Debt collection turnover | |

Credit capital turnover | = |

Average outstanding balance |

Maybe you are interested!

-

Factors Affecting the Efficiency of Working Capital Use in Enterprises

Factors Affecting the Efficiency of Working Capital Use in Enterprises -

Indicators for Evaluating Capital Utilization Efficiency at Khanh Ha Import-Export Trading and Transport Company Limited

Indicators for Evaluating Capital Utilization Efficiency at Khanh Ha Import-Export Trading and Transport Company Limited -

Group of Indicators for Efficiency of Capital Use in Production and Business

Group of Indicators for Efficiency of Capital Use in Production and Business -

Overview of Research on Factors Affecting the Linkage of Small and Medium Enterprises with Enterprises with Direct Investment Capital

Overview of Research on Factors Affecting the Linkage of Small and Medium Enterprises with Enterprises with Direct Investment Capital -

Cronbach's Alpha Reliability Coefficient of Components of the Scale of Factors Affecting Investment Capital Attraction for Tourism in Ba Ria Vung Tau Province

Cronbach's Alpha Reliability Coefficient of Components of the Scale of Factors Affecting Investment Capital Attraction for Tourism in Ba Ria Vung Tau Province

Credit turnover is used to measure the speed of capital circulation of bank credit, it shows the time to collect debt quickly or slowly. If the credit turnover is fast, it means that the bank's capital investment in production and business is highly effective.

Net profit after tax

Profit is the final measure in the business performance report, a financial performance indicator that commercial banks pay special attention to. Profit is a measure of the ability to create value for shareholders, create additional business capital and maintain or improve the reputation of the bank. Profit is also a measure of the capacity of the management and operation in relation to the quantity and quality of the assets and capital of the bank.

Profit after tax = (Interest revenue - interest expense + other revenue - other expenses - loss provision) x (1 - corporate income tax rate)

There are many factors that make up the after-tax profit index.

- Interest revenue

Interest revenue = Interest revenue from credit + interest revenue from deposits + interest revenue from securities = ∑ (Balance from interest-bearing loan contracts in the period x loan interest rate + Balance of interest-bearing deposits in the period ix × deposit interest rate i + face value of interest-bearing securities in the period ix × interest rate i)

Interest revenue is calculated for each detailed asset item, each customer group with different interest rates, different times. Interest revenue is an important result indicator of primary concern for banks. For most commercial banks, interest revenue accounts for the majority of revenue and determines the size of net income.

The factors that make up the interest income of a commercial bank are the size, structure, interest period and interest rate of interest-bearing assets and overdue debts. If the bank has a portfolio of high-risk assets, the expected interest income will be high. The interest rate is determined by the market. Commercial banks

25

To increase interest revenue, it is necessary to increase the scale of interest-bearing assets, increase the proportion of assets with high interest rates and limit losses. Thus, interest revenue reflects the business capacity of very important capital-using activities in commercial banks such as credit and investment. Therefore, the indicators of interest revenue from credit activities/average outstanding loans and interest revenue from investment activities (bonds)/bond outstanding loans are also used by commercial banks to reflect the efficiency of these two types of activities.

- Interest expense

Total interest expense during the period = interest payments on deposits + interest payments on loans = ∑ (Deposit balance subject to interest payment during period ix interest payment rate i + Balance from loan contracts subject to interest payment during period ix interest payment rate i)

Interest payments are the largest expense of banks and tend to increase due to the increase in the scale of mobilization as well as the mobilization term (higher interest rates when the mobilization term is longer). Interest payments depend on the scale of mobilization, mobilization structure, mobilization interest rate and form of interest payment during the period.

- Basic interest rate difference

Basic interest rate spread = (Interest revenue - interest expense)/ Average interest-earning assets

Capital use activities of commercial banks can be divided into activities that create interest-bearing assets and non-interest-bearing assets. Therefore, the basic interest rate spread reflects the efficiency of capital use for interest-bearing assets.

- Other revenue

In addition to interest income, banks also have other income such as fees (guarantee fees, L/C opening fees, payment fees, etc.); income from foreign currency and gold trading (difference in buying and selling prices, commissions for buying and selling on behalf of others); income from securities trading (fees, difference in buying and selling prices, dividends); fines, and other income. Many incomes are calculated as a percentage of fees to service revenue, such as money transfer fees, L/C opening fees, etc.

With the development towards diversification, and the support of information technology, other services (besides lending) are constantly developing, increasing

26

Thang Long University Library

increase other income, especially for large banks near financial centers.

Many other revenues arise directly from asset items, such as dividends or the difference in the buying and selling prices of securities. Therefore, when calculating the efficiency (revenue) from investment activities, managers include interest income, dividends and price differences.

Other factors that directly affect revenue are the diversity of banking services, service quality, and a favorable environment for the development of these services.

- Other costs

Other expenses include salaries, insurance, fees (electricity, water, postage...), office expenses, depreciation, rent, advertising, training, other expenses...

Salary expenses are usually the largest expense among other expenses, and tend to increase. For banks that pay fixed salaries, salary and insurance expenses are calculated based on the unit price of salary and the number of bank employees. For banks that pay based on final results, salaries are calculated based on net income before tax, ensuring that the bank can cover other expenses besides salaries. Other expenses are allocated (directly and indirectly) to the bank's activities. For example, salaries and management expenses of the credit department are included in the expenses for credit activities to determine the net income of credit activities. Effective management of expenses (other expenses) contributes to increasing the efficiency of capital use. Managers can use the outstanding debt (lending activities) / management expenses of the credit department to evaluate the efficiency of capital use (credit activities).

- Loss provision

Provisions for losses during the period depend on the provisions on the provision rate and the provisioning object. The provisioning rate may be prescribed by the State management agency based on the average loss rate of a number of years in the past; (usually problem loans or overdue debts are the objects of provisioning).

Loss reserves are established to offset losses in commercial banking operations, such as credit risk, interest rate risk, exchange risk,

27

payment risk, operational risk... Risks are losses that can occur unexpectedly. Thus, bank risks must be associated with unexpected declines in income.

* Investment and lending scale indicators

- Loan turnover : is a basic indicator to evaluate the general loans of commercial banks at certain times, and it also reflects the scale of investment and lending capacity in a certain period. With this indicator, we know the ability to circulate and use capital of the bank, from which we can evaluate and make judgments about the bank's operating situation. In addition, loan turnover is also the basis for accurately determining the bank's short-term credit capital turnover.

- Outstanding loans : is the amount at the end of the planning period reflecting the credit relationship between the bank and the customer. This is also an indicator reflecting the investment and lending capital of the bank that has not been recovered and the relationship between capital mobilization and capital use of the bank.

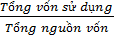

- Capital utilization ratio : is an indicator reflecting the ability to use capital compared to total capital sources according to the formula:

Capital utilization ratio =

The capital utilization ratio is always less than 1. Because banks always have to maintain a certain amount of reserves to meet customers' payment and disbursement needs when necessary. It generally reflects the bank's capital utilization situation. The higher this ratio is, the more the bank has fully utilized the mobilized capital for business activities to make a profit. If this ratio is low, it shows that the bank has not properly balanced the mobilized and used capital. This can cause the bank to encounter many problems such as increasing the opportunity cost of preserving money, the cost of paying interest on mobilized capital, etc., thereby affecting the bank's business activities and profits.

28

Thang Long University Library

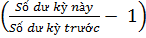

- Growth rate of profitable capital use activities

Growth rate =  × 100

× 100

Growth rates are calculated separately for each specific earning activity. A positive growth rate indicates an expansion in earning activities, a negative growth rate reflects a contraction in activities.

For customer lending activities, which are the main profit-making activities of commercial banks, according to Circular No. 49/2004/TT-BTC dated June 3, 2004, this rate must be ≥ 10%. At the same time, when assessing the growth rate, ensuring compliance with the credit limit limits set for each period must be considered.

For capital contribution investment activities to purchase shares: banks are only allowed to use charter capital and capital reserve fund to supplement charter capital to participate in capital contribution. Growth must ensure compliance with the prescribed limits. According to Decision 457/2005/QD-NHNN dated April 19, 2005 of the State Bank promulgating regulations on capital contribution to purchase shares of credit institutions, Decision No. 03/2007/QD-NHNN, Decision No. 34/2007/QD-NHNN amending and supplementing Decision 457:

The maximum level of capital contribution and share purchase of a credit institution in a commercial investment shall not exceed 11% of the charter capital of the enterprise or investment fund or 11% of the investment value.

The total investment in capital contribution and share purchase in all commercial investments of a credit institution shall not exceed 40% of the charter capital and reserve fund of the credit institution.

In case of investment in a commercial investment exceeding the above ratio, it must be approved in writing by the State Bank.

1.3.4 Factors affecting the efficiency of capital use of commercial banks

29

1.3.4.1 Uncontrollable factors

Factors affecting the efficiency of capital use of banks in the context of international integration are reflected in: Legal environment; Economic environment; Socio-cultural environment; Competitors.

+ Legal environment : In general, the legal environment related to the financial and banking sector has been improved in many aspects.

One is: Perfecting the mechanism related to monetary, foreign exchange, payment policies and regulations on the organizational structure and operation of the Board of Directors (BOD), Supervisory Board (BOS) and Executive Board (EO) of commercial banks.

Second: Perfecting the credit mechanism to guarantee loans

Third: The Government has issued a Decree on registration of secured transactions. Fourth: Completing the foreign exchange management mechanism, there is a foreign exchange ordinance. Fifth: Completing the mechanism and policies on payment, interest rates,...

+ Economic environment: Despite many fluctuations at home and abroad, joint stock commercial banks have been developing and restructuring to improve competitiveness, develop banking services, and increase profits.

+ Cultural and social environment: The modern economic development leads to an increasing demand for banking transactions. In recent years, banking services and utilities have developed, especially the development of ATM card issuance and payment. People have the need to open personal accounts to easily transact and buy and sell.

+ Competitors: Essentially, it is a comprehensive study of the capital market and the money market in each development period. The goal is to analyze each type of competitor in each type of product supplied in the market to have a theory in finding the comparative advantage of your bank in the competitive environment so that it is most beneficial. The biggest advantage of Vietnamese commercial banks is the potential of a branch network spread across the "home field" with a very large market capacity, traditional customers have been shaped quite clearly in reality and all activities of the bank.

30

Thang Long University Library

Banks are always the subject of attention of the Party, the State and all levels and sectors. It is necessary to exploit that advantage to the maximum for the business activities of each bank.

The banking service business environment has changed in a favorable direction - there has been a change in the strategy of groups of competitors in the banking sector. This is reflected in the fact that some foreign bank branches have begun to shift their business strategy towards a wider penetration of the banking service market along with the process of opening up the financial market:

- Target customers: Maintain traditional customers, while approaching domestic enterprises and some State-owned corporations, and individual customers.

- Strategic banking services: Continue to maintain banking services with many competitive advantages, while expanding retail banking services, including consumer lending.

- Distribution channels: Expand through electronic distribution channels, remote transactions (internet, telephone and ATM) and link with strategic partners and domestic commercial banks in general, joint stock commercial banks in particular to jointly deploy new banking services and exploit potential market segments.

Changes in business strategy show that commercial banks of different types, both domestic and foreign, converge more on customer strategy and products, services, and different strategic solutions due to the influence of competitive advantages, philosophy and business culture of each commercial bank. This brings about different results and value added levels among commercial banks.

1.3.4.2.Controllable factors

Controllable factors affecting the competitiveness of capital use of commercial banks in the context of international integration, reflected in: Capital scale and financial situation; banking products and services

31

supply; science and technology; human resources; business strategy and control systems; organizational structure; reputation and seniority of the bank.

+ About capital scale and capital usage

The biggest challenge for commercial banks in banking activities today when participating in international integration is that their equity capital is too small. Therefore, their capacity to use capital is limited.

- Regarding service provision: In the context of Vietnam's economy integrating more and more deeply with the region and the world, the banking service market has made strong developments and is quite active. Participating in banking services in the market, in addition to state-owned commercial banks, joint-venture banks, foreign bank branches, and joint-stock commercial banks, there are also non-bank credit institutions. The promotion of modernizing banking technology, applying information technology and expanding the transaction network has created conditions for the development of banking services. Currently, banking services of Vietnamese commercial banks in general and joint-stock commercial banks in particular are the most important and developed service types in the financial services market in Vietnam. Some basic services can be generally assessed as follows:

Capital mobilization services: Savings deposit services account for up to 80% of mobilized capital of Vietnamese credit institutions in general, joint stock commercial banks in particular in Hanoi as well as the whole country. In recent years, thanks to the diversification and development of a number of new savings services such as: depositing money in one place and withdrawing in many places, saving money with a purpose, saving in gold., the amount of money mobilized at credit institutions, including joint stock commercial banks, has continuously increased.

Credit services: In recent years, outstanding loans of the commercial banking system in Hanoi have also continuously increased. The credit growth rate of joint stock commercial banks from 2012 to 2014 also increased sharply.

32

Thang Long University Library