is focused by the Government. The Indonesian Government has established the “National Fleet Development Company” to provide financial assistance to shipping companies in purchasing ships. The main policies to encourage fleet development are:

- Policy on the right to transport goods: Indonesia is a country that has participated in the division of transport rights according to the Liner Code of the World Trade Organization, specifically: signed with the Singapore Shipowners Association, bilateral agreements on the transport of goods with Japan, Taiwan and North Korea. Particularly for the transport of import and export goods with financial resources from the Government, it must be reserved for the national fleet or ships chartered by Indonesians. In case Indonesian ships are not capable of transporting, the Government will allow foreign ships to participate in the transport, but the main policy is still to limit the licensing of international Liner ships.

- The policy of restricting entry and exit for foreign ships at some Indonesian ports is also a policy to protect and facilitate the development of the national fleet, for example: all importers and exporters of goods other than petroleum must load goods at one of four ports: Belawan, Tanjung, Jungjung and Perak, and ships can only unload import and export goods at one of the 48 ports open to foreign ships.

- The policy of not opening the domestic shipping market is still strictly implemented by Indonesia to protect the development of the national shipping fleet.

- Implement an open policy in ship registration. Compared to Thailand, the proportion of foreign-flagged ships of Indonesian ships is higher - accounting for 16.88% of the total (Table 1.3).

1.5.1.4 Philippines

The Philippines is an archipelagic country, international shipping and inland shipping play a particularly important role in the country's economic development. In addition

Implementing an open registration policy for ships like other countries in the region, the fleet development policy mainly focuses on:

- Policy to encourage cargo owners: Import and export goods when transported by Philippine ships are reduced in freight rates and shipping costs. Unlike Thailand's view, the Philippines believes that this policy has encouraged Philippine importers and exporters while protecting the national fleet.

- Cargo allocation policy: The Philippines has been a party to the Liner Act since 1975. The Philippine government has applied the principle of cargo allocation into Philippine law. Goods with direct or indirect financial sources from the Government are still reserved for the national flag fleet, foreign ships are only allowed to transport in cases where Philippine ships are unable to transport.

- Financial support policy: The government sponsors and provides preferential loans to develop the fleet and modernize maritime transport. The domestic maritime transport modernization program is a policy-based loan program of the Philippine government and the Philippine Development Bank - considered the executive agency, while the Japan Bank for International Cooperation is the funding agency [11, p.I-4-3].

- Tax policy: a 1997 tax reform law stipulates that only Filipino seafarers working on ships operating on domestic shipping routes are required to pay income tax. At the same time, the Philippine government also issued the International Shipping Development Act 3, p.I-17 , which stipulates: exemption from import tax on ships and spare parts for overhaul and repair of ships operating on international shipping routes; reduction of income tax for businesses operating on international shipping routes (from 1992-2002) on the condition that businesses spend 90% of net revenue on fleet modernization.

1.5.1.5 Malaysia

- Tax policy: To encourage the development of the fleet, the Government does not impose rigid import taxes on imported ships, for example: applying a tax rate of 30% for ships under 26 GRT, 10% for ships from 26-4,000 GRT, and at the same time exempting import taxes on ships with a registered capacity of over 4,000 GRT [11, p.I-4-3]. This policy has really encouraged the use of large tonnage ships.

- Financial policy: Malaysia has established the Industrial Bank and the Maritime Transport Fund. The bank provides capital to domestic shipyards, and shipping enterprises wishing to borrow capital to invest in ships must purchase ships at domestic shipyards, unless these factories do not meet the requirements, then they have the right to purchase ships abroad. This bank creates a solid foundation for Malaysia to become a country with a developed maritime industry in the region by providing financial instruments for building new ships, purchasing used ships, and providing working capital for shipping enterprises. In addition, Malaysia has also established a large financial center to attract and concentrate foreign financial institutions to provide financial instruments without having a representative office at this center. This is an important channel to meet the capital needs for developing the fleet. The Government's maritime transport fund has also created conditions for maritime transport enterprises to expand and modernize their fleets, increase transport capacity, meet the needs of transporting import and export goods and develop the country's economy.

- Domestic shipping policy: Although Malaysia does not have a policy of reserving goods for domestic transport to protect the national fleet like some countries, the transportation of goods between domestic ports is only for the national fleet and is limited to foreign ships.

- Crew policy: Malaysian-flagged ships are only allowed to hire foreign crew members to work on board up to 25% of the ship's crew size.

This policy facilitates local seafarers to work on Malaysian-flagged vessels, while also opening up opportunities to gain practical experience working alongside foreign seafarers.

1.5.1.6 China

To develop the maritime transport fleet, especially the fleet operating on international routes, China has used investment incentive policies, provided loans for fleet development with low interest rates, reduced transport turnover tax, encouraged the private sector to participate in international maritime transport, and applied many open policies to attract investment capital for the development of the national fleet. By the end of 2000, China had 2,300 ships with a total tonnage of 50 million DWT, of which 20 million DWT participated in international routes 51, p.20 , by 2006 this number had reached 2,893 ships with a total tonnage of over 65 million DWT (Table 1.3), of which 35 million tons were registered under foreign flags. China is one of the world's major powers in maritime transport and shipbuilding. Domestic commercial banks (China Exim Bank, Bank of China, Industrial Commercial Bank of China) and foreign credit institutions are the sources of capital for investment in the development of China's shipping fleet.

1.5.1.7 Japan

As a country with a strong economic development, the main policy to develop the national fleet is to invest in using large-tonnage ships. Since the 1950s, Japan has used ships of 10,000 DWT - 20,000 DWT and in the early 1960s it reached 100,000 DWT. The policy of using large-tonnage ships has brought success to Japan, the transport capacity of the national fleet has increased, meeting the demand for transporting goods and raw materials for production, reducing transportation costs... In addition, Japan also maintains an open registration policy for ships, implementing the policy of

According to the "flag of convenience" policy, by 2006, 77.13% (Table 1.3) of the total number of Japanese ships flying foreign flags were conducting business on international routes and the country with the largest number of foreign flagged ships in the Asian region in recent years has truly affirmed the growth of the Japanese fleet in the international shipping business.

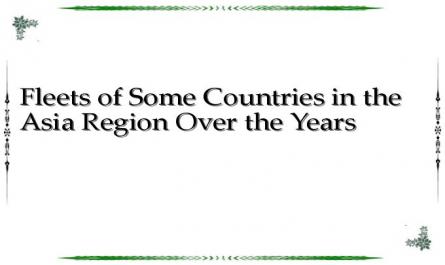

Thus, using appropriate fleet development policies, most of the fleets of Japan, China, Singapore, Malaysia, Indonesia, Philippines, Thailand (- a country ranked in the group of 35 countries with strongly developed maritime industries in the world) always have an increase in both quantity and total tonnage, table 1.4 [55, 56, 57, 58, p.33] is specific data:

Table 1.4 : Fleets of some countries in the Asian region over several years

Country name

Number of ships (units) | Ship's deadweight (1000.DWT) | |||||

2003 | 2005 | 2006 | 2003 | 2005 | 2006 | |

Japan | 2,910 | 2,945 | 3,091 | 104,396 | 117,662 | 131,703 |

China | 2,321 | 2,612 | 2,893 | 44,304 | 56,812 | 65,488 |

Singapore | 714 | 740 | 754 | 19,392 | 22,333 | 22,980 |

Malaysia | 306 | 327 | 325 | 6,589 | 9,835 | 9,633 |

Indonesia | 610 | 672 | 711 | 4,315 | 5,754 | 6.231 |

Philippines | 336 | 326 | 312 | 4,847 | 5.008 | 5.023 |

Thailand | _ | 297 | 318 | _ | 2,982 | 3,198 |

Maybe you are interested!

-

Nakao, T. (2020), 'The Asia And Pacific Region: Development Achievements, Challenges And The Role Of The Adb', Asian‐Pacific Economic Literature, 34(1), 3‐11.

Nakao, T. (2020), 'The Asia And Pacific Region: Development Achievements, Challenges And The Role Of The Adb', Asian‐Pacific Economic Literature, 34(1), 3‐11. -

The Impact of Financial Integration on Poverty in Developing Countries in Asia.

The Impact of Financial Integration on Poverty in Developing Countries in Asia. -

In terms of space, the research topic is the relationship between two subjects in the Asia-Pacific region, the United States and Vietnam, on the economic level.

In terms of space, the research topic is the relationship between two subjects in the Asia-Pacific region, the United States and Vietnam, on the economic level. -

Experience of Some Countries in the Region in Improving the Quality of State Administrative Civil Servants

Experience of Some Countries in the Region in Improving the Quality of State Administrative Civil Servants -

De Gruyter, C., Currie, G., Rose, G. (2017). Sustainability Measures Of Urban Public Transport In Cities: A World Review And Focus On The Asia/middle East Region . Sustainability, Vol. 9, No. 1,

De Gruyter, C., Currie, G., Rose, G. (2017). Sustainability Measures Of Urban Public Transport In Cities: A World Review And Focus On The Asia/middle East Region . Sustainability, Vol. 9, No. 1,

Source: UNTAD Secretariat compiled based on data from Lloyd's Register

- Fairplay provides the common fleet development policy of these countries mainly focusing on not opening up domestic shipping routes to reserve the right to transport goods for the national fleet, maintaining an open policy on ship registration, and providing capital support to develop the national fleet.

1.5.2 Port development policies of some countries

1.5.2.1 Japan

Japan is an island nation, maritime transport tends to play a particularly important role in the country's economic development. Due to the fierce competition of the industry in the international market, the Japanese industry wants to survive and develop, the top priority is to reduce production costs while still ensuring quality. There are many measures implemented, in which reducing costs through transporting raw materials by large-tonnage ships has really brought about efficiency. Therefore, the construction of deep-water ports to receive large ships has been built throughout Japan, especially the policy of renovating the existing port system since the early 19th century, this policy mainly includes:

- Policy on selection and improvement of important ports (resolution passed by the Port Council on 10/1907). Through the Port Council's charter (established by the Ministry of the Interior) on port facilities, planning and income from ports, 14 ports were selected by the Port Council and divided into 2 categories, category 1 ports and category 2 ports. Category 1 ports (including 4 ports) are ports managed and built by the state with financial contributions from relevant local authorities; category 2 ports (including 10 ports) are ports managed and operated by local authorities with state subsidies. All other ports are placed under the autonomy of relevant local authorities and do not receive subsidies from the government 40, p.6 . To date, the number of Type 1 ports has remained unchanged, the number of Type 2 ports has reached 37, the additional ports have been classified by the Ministry of the Interior based on the recommendations of the Port Council. Clear port classification is a transparent basis for determining investment and port management rights.

- Subsidy policy for the renovation of designated ports. In addition to the ports that have been designated as particularly important ports, the remaining ports (which have been designated) under the management of relevant local authorities are still subsidized by the state for 1/3 of the cost of renovation work.

- Port management and development policy: This policy is built on the basis of various laws, decrees and regulations, of which the Port Law is the most basic law. The basic content of the port management and development policy is that Japanese ports are under the management of port authorities - the authority to develop, use and maintain ports. The State only has minimal supervisory rights to protect national interests.

- Japan's long-term port policy: In October 1997, the Japanese government announced a new long-term port policy titled "Ports in the Decade of Global Exchange". This new policy has been officially used and is the basic guiding method for port development in Japan 53, p.4 . The basic directions of the policy are: Improving berth capacity; developing upgraded industrial zones in the land behind the ports to stimulate the regional economy, creating employment opportunities in the local area; protecting and creating a good environment for the future; promoting disaster prevention programs, protecting the stability of coastal areas. The important points of port management according to the above policy are: the role of the government; developing and using new technology; coordinating policy implementation; supporting port development activities.

1.5.2.2 China

- China's policy of reforming the port management system: clearly distinguishing the state economic management function from the production and business management function, on that basis forming a management system in accordance with advanced port management practices in the world. The steps are shown [5, p.19]:

+ Port enterprises and factories separated from the Ministry of Transport

+ Administrative management functions assigned to local authorities

+ The port fee collection policy is based on the Fee Collection Rules issued by the Ministry of Transport on July 20, 1997. Fees for foreign ships are uniformly regulated by the state, fees collected at domestic ports are based on state-directed prices, and at joint venture ports are based on market prices. The main viewpoint of the port fee policy is to minimize unnecessary fees and increase the number of ships entering the port. Therefore, the port fee level in China is lower than many ports in the world.

- Investment policy for seaport development: Focus on investing in building deep-water wharves, this policy is shown in the 9th 5-year plan (1996-2000), China spent 42.1 billion Yuan to build seaports, 133 large and medium-sized wharves were built, including 96 deep-water wharves, thereby increasing the volume of goods passing through to 190 million tons, the capacity to handle container cargo reached 8.48 million TEU 51, p.20 . The investment policy for the period 2001-2005 is still issued and implemented by the Chinese government, the plan is that by 2005 the number of deep-water wharves will be 800; Investment capital for ports can be mobilized from: the state budget, loans from international organizations as well as domestic and foreign banks, and at the same time, private and foreign economic sectors are encouraged to invest in port construction and loading and unloading business. Therefore, by 1998 alone, China had attracted 2.6 billion USD in foreign investment to build 40 container terminals with a capacity of 80 million tons, accounting for 66% of the volume of containers passing through Chinese ports 5, p.20 . Since March 2002, China has implemented an open-door policy to receive foreign investment in seaports. Since implementing the open-door policy to foreign investment in seaports, in 2003, foreign investment in seaports reached 18 billion Yuan [46].