The integration process creates many challenges because in addition to having to compete with domestic banks, banks now also have to compete with foreign banks that have high levels of management, a lot of experience in business, sophisticated technology... therefore, with weak financial capacity, outdated technology, limited management and operation capacity of commercial banks... we will face many difficulties in competition.

The process of reforming state-owned enterprises as well as the banking and financial system is slow, many economic sectors face many difficulties in the integration process, the state budget allocated by ministries and branches is not timely with investment progress, leading to a situation of outstanding debt and mutual capital appropriation by enterprises.

Some young staff lack experience so sometimes they cannot meet the requirements of the job.

Despite many difficulties, the Department's activities still achieved very good results.

Good:

In 2003 , SGD made significant contributions, contributing to creating events.

important in the performance of the Bank for Investment and Development of Vietnam:

Complete the business plan with total assets reaching 95,000 billion, revenue serving investment and development reaching 28,000 billion VND.

Completed the investment phase of the restructuring project - charter capital reached 3,650 billion VND.

100% of BIDV member units are granted ISO 9001.2000 certificates.

BIDV brand won the "Golden Star of Vietnam" award.

Is an official member of the international organization Visa international.

Successfully implemented phase 1 of the Bank modernization project.

In 2004, we can see the business performance through the following aspects:

2.1.3.1. Capital mobilization

SGD's capital mobilization activities in the past time have achieved good results. SGD has mobilized customers to renew a relatively large amount of deposits such as: development support fund,

Social insurance (SI)... mobilized new capital from many customers such as Nam Thang Long Urban Area Investment and Development Company 150 billion... New customers in the non-state-owned enterprise sector (NPE) received a lot of attention and interest, such as Ham Rong Joint Stock Company, Ho Guom Garment Joint Stock Company. This activity contributed significantly to the growth of SGD's capital.

In 2004, short-term mobilization was 3,849 billion VND, medium and long-term was

5,275 billion VND, accounting for 42.2% and 57.8% of the total source respectively. Compared to 2003, the term of capital sources has tended to change positively: medium and long-term capital sources have increased in absolute numbers. Besides, compared to 2003, although there was an increase in medium and long-term capital (from 5,086 billion in 2003 to 5,275 billion in 2004), short-term sources have decreased (from 4,124 billion in 2003 to 3,849 billion in 2004). Thus, the capital source has a relatively stable structure.

During the capital mobilization process, the Department always closely monitors the market interest rate developments to ensure competitiveness to maintain and increase capital sources in accordance with the direction of the Head Office and the commitment to the banking association. The issuance of valuable papers is always well prepared and carried out by the Department. The first issuance of valuable papers in 2004 helped the Department complete the mobilization target before the assigned deadline.

The capital mobilization work of the Department in the past period has generally continued to maintain a high mobilization balance and growth structure, thanks to which the assigned plan has been well completed by the Department. The increase in medium and long-term capital has met the capital needs in investment and lending activities.

2.1.3.2. Credit work

Credit growth scale: SGD has ensured credit balance within the assigned limit, specifically as of December 31, 2004, the total outstanding balance reached 5,057 billion thanks to seriously implementing the direction on credit growth.

Credit structure: under the direction of the Bank for Investment and Development of Vietnam and the management board of SGD, in 2004, although there were not many advantages in interest rate competition compared to other banks,

However, SGD still strives to promote short-term loans, reduce outstanding medium and long-term loans, and construction loans, so the short-term credit structure at SGD has been significantly improved.

2.1.3.3. Some other work

SGD continues to promote its strengths in payment, guarantee... Some encouraging results in these activities are: net service revenue reached 25.63%, the proportion of net service revenue to total revenue was 20%...

The number of customers opening accounts at SGD has increased significantly, the Department has added 300 new customers who are economic organizations and 3,550 individual customers. It can be said that such results are due to the fact that the staff and departments at SGD have coordinated well with each other in marketing to new and potential customers.

To create a more favorable environment for staff, SGD has constantly improved and upgraded technical equipment, technological infrastructure...

Always launch competitions such as: women's movement to be good at housework and banking; movement to research and apply innovative initiatives to improve work efficiency; movement to repay gratitude... on important occasions such as International Women's Day, industry establishment day... thereby creating a good "land" for innovative and creative initiatives to flourish, arousing and promoting the inner strength of each individual and collective.

2.2. CURRENT SITUATION OF MEDIUM AND LONG-TERM CREDIT FOR STATE-OWNED ENTERPRISES INVietnam Investment and Development Bank

2.2.1. General regulations on medium and long-term credit activities 2.2.1.1. Borrowing principles

Use loan capital for the purpose agreed upon in the credit contract: in banking operations there are always legal regulations to ensure safety.

not only for the bank but also for the economy. The activities of banks will have their own purposes and scope, which are often stated in credit contracts to ensure that the bank does not finance illegal activities and that it is not contrary to the bank's platform.

Repay the principal and interest of the loan on time as agreed in the credit contract.

2.2.1.2. Loan conditions

Legal purpose of using loan capital: this purpose is not contrary to the provisions of law and not contrary to the commitments in the credit contract with the bank.

Have financial capacity to ensure debt repayment within the committed period, effective business operations (profitable), in case of loss, must have a feasible plan to overcome the loss to ensure debt repayment within the committed period.

Have a feasible and effective investment, production, business or service project or plan; or have an investment project or plan to serve life with a feasible debt repayment plan.

2.2.1.3. Loan interest rate

The specific loan interest rate is agreed upon by the Bank and the customer: a fixed loan interest rate may be applied throughout the loan period or an adjustable loan interest rate may be applied.

The bank applies a maximum overdue interest rate of up to 150% of the agreed on term loan interest rate in the signed or adjusted credit contract.

For interest due that customers cannot pay, even in cases where the interest term has been extended or adjusted, the Bank may apply a penalty for late payment of overdue interest according to the instructions of NHĐT&PTVN.

2.2.1.4. Lending method

Loans according to credit limit:

SGD and the customer determine and agree on a credit limit to be maintained for a certain period of time. The method of lending according to the credit limit is applied to customers with stable and effective production and business and regular credit relations with SGD.

When determining the credit limit, it is necessary to base on: The previous year's final report, the most recent accounting report along with the annual and quarterly business production plan and economic contracts, construction contracts...

During the validity period of the credit limit contract, customers can both withdraw the loan capital and repay the loan debt, but must ensure that the outstanding balance does not exceed the credit limit agreed upon in the credit limit contract.

To ensure stable production and business, annually or according to the needs of expanding or narrowing production, business, and services of customers, or the conditions of customers' loans, SGD and customers agree to sign an additional appendix to the credit contract to adjust the credit limit for the next period, or sign a new credit limit contract or terminate this lending method.

Loans for investment projects:

When a state-owned enterprise has a plan to invest in developing production, business services... it can apply for a bank loan. However, to get a loan, the State Bank of Vietnam requires customers to develop a project, showing the purpose, investment plan as well as the project implementation process. Project analysis and appraisal are the basis for the bank to decide on the loan capital and determine the enterprise's repayment capacity.

Syndicated loans:

The bank and one or several other credit institutions jointly lend to a loan project or loan plan of a customer, in which the SGD or another credit institution acts as the focal point for arrangement.

Syndicated lending is carried out in accordance with the Co-financing Regulations of credit institutions issued by the Governor of the State Bank of Vietnam and the guidance of the General Department.

Director. Project appraisal, loan plan, and decision to participate in bank co-financing shall be carried out in accordance with these regulations.

Other lending methods:

In addition to the above lending methods, SGD lends capital to customers in other lending methods not prohibited by law, in accordance with the lending regulations of the State Bank of Vietnam, this Regulation and the business conditions of the Bank and the characteristics of each type of borrowing customer.

2.2.1.5. Loan security measures

Measures to secure loans with assets:

Pledge, mortgage with the borrower's assets.

Guarantee by third party assets.

Secured by assets formed from loan capital

Measures to secure loans in case of unsecured loans:

Unsecured loans to qualified customers.

Unsecured loans as designated by the Government.

2.2.1.6. Repayment of principal and interest on loans

Based on the characteristics of production and business, capital circulation, financial capacity, income and debt repayment sources of the enterprise, the repayment period of principal and interest on loans is determined and regulated as follows:

Principal repayment terms and repayment amount of each term.

Collect loan interest periodically every month or quarter, season, production cycle, or collect loan interest together with principal according to repayment period.

When the principal or interest payment deadline comes, if the enterprise fails to pay the debt on time, measures will be applied to adjust the principal and interest payment deadline, extend the principal and interest payment, or convert the debt to overdue.

In case the enterprise requests to repay the debt before the due date, the State Bank and the enterprise can agree on the conditions, the loan interest, and the fees payable, but not exceeding the interest (or fees) agreed upon in the credit contract.

Repayment in foreign currency: Enterprises borrowing in foreign currency must repay principal and interest in that foreign currency. In case of repayment in other foreign currencies or Vietnamese Dong, the enterprise and the State Bank shall agree in accordance with the provisions of law on foreign exchange management and the instructions of the General Director.

2.2.2. Current status of medium and long-term credit for state-owned enterprises at the SBV

GENERAL ASSESSMENT :

In the recent business activities of the Department, the Department has always strictly implemented the law on credit institutions, the business processes and authorization mechanisms of the Vietnam Development Bank, and always closely followed the development orientation of the sectors and the whole society.

In recent times, the Bank for Investment and Development of Vietnam in general and the State Bank of Vietnam in particular have proposed many measures to improve the ability to supply medium and long-term capital to the economy, such as mobilizing long-term capital through issuing bonds, promissory notes, etc., and at the same time applying appropriate lending methods (co-financed loans) to mobilize capital from other credit institutions, investors, etc. to invest in major programs and key projects of the country. Thanks to that, many projects and programs have been provided with capital in a timely manner, contributing to promoting the development of industries and sectors: electricity, post and telecommunications, cement, sugar cane, agricultural infrastructure development and offshore fishing, etc.

Recognizing the importance of credit activities, in addition to performing the above activities, SGD also applies many measures to ensure safety during operations, typically:

Evaluate customers in terms of: evaluating customers' assets, evaluating customers' debts... thereby being able to select good customers.

Customer assessment reports are prepared periodically by credit officers. The content of the reports is very important: talking about the financial situation, production and business situation, cash flow analysis... of the customer.

The Department has implemented many types of credit suitable for all businesses and ensured the management of debt collection of the Bank such as project-based loans for construction enterprises, loans to commercial units when the customer's partners have been assessed...

Thanks to these measures, the medium and long-term credit activities for state-owned enterprises of the Department in the past time have achieved many good results, credit quality has achieved good results. The Bank has provided capital in a timely manner for enterprises to operate effectively, supporting enterprises to develop more and more sustainably; the Department has also provided capital in a timely manner for projects and works serving socio-economic development, contributing to the cause of national construction, helping the country become more and more prosperous and beautiful.

SOME SPECIFIC RESULTS:

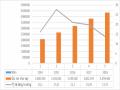

Credit structure over time and by economic sector:

Total outstanding debt increased from VND4,478 billion in 2002 to VND5,186 billion in 2003, an increase of 15.81% compared to 2002. But by 2004, the scale decreased again and was only VND5,057 billion, a decrease of VND129 billion, equivalent to 2.5%.

Unit: billion VND

Credit type

2002 | 2003 | 2004 |

Maybe you are interested!

-

Current Status of Medium and Long Term Credit Risks at Vietnam Bank for Agriculture

Current Status of Medium and Long Term Credit Risks at Vietnam Bank for Agriculture -

Current status of short-term lending activities and some solutions to improve the quality of short-term credit services at Vietnam Joint Stock Commercial Bank for Industry and Trade Vietinbank - Branch 12 - 1

Current status of short-term lending activities and some solutions to improve the quality of short-term credit services at Vietnam Joint Stock Commercial Bank for Industry and Trade Vietinbank - Branch 12 - 1 -

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks -

Assessment of the Current Status of Access to Bank Credit Capital of Small and Medium Enterprises in Thai Nguyen Area in the Period of 2013 - 2018

Assessment of the Current Status of Access to Bank Credit Capital of Small and Medium Enterprises in Thai Nguyen Area in the Period of 2013 - 2018 -

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period