18

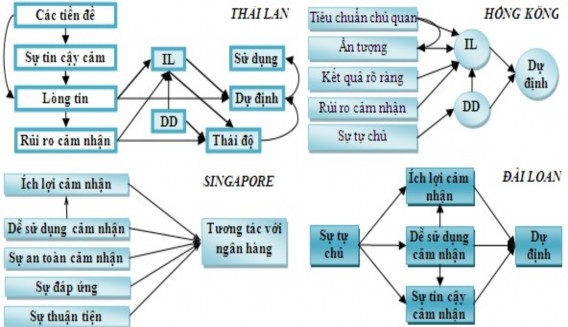

Content and research results from technology acceptance models in some countries.

Country

family

Author | Model | Research content | Research results | |

Thai L safe | Bussakorn Jaruwachiratha nak ul, Dieter Fink | Original TPB | IB approach - strategy for a developing country | - Incentive factors: perceived usefulness and features of the website - Obstructive factors: external environment. |

Malaysia ia | Petrus Guriting, Nelson Oly Ndubisi | Extended TAM, adding two variables: computer confidence and experience | Assessing customer intentions and acceptance of IB services | - Perceived usefulness and ease of use are the two most important factors. - Confidence directly and indirectly influences behavioral intention through usefulness and ease of use. - Computer experience factor has no influence. |

Finland | Heikki Kajaluoto, Minna Mattila, Tapio Pento | Original TPB | Factors influencing IB attitudes and acceptance | - Computer experience, banking experience and attitude strongly influence intention. - Demographic variables influencing intention - Group |

Maybe you are interested!

-

History of Formation and Development of Thanh Hoa Province

History of Formation and Development of Thanh Hoa Province -

Brief History of the Formation and Development of Accounting Information System in Vietnam

Brief History of the Formation and Development of Accounting Information System in Vietnam -

History of Formation and Development of Agricultural Tourism

History of Formation and Development of Agricultural Tourism -

Overview of the History of Formation and Development of Vietnam Joint Stock Commercial Bank for Foreign Trade

Overview of the History of Formation and Development of Vietnam Joint Stock Commercial Bank for Foreign Trade -

History of Formation and Development of Vietnam Joint Stock Commercial Bank for Industry and Trade

History of Formation and Development of Vietnam Joint Stock Commercial Bank for Industry and Trade

19

References have no effect. | ||||

Radio L injustice | Yi-Shun Wang, Yu-Min Wang, Hsin-Hui Lin, Tzung –I Tang | Open TAM expanded, adding two variables: computer confidence and trust. | Factors determining IB service acceptance | - Ease of use, perceived usefulness and perceived trust directly influence intention. - Self-confidence indirectly affects intention through the above three variables. |

Newze- land | Praja Podder | Open TAM wide, adding two variables: confidence and risk | Intention and habit of using IB services | - Ease of use, perceived usefulness and confidence influence intention to use. - The reliability variable has no influence |

Estonia | Kent Ericksson, katri Kerem, Daniel Nilsson | Open TAM wide, adding 1 variable is risky | IB service acceptance in Estonia | Perceived ease of use, perceived usefulness, and perceived trust directly influence intention. |

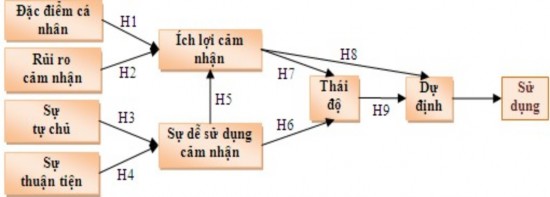

TAM applied theoretical model (researched in Vietnam)

Figure 1.4: Research model of electronic banking in Vietnam

(Source: Huy and Anh, 2008)

In there:

Personal characteristics are related to perceived benefits (H1) . In the context of inequality in educational levels, especially in the IT sector of Vietnam, it is necessary to study the role of personal characteristics variables (income, age, gender).

Perceived risk is related to perceived benefit (H2), which is considered the uncertainty that customers face when they cannot measure the consequences of their usage decision.

20

Customers are influenced by the risks they perceive, whether or not they exist. Hewer and Howcroft (1999) and Howcroft et al. (2002) argue that although customers trust their banks, they have little trust in technology. In the context of Vietnam (limited technical skills, information security and electronic transaction laws, and a fear of contact with machines), this is a major obstacle to the development of e-commerce in general and the transition of business forms from traditional banking to e-banking in particular.

Autonomy is the ability of an individual to use a computer (Compeau and Higgins, 1995) and is related to perceived ease of use (H3) (Venkatesh and Davis, 1996; Igbaria and Iivari, 1995; Venkatesh, 2000; Agarwal et al., 2000). According to O'Cass and Fenech (2003), when users have enough experience with technology, they will have confidence in their ability to use the system. Vietnam's technological level is nearly half a century behind that of developed industrial countries, which partly explains the lack of technological autonomy of a large part of the Vietnamese people. Therefore, autonomy plays an important role in measuring the level of acceptance of e-banking in Vietnam, people with high computer autonomy will be more likely to use the system.

Convenience is related to perceived ease of use (H4), which is the customer's comfort with logging in/out of the system, transaction location, transaction time... Dennis and Papamatthaiou's (2003) study on online shopping motivations has shown that convenience is closely correlated with online transaction intention and convenience is also positively related to the use of online banking (Polatoglu and Ekin, 2001; Gerard and Cunningham, 2003). With the current state of unsynchronized infrastructure in Vietnam, this will be a factor that strongly affects perceived ease of use.

Perceived ease of use is related to perceived utility (H5) (Davis, 1989). These are two belief variables in the original TAM model. Users feel that the system is useful when it makes transactions faster, is easy to use, improves efficiency, etc. On the other hand, customers will not feel that the system is useful.

21

benefits that e-banking brings if they do not find the system easy to use.

Attitude is related to perceived ease of use (H6) and perceived benefit (H7). Accordingly, individuals will intend to use the system when they have a positive attitude and conversely will not accept the system when they have a negative attitude towards its use (Davis et al., 1989).

Intention is related to perceived benefits (H8) and attitude (H9). Individuals have intention towards a behavior when they believe it will improve their work performance. This improvement brings different benefits and affects the behavior (Davis et al., 1989). Perceived benefits are also one of the strongest variables influencing intention to use (Venkatesh and Davis, 2000).

1.2.3 Proposed model of the study:

The study uses the extended TAM model, adding a motivational variable according to the TPB model, which is social influence: the level of influence from the attitudes of relevant people on the customer's decision to use. In the proposed research model, external variables related to perceived benefits include: work, compatibility, usefulness, risk reduction; external variables related to perceived ease of use include: access and flexibility. In addition, according to the reference of some banking experts, the study also added a factor affecting the customer's decision to use, which is the cost factor. Customers decide to use Internet Banking services because it saves a lot of time and travel costs because customers do not have to go directly to the bank or service providers to pay bills for goods, electricity, water, insurance premiums, etc.

22

Decision to use

Job

Flexibility

Social impact

Usefulness

Approach

Reduce risk

Compatibility

Expense

Figure 1.5: Research model of factors influencing the decision to use Internet Banking of individual customers at VCB HCM

In summary, the model proposes 8 factors influencing individual customers' decision to use Internet Banking, including: work, social influence, access, compatibility, flexibility, usefulness, risk reduction, and cost. In which:

Work has a relationship with the customer's decision to use Internet Banking. If the customer's work mainly involves transactions via the Internet, the need to make payment transactions quickly and promptly is inevitable. On the other hand, if the customer's workplace is not near the bank and the customer feels that going to the bank to make transactions takes a lot of time, the customer will choose to use Internet Banking transactions.

Social influence has a relationship with the decision to use Internet Banking of customers. The stronger the attitude of the people involved and the closer the relationship with those people involved, the more influenced the consumer's purchasing tendency is (Fishbein and Ajzen, 1975). Customers use Internet Banking because they listen to the recommendations of relatives, friends, colleagues or they use it because they see people around them also use it to fit the general trend of the times.

Access is related to the customer's decision to use Internet Banking. Customers will use the service if they know about the service's benefits because the service is widely advertised. Customers feel comfortable using the service if the service is guided clearly and easily, and the program's transaction operations such as logging in/out, payment, transfer... are performed easily and quickly.

23

Compatibility has a relationship with the customer's decision to use Internet Banking. Internet Banking service has a more limited customer base than other banking services because customers are those who have knowledge about accessing the Internet. Customers will use Internet Banking because they find it suitable for their current status, lifestyle and interests.

Flexibility is related to the decision to use Internet Banking of customers. Customers use Internet Banking because they can make transactions with the bank anywhere, anytime as long as they can access the Internet. Customers do not need to go directly to service providers to pay bills, pay insurance premiums, etc. Customers also do not need to go to the bank to wait for their turn to make a transaction, but customers can flexibly make any transaction they want on the Internet Banking program.

Usefulness is related to the customer's decision to use Internet Banking. Customers will use the service if they feel the service is useful such as: diverse services that meet the customer's needs, transactions are easy and fast. Through Internet Banking service, customers can actively control their finances effectively.

Reducing risk is related to the decision to use Internet Banking of customers. Nowadays, criminal activities are increasing in all fields, so the need to ensure the safety of assets and lives is always a top priority for customers. Transactions via Internet Banking will ensure more safety for customers because customers do not need to carry cash when paying partners and customers are guaranteed confidentiality of information when making transactions.

Cost is related to the decision of customers to use Internet Banking. Customers make transactions via Internet Banking because they save a lot of time and costs when making transactions because they do not need to go directly to the bank or service providers to pay or perform financial services, securities, etc.

24

Chapter 1 Conclusion

In this chapter, the thesis has presented the theoretical basis of Internet Banking services including the concept, levels of Internet Banking, important factors for developing Internet Banking, benefits, risks in the process of developing and using Internet Banking services. This chapter has also presented the theoretical basis of the research model of factors affecting the decision to use Internet Banking of individual customers at VCB HCM, thereby proposing a research model and some factors affecting the decision to use Internet Banking of individual customers at VCB HCM.

Next, Chapter 2 will present the current situation of Internet Banking usage in Vietnam in general and at VCB HCM in particular. Thereby, it will point out the advantages and disadvantages in providing Internet Banking services at VCB HCM. At the same time, it will conduct a survey and examine the factors affecting the decision to use Internet Banking of individual customers at VCB HCM. From there, it will assess the level of influence of these factors on the decision to use Internet Banking services of customers.

25

CHAPTER 2:

LETTER ON FACTORS AFFECTING THE DECISION TO USE INTERNET BANKING OF INDIVIDUAL CUSTOMERS AT JOINT STOCK COMMERCIAL BANK FOR FOREIGN TRADE OF VIETNAM

HCM CITY BRANCH

2.1 General introduction to VCB HCM

2.1.1 Brief history of formation, development, and position of VCB HCM in the system and in the area

Joint Stock Commercial Bank for Foreign Trade of Vietnam, Ho Chi Minh City Branch was established under Decision No. 951/NH-QD of the General Director of the Bank for Foreign Trade of Vietnam on November 1, 1976. After 36 years of construction and growth, VCB HCM has made outstanding progress in the cause of economic construction and development.

- the society of Ho Chi Minh City in particular and the whole country in general. Throughout that journey, generations of officers and employees of VCB HCM have overcome all difficulties and challenges, united, united, dynamic and creative, ready to receive and complete assigned tasks, building and developing a strong, modern and civilized bank.

As of December 31, 2012, there were 1,400 employees, 24 functional departments, and 20 transaction offices. VCB HCM organizational chart (see Appendix 2A).

Located in the area with the most dynamic economic market in the country, VCB HCM welcomes many opportunities as well as faces many difficulties and challenges in the process of developing the city's economy and the process of international economic integration. In fact, over the past many years, VCB HCM has faced fierce competition from domestic and foreign banks. With its position as a large state-owned commercial bank that has been equitized, holding a high market share in the area, especially playing a leading role in international payment activities, foreign currency trading, card payment, capital trading... the branch has always been considered a counterweight to other commercial banks.