listing and trading;

(3) At the same time, strengthen propaganda to stabilize people's psychology and implement measures to create consensus among commercial banks, agree to increase USD mobilization interest rates and reduce foreign currency lending interest rates to overcome the imbalance between foreign currency supply and demand. The above measures of the State Bank have helped the foreign exchange market in the third quarter of 2009 to be relatively stable.

Based on the causes of the tension in foreign currency demand, the State Bank has taken appropriate measures. At the end of 2009, the imbalance in foreign currency supply and demand reappeared, the cause of which was the impact of information on the increasing trade deficit and declining foreign exchange reserves, especially under the impact of the gold fever, the high domestic gold price caused a sudden increase in foreign currency demand due to speculators stepping up the purchase of USD to buy gold. In this situation, the State Bank immediately announced the import of gold to reduce pressure on gold prices and increased the BQLNH exchange rate to 5.44%; narrowed the margin from ±5% to ±3% and increased the basic interest rate of VND to 8%. With the above measures, Vietnam's banking system has temporarily stabilized, the phenomenon of hoarding and hoarding foreign currency has gradually been overcome.

In 2010, the SBV simultaneously implemented measures to

affecting the tense foreign currency supply, that is (1) adjusting the exchange rate upward

(2) sharply reduce the foreign currency reserve requirement ratio for credit institutions [34]. Reducing the foreign currency reserve requirement ratio from 7% to 4% for terms under 12 months, from 3% to 2% for terms over 12 months has created conditions for commercial banks to increase foreign currency lending in the market. (3) stipulate the maximum deposit interest rate ceiling in USD of economic organizations at credit institutions is

1%/year [34] to reduce the hoarding of foreign currency in accounts and switch to selling foreign currency to increase the supply of USD.

In summary, since joining the WTO, in the face of market fluctuations due to causes from the world economy and the domestic situation, the State Bank has operated the exchange rate policy with changes in the frequency of impact and adjustment of the amplitude, combined with other measures to limit the tension in foreign currency supply and demand such as regulations on ceiling interest rates on foreign currency deposits, reducing the required reserve ratio of USD, in addition to implementing measures to impact the psychological factor that causes tension in our country's foreign currency by using the media to officially announce the direction of exchange rate intervention to limit rumors that cause public confusion.

2.4.2. Measures to limit the activities of the unofficial foreign exchange market.

The issuance of the Foreign Exchange Ordinance [39] as a legal basis to regulate activities related to foreign exchange is a step forward in the process of building an institutional framework to operate the foreign exchange market, but since its issuance, monitoring and using sanctions against violations of the Foreign Exchange Ordinance have not been given much attention, but only inspections, checks and penalties are carried out when the foreign exchange market encounters difficulties in foreign currency supply and demand, exchange rate tensions, etc.

In 2008, after a series of actions by the State against the stock market, which peaked around mid-2008, the stock market was quiet for a while, at times almost frozen, but then the market became active again due to the State's negligence in inspection.

The State Bank of Vietnam issued directives to inspect and handle violations in foreign currency trading and price listing [17] to limit the foreign exchange market and dollarization. However, in 2010, foreign currency trading activities on the foreign exchange market were still bustling because at that time the exchange rate difference between the two markets was very high, sometimes up to 2000 VND, most commercial banks could not buy foreign currency, leading to a situation of foreign currency tension while the demand for payment for imported goods increased.

The State Bank of Vietnam, in coordination with relevant agencies, has implemented many strong measures to limit the existence of the foreign exchange market, such as: completely banning the buying and selling of foreign currencies outside the bank, accompanied by sanctions such as confiscating foreign currencies, and at the same time making recommendations to limit the trading of gold bars outside the official market. During this time, the foreign exchange market has shrunk and is no longer as active as before, and more foreign currencies have flowed into the bank. However, the pressing problem has arisen that the legitimate foreign currency needs of the people are not met by the bank, and they have to secretly buy on the foreign exchange market at much higher prices.

2.5. Evaluation of the development process of Vietnam's TTNH in recent times and the causes of existing problems

2.5.1. Achievements

Firstly, it has built the legal foundation for the operation of TTNH.

TTNH operates according to the regulations issued [29] which are basically in accordance with the Law on the State Bank and the Law on Credit Institutions, ensuring that market operations comply with the law. At the same time, the legal basis for foreign exchange trading activities is gradually being improved. The State Bank has built a system of legal documents on foreign exchange management activities with a higher level of legalization, no longer in the form of decrees but in the form of ordinances (Foreign Exchange Ordinance issued in 2005), creating an environment for the operation and implementation of exchange rate policies, foreign exchange management and foreign exchange trading within the framework of the law.

Foreign exchange regulations meet the requirements of Article VIII of the GATT 1994, current account control measures have been liberalized, foreign exchange controls are only applied in exceptional cases to maintain national financial and monetary stability.

The State Bank has established a foreign exchange trading center to create a basis for activities.

operation of a foreign exchange, but the payment and transaction mechanisms