SERVPERF has certain advantages, customer satisfaction studies

Customers often use the SERVQUAL model.

The SERVPERF scale aims to measure the perception of service through 5 components of service quality. For each type of service and each different research nature, the number of observed variables is also different, including 21 observed variables shown in the table below:

Table 2: SERVPERF scale

Ingredient

Observation variable | |

1. Reliability: demonstrates the ability to perform services appropriately and on time the first time | 1. XYZ Company promises to do something by a specified time. and XYZ will perform. |

2. When you have a problem, XYZ company can show concern and sincerity in solving that problem for you. | |

3. XYZ Company performs the service correctly. right the first time | |

4. XYZ Company provides the right service. at the time they promised to do so. | |

5. XYZ Company informs customers when services will be performed. | |

2. Responsiveness: shows the willingness of service staff to provide timely service. time for customers | 6. XYZ company employees serve you quickly and on time. |

7. XYZ company employees are always ready to help you. | |

8. Employees of XYZ company are never too busy to respond. meet your requirements. | |

3. Service capacity (assurance): demonstrates professional level and manner | 9. The behavior of XYZ company's employees increasingly creates trust in you. |

Maybe you are interested!

-

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks

Current Status of Credit Quality at Vietnamese Joint Stock Commercial Banks -

Research on the relationship between social responsibility, brand value and financial performance of joint stock commercial banks in the Mekong Delta - 24

Research on the relationship between social responsibility, brand value and financial performance of joint stock commercial banks in the Mekong Delta - 24 -

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9 -

Evaluation of Electricity Bill Collection Service Quality at Vietnam Technological and Commercial Joint Stock Bank - Hue Branch

Evaluation of Electricity Bill Collection Service Quality at Vietnam Technological and Commercial Joint Stock Bank - Hue Branch -

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31

Improving credit quality at Vietnamese joint stock commercial banks 1669220937 - 31

serve guests politely and warmly

row.

10. You feel safe when doing business with XYZ company. | |

11. Employees of XYZ company are always polite and courteous to you. | |

12. XYZ company employees have the knowledge to answer your questions. | |

4. Empathy: Showing concern and care for each individual customer. | 13. XYZ Company shows interest to you personally. |

14. XYZ Company has employees who show personal interest in you. | |

15. XYZ Company shows special attention to your concerns. | |

16. Employees of XYZ company understand your special needs. | |

5. Tangibles: expressed through the appearance and uniform of service staff, infrastructure and equipment to perform the service. service. | 17. XYZ Company has modern equipment. grand. |

18. The facilities of XYZ company look very attractive. | |

19. Employees of XYZ company are neatly and politely dressed. | |

20. Material means in activities very attractive service at XYZ. | |

21. XYZ Company has convenient trading hours. |

(Source: Cronin & Taylor, 1992)

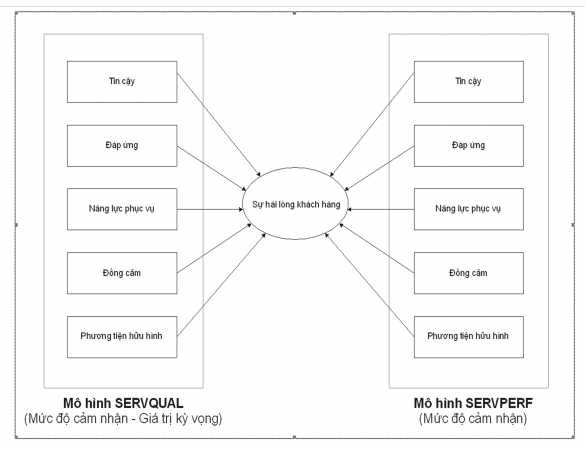

1.1.1.5. The relationship between service quality and customer satisfaction:

The relationship between service quality and customer satisfaction has been a topic of constant discussion among researchers over the past decades. Many studies on customer satisfaction in the service industry have been conducted. Some authors argue that there is a overlap between service quality and customer satisfaction and therefore the two concepts can be used interchangeably.

Service quality and satisfaction are two different concepts but are closely related in service research (Parasuraman et al. 1988). Previous studies have shown that service quality is the cause of satisfaction (Cronin and Taylor, 1992; Spreng and Taylor, 1996). The reason is that service quality is related to service delivery, while satisfaction can only be assessed after using the service.

Customer satisfaction is seen as a result, service quality is seen as a cause, satisfaction is predictive, expected; service quality is an ideal standard. Customer satisfaction is a general concept, expressing their satisfaction when consuming a service. Meanwhile, service quality only focuses on specific components of the service (Zeithaml & Bitner, 2000). Although there is a relationship between service quality and satisfaction, few studies have focused on testing the level of explanation of service quality components for satisfaction, especially for each specific service industry (Lassar et al., 2000). Cronin and Taylor tested this relationship and concluded that perceived service quality leads to customer satisfaction. Studies have concluded that service quality is an antecedent of satisfaction (Cronin and Taylor, 1992; Spereng, 1996) and a major factor influencing satisfaction (Ruyter, Bloemer, 1997).

In short, service quality is a factor that greatly affects customer satisfaction. If a service provider provides customers with quality products that satisfy their needs, that network has initially made customers satisfied.

customer satisfaction. Therefore, to improve customer satisfaction, service providers

must improve service quality.

In other words, service quality and customer satisfaction are closely related, in which service quality is the first thing that determines customer satisfaction. The causal relationship between these two factors is the key issue in most customer satisfaction studies. If quality is improved but not based on customer needs, customers will never be satisfied with that service. Therefore, when using a service, if customers feel that the service is of high quality, they will be satisfied with that service. Conversely, if customers feel that the service is of low quality, dissatisfaction will arise.

Figure 3: Research model of the relationship between service quality and

satisfaction

1.1.2. Consumer lending and contents related to consumer lending activities of commercial banks:

Concept of consumer lending: Consumer lending is a form of credit in which the bank agrees to let individual or household customers use a sum of money for consumption purposes with the principle of repaying both principal and interest within a certain period of time.

Classification of consumer lending activities:

Classification by income:

- Low-income earners: The credit needs of this group are often limited because their income is not enough to satisfy their diverse needs. However, their spending needs are not much different from those of higher-income earners. Therefore, if there is a suitable method, it is also possible to form reasonable loans for this group.

- Middle-income individuals: Credit demand tends to grow more and more strongly because although this group's savings are small, their future income is stable and can cover current needs.

- High-income individuals: These people often need loans as flexible supplements, helping to supplement special payments when their money is invested in long-term investments. Although their consumer loans only represent a small proportion of their total assets, they are a large amount of money compared to other customer groups, so banks are very interested in this group of customers.

Classification by working status:

Individual consumption needs also depend a lot on the nature of work and occupation. In this aspect, we have the following customer groups:

- Officials and civil servants.

- People who do their own business.

- Professionals (Doctors, singers, consultants...).

- Freelancers.

In fact, customers in the first three customer groups have higher and more stable incomes than the last customer group, so the demand for consumer loans mainly arises from the above three groups.

Consumer loan features:

- Small loan size but large number of loans

- Consumer loans with “hard” interest rates

- Consumer loans are often high risk.

- Consumer loans have quite large costs.

Consumer loan classification:

Based on loan purpose:

- Residential consumer loans: Loans to finance the needs of purchasing, building or renovating houses for customers who are individuals and households.

- Non-residential consumer loans: Loans to finance expenses such as purchasing vehicles, household appliances, education, entertainment, travel, etc.

Based on the payment method:

- Installment consumer loans: This is a form of loan in which the borrower repays the debt (including principal and interest) to the bank many times, according to certain terms within the loan term. This method is often applied to large loans or the borrower's income each period is not enough to pay off the loan in full at once.

- Non-installment consumer loans: This is a form of loan in which the loan is paid by the customer only once when due. Usually, non-installment consumer loans are granted for small borrowing needs and short terms.

- Revolving consumer loan: Is a loan in which the bank allows the customer to use a credit card or the bank issues a type of check that allows overdraft based on the amount in the current account. According to this method, within the pre-agreed credit period, based on spending needs and income earned each period, the customer is allowed by the bank to borrow and repay the debt in many periodic installments, according to a credit limit.

Based on the origin of the debt:

- Indirect consumer lending: Is a form of lending in which banks purchase debts incurred by retail companies that have sold goods or services to consumers on credit.

- Direct consumer loans: These are consumer loans in which the bank directly contacts and lends to customers as well as directly collects debts from these people.

Personal consumer loan process:

The personal consumer loan process will start from the time the credit officer receives the loan application until the time of final settlement and liquidation of the credit contract. The loan process will have the following 6 basic steps:

Step 1: Receive loan application.

Step 2: Assess personal loan conditions.

Step 3: Credit analysis.

Step 4: Approval for personal consumer loans.

Step 5: Sign contract and disburse.

Step 6: Collect debt and issue new credit judgment.

The role of consumer lending:

From the consumer perspective:

- Consumer lending solves the conflict between the consumer's current consumption needs and the ability to accumulate to meet that need. Customers have a need to consume a product or service at the present time, but their savings are not enough to cover the cost of satisfying that need. Consumer lending solves that problem for customers, helping them to immediately solve their current consumption needs without having to wait.

- Consumer loans help improve people's lives, help them have a comfortable and fulfilling life, and improve their quality of life.

From the perspective of Commercial Banks:

- Consumer lending helps banks expand their relationships with customers. That is the basis for banks to provide more products and services, increasing the bank's income. As we know, when a customer has used a product of a bank, if they are satisfied, they can completely continue to use other products and services of that bank when they have a need. Consumer lending customers are often large in number, so the ability to expand the bank's customer base is very high. Implementing consumer lending well will help banks gain more customers, not only in the field of consumer credit but also in other products and services such as capital mobilization, international payment, guarantee, etc.

- Consumer lending helps banks diversify their business activities, thereby

can increase income and diversify risk for banks.

In terms of Socio-Economic aspects:

- Consumer lending plays an important role in stimulating demand, that is, increasing people's spending, and increasing the demand for goods and services for daily life. When consumer demand increases, it will stimulate production development, thereby contributing to promoting economic development.