When their business is profitable, they can manage their capital, their cash flow rotates according to the expected cycle, and they will repay their debts on time. On the contrary, when their business is losing money, the capital cycle is longer than the loan term, and repaying the debt becomes difficult. This is one of the problems that banks always try to minimize: credit risk, liquidity risk.

In addition to the inherent characteristics of the credit category, personal credit also includes its own characteristics (which help distinguish it from other business sectors such as production credit for state-owned enterprises, limited liability companies, etc.) in the following aspects:

- Borrowers : are individuals and households. Reality has proven that when people have high income, they will have a progressive tendency to keep up with the times, wanting to improve their quality of life more, even beyond their current income. This leads to an increase in the demand for loans. The same is true for households, when family members have high income, want to do business or need to use better, more advanced services and products, the demand for loans will also increase.

- Loan purpose : This has been partly shown through the definition of personal credit. When borrowers borrow, mainly for consumption purposes, serving daily needs (in the short term) such as: buying household items, paying tuition fees, ... or serving needs that require large amounts of capital (in the medium - long term) such as: small retail business, buying means of transport (motorbikes, cars), buying houses, ...

- Debt repayment source : Because the purpose of the loan is not mainly for production and business, it is easy to see that the amount of loan value often does not bring profit. The subjects often use their salary or income from other sources: tutoring, small business, commission from brokerage, etc. to repay the bank loan. This also indirectly affects their work intensity, giving them more motivation to earn money to pay off the debt.

- Loan size : As mentioned, each borrower here usually borrows a small amount of value. However, the number of borrowers is quite large, so the total loan size is not small.

- The need for loans to serve consumption is greatly affected by the economic situation . Indeed, when the economy develops and income increases, people have the need to shop.

3

more, borrow more. On the contrary, when the economy is in recession, prices do not tend to decrease, all human spending becomes tighter, the need to borrow is also less because the source of money that can be used to pay off debt is decreasing. And instead of borrowing, they switch to another form to pay for daily expenses, which is saving.

- High risk : Personal credit always has potential risks in almost every step of the credit granting process as well as credit-related aspects:

+ The appraisal often does not bring about accurate results due to incomplete information sources. This is inevitable because information about the feasibility, prospects of capital use as well as health status often has no specific basis for verification, is not clear and transparent as with the financial reports of the enterprise. Subjects can easily conceal for the purpose of borrowing capital.

+ The main source of debt repayment is the borrower's personal income. This source of income is unstable and can easily change, increase or decrease due to the impact of health status (healthy, weak), work situation (promotion, demotion, job transfer, etc.), family circumstances (additional dependents, unexpected events, etc.), etc.

+ High loan management costs: It takes a lot of time and effort to collect and investigate information about individuals and households before granting credit, which is inevitable in the appraisal process. Not only that, the number of personal loans is very large. These things show that the costs used to manage these loans are not small.

+ High profit from personal credit: Reality has proven that profit and risk are two factors that always go hand in hand. To gain profit, banks often apply high interest rates, making it difficult for customers to fully repay their debts when due, thereby making it disadvantageous for banks to collect debts (causing liquidity risks). That shows that when profits are large, the risk is also relatively high.

1.3. The role of personal credit

Personal credit is an indispensable part of banking operations, a solid link with customers and an impact on the entire economy. Specifically:

4

1.3.1. For banks

Personal credit is a typical business line of the bank. Therefore, this business line plays a very important role for the bank. Typically, the following 3 main roles:

- Firstly, personal credit is a channel to strengthen the relationship between banks and individual customers . Through this activity, bank employees will communicate with customers, thereby promoting the connection as well as expanding other business activities to them: capital mobilization, payment services, etc. Through communication, banks can also increase their own marketing to improve their competitiveness with other banks.

- Second, personal credit is a traditional business in the banking business, bringing a significant profit and accounting for a high proportion of the total profit that the bank earns . Indeed, the value of personal loans is usually relatively small, but the number of loans is very large, so the bank can easily disperse the risk. Besides, when considering the total value of the loans that the bank has lent to individuals, it will be a not small number. Furthermore, personal credit involves a very large risk (this is one of the characteristics of this activity), so the interest rate that the bank applies when lending to customers is often large, thanks to which, the profit from lending (under the condition that customers repay the loan on time) is also very high.

- Third, personal credit is the savior for the initial business of small, weak banks in the market . When they first start operating, these banks need to rely on personal credit to attract customers, gain market share, and gradually increase their competitiveness with other banks. Through this, it will also increase resources, creating opportunities to connect with corporate customers.

1.3.2. For customers

For customers, personal credit has the following roles:

- Firstly, personal credit helps satisfy the necessary or urgent needs of customers . Indeed, bank loans are one of the channels through which individual customers can use a sum of money quickly and safely within a certain period of time before having time to accumulate a corresponding amount. Currently, as society develops, human needs are increasingly rich and diverse, leading to increased spending levels, even exceeding the allowed level.

5

For that reason, banks providing loan services to individual customers has contributed to improving their quality of life.

- Second, personal credit is increasingly improved, bringing many incentives to customers . Specifically, interest rates at banks are often lower than interest rates applied in the free market (black market). Current procedures have also been shortened, bringing the most comfort and convenience to customers. In addition, loan terms as well as repayment methods can be negotiated depending on each customer's circumstances, helping them feel more secure when using this service.

1.3.3. For the economy

Currently, personal credit holds a very important position and has a significant impact on different entities in the economy. Specifically:

- Firstly, personal credit contributes to the circulation of capital from places with surplus to places with shortage . This helps increase the amount of money in the market, stimulates demand, increases the level of circulation of goods, thereby partly promoting economic growth, increasing revenue for businesses, reducing unemployment rates for society, etc.

- Second, personal credit is one of the core retail services of banks . When these services develop, it will speed up the process of money circulation, take advantage of the great potential of the population to develop the economy, improve the quality of life of people, limit the use of cash, ...

1.4. Personal credit classification

Currently, to increase competitiveness compared to other banks as well as attract customers and gain market share, banks have always researched and developed new types of credit based on 4 main criteria:

1.4.1. Based on credit term

Term is one of the important factors when lending that banks care about. It will be the basis for deciding the loan amount, interest rate as well as other conditions related to lending. And based on the credit term, personal credit is divided into 3 types:

- Short-term credit: is credit with a term of less than or equal to 1 year. This is the main form of credit, directly serving the necessary consumption needs of individuals and households. The risk of short-term lending is the lowest.

6

- Medium-term credit: is credit with a term of over 1 year to 5 years. For individuals, this type of credit is often used to serve needs such as buying a car, repairing or building a house, etc.

- Long-term credit: is credit with a term of 5 years or more. With this type, individuals often use it when borrowing large amounts of money from banks, serving needs related to real estate (buying land, buying houses, apartments, etc.), securities, etc. Long-term credit always contains more risks than other types of credit.

1.4.2. Based on credit guarantee

Credit always involves risk, so credit assurance is necessary. Whether or not there is a guarantee will also be one of the factors affecting the bank's lending decision in terms of: lending or not, loan amount, loan term, etc. And based on credit assurance, personal credit is divided into 2 types:

- Secured credit: is a form of credit with collateral, mortgage or third party guarantee. This type of credit is applied to customers with no reputation or low reliability. Having a guarantee will create a legal basis for the bank to feel secure about the reserve income when the main income is lacking, minimizing risks. And for individuals, credits granted in the medium to long term and with large value are often guaranteed.

- Unsecured credit: is a form of credit without collateral, mortgage or third party guarantee. This type of credit is mostly applied to familiar customers, reputable or with stable jobs, income, and savings. Loans of this type are often low in value and granted for a short period of time.

1.4.3. Based on the method of loan repayment

The method of debt repayment is also one of the issues that banks often care about. It can affect debt collection turnover, risk level, etc. and is decided based on each subject and each customer's situation. Based on the method of debt repayment, personal credit is divided into 2 types:

- Installment credit : is a form of loan in which the borrower repays the bank in many times with certain terms as stipulated by the bank (month, quarter, ...). Type

7

This usually applies to large loans or customers with regular income.

- One-time repayment credit : is a form in which the borrower repays the debt at once when the credit contract matures. This type is often applied to loans with small value and short loan terms.

1.4.4. Based on credit purpose

Credit purpose or purpose of use is one of the important criteria to help classify credit, from which appropriate conditions can be given when deciding to lend such as loan ratio, term, collateral conditions, etc. And based on the purpose of use, credit can be divided into 4 types:

- Real estate loans: are credit products to serve the needs of customers to buy houses, buy land, repair and build houses, etc. in their current difficult and lacking financial conditions.

- Consumer loans: are credit products that serve the needs of regular spending and shopping, contributing to improving the quality of life of customers (usually those with stable jobs and incomes). The number of customers using this product is often quite large.

- Production and business loans (Small industry): is a credit product to compensate for the shortages in the small business process of individuals or households. For this product, the number of customers in need is quite large, but the revenue from lending is not much due to the limitations of the customer's qualifications and time as well as the small scale of business activities (loan size).

- Agricultural loans: this is also a credit product related to production and business, but it is more specific because mentioning agriculture means mentioning cultivation and livestock - things that depend largely on the weather and contain many unusual risks. This type of credit not only provides capital to meet the production needs of farmers but also contributes to changing farming methods from manual to applying machinery in production and harvesting, from small scale to larger scale, even towards a wide export market. From there, it promises to fundamentally change the quality and value of farmers' lives.

8

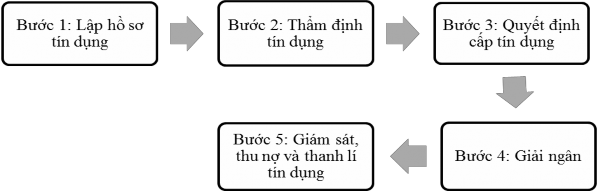

1.5. Personal credit process

The credit process is formed on the basis of a synthesis of the bank's principles and regulations in granting credit, including many stages arranged in a logical sequence, closely related to each other. Normally, the personal credit process consists of 5 stages:

Diagram 1.1. Personal credit process

(Source: Commercial Banking Course, 2011)

Specifically the steps are as follows:

1.5.1. Establishing a credit profile

This is the initial stage of the relationship between the customer and the bank, helping to provide customer information through documents and papers proving the need for credit capital, the legality of the customer's identity as well as the customer's willingness to apply for credit. From there, it creates the basis for all future credit transactions. And for customers, banks often require the following types of documents:

- Loan application form : according to each bank's form

- Legal documents : including ID card, household registration book/temporary residence book,...

- Loan description : describe the purpose of the loan.

- Income proof documents : employment contract, salary confirmation,...

- Collateral documents : house papers, land papers, etc.

1.5.2. Credit appraisal

This is the most important stage in the credit process. In this step, the bank will check the accuracy of the information provided by the customer in step 1, thereby creating

9

The basis for banks to analyze the purpose of using credit capital as well as the customer's ability to repay the loan. This assessment must be based on both qualitative and quantitative aspects.

- Qualitatively, banks often use the 5C analysis method.

(According to the Commercial Banking Course, 2009) as follows:

+ Character (Customer's character): Here, character is expressed through the clear purpose of the loan as well as honesty, responsibility, and goodwill in repaying the debt. Determining the purpose of using the capital is very important, helping the bank to make a preliminary assessment of the customer's ability to repay the debt in the future through the potential and profitability of that purpose. In addition, the purpose of using the loan also creates the basis for the bank to decide whether to lend or not when comparing with the current credit policy. In addition, honesty and responsibility will be the basis for creating trust in the bank regarding the issue of loan repayment.

+ Capacity (Customer capacity): Customers need to ensure civil legal capacity (having civil rights and obligations according to the law) and civil conduct capacity (the ability of an individual to exercise civil rights and obligations).

+ Capital (Customer's own capital): This is one of the criteria that banks are most interested in because it affects loan repayment. The bank will assess what the customer will do and how to generate money to repay the debt (in addition to salary, the bank will base on the customer's other income such as retail trading, brokerage commissions, etc.).

+ Collateral (Assets securing the loan): This is also a basis for the bank to decide whether to lend to customers or not. It is usually a guarantee or a valuable asset (usually larger than the loan amount), which is a second source of income when the customer cannot pay the loan. It must ensure legality, liquidity, value retention, etc. to limit risks for the bank.

+ Conditions (Debt repayment conditions): The bank needs to seek information as well as make preliminary assessments about the development trends, potential of the job or industry that the customer is pursuing as well as how economic conditions will affect the credit.

- Quantitatively, banks can use the credit score method. This is a way to consider credit requests for customers through scores by

10

automatically scores customer-related factors. From there, this analysis becomes more specific and simplified. This model usually uses 7 to 12 categories and each category is scored from 1 to 10. Specifically, commercial banks in Vietnam often absorb, learn and propose credit scorecards based on the categories and corresponding scores applied in the US, built by Anthony Sauder, an economist, as follows:

Table 1.1. Credit categories and corresponding scores

Factors

Score | |

1. Borrower's occupation | |

Specialist | 10 |

Skilled labor | 8 |

Office staff | 7 |

Student | 5 |

Unskilled labor | 4 |

Part-time worker | 2 |

2. Residence status | |

Have own house | 6 |

Rent a house or apartment | 4 |

Stay with relatives or friends | 2 |

3. Credit rating | |

Good | 10 |

Medium | 5 |

No profile | 2 |

Bad | 0 |

4. Working time for current occupation | |

More than 1 year | 5 |

1 year or less than 1 year | 2 |

5. Length of stay at current address | |

More than 1 year | 2 |

1 year or less than 1 year | 1 |

6. Telephone available at accommodation | |

Have | 2 |

Are not | 0 |

Maybe you are interested!

-

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank -

Some Online Content Marketing Solutions To Improve Business Efficiency Of Ani International Training Academy

Some Online Content Marketing Solutions To Improve Business Efficiency Of Ani International Training Academy -

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank -

Some solutions to improve the efficiency of attracting and using ODA capital in the forestry sector in Vietnam - 13

Some solutions to improve the efficiency of attracting and using ODA capital in the forestry sector in Vietnam - 13 -

Solutions to promote the process of restructuring and innovating state-owned enterprises to improve the efficiency of state-owned enterprises in Quang Binh province today - 10

Solutions to promote the process of restructuring and innovating state-owned enterprises to improve the efficiency of state-owned enterprises in Quang Binh province today - 10

11

7. Number of people living off the borrower | |

No/One | 4 |

Two/Three | 3 |

More than three | 2 |

8. Type of account available at the bank | |

Have both checking and savings accounts | 4 |

Only savings account | 3 |

Checking account only | 2 |

No account yet | 0 |

According to the above category table, the customer will have the highest score of 43 and the lowest of

9. In addition to this table, the bank must also rely on statistics from previous transactions to determine the score that is the boundary between the decision to lend or not, and from there decide how much to lend depending on each specific score scale.

Although this method is superior to the qualitative method, it is not without risks and errors when socio-economic conditions have major changes and strong impacts on the categories. At that time, when the scoring table is not flexible, it will lead to many bad consequences: wrongly identifying the loan object and amount, missing out on potential customers, etc.

1.5.3. Credit granting decision

After the appraisal, an equally important stage is the decision to grant credit because this is the final step in the process of researching, assessing information and providing answers to customers' loan requests. Banks will have to bear all risks and consequences from lending, so they are very cautious. In addition to using the results from the appraisal process, banks also base on other sources of information such as updated information about customers, related legal policies, etc.

From the above sources of information, the bank will make its decision. If rejected, the bank will send a written notice stating the reasons. If agreed, the bank and the customer will sign a credit contract with detailed and clear contents: loan purpose, loan amount, loan term, loan interest rate, etc.

1.5.4. Disbursement

After signing a credit contract with a customer, depending on the terms stated in the contract, the bank will disburse the loan. The disbursement can take place once.

12

(if the loan value is small) or many times (if the loan value is large) in many ways: disbursement by bank transfer or cash, direct payment to the goods supplier to the customer,...

1.5.5. Credit monitoring, collection and liquidation

The objective of this step is to monitor and evaluate the customer's compliance with the contract and take appropriate action when necessary. Credit officers need to monitor:

- The financial stability of the borrower

- Use of loan for the right purpose

- Collateral value

- Debt repayment progress

- New customer needs

Before the due date, the bank has the right to collect the debt or stop disbursing if the customer violates the contract. When the due date comes, if the customer pays the full principal and interest, the credit relationship between the bank and the customer is considered to be over. If the customer does not pay the full principal and interest, the bank will investigate the cause and make decisions: extend the contract, change the debt repayment method, sell collateral to compensate for risks, etc.

Thus, a credit process plays a very important role in the operation of a bank. It is built based on the conditions of legal regulations and the conditions of each bank. The process needs to be built flexibly to adapt promptly to sudden changes as well as ensure efficiency, simplicity, and no hassles for customers. With a good process, the bank's business will develop more, minimizing unnecessary risks.

1.6. Personal credit efficiency of commercial banks

1.6.1. Concept

Personal credit of commercial banks is considered effective when it ensures the following criteria:

- Firstly, ensuring the interests of the bank (lender) through maintaining the difference between the deposit interest rate and the lending interest rate as well as ensuring liquidity . Indeed, credit is a lending bank activity to earn profits from the difference between the deposit interest rate and the lending interest rate. And when that interest rate difference is maintained, the interests of the bank are guaranteed.

13

Besides, liquidity is also a factor that helps ensure the bank's interests because when the capital turnover rate is too slow, the bank may lose its ability to pay, causing loss of reputation.

- Second, ensuring the interests of customers (borrowers) through the speed and convenience of loan procedures as well as the diversity of support and incentive policies. On this point, it can be seen that in the past, with cumbersome regulations and procedures, customers were often hesitant in dealing with banks. When this problem is resolved, the frequency of customers coming to banks will increase. Along with that, support and incentive policies are also a factor that helps retain customers because then they feel their interests are guaranteed: the poor can borrow at low interest rates, customers who pay late within a certain period of time (this period will be specifically regulated according to each stage of development of the bank) may not have to pay penalty interest, customers can pay in installments according to the term depending on the agreement, ...

- Third, ensuring the benefits of the economy and society through ensuring economic growth as well as ensuring the stability of social life . When customers are able to borrow capital, they can invest in projects, businesses, etc. (to earn profits) or buy household items, repair or build new houses, etc. (to improve the quality of life). And when banks can lend, it means that business activities are favorable, so the amount of taxes they pay to the state is also guaranteed and the amount of money they can finance or invest in society is also maintained. Only when these things are done, can personal credit truly ensure the benefits of the economy and society.

On the contrary, when personal credit is effective, the interests of banks, customers and the economy and society are also guaranteed. Because when this activity is effective, it means that the bank's business is profitable, customers have easier access to loans and the amount of money invested in the economy and society also increases. Therefore, improving the effectiveness of personal credit is very necessary.

1.6.2. Indicators for evaluating the effectiveness of personal credit

1.6.2.1. Loan turnover

Loan turnover is the amount of credit that a bank has lent out over a given period of time, usually a month, quarter or year. High loan turnover

14