issued, an increase of more than 20% compared to the number of 2012. VCB-HCM alone issued more than 400 thousand cards of all kinds last year, about 1.3 times higher than the planned target. Card usage and payment sales both grew very strongly. Of which, international payment card sales increased by 26.1% compared to the end of 2012, domestic card payment sales increased by 73.5% compared to the same period. Currently, the number of customers paying salaries via ATM system at the Ho Chi Minh City branch is more than 400 units, so on the last payday of the month, the amount of money withdrawn is about 20-22 billion VND/day. During the holidays, this number can reach 30 billion VND/day. Despite having the largest ATM network in the country, Vietcombank still cannot avoid overloading some ATMs.

Electronic banking services

Over the years, Vietcombank has always been at the forefront of developing advanced technology, providing modern, multi-utility banking services according to international standards, so that customers can use Vietcombank's services anytime, anywhere such as Connect 24 card, VCB-iB@nking, SMS-Banking... Customers can pay for electricity, phone, ADSL, tuition, air tickets, insurance fees... easily and conveniently.

In 2013, Vietcombank was the first bank to charge ATM withdrawal fees within its network. And from mid-January 2014, Vietcombank also took the lead in charging a fee of VND3,300 for money transfers to individuals or organizations within the same system via the VCB-iB@nking channel instead of being free as before. However, with diverse utilities and continuous efforts to improve the quality of e-banking services, Vietcombank brings customers the experience of a "bank where you want".

* In general, the results show that both Vietcombank and the HCM branch have constantly strived to perform their best to build their image and reputation in the market. Vietcombank's services are associated with high-tech applications that are superior in features, diversity and convenience. The Ho Chi Minh branch has always been at the forefront of successfully piloting many new services. The service promotion campaign through media channels, sponsorship activities, posters, brochures, etc. is carried out more and more carefully.

increasingly, promoting efficiency. The advantages that the branch has must be mentioned that the income and living standards of the people have increased, so the demand for using banking services has increased and become more diverse. The policy of promoting retail banking activities is consistent throughout the unit, with close coordination between the headquarters and the branch in implementing the orientation. The image and position that Vietcombank has built over the past time has increasingly strengthened the trust of customers, helping them feel secure in using the service and not hesitate to introduce new customers to the Branch.

However, in addition to the above advantages, the Branch still faces many difficulties and limitations. Due to economic difficulties, customers rarely use loans. Monetary policies change frequently, affecting customers as well as the balance and use of capital of the bank. Moreover, competition between banks is increasingly fierce to gain market share, especially the trend of increasingly strong development of retail banking activities.

2.3 Measuring individual customer satisfaction with service quality of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Ho Chi Minh Branch through customer survey

2.3.1 Research methods

Based on the theory of service quality, customer satisfaction and research models as presented in chapter 1, the author uses qualitative, quantitative, descriptive, regression analysis methods... to evaluate the level of satisfaction with the quality of personal customer service of VCB-HCM through customer surveys and proposes some solutions to improve the service quality of VCB-HCM. The research process is presented specifically as follows:

2.3.1.1 Research survey process

During the research process, the author used two data sources: primary data (results of discussions with bank employees to better understand their opinions and assessments of the research topic, and customer opinion polls) and secondary data (references from theses on service quality, articles, banking magazines, from banks' performance reports, from the Internet...)

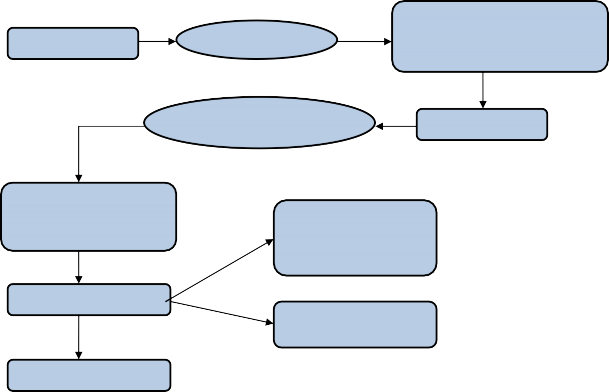

Theoretical basis of Draft scale

Qualitative research

- Discuss

- Mock interview

Formal research

Adjust

Survey method

-Questionnaire design

-Data collection

-Reliability analysis

-Factor analysis

-Regression analysis

Quantitative research

-Hypothesis testing

-Research results

Conclusion and recommendations

Figure 2.7: Research survey process

2.3.1.2 Qualitative research

This is a preliminary research step to screen variables and build a questionnaire for data collection. Based on the contributions of colleagues and 10 random customers in the form of group discussions to record their initial opinions on customer service quality, and using additional documents and books from many sources, the author has considered the limitations, whether the questions are suitable for the actual situation at VCB-HCM or not and completed the official survey questionnaire for customers.

Finally, the official scale was surveyed including 6 factors affecting satisfaction with individual customer service quality with 26 variables and 3 additional scales for measuring the overall customer satisfaction level to serve the next quantitative research. Specifically:

- Tangibility component: 4 variables

- Trust components: 5 variables

- Service efficiency components: 4 variables

- Guarantee components: 4 variables

- Empathy components: 3 variables

- Corporate image components: 6 variables

2.3.1.3 Quantitative research

This is the step of re-examining the scales in the model to determine the suitability and correlation of the factors with each other and from there give specific results. After building the questionnaire, the author determines the number of samples needed for the study and sends out the survey form. The data collected from the customer survey will be processed with SPSS software for analysis.

Information collected from the survey questionnaire was sent to individual customers of VCB–HCM during the period from March to April 2014 by sending directly to individual customers through the transaction counter and asking staff to send it on their behalf.

According to many researchers, the representativeness of the number of samples for the survey will be appropriate if the sample size is 5 for an estimate. In his research model, the author proposed 29 questions (26 variables to evaluate service quality and 3 variables on general satisfaction), so the minimum number of samples needed for the study will be 145 samples (n = 29 * 5 = 145). After nearly two months of distributing 200 survey forms to customers, the author received 185 forms but only 175 were valid with full information. The official number of observation samples is 175 representative samples to ensure the implementation of the study (n>145).

One of the most commonly used measurement forms in quantitative research is the scale introduced by Rennis Likert (1932) with 5 levels from 1 to 5, which was included in this study for customers to evaluate according to their own opinions with levels from completely disagree to completely agree about the quality of service for individual customers of VCB–HCM.

The quantitative research process begins with coding the observed variables for processing in SPSS 20.0 software specifically as follows:

Table 2.3 Summary table of coding of scales

STT

Encryption | Interpretation | |

Tangibility component | ||

1 | HH1 | The bank has modern machinery and equipment (machinery, transaction software) translation, internet services…) |

2 | HH2 | The bank's facilities are spacious and comfortable (headquarters, transaction counters, waiting chairs, parking space, etc.) |

3 | HH3 | Bank staff dressed formally |

4 | HH4 | The bank has branches, transaction offices, ATMs widely, and convenient transaction locations. |

Trust Components | ||

5 | NEWS1 | The bank focuses on not making any errors or mistakes in the transaction process. |

6 | TIN2 | Staff satisfactorily resolve customer complaints |

7 | TIN3 | The bank performs the service correctly the first time. |

8 | TIN4 | The bank provided service on time as promised. |

9 | TIN5 | The bank 's storage reporting system always keeps customer account and transaction information confidential. |

Effective ingredients serve | ||

10 | HQPV1 | Staff answer all customer questions accurately and clearly |

11 | HQPV2 | Staff are polite, attentive and always respectful of customers. |

12 | HQPV3 | Staff process transactions quickly and proficiently, without keeping customers waiting long. |

13 | HQPV4 | Staff are always ready to serve and welcome customers very enthusiastically. |

Components of the guarantee | ||

14 | BDAM1 | ATMs, card machines, etc. operate stably and safely. |

5 | BDAM2 | Do you feel confident in bank employees? |

16 | BDAM3 | Knowledgeable staff to meet customer needs |

17 | BDAM4 | Bank transaction documents are accurate, clear and easy to understand. |

Components of empathy | ||

18 | CAM1 | Banks have programs that show concern for customers. |

19 | CAM2 | Business hours are very convenient for customers to transact |

20 | CAM3 | Staff understand customer needs |

Corporate image components | ||

21 | HADN1 | The bank has very effective and impressive marketing activities. |

Maybe you are interested!

-

Analyze and propose solutions to improve individual customer satisfaction with lending services of Global Petroleum Joint Stock Commercial Bank GP. Bank, Vung Tau branch - 2

Analyze and propose solutions to improve individual customer satisfaction with lending services of Global Petroleum Joint Stock Commercial Bank GP. Bank, Vung Tau branch - 2 -

Measuring the level of satisfaction of individual customers with ATM card services at Vietnam Joint Stock Commercial Bank for Investment and Development, Tay Nam Branch - 1

Measuring the level of satisfaction of individual customers with ATM card services at Vietnam Joint Stock Commercial Bank for Investment and Development, Tay Nam Branch - 1 -

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3 -

Assessing the level of satisfaction of individual customers with savings deposit services at Saigon Commercial Joint Stock Bank SCB - Ninh Kieu Branch - 13

Assessing the level of satisfaction of individual customers with savings deposit services at Saigon Commercial Joint Stock Bank SCB - Ninh Kieu Branch - 13 -

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

22

HADN2 | The bank always puts the interests of customers first. | |

23 | HADN3 | The bank is always at the forefront of innovations to make a difference. |

24 | HADN4 | Bank with sustainable development strategy |

25 | HADN5 | The bank is always interested in social activities. |

26 | HADN6 | The bank always keeps its word with customers. |

Components of satisfaction | ||

27 | HL1 | I am completely satisfied with the quality of service of the bank. |

28 | HL2 | Would you be willing to recommend the bank's services to others? |

29 | HL3 | In the future, you will continue to use the bank's services. |

In addition to the main part including questions for customers to evaluate the components of service quality and their satisfaction at VCB–HCM, the author also provided 5 more questions to find out some information about individual customers using the service including gender, age, education level, income, time of service use to statistically describe the sample being observed.

2.3.2 Research model and assumptions

2.3.2.1 Research model

The SERVQUAL model is widely used in many fields such as health care services, retail services, supermarket services, banking services. This model still has some disadvantages such as focusing mainly on measuring and evaluating the supply process without paying attention to the implementation results, as well as not considering external factors or marketing activities but only focusing on the internal part. The FTSQ model can overcome these disadvantages because this model considers both functional quality and technical quality, that is, it considers both what services the bank provides and how the services are provided.

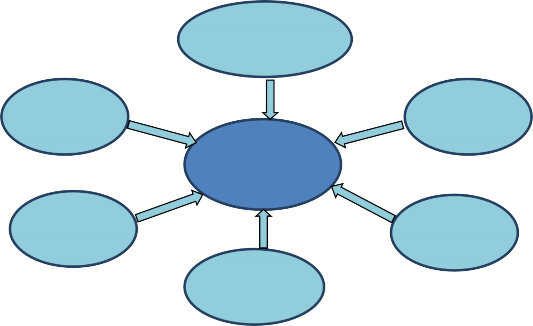

Based on the study of service characteristics and surveys on service quality models as well as the study of the relationship between service quality and customer satisfaction (as presented in sections 1.3 and 1.4), the author proposes an initial research model with components as described in Figure 2.8.

Corporate Image

Tangibility

SATISFACTION

Sympathy

Trust

Service efficiency

Guarantee

Figure 2.8 Research model of factors affecting satisfaction

The initial regression model has the form:

SHL = β 0 + β 1 HH + β 2 TIN + β 3 HQPV + β 4 BDAM + β 5 CAM + β 6 HADN + ε i

In there:

* SHL: Individual customer satisfaction with VCB's service quality-

HCM

* β 0 : Individual customer satisfaction with VCB's service quality-

HCM when other factors are 0.

* β i (i = 1.6): The slope coefficients of the regression equation.

* ε i : Remainder

* HH: Tangibility

* TRUST: Trust

* HQPV: Service efficiency

* BDAM: Guarantee

* ORANGE: Sympathy

* HADN: Corporate Image

2.3.2.2 Assumptions :

The assumptions made for the research model are as follows:

- H1: The higher the customer's assessment of tangibility, the higher the customer satisfaction and vice versa.

- H2: The higher the customer's rating of reliability, the higher the customer satisfaction and vice versa.

- H3: The higher the service efficiency for customers, the higher the customer satisfaction and vice versa.

- H4: The higher the bank's guarantee to customers, the higher the customer satisfaction and vice versa.

- H5: The higher the sympathy that the bank brings to customers, the higher the customer satisfaction and vice versa.

- H6: The higher the customer's rating of the business image, the higher the customer satisfaction and vice versa.

Table 2.4 Expected signs of variables in regression models

STT

Variable | Symbol | Expected sign | |

Dependent variable | |||

1 | Satisfaction | SHL | |

Independent variable | |||

2 | Trust | BELIEVE | + |

3 | Tangibility | HH | + |

4 | Service efficiency | HQPV | + |

5 | Guarantee | BDAM | + |

6 | Sympathy | ORANGE | + |

7 | Corporate Image | HADN | + |

2.3.3 Research results

2.3.3.1 Sample description:

The survey sample was randomly selected over a period of more than a month, so the characteristics of the sample were also random, and the dispersion of the sample was