2.3.4 Guarantee product group

Segment customers to apply minimum deposit conditions, credit

Specific maximum handicap:

Manure

group

Customer target | |

Group 1 | - The customer has a guarantee relationship with VPBank and has liquidated at least 3 guarantees, without having incurred any obligation to pay on behalf of VPBank/compulsory loan. Net revenue in the most recent fiscal year is from 20 billion VND or more. - New customers or those with a guarantee relationship but with at least 3 guarantees already in place liquidation, no obligation to pay on behalf/compulsory loan of VPBank has arisen, with net revenue in the most recent fiscal year from 100 billion VND or more. |

Group 2 | - The customer has a guarantee relationship with VPBank and has liquidated at least 3 guarantees, without having incurred any obligation to pay on behalf of VPBank/compulsory lending. Net revenue in the most recent fiscal year is less than 20 billion VND. - New customers or customers with a guarantee relationship but with at least 3 liquidated guarantees, no obligation to pay on behalf/compulsory loan of VPBank, with revenue net income of the most recent fiscal year from VND 20 billion to less than VND 100 billion. |

Group 3 | Other customers |

Maybe you are interested!

-

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Business Results of Quang Binh Tourism Industry in the Period 2014 - 2019

Business Results of Quang Binh Tourism Industry in the Period 2014 - 2019 -

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company -

Company's Business Performance Results for 3 Years (2018-2020)

Company's Business Performance Results for 3 Years (2018-2020) -

Accounting for revenue, expenses and business results at Long Bien Industrial Gas Joint Stock Company - 2

Accounting for revenue, expenses and business results at Long Bien Industrial Gas Joint Stock Company - 2

Minimum margin ratio, maximum margin ratio:

TT

Type of guarantee | Minimum margin ratio/guaranteed value lead | Maximum margin ratio/guaranteed value lead | |||||

Group 1 | Group 2 | Group 3 | Group 1 | Group 2 | Group 3 | ||

1 | Bid security | 0% | 0% | 0% | 100% | 100% | 100% |

2 | Performance Guarantee contract | 5% | 10% | 15% | 95% | 90% | 85% |

3 | Warranty Guarantee | 5% | 10% | 15% | 95% | 90% | 85% |

4 | Advance guarantee | 10% | 15% | 20% | 70% | 60% | 0% |

5 | Payment Guarantee | 15% | 20% | 25% | 0% | 0% | 0% |

6 | Other guarantees | 15% | 20% | 25% | 0% | 0% | 0% |

Applicable principles:

- If the customer requests to use the TSBĐ to replace all/part of the signed part

Cash funds will apply:

Asset Type

Replacement value ratio | Fee (%/year) | |

Debt certificate issued by VPBank onion | 100% | 3% |

Debt certificates issued by other credit institutions are accepted by VPBank. | 120% | 4% |

Real estate; Cars with 7 seats or more down to 70% or more of its value | 150% | 5% |

- For advance payment guarantee: when the advance payment is transferred to the customer's account at VPBank, immediately freeze the above amount. When the customer needs to use the advance payment, he/she must present documents proving the purpose of using the advance payment to perform the contract for which the advance payment was made, and a request for release. At the same time, he/she is responsible for regularly monitoring and checking the progress of the output contract, and fully supplementing the supporting documents.

- For contract performance guarantee: Only apply partial credit if the payment account of the guarantor in the contract is an account opened at VPBank.

- For warranty guarantees: Credit is not applicable for warranty guarantees with a term of more than 12 months.

2.3.5 Other product and service groups

2.3.5.1 VPB VnTopup - VPBilling VPB VnTopup

Allows customers to top up prepaid mobile phone accounts of 7 networks: VinaPhone, MobiFone, Viettel, S-Fone, EVNTelecom, Vietnamobile, Beeline; top up to pay for postpaid subscribers of 2 networks: Viettel and MobiFone; buy prepaid card codes through the account system at VPBank on VPBank's electronic transaction channels including Internet Banking (i2b) and SMSBanking, ATM

VPBilling

Allows customers to pay postpaid mobile phone bills of: Viettel, S-Fone, Homephone Viettel, Viettel Internet bills through the account system at VPBank on VPBank's electronic transaction channels including Internet Banking (i2b) and SMSBanking, ATM

2.3.5.2 Internet Banking and Mobile Banking

Building and developing new products and services operating on the Internet

Internet Banking

VPBank's Internet Banking service, abbreviated as i2b, is a high-tech application service package of VPBank, allowing customers to make transactions, look up accounts, transfer payments and other products via the Internet. i2b service operates continuously 24 hours a day and 7 days a week, via the Internet via the Website https://i2b.vpb.com.vn/ebankwill provide customers with the following amenities:

- Look up information of customer accounts at VPBank.

- Print account statements for the last 3 months.

- Transfer between VND payment accounts of the same customer.

- Transfer between VND payment accounts of customers opened at

VPBank

- Interbank electronic money transfer.

- Look up outstanding debt information, transfer principal and interest payments.

- Online payment when shopping online.

- Pay postpaid bills: electricity, water, phone, telecommunications....

- Book tickets, book tours online.

- Buy prepaid cards of all kinds of Internet and phone cards.

- Electronic top-up: Top up your mobile account

Mobile Banking

SMS Banking is a utility package and service that applies modern technology of VPBank, allowing transactions, account information lookup and registration to receive the latest information from the bank via your mobile phone. The system operates continuously 24 hours a day, 7 days a week, this product and service through the switchboard 8149 will provide the following utilities:

- Check account balance.

- Detailed statement of the 5 most recent transactions.

- Receive notifications of account balance changes.

- ATM transfer within VPBBank system.

- Look up foreign exchange rates.

- Look up bank interest rates.

- Look up help information.

- SMS Banking service applies to all Vinaphone subscribers,

Mobifone, Viettel, S-phone, EVNTelecom, Beeline, Vietnam Mobile.

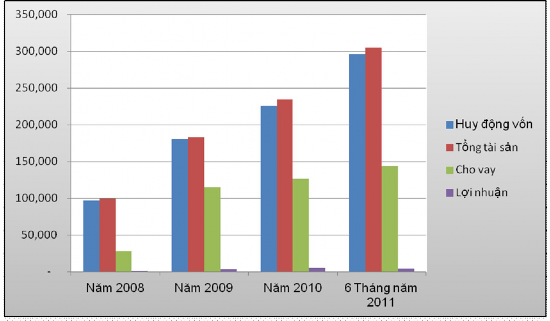

2.3.6 Business results for the years 2008 – 2011

2.3.6.1 Balance sheet for the years 2008 – 2011

Unit: Million VND

Item

Year 2008 | Year 2009 | Year 2010 | 6 months 2011 | |

ASSETS | ||||

Cash, foreign currency at the fund | 5,593 | 1,380 | 3,007 | 5,099 |

Cash in VND | 4,231 | 1,099 | 2,626 | 4,477 |

Deposits at the State Bank | 1,362 | 281 | 381 | 622 |

Customer Loans | 28,159 | 115,351 | 126,740 | 143,326 |

- Classify by customer group | 28,159 | 115,351 | 126,740 | 143,326 |

Personal Loans | 12,747 | 65,039 | 73,243 | 58,750 |

Business Loans | 15,412 | 50,312 | 53,497 | 84,576 |

Other loans | - | - | - | - |

Debt 3-5 | - | 990 | 1,799 | 1,937 |

- Classified by currency | 28,159 | 115,351 | 126,740 | 143,326 |

VND | 28,159 | 115,351 | 126,740 | 143,326 |

NTQD | ||||

RRTD reserve | (36) | (639) | (1,221) | (1,332) |

TSCD | 1,558 | 1,402 | 1,021 | 911 |

Accounts Receivable | 1,998 | 2,425 | 2,408 | 2,445 |

Send HO | 61,713 | 63,344 | 102,255 | 154,818 |

Other assets | 47 | 50 | 50 | 19 |

Total assets | 99,032 | 183,313 | 234,260 | 305,286 |

LIABILITIES | ||||

Total Customer Mobilization | 96,744 | 180,766 | 225,321 | 296,152 |

By customer | 96,744 | 180,766 | 225,321 | 296,152 |

Personal Mobilization | 90,472 | 151,346 | 198,971 | 243,825 |

Mobilizing economic organizations | 6,272 | 29,420 | 26,350 | 52,327 |

By currency | 96,744 | 180,766 | 225,321 | 296,152 |

VND | 92,752 | 171,100 | 206,687 | 275,854 |

NTQD | 3,992 | 9,666 | 18,634 | 20,298 |

Classification by term | 96,744 | 180,766 | 206,687 | 296,152 |

KKH Deposit | 608 | 6,247 | 11,105 | 27,310 |

Short term deposits | 96,013 | 164,914 | 175,902 | 239,496 |

Medium and long term deposits | 123 | 9,605 | 19,680 | 29,346 |

Other debt | 2,460 | 2,320 | 5,633 | 5,573 |

HO Loan | ||||

TN-CP | (172) | 227 | 3,306 | 3,561 |

Total liabilities | 99,032 | 183,313 | 234,260 | 305,286 |

Off balance sheet | 282 | 2,063 | 1,239 | 199 |

Insurance services | 282 | 2,063 | 1,239 | 199 |

Commitments in L/C business | - |

Figure 2.4: Balance sheet

In 2009, total assets were 183 billion VND, an increase of 85% compared to 2008. In 2010, total assets were 234 billion VND, an increase of 28% compared to 2009, of which total profitable assets were 229 billion VND, accounting for 98%, the debt asset structure has changed in a positive direction. In the difficult economic conditions of the world and the country, the branch has boldly promoted capital mobilization activities with a growth rate of 2.37 times, bringing the capital mobilization structure on outstanding credit to 1.86 times, contributing to increasing the difference between revenue and expenditure, improving the quality and efficiency of the branch's business activities. In the first 6 months of 2011, total assets reached 305, an increase of 30% compared to the whole year of 2010.

2.3.6.2 Mobilizing capital from customers

Some ratios

Year 2008 | Year 2009 | Year 2010 | 6 months 2011 | |

Customer Mobilization Growth | 86.85% | 24.65% | 31.44% | |

Sort by customer | ||||

Personal Mobilization | 89.12% | 16.29% | 22.54% | |

Mobilizing economic organizations | 54.11% | 172.61% | 98.58% | |

VND proportion, in which proportion: | 94.65% | 91.73% | 93.15% | |

KKH Deposit | 3.42% | 4.93% | 9.22% | |

1 month | 42.52% | 41.46% | 37.19% | |

2 months | 3.27% | 6.88% | 23.88% | |

3-12 months | 32.15% | 29.74% | 12.95% | |

> 12 months | 13.28% | 8.73% | 9.91% | |

Foreign Currency Proportion | 5.35% | 8.27% | 6.85% | |

Item | Year 2008 | Year 2009 | Year 2010 | 6 months 2011 |

Customer Mobilization | 96,744 | 180,766 | 225,321 | 296,152 |

Sort by customer | 96,744 | 180,766 | 225,321 | 296,152 |

Personal Mobilization | 90,472 | 171,100 | 198,971 | 243,825 |

Mobilizing economic organizations | 6,272 | 9,666 | 26,350 | 52,327 |

VND | 92,752 | 171,100 | 206,687 | 275,854 |

KKH Deposit | 608 | 6,188 | 11,105 | 27,310 |

1 month | 61,409 | 76,869 | 93,410 | 110,135 |

2 months | 23,789 | 5,908 | 15,492 | 70,707 |

3-12 months | 6,823 | 58,122 | 67,000 | 38,356 |

> 12 months | 123 | 24,013 | 19,680 | 29,346 |

Foreign currency | 3,992 | 9,666 | 18,634 | 20,298 |

Figure 2.5: Capital resources table

Total mobilized capital at the end of 2010 was 225 billion VND, an increase of 133% compared to 2008. In the first 6 months of 2011, economic organization deposits increased by 26 billion VND.

VND, up 98.58% compared to the beginning of the year, reaching VND52 billion. Residential deposits increased 22.54% compared to the beginning of the year, reaching VND244 billion. Total mobilized capital as of June 30, 2011 was VND296 billion, an increase of VND71 billion, equal to 31% compared to the end of 2010.

Figure 2.6: Capital structure table

The structure of economic organization and individual deposits is 82:18. Economic organization deposits increased by 26 billion VND (100% increase) compared to 2010. Individual deposits increased by 45 billion VND (23% increase) compared to the end of 2010. The branch's capital mobilization grew rapidly and steadily in the first 6 months of 2011: 9.22% were non-term deposits, 37.19% were 1-month term deposits, 23.88% were 2-month term deposits, 29.71% were terms from 3-36 months. The mobilized capital source depends largely on 3 individuals, one organization with a balance accounting for 40% of the total mobilized capital balance of the branch. Mobilizing capital from the population in the first quarter of 2011 increased by 63 billion compared to December 31, 2010. However, in the second quarter of 2011, the branch only increased by 11 billion VND compared to the first quarter of 2008. Mobilizing capital from the population in the second quarter of 2011 grew slowly because commercial banks and credit funds competed to increase interest rates, causing customers to withdraw their deposits from one bank to another. However, this is a very encouraging result because in the current period of fluctuating interest rates, maintaining and developing the source of mobilizing capital from the population is a very difficult task.

2.3.6.3 Customer loans

Item

Year 2008 | Year 2009 | Year 2010 | 6 months 2011 | |

Customer Loans | 28,159 | 115,351 | 126,740 | 143,326 |

- Classify by customer group | 28,159 | 115,351 | 126,740 | 143,326 |

Personal Loans | 12,747 | 65,039 | 73,243 | 58,750 |

Business Loans | 15,412 | 50,312 | 53,497 | 84,576 |

Other loans | - | - | - | - |

- Classification by debt group | 28,159 | 115,351 | 126,740 | 143,326 |

Debt type 1 | 27,429 | 105,883 | 122,165 | 129,636 |

Debt type 2 | 730 | 8,478 | 2,776 | 11,609 |

Debt type 3 | - | 990 | 1,050 | 711 |

Debt type 4 | - | - | 679 | 1,288 |

Debt type 5 | - | - | 70 | 82 |

- VND | 28,159 | 115,351 | 126,740 | 143,326 |

Short term | 25,804 | 69,861 | 78,212 | 109,292 |

Medium and long term | 2,355 | 45,490 | 48,528 | 34,034 |

- Foreign currency | - | - | - | - |

Growth rate | Year 2008 | Year 2009 | Year 2010 | 6 months 2011 |

Customer Loans | 309.64% | 9.87% | 13.09% | |

- Classify by customer group | 0.00% | |||

Personal Loans | 0.00% | 410.23% | 12.61% | -19.79% |

Business Loans | 0.00% | 226.45% | 6.33% | 58.09% |

Other loans | 0.00% | 0.00% | 0.00% | 0.00% |

- Debt ratio 3-5 | 0.00% | 0.86% | 1.42% | 1.45% |

Debt Ratio Type 2 | 7.35% | 2.19% | 8.10% | |

- VND loan ratio, of which | 100.00% | 100.00% | 100.00% | 100.00% |

Short term | 60.56% | 61.71% | 76.25% | |

Medium and long term | 39.44% | 38.29% | 23.75% | |

- Foreign currency lending ratio | 0.00% | 0.00% | 0.00% | 0.00% |

Figure 2.7: Credit balance table

In 2010, total outstanding debt reached 127 billion VND, equal to 9.87% compared to 2009, equal to 350% compared to 2008. In the first 6 months of 2011, total outstanding debt was 143 billion VND, an increase of 13.06% compared to 2010.

Regarding the implementation of ratios and structures: Correctly implementing the assigned credit structure targets: Non-state outstanding debt/Total outstanding debt is 100%, meaning only lending to private enterprises. Medium and long-term outstanding debt/Total outstanding debt was 48.53% in 2010, but in the first 6 months of 2011 it decreased to 34%. The implementation of the outstanding debt ratio