Not only does it make commercial banks "multi-functional" banks, but through service activities it will also generate a large portion of income at low cost.

1.3. Content of building Marketing for banks

1.3.1. Factors affecting bank marketing activities

1.3.1.1 Macro environmental factors

Maybe you are interested!

-

Factors affecting consumer behavior towards Mobile Marketing activities in Hanoi inner city area - 1

Factors affecting consumer behavior towards Mobile Marketing activities in Hanoi inner city area - 1 -

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2 -

Solutions to improve marketing activities of Vietnam Bank for Agriculture and Rural Development - Bac Ninh Branch - 11

Solutions to improve marketing activities of Vietnam Bank for Agriculture and Rural Development - Bac Ninh Branch - 11 -

![Experience in Bank Marketing Activities in Some Countries [4] & [24]](https://tailieuthamkhao.com/en/uploads/2024/08/22/experience-in-bank-marketing-activities-in-some-countries-4-24-120x90.jpg) Experience in Bank Marketing Activities in Some Countries [4] & [24]

Experience in Bank Marketing Activities in Some Countries [4] & [24] -

The effectiveness of marketing communication activities for the program "An gia lap nghiep" for individual customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Thua Thien Hue branch - 13

The effectiveness of marketing communication activities for the program "An gia lap nghiep" for individual customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Thua Thien Hue branch - 13

In essence, a bank is still a business enterprise and is also governed and affected by the macro environment of the enterprise (external environment). The external environment always contains opportunities and threats for the enterprise. To study the impacts of the macro environment, people often rely on the PETS model including: political, economic, technology, nature and sociology.

Economic factors

Economic factors have a huge impact on business units, mainly: growth trends of gross domestic product, bank interest rates, stages of the economic cycle, balance of payments, financial and monetary policies, etc. In the economy, market demand depends greatly on the development and stability of these economic factors.

Political factors

Including legal regulations that these factors affect the business results of banks such as: business law, banking law, policies, regulatory tools of the state bank and the government... These factors can create opportunities or risks for banks. The legal system sets out regulations and constraints that businesses must comply with. The government and the state bank are the ones who control, manage and regulate the banking system.

Natural and social factors.

Natural factors including geographical location and region also greatly affect the performance of banks.

Social factors include norms, values, lifestyles, occupations, population, religion, ethical concepts, customs, etc. The impact of socio-cultural factors is often long-term and sometimes difficult to recognize. The scope of impact of socio-cultural factors is often very wide and strongly affects banking operations.

Technological and technical factors

Technology can create opportunities or threats for banks such as creating new products but also making existing products obsolete, creating pressure for banks to quickly innovate technology to compete.

1.3.1.2 Micro-environmental factors

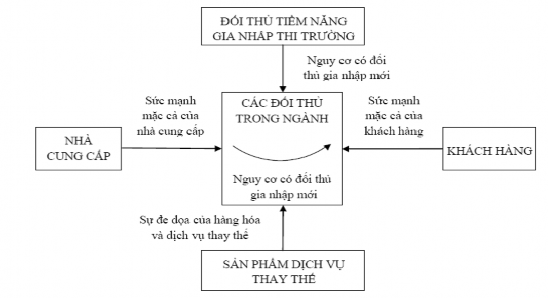

Michael E. Porter (Harvard Business School) has identified five competitive forces that businesses need to analyze to assess the long-term attractiveness of a market or a market segment ( Figure 1.1). Therefore, analyzing the impact of these factors on the business is the basis for selecting the target market and building the business's marketing plan.

Source: Michael E. Porter, 2012, page 37

Figure 1.1: Factors determining competition in the industry Competitors in the industry

Competitors pose a direct threat to the business of banks because modern banks today have to spend more on competition such as advertising, sales, research and development. The main factors in understanding competitors are the future objectives of competitors, the current strategies of competitors, the potential of competitors, the strengths and weaknesses of major competitors, the objectives and strategies of major competitors.

Threat of substitute products

Businesses will be seriously threatened by other businesses that provide products that can replace their products when: (1) new technologies appear that will make existing technologies obsolete; (2) rapid product changes, the continuous appearance of new products based on technological breakthroughs can make many traditional businesses disappear. Therefore, a long-term marketing strategy must take into account substitute products. Turning a business's products into products that are difficult to replace is a strategic idea that helps businesses survive longer and be more successful in the market.

Supplier bargaining power

Suppliers often provide raw materials, equipment, labor, capital, etc. Suppliers can increase the selling price or reduce the quality of the products and services provided. Conditions that increase the pressure of suppliers are: there are only a few suppliers, substitute products are not available, when the supplier's products are different from other suppliers and are highly valued by buyers, or when buyers have to bear high costs due to changing suppliers...

Customer bargaining power

Customers are an indispensable part of the banking system's business operations and customers decide the success or failure of the company as well as the bank through the use of banking products and services or not. Pressure from customers is to reduce prices or improve service quality. Pressure from customers is due to the following conditions: when the number of buyers is small, when buyers are large, products

products that are not different from other products…

Potential competitors

The level of future competition depends on the entry of potential competitors. New competitors will limit the profit potential of the industry. There are several barriers to entry into the market, including:

Economies of scale: This is the reduction in cost per unit of product due to the increase in volume of production. However, nowadays instead of mass production according to product orientation as before, businesses produce on a small scale according to customer orientation.

Product differentiation: Differences in quality, utility, service, advertising… This differentiation creates barriers to entry into the industry.

Capital: To produce some products requires a large amount of capital.

Access to distribution channels: It is very difficult to convince distributors to accept distributing the products of a new business such as: reducing prices, sharing advertising costs and these measures reduce business profits. When the distribution channel is stable, the new company has to spend more on advertising, supporting sellers... Switching costs: are the costs that buyers encounter when switching from products

from one supplier to another supplier's product.

In general, to develop an effective marketing plan, businesses need to analyze the above competitive forces for each product or product group to choose a target market or brand. At the same time, businesses need to analyze the stability of the factors of the competitive environment and only factors with high probability of occurrence are a solid basis for choosing a marketing strategy.

1.3.2. Building a Marketing Strategy

Marketing in the 21st century is no longer limited to the traditional 4P formula but has expanded to 3P to form the 7P formula. According to author Luu Van Nghiem (2008), service marketing includes 7 basic elements, including: product services (Product Services), price (Price), promotion communication (Promotion), distribution network.

(Place), people (People), service processes (Processes) and customer services (Provision for customer services).

1.3.2.1 Product Services Strategy

A bank is an organization that trades in money - a special type of commodity and the products of a bank are the monetary services that the bank provides to customers to meet their needs. Therefore, the products of a bank have all the characteristics of a service product that existing goods do not have. Service products have four outstanding characteristics (Luu Van Nghiem, 2008):

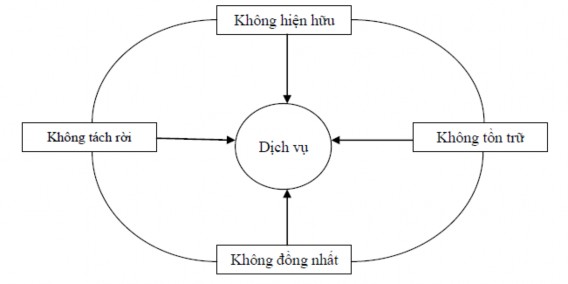

Source: Luu Van Nghiem, 2008, page 12

Figure 1.2: Four basic characteristics of service

Intangible services : This is the basic characteristic of banking services. Because banking products and services are intangible and do not exist in physical form, it causes many difficulties for banks in managing service provision activities, making it difficult to market services and identify services. Banking products and services are implemented according to a sales process that can only be sold and determine the quality of products and services during and after use, so trust is an extremely important factor. On that basis, the important task of banking marketing is to build and strengthen customers' trust in the bank.

Heterogeneous services : Banking products and services cannot be measured and standardized, so banking services are often heterogeneous. The components of banking products and services are: staff, technology, customers, etc. During the supply process, banking services are subject to many factors that are difficult to control because in customer service activities, bank employees cannot create the same services at different times or working spaces such as: implementation methods, completion time, service attitude, etc.

Inseparable services : Based on the service characteristics of banking products, the process of providing and consuming products takes place simultaneously and customers directly participate in the product supply process, requiring marketing to coordinate closely with product and service supply departments as well as determining customers' needs and ways of choosing to use banking products and services.

Non-storage products and services : Banking products and services cannot be stocked, stored, or moved from one area to another, so the provision of banking products and services and the consumption of customers are limited in time. Therefore, the more scientific the service provision process, the simpler the procedures, and the faster the operations of professional staff are, these are the top criteria that influence customers' choices.

1.3.2.2 Pricing strategy

Pricing strategy plays a very important role in banking business. It is one of the basic factors that determine the choice of buyers. Price is the only element in Marketing that generates revenue, it directly affects revenue and profit. In addition, banking enterprises can use “price” as a tool to pursue different goals and this tool can often be used very flexibly.

Price policy is closely related to product policy, it precisely coordinates the conditions between input capital costs and the market. The enterprise's price strategy must be built on the basis of estimating the total demand for goods and services.

services of the market. However, because banks trade in a special commodity called “money”, the price of mobilized capital products will be the basis for banks to set prices for output capital products (loans). Lending interest rates are often priced by the method of mobilization interest rate + a%. In which a%: is called the bank's desired profit margin depending on the lending object and loan product.

1.3.2.3 Distribution network strategy (Place)

Distribution is the act of directly influencing the delivery of services to customers or the delivery of services to consumers in different market areas. Accordingly, members of the distribution channel include service providers, intermediaries and consumers. Thus, the bank's distribution channel is a system of branches and transaction offices of the bank with the same goal of maximizing customer needs, promoting the brand and improving operational efficiency.

Distribution channels require the way the bank distributes its products to create convenience for customers. Typical examples of convenience in distribution include the network of bank branches and the network of ATMs of banks. Banks with many machines, located in many places, and machines that have less problems when withdrawing money will attract more customers.

Because banking products are service products, the way these products are distributed will always involve both customers and the service creation process. Therefore, banks must have specialized departments in charge of specialized products. A product supply network that is suitable for customers, locations and service supply times of the bank is really necessary. In the past, most banks focused all their resources on developing a network of transaction offices and branches nationwide with thousands of employees because this was considered the only sales channel for the bank. However, today, thanks to the remarkable development of electronics and information technology, the bank's distribution network has been and is changing significantly. Instead, people pay attention to business points, electronic sales instructions, home banking services and telemarketing. Rapid technological changes also

affecting the product distribution network, currently banks also sell their products and services via the internet such as: online payment services, online loans, online savings, ...

1.3.2.4 Communication and promotion strategy

Service communication plays a very important role in the marketing mix because it provides information to customers and solutions to internal and market relationships. Service communication includes activities such as:

Advertisement

Advertising in the banking sector with the main function of identifying information about services, positioning services, helping customers better perceive the quality and quantity of services, forming expectations and persuading customers to use banking services. Currently, commercial banks have carried out advertising in many forms such as: newspapers, magazines, television, radio, banners, posters, internet, sponsorship activities, product introductions, etc. Because each form targets different customer groups, commercial banks often apply many suitable advertising methods at the same time to attract customers.

Personal communication

This is considered as service sales, the process of transferring services between bank employees and customers. In service provision, in addition to meeting customers' product consumption needs, bank employees need to perform well a number of other functions such as: exchanging, providing additional information, answering questions... to satisfy customers' desires.

Encourage consumption

Including the use of tools and solutions to stimulate short-term market demand, specifically: giving away lucky draw codes when making transactions, free use of new products and services (internet banking, home banking), giving gifts to customers opening accounts for the first time...

1.3.2.5 Human resources strategy (People)