CHAPTER 2: THEORETICAL BASIS

This chapter provides the theory of liquidity, the theory of liquidity risk management in commercial banks. Finally, it is an overview and system of domestic and foreign studies related to the research topic of liquidity risk.

2.1 OVERVIEW OF COMMERCIAL BANKS

2.1.1 Concept:

According to the French Banking Law of 1941, it is defined as: “Those enterprises or establishments which regularly receive from the public in the form of deposits or other forms of money which they use for themselves in operations, discount or finance are considered banks”.

Or as per the Indian Banking Act 1959 stated; “Bank is an establishment which accepts deposits for lending or financing or investment”.

And in Vietnam, in the Law on Credit Institutions No. 47/2010/QH 12 passed by the National Assembly on June 16, 2010, it is stated: "A commercial bank is a type of credit institution that can perform all banking activities and other related activities for the purpose of profit". This law also defines: "Banking activities are the business of regularly providing one or more of the following operations: receiving deposits, granting credit, providing payment services through accounts".

From the above comments, it can be seen that commercial banks are one of the financial institutions that are characterized by providing a variety of financial services with the basic business of receiving deposits, lending and providing payment services. In addition, commercial banks also provide many other services to satisfy the maximum demand for products and services of society.

2.1.2 Functions of commercial banks:

According to Le Trung Thanh (2002), commercial banks have three basic functions: credit intermediary function, payment intermediary function, and money creation function.

Credit intermediary function: Credit intermediary function is considered the most important function of commercial banks. When performing the function

As a credit intermediary, commercial banks act as a bridge between those who have excess capital and those who need capital. With this function, commercial banks act as both borrowers and lenders, and enjoy profits from the difference between deposit interest rates and lending interest rates, contributing to the benefits of all parties involved: depositors and borrowers... Lending is always the most important activity of commercial banks, it brings the greatest profits to commercial banks.

Payment intermediary function: Commercial banks provide customers with many convenient payment methods such as checks, payment orders, collection orders, cash cards, payment cards, credit cards, etc. Depending on their needs, customers can choose a suitable payment method. Thanks to that, economic entities do not have to keep money in their pockets, carry money to meet creditors, meet payers whether near or far, but they can use a method to make payments. Therefore, economic entities will save a lot of costs and time, while ensuring safe payments. This function has promoted the circulation of goods, accelerated payment speed, capital circulation speed, thereby contributing to economic development.

“Money creation” function: The money creation function is implemented on the basis of two other functions of commercial banks, which are the credit function and the payment function. Through the credit intermediary function, banks use the mobilized capital to lend, the loaned amount is used by customers to buy goods and pay for services, while the balance in the customer's payment deposit account is still considered a part of the transaction money, used by them to buy goods and pay for services... With this function, the commercial banking system has increased the total means of payment in the economy, meeting the payment and spending needs of society.

The functions of commercial banks are closely related, complementary and supportive to each other, in which the credit function is the most basic function, creating the basis for the implementation of the following functions. At the same time, when banks perform well the payment intermediary function and the money creation function, it contributes to increasing credit capital and expanding credit activities.

2.2 THEORY OF RISK

2.2.1 Concept of risk

Nguyen Thi Thu Hang (2009) believes that risk is the probability of encountering danger from any negative incident such as injury, theft... due to the impact of dangerous factors from inside or outside and this can be prevented and limited by prior planning. From a financial perspective, risk is defined as the probability that the actual profit earned from an initial investment is lower than expected.

Risks in banking business are understood as unexpected events that, when occurring, will lead to loss of bank assets, decrease in actual profits compared to expectations or have to spend additional costs to complete a certain financial transaction.

2.2.2 Types of risks in banking business

According to Nguyen Van Tien (2010) presented in the book Risk Management in Banking Business - Statistical Publishing House, it is said that:

- Credit risk: Credit risk arises when the bank does not collect the full principal and interest of the loan, or when the principal and interest are not paid on time.

- Exchange rate risk: Is the possibility of loss to the bank when the exchange rate changes beyond the bank's expectations.

- Interest rate risk: Is the possibility of loss for the bank when interest rates change unexpectedly (both asset and capital interest rates). Thus, this risk is a consequence of interest rate changes.

- Liquidity risk : Liquidity risk is the risk that occurs when a bank lacks funds or short-term assets that are viable to meet the needs of depositors and borrowers. In other words, liquidity risk occurs when a bank does not have enough reserves to meet customers' withdrawal needs.

2.2.3 Risk management in banking business

Trinh Hong Hanh (2015) believes that liquidity risk management is the use of a system of management mechanisms, business solutions and technology by commercial banks.

appropriate technical tools to maintain a constant balance between supply and demand for liquidity, promptly handle liquidity risk situations while still ensuring profitability for the bank. Risk management includes the following steps: Risk identification; Risk assessment; Preventive control; Risk financing.

2.3 THEORY OF LIQUIDITY AND LIQUIDITY RISK

Liquidity in financial markets has many meanings. Liquidity means the ability of a financial firm to maintain a balance between its financial inflows and outflows at the same time (Vento & Ganga, 2009).

According to the Basel Committee on Banking Supervision (Sep, 2008), for banks, liquidity means having enough assets to pay debts to meet financial obligations promptly when they come due within the acceptable loss range.

According to Duttweiler (2009), there are two different aspects of liquidity that need special attention, which are natural liquidity and artificial liquidity. In which liquidity means the flows originating from assets or liabilities but with a time limit prescribed by law. In the banking sector, when a transaction with a customer is often repeated, perhaps for the same amount or for a smaller or larger amount, this group of customers generally acts in a predictable manner. This is true not only for assets but also for liabilities. Artificial liquidity is created through the ability to convert assets into cash before the maturity date.

According to Truong Quang Thong (2012), liquidity is the ability to access assets and capital at a reasonable cost to serve the various operational needs of the bank. An asset has high liquidity when the cost of converting into cash is low and the conversion time into cash is fast. Meanwhile, capital has high liquidity when the cost of mobilization is low and the mobilization time is fast.

According to Truong Quang (2012), liquidity risk is a typical and common type of risk. Liquidity risk is the risk that a bank lacks the ability to pay, due to the inability to convert assets into cash, or the inability to mobilize and borrow to meet previously committed contracts.

According to Rudolf Duttweiler (2009), liquidity risk is the risk of not being able to fulfill payment obligations, and this inability to fulfill will lead to undesirable consequences.

Liquidity risk according to Basel Committee on Banking Supervision (1997) arises from the bank's inability to increase capital items to finance the increase in bank assets.

As Golin (2001) mentioned that the important thing for a bank manager to be concerned about is the liquidity risk, whether the bank has enough current assets such as cash or highly liquid securities, to meet its liquidity obligations to depositors, especially in times of economic crisis. Without the ability to pay, the bank may fail.

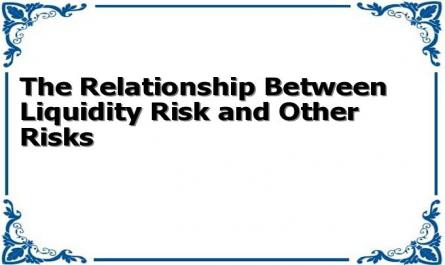

2.3.1 Relationship between liquidity risk and other risks

Liquidity risk is often a consequence of many other risks, so liquidity risk has many close relationships with each other.

Concentration risk

Reputational risk

Market risk

Operational risk

According to Gianfranco A.Vento (2009) the correlation of liquidity risk and credit risk, reputational impact on liquidity, and other links between bank liquidity and other typical features. Liquidity risk is not an "isolated risk" like credit, market risk (although credit risk often arises as a lack of liquidity when scheduled repayments are due).

Credit risk

Liquidity risk | |

Risk of the day | |

Maybe you are interested!

-

The Impact of Investor Protection Rights on the Relationship Between Liquidity and Firm Value

The Impact of Investor Protection Rights on the Relationship Between Liquidity and Firm Value -

The impact of liquidity risk on banking performance: a case study of Southeast Asian countries - 2

The impact of liquidity risk on banking performance: a case study of Southeast Asian countries - 2 -

Factors affecting liquidity risk of Vietnamese state-owned commercial banks - 10

Factors affecting liquidity risk of Vietnamese state-owned commercial banks - 10 -

Liquidity risk management of commercial banks of the State Bank of Vietnam - 1

Liquidity risk management of commercial banks of the State Bank of Vietnam - 1 -

The Relationship Between Risk Perception, Subjective Happiness and Tourists' Revisit Intention in Vietnam - A Case Study in Ho Chi Minh City - 39

The Relationship Between Risk Perception, Subjective Happiness and Tourists' Revisit Intention in Vietnam - A Case Study in Ho Chi Minh City - 39

Figure 2.1: Relationship between liquidity risk and other risks

Source: Gianfranco A.Vento (2009)

2.3.2 Causes of liquidity risk of commercial banks

According to Valla and Escorbiac (2006) liquidity risk can come from the liability or asset side, or from off-balance sheet activities.

According to Truong Quang Thong (2012) mentioned in the book Commercial Bank Management, there are three reasons why banks face liquidity risks:

Liquidity risk comes from the capital side of the balance sheet.

Banks lack funds to meet the needs of paying depositors, or repaying short-term debts that the bank has borrowed. In the capital structure of a commercial bank, there is usually a large proportion of short-term liabilities such as deposits on current accounts, short-term savings, interbank loans, of which a part is deposits on current accounts withdrawn by customers, the rest is considered as unsecured deposits, which are stable sources of funds that they can use for longer terms. Therefore, managers must know how to adjust net capital withdrawals.

Liquidity risk comes from the asset side of the balance sheet.

Banks must meet the disbursement needs for committed loans. Accordingly, banks must have money to disburse to borrowers when they want to withdraw capital according to the agreed demand and schedule, and thus give rise to liquidity demand.

Liquidity risk arises from lack of funds.

When the commercial bank's funds are low, it will have a significant impact on the bank's liquidity problem. Suppose that when an incident occurs such as customers borrowing too much or customers withdrawing money too much, if the bank has a strong charter capital, it will not be afraid of being affected when abnormalities occur, but for small banks, it will be difficult for them to handle it in time, and the problem of losing liquidity may occur.

2.4 LIQUIDITY RISK MANAGEMENT IN COMMERCIAL BANKS

2.4.1 The need for liquidity risk management

According to Samuel Siaw (2013) effective liquidity risk management will help ensure a bank’s ability to meet its cash flow obligations without the uncertainty that they are affected by external events and the actions of other actors. Dragos (2006) also explains the liquidity risk for a bank; is the probability of being unable to finance its transactions, or the probability that the bank cannot honor its day-to-day obligations to customers which include deposit withdrawals, maturity of other liabilities, and the need for additional funding for its loan and investment portfolio. According to Crowe (2009), a bank with good asset quality, strong earnings and adequate capital can still fail if it does not maintain adequate liquidity.

Therefore, liquidity risk management plays a very important role in the business activities of commercial banks for the following reasons:

The trade-off between liquidity and profitability

Bad debts and poor liquidity are two major causes of failure in banking operations, therefore liquidity has attracted great attention from researchers to examine its impact on bank profitability. Referring to previous research, the results related to liquidity such as Molyneux and Thorton (1992) found a negative and significant relationship between liquidity level and profitability. Therefore, ensuring reasonable liquidity is always important for the profitability of banking operations.

Liquidity risk makes banks insolvent

Serious liquidity problems can only arise when there are excessive and unplanned withdrawals of deposits. As withdrawals increase, so does the outflow of money from the bank. If cash balances are insufficient to meet withdrawal requests, the bank is forced to sell liquid securities such as bonds, treasury bills, or borrow in the money market. If withdrawals continue to increase, the bank will no longer be able to pay its bills.

If banks cannot borrow more in the money market, a liquidity crisis will occur, forcing them to sell assets regardless of price. This will put the bank at risk of insolvency.

Systemic liquidity risk

When a bank becomes insolvent and is forced to close, it can cause anxiety among customers of other banks. Customers fear that the bank where they have deposited their money may also go bankrupt, so they try to withdraw their money from that bank. If public confidence is shaken, in such a case, it can lead to a series of banks becoming insolvent in a short period of time and cause the banking system to fall into chaos. The chaos of the banking system can turn into a socio-economic and political crisis of a country.

2.4.2 Liquidity risk management strategy

According to Truong Quang Thong (2012), establishing and implementing liquidity risk management strategies must be based on carefully organizing the work of planning liquidity supply and demand; must aim at contingency solutions and coping in situations of imbalanced liquidity status.

Depending on conditions and operating characteristics, banks can choose the following liquidity management strategies:

Asset-Based Liquidity Management Strategy

Under this strategy, the bank will focus its management activities on short-term credit. The volume and duration of expected credit needs will be planned in accordance with the available monetary instruments.

With this strategy, banks will be more proactive in meeting credit needs without having to rely on other external entities. However, the asset-based strategy has disadvantages such as the trade-off between highly liquid assets but low profitability. In addition, selling or converting assets also causes risks when having to sell or convert assets with high transaction costs.

Liquidity management strategy based on debt items